Delusional Crowds, Booming Economies, Stock Markets and the End Game

Stock-Markets / Stock Markets 2011 Mar 06, 2011 - 08:19 AM GMTBy: John_Mauldin

The Delusion of Crowds and the Endgame

The Delusion of Crowds and the Endgame

Let the Good Times Roll

Are Booming Economies Good for the Markets?

Back to 2007?

People only accept change in necessity and see necessity only in crisis. —Jean Monnet

The economy is doing better, and we will survey some of the highlights. But does this mean the stock market is headed higher? A chart from Louis Gave got me to thinking, and I shot off a few thoughts and questions to Ed Easterling and Vitaliy Katsenelson. What ensued was a lively “battle” of charts and thoughts and more questions, so this week I let you look over my shoulder at our conversation. This letter will print longer than normal, as there are a lot of charts. I think you will find it very thought-provoking, if only a little cautionary. And we start with a look at a survey about what Americans think of the current fiscal deficit and the ways to remedy it.

At the end of the letter I give you a link to a speech by my friend Pat Cox, which is one of the best speeches and PowerPoints I have seen in a long time. It will only remain up for another ten days, per agreement with his publisher, so you really do want to find some time to listen. And I remind you about my conference in La Jolla April 28-30, with its gonzo all-star lineup, which I modestly think makes it the best investment conference anywhere. It is rapidly filling up. Don’t procrastinate. And I have some TV and radio times for next week as well. Now, let’s jump in to today’s letter.

The Delusion of Crowds and the Endgame

My good friend Dennis Gartman pointed me to a recent survey of “likely voters” done by the Tarrance Group. The results were disturbing to me, and show how truly ill-informed the American electorate is. This does not bode well. You can see the survey at http://www.politico.com/static/PPM191_poll.html , but let me highlight a few key points.

“There are widespread misperceptions about the state of the federal budget. A majority of voters incorrectly believes the federal government spends more on defense/foreign aid than it does on Medicare and Social Security (63%). Also, a similar majority (60%) incorrectly believes problems with the federal budget can be fixed by just eliminating waste, fraud and abuse. Voters do not casually agree with these untruths – at least 40% strongly agree. Further, less than half (44%) believe Medicare and Social Security costs are a major source of problems for the federal budget (49% disagree).

“The waste in government is a strong concern to voters – again 60% believe fixing the waste will solve the nation’s budget problems, and voters say that a mean of 42% of each federal dollar is wasted.”

I was on the speaking platform yesterday with David Walker, the former Comptroller General of the United States and head of the Government Accountability Office (GAO) from 1998 to 2008, and we once again got to spend a good deal of time afterwards talking about the fiscal crisis as we were waiting for our respective spots on a PBS interview talk show hosted by Dennis McCuistion. Walker and I share a mutual concern that if “We the People” do not come to an agreement on the fiscal deficit of the US government, the country could be plunged into a crisis of Greek proportions. But he feels (and I agree) that part of the real problem is that people do not understand the true nature of the problem. The survey underscores his point. We have a deficit of $1.6 trillion, and Congress is debating over $61 billion in spending cuts, as if the Republic would founder with those cuts.

That is in large part the message of my new book, Endgame: The End of the Debt SuperCycle and How It Changes Everything. To avoid a crisis that would devastate this country, putting us into a decade-long recession (or worse), we must bring the deficit back (to at least!) below nominal GDP. That means a trillion dollars plus in spending cuts and/or tax increases.

I agree there is room for some serious reduction in waste, etc. The GAO just came out with a paper highlighting scores of redundant government programs. But reducing waste and redundant government programs won’t get us there. Not even close.

There are going to have to be a lot of “sacred cows” led to the altar. The weeping, wailing, and gnashing of teeth as subsidies, tax preferences, deductions, and other government benefits are eliminated or curtailed will be loud and long. The simple fact is that the federal government is now too large for our current income tax base as it is structured, and we have made promises that cannot be kept without a major change in the tax structure. Long-time readers know that I do not like taxes. I stutter when I even try to say the word. But the national conversation we must have as adults is, how much Medicare do we want and how are we going to pay for it? If We The People decide we want Medicare at close to the level we have today, even reformed and optimized, it is likely going to require some form of value-added tax (VAT). Even rescinding the Bush tax cuts on the rich won’t get us close. But we need to recognize there are growth costs (and thus joblosses) that come with higher taxes. If we are going to have a VAT, we need a true top-to-bottom reform of the tax system.

Whatever we decide, we must get the fiscal house in order before the bond market forces us to, because waiting until there is a true crisis will leave us with only very bad choices. Now our choices are merely very difficult. This is going to require either true compromise, which today seems sadly lacking, or political courage that is all too rare, to avoid the very bad choices and long-term destruction that a crisis will force upon us.

