Is QE2 an Unmitigated Disaster?

Economics / Quantitative Easing Mar 07, 2011 - 04:11 AM GMTBy: Dian_L_Chu

There was a debate recently between Rick Santelli of CNBC and James Bullard, President of the Federal Reserve Bank of St. Louis regarding the inflation effects of the QE2 initiative.

There was a debate recently between Rick Santelli of CNBC and James Bullard, President of the Federal Reserve Bank of St. Louis regarding the inflation effects of the QE2 initiative.

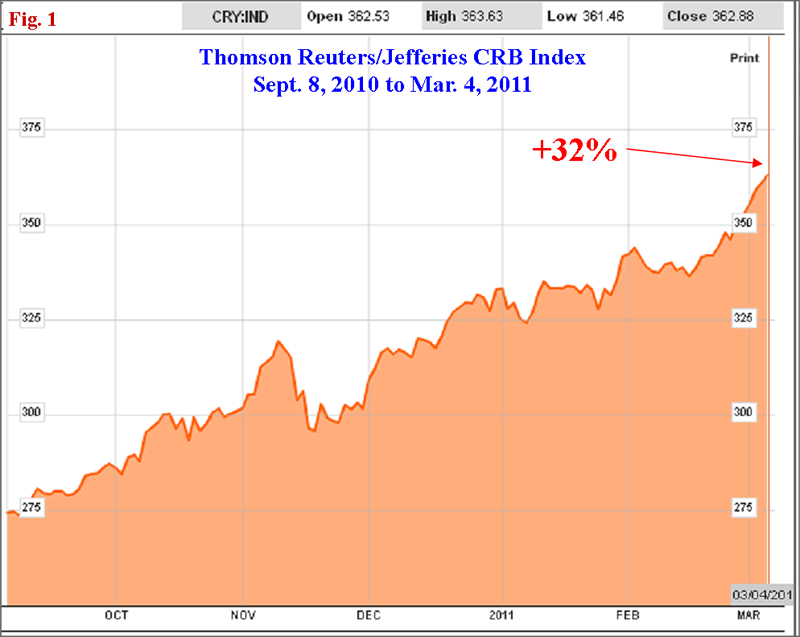

Bullard, the economist, cited the core inflation rate, and even the headline inflation rate as illustrative of a lack of serious inflation pressures in the US economy. Santelli, on the other hand, talked the trader's perspective of inflation wanting to use the CRB Index (Fig. 1) as a true indication of inflation effects since QE2 was brought up at Bernanke’s Jackson Hole Speech in August 2010.

So let us compare two scenarios and ask ourselves would the US economy be doing better without the QE2 initiative?

Pre-QE2 Prices:

- 2.50-2.70% 10-Year Treasury Yield

- $2.64 US Gasoline Price (August 2010)

- Cotton Prices at $85 (Contract Size 50,000 pounds)

- S&P 500 Index 1100

- Copper Prices $3.25 a pound

- US Dollar Index at 83.00

- Lumber Prices at $200 (Futures Contract –Contract Size 110,000 board feet)

- Sugar Prices at $17.50 (Futures Contract-Contract Size 112,000 Sugar #11)

- Cattle Prices at $92 (Futures Contract-Contract Size 40,000 pounds)

- Milk Prices at $14 (Futures Contract-Contract Size 200,000 pounds Class III)

- 3.50% 10-Year Treasury Yield

- $3.50 US Gasoline Price

- Cotton Prices at $215 (Futures Contract -50,000 pounds)

- S&P 500 Index 1320

- Copper Prices $4.50 a pound

- US Dollar Index at 76.40

- Lumber Prices at $303 (Futures Contract)

- Sugar Prices at $30 (Futures Contract)

- Cattle Prices at $114 (Futures Contract)

- Milk Prices at $19.50 (Futures Contract)

About That Unemployment Rate...

This just gives a snapshot of some of the inflationary effects for the US consumer. I cannot think of any argument where higher interest rates resulted from QE2 are good for the housing sector, which is the most troubled part the US economy.

Nevertheless, I must add that the unemployment rate is better, and we have created more jobs since QE2 but with a highly fluctuating job pool where workers give up looking and leave the labor market it is hard to gauge the real unemployment numbers.

Plus how much of the job creation is due to other factors like more business friendly policies from the Obama administration, a Republican Landslide in the Midterm Election, and the extension of the Bush Tax Cuts and a reduction in the payroll taxes for businesses?

