Negative Returns for a Decade, Is Gold in a Bubble?

Stock-Markets / Stock Markets 2011 Mar 15, 2011 - 06:53 AM GMTBy: Mike_Shedlock

John Hussman is is once again exploring the topic of valuations and expected future returns. Please consider this snip from Anatomy of a Bubble

John Hussman is is once again exploring the topic of valuations and expected future returns. Please consider this snip from Anatomy of a Bubble

When valuations are reasonable, investors can expect satisfactory long-term returns simply on the basis of the stream of cash flows they receive over time. But once valuations are elevated, investors become increasingly reliant on pure increases in prices and valuations in order to achieve satisfactory returns. This is easily seen in historical data for the S&P 500.

The chart below is based on post-war U.S. data, and illustrates the interaction between valuation levels and valuation changes in producing long-term total returns for the S&P 500, and expands on some of Mike Shedlock's recent observations on valuations and prospective returns.

As I've frequently noted, Depression-era data is far more hostile than post-war data, as is data surrounding other historical and international credit crises, so investors would have needed more stringent valuation criteria in order to accept market risk during these periods. Still, post-war data is sufficient to convey some important ideas.

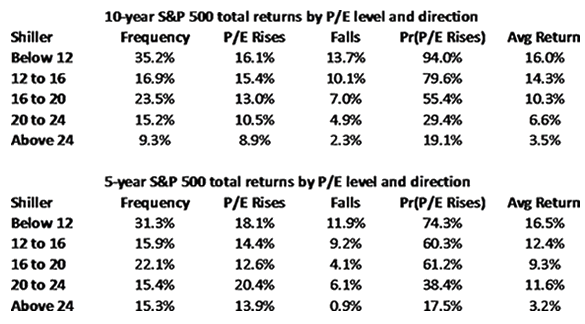

The first two columns below reflect the Shiller P/E (also known as the "cyclically adjusted" price/earnings ratio), and the frequency of various P/E ranges in historical data. The next two columns show the average annual total return of the S&P 500 Index, based on whether the Shiller P/E rose to a higher level during the 10- or 5-year horizon, or whether it fell to a lower level by the end of that horizon. The next column is the percentage of observations where the P/E was higher at the end of the horizon, and the last column is the weighted average return for each level of Shiller P/Es.

Notice that regardless of whether P/E ratios rose or fell during these investment periods, subsequent returns were substantially higher from low valuations than from high ones. Of course, subsequent returns were higher for horizons where the P/E increased than for those where the P/E fell.

Since data is available for 5-year returns through 2006, but only through 2001 for 10-year returns, the two tables cover slightly different horizons since 1940. Notably, the frequency of Shiller P/Es greater than 24 is 15.3% in 5-year data but only 9.3% in 10-year data. This is because extreme valuations have been the norm in recent years (where the P/E has exceeded 24 over half the time, interrupted only briefly by the recent plunge and rebound).

Presently, the Shiller P/E stands at 24. Be careful how you interpret the data in the table for Shiller P/E's above 24, since these levels were almost never observed in data prior to the late-1990's market bubble. You can see the odd effect of the bubble on the P/E categories above 20. The recent tendency for high valuations to move even higher over the short-term, coupled with the rapid recovery of much of the 2008-2009 loss, creates a "hump" in the 5-year profile - average returns first decline as valuations increase, and then actually improve for the 20-24 bracket. This is an artifact of recent years, and appears neither in pre-1995 data nor in 10-year return data.

The implication of this data for long-term returns is clear. With the Shiller P/E presently at 24, we observe about the same implications for 10-year S&P 500 total returns as we obtain from our broader valuation methods (expected total returns averaging about 3.5% annually). Still, the actual course of total returns will depend on whether valuations become even more extended over the next 5-10 years, or if they contract instead. Even if one includes data from the late-1990's bubble, the probability of rising P/E multiples from these levels is less than 1-in-5.

The post of mine John Hussman referred to is Negative Annualized Stock Market Returns for the Next 10 Years or Longer? It's Far More Likely Than You Think

Thanks John, I appreciate the mention.

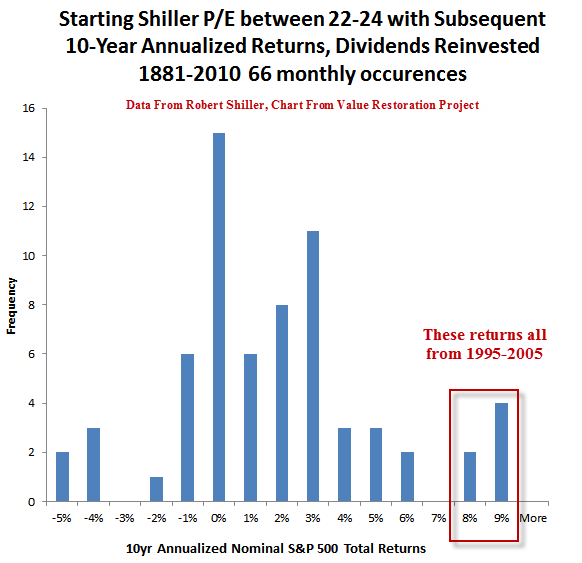

Here is another chart I would like everyone to consider.