As noted at the beginning of the letter, “People only accept change in necessity and see necessity only in crisis” (Jean Monnet). Endgame tries to show why we need to make the difficult choices now.

The official publication date is next Tuesday, March 8. It may (should) start showing up in bookstores this weekend. If you are buying online, kindly wait until Tuesday. I will send you a friendly reminder (actually lots of them!). The reviews have been very kind so far. I am proud of the book, and must say that no small part of its value was contributed by my brilliant young Rhodes scholar co-author, Jonathan Tepper.

I truly hope it leads to a more informed national conversation, not just here in the States but throughout the world, as we all must come to terms with a world that now has a debt-to-GDP ratio of over 300%. We simply must if our children are to enjoy a better economic life than we have been privileged to have (so far). Waiting until the crisis actually hits us (and it will, if we do not act!) is a guaranteed life- and investment-altering event. It will not be fun. Think Greece or Ireland.

Let the Good Times Roll

The economic data that came out this week was mostly strong. The ISM survey numbers, both manufacturing and service, were quite robust. The new unemployment claims were as low as we have seen in years. Today’s employment number was 192,000, which is good, although it should be averaged with a weather-affected January, which brings us back to a number that is growing only slightly more than the population. But we have had four months in a row where the revisions have been upward. That is a good trend.

Same-store sales were solid. Factory orders were also in very good territory. The unemployment rate fell by 0.1%, this time without help from people dropping out of the workforce, although the total employment rate (jobs per population) was down.

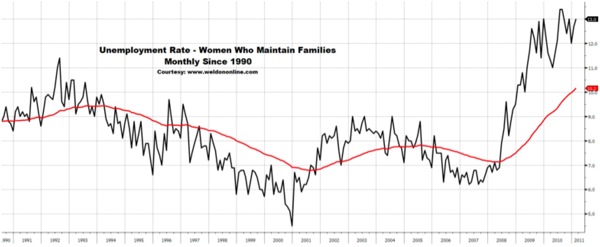

Still, the bears in the crowd can point to very disappointing income growth, and there are spots in the jobs picture that are unsettling. More than one commentary I read pointed out the fact that the following chart from data maven Greg Weldon ( www.weldononline.com) shows. The unemployment rate for certain sectors of the economy is not good at all. Single mothers are still above 13%. Plus, the average duration of US unemployment is still rising and is at an all-time high:

The average duration of US unemployment is at an all-time high:

Still, the economy is doing as well as it has in a long time, and the trends are more or less improving.

Are Booming Economies Good for the Markets?

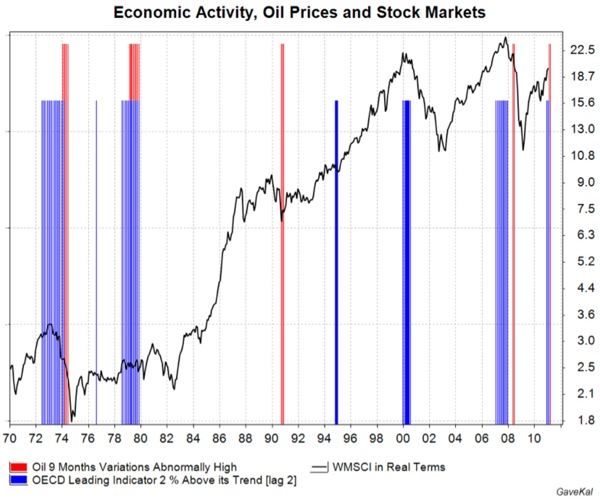

As I noted above, I was reading the daily missive from GaveKal, one of my normally more bullish reads, and I found the following:

“The important question instead is whether booming growth is always good for equity markets. And on that, the data is frankly mixed. Indeed, while strong growth usually leads to higher earnings (good news), it also typically leads to a tighter liquidity environment as a) companies need money to finance larger inventories and capital spending, b) inflationary pressures may impact margins and c) central banks usually respond by draining excess cash away from the system. Of course, today, one could argue that the strong growth need not be a concern as a) companies are sitting on record amounts of cash and are still seeing their financing costs drop and b) Western central banks have yet to start tightening monetary policies. So the liquidity environment has yet to really tighten up.

“Still, we thought we would look at periods when the OECD LI stood 2% above their long term trend—identified as the areas shaded in blue on the chart overleaf. Interestingly, as the performance of the World MSCI (black line) shows, periods of strong economic growth do not always equate to tremendous stock market performance over the following six months. Equity markets struggle all the more if, while growth is booming, oil prices suddenly surge (red bars on the chart); a relationship which makes sense given that a high price of oil further drains excess liquidity from financial markets and typically generates large misallocations of capital (moving money from the pockets of Western consumer to those of Ahmadinejad, Chavez and Gaddafi is not really a good long-term use of capital). In fact, as the chart illustrates, the most dangerous periods for equity markets are typically periods of strong economic activity combined with rapidly rising oil prices.”