Equity Gains Don’t Mean Much

The S&P 500 is 230 points higher which can be argued is good for the “wealth effect” but stocks usually have a year-end rally so some of these gains probably would have occurred even without QE2.

Clear Present Danger – Inflation

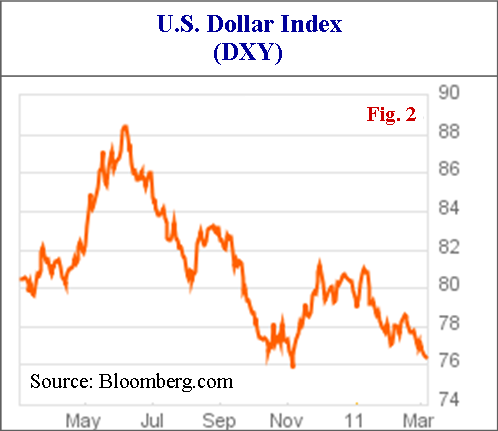

There are some substantial price increases in a lot of these inflationary metrics for both businesses and the US consumer, not to mention the reduced purchasing power of a much lower US dollar (Fig. 2).

More importantly, inflation data utilized by the core and headline rates are behind the curve of futures prices by anywhere from 3-6 months so the true inflation pass through effects of these higher input prices at the futures level have yet to be realized in the Fed`s measures of inflation data.

For example, gasoline prices at the pump probably lag the futures prices established by the RBOB contract by 20-30 cents. Likewise, the full effects of higher cotton prices will take much longer to work their way through the supply chain to consumers at the retail level for clothes they purchase. It may take another six months for the damage that has already occurred at the futures level to be fully experienced by consumers of cotton products, which would lead to an underestimate of the current inflationary effects in the economy.

Biflation at Work

It should be noted that parts of the economic data are deflationary in nature like housing and wages, which serve to artificially keep the inflation numbers utilized by the fed down--the biflation phenomenon--I previously discussed.

And if you add in the 6 month lag factor for inflation effects to pass through to the data, a completely different inflation story starts to emerge.

Wanted – Lower Inflation & Interest Rate

However, this still misses the important barometer for analyzing QE2 which should be the following question: “Which scenario is better off for the US economy?” and not any argument of what the current inflation level is in the economy.

This assumes that some inflation is better than no inflation, and I would argue that being able to finance a home mortgage at 100 bps lower, and a dollar per gallon cheaper gasoline is better for businesses and consumers, and that this scenario is far better for fostering sustainable economic growth than the current scenario of QE2 and its effects.

Really Better Off with QE2?

So the question for Bullard misses the mark if one argues with him what the current or even future inflation effects are for the economy due to QE2. The real question for Bullard is would the US economy be performing that much better without QE2? If you add up all the pros and cons of QE2, guess which scenario would 9 out of 10 independent economists pick for an environment that fosters economic growth?

It seems regardless of what the inflation data says is the overall inflation rate in the economy, QE2 gave us all the negative, anti-growth, lowered standard of living type of inflationary effects that act as a major tax and headwind for both businesses and consumers going forward, and very little of the much needed “Record GDP Growth” and “Eye-Popping Job Creation” bang for our costly buck.

Right Back Where We Started

It seems we pretty much could have gotten this same level of current GDP growth and job creation without massively devaluing the dollar in the process. Sometimes a little patience goes a long way, and if the fed would have waited until the November elections where both the business climate and economic data were improving all on their own we could have had the best of both worlds with a low inflationary price stable environment, and a slow but steadily improving employment situation.

The real fear and irony is that once the full effects of QE2 are realized in the US economy, that we start reacting to said inflationary effects both through tightening monetary policy and consumer/business behavioral changes, and the US starts giving back some of its recent economic gains, and becomes vulnerable to the very scenario that the fed was trying to avert in the first place--a double dip, deflationary downturn--in the economy.

Disclosure: No Positions

Dian L. Chu, M.B.A., C.P.M. and Chartered Economist, is a market analyst and financial writer regularly contributing to Seeking Alpha, Zero Hedge, and other major investment websites. Ms. Chu has been syndicated to Reuters, USA Today, NPR, and BusinessWeek. She blogs at http://econforecast.blogspot.com/.

© 2011 Copyright Dian L. Chu - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.