The above chart was produced by an associate of mine, JJ Abodeely.

Please see his post Expensive Markets Mean Low or Negative Prospective Return for additional charts and commentary including a chart showing "real" inflation-adjusted returns.

Data for the charts is from Robert Shiller.

The chart above shows the frequency distribution of 10-year annualized gains (dividends reinvested) when the starting PE was in the range 22-24.

Frequency represents the number of occurrences, totaling 66 as opposed to a percentage that would total 100%.

There have been 66 monthly occurrences of PEs in the range 22-24 since 1881. The 10-Year annualized returns were only hugely positive a grand total of 6 of those 66 times, and all of those occurrences happened between 1995 and 2005.

This is what Hussman referred to when he said "Be careful how you interpret the data in the table for Shiller P/E's above 24, since these levels were almost never observed in data prior to the late-1990's market bubble."

There are 33 occurrences 1% and below, and 33 occurrences 2% and above. The average nominal annualized return is 1.2%

On that basis I think Hussman is likely a bit high with his estimate of 3.5% annualized returns for the next 10 years. However, rather than picking a precise number, I propose a range of -2% to +3%, with a skew to the downside for the next 5 years or so.

Meanwhile, pension plan assumptions are 7.5-8.5% everywhere you look. Odds of that are minuscule in my opinion.

Commodity Bubble

Let's return to Hussman for a look at the bubbles.

In the stock market, I believe that there is indeed a "bubble" component in current prices, but it is not nearly as large as we observed in the approach to the 2000 peak, nor as extreme as we observed on the approach to the 2007 peak. My hope is that investors have learned something. That's not entirely clear, but we'll be as flexible as we can while also being mindful of the risks.

While my view is that bubble components can come and go in the markets, they sometimes become so large and well-defined that they take on a very distinct profile. Such bubbles included the advance to the 2000 stock market peak, the housing bubble, the advance in oil prices to their peak in 2008, the advance in the Nikkei in the late 1980's, and other clearly parabolic advances.

On that note, it's clear to me that we're seeing classic bubbles in a variety of commodities. It is very unlikely that this is simply due to global demand growth. Even with an exhaustible resource, it is a well-known economic result (Hotelling's rule) that the optimal extraction rule is one where the price rises at a rate not much different from the interest rate. What we've seen lately is commodity hoarding, predictably resulting from negative real interest rates provoked by the Fed's policy of quantitative easing.

Fortunately for the world's poor, the speculative dynamic that has created a massive surge in commodity prices appears very close to running its course, as we see very similar "microdynamics" in agricultural commodities as we saw with oil in 2008. That's not to say that we have a good idea of precisely how high prices will move over the short term. The blowoff phase of a bubble tends to be steep, but so short-lived that it affords little opportunity to exit. As prices advance in an uncorrected parabola, the one-sided nature of the speculation typically gives way to a frantic effort of speculators to exit simultaneously. Crashes are always a reflection of illiquidity in two-sided trading - the inability of sellers to find eager buyers at nearby prices.

On the subject of commodities, it's a natural question whether gold falls into the same category as agricultural commodities. After all, gold and other hard assets have an important role as an alternative to money to store value, and it appears clear that the world is monetizing in a way that is unlikely to be fully reversed even if policy makers wish to do so down the road.

In my view, it's not clear that gold is in a bubble here, but it will be important to watch for the earmarks of a classic bubble. Below, I've plotted the price of gold against a "canonical" log-periodic bubble. Already, we're seeing some behavior that is characteristic of a bubble-type advance. A Sornette-type analysis generates a finite-time singularity as early as April, but there are other fits that are consistent with a more sustained advance. If we observe a virtually uncorrected advance toward about 1500 in the next several weeks, the steep and uncorrected advance would imply an increasing hazard probability.Is Gold in a Bubble?

Please see Hussman's article for the charts he mentions.

I agree with Hussman about the bubble in commodities not only because of the speculation angle but also because of unsustainable growth in China. When China stalls, it will likely take commodities and the commodity producing countries down with it, notably Australia and Canada.

Finally, gold is acting more like a currency than a natural-resource commodity (because that is what it is). It may or may not be immune to a commodity-related selloff, and much depends on the actions of central banks down the road.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2011 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.