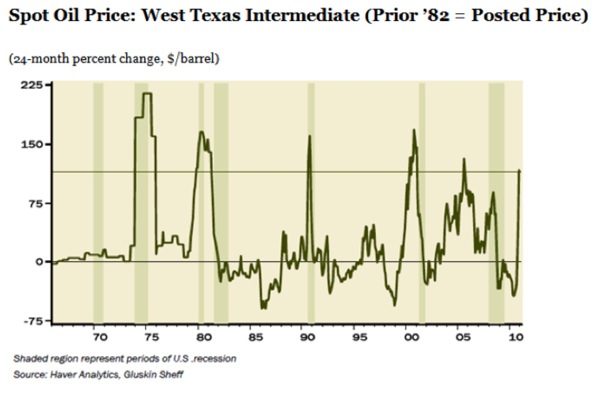

The team at GaveKal rightly noted the problems of a doubling in the price of oil and the shocks to the stock markets and world economy that would result. Good friend David Rosenberg puts those facts into this commentary, along with a graph:

“There have been only five times in the past 70 years when this has happened within a two-year time frame: January 1974, November 1979, September 1990, June 2000, and August 2005. And now, December 2010. . . . Of the five instances cited above, all but one involved a recession for the U.S. economy and that was in 2005 during the height of the credit and housing boom, which acted as a huge offset. But oil prices did keep rising and managed to outlast the euphoria in credit and residential real estate, so the recession may have been delayed at the peak of the ‘growth rate’ in the oil price, but it was not derailed, as history shows.”

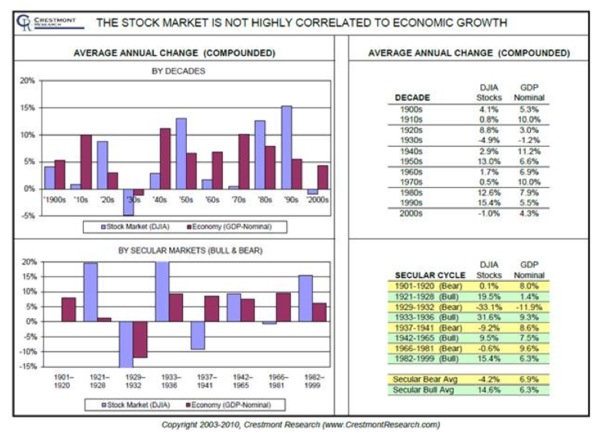

So, I posed the following question to Ed Easterling of Crestmont Research (latest book, Probable Outcomes) and Vitaliy Katsenelson (The Little Book of Sideways Markets). They love this type of stuff.

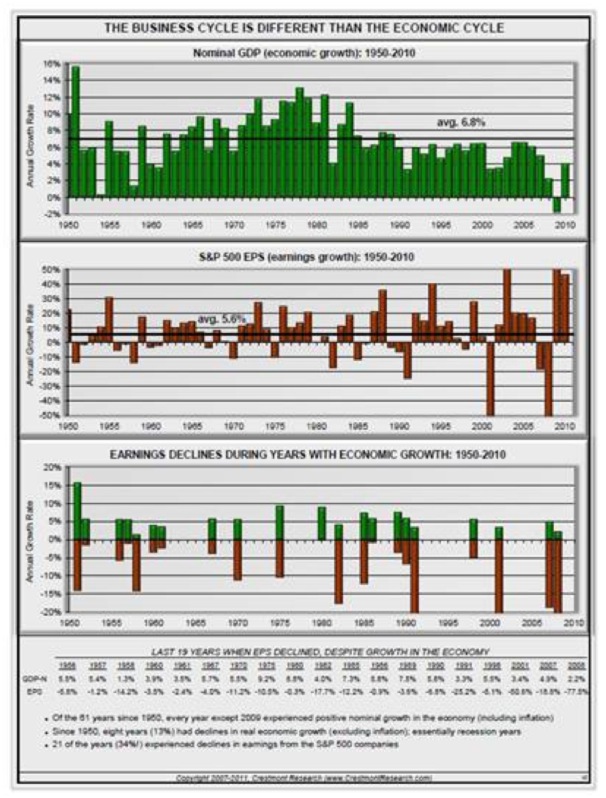

As Ed notes, the stock market is not correlated with economic growth. In fact, as the next charts and tables show, secular bear markets even have higher nominal GDP growth than secular bulls.

Next he points out that 34% of the years since 1950 with economic growth have experienced declining earnings per share (EPS) growth!

Back to 2007?

Vitaliy wrote back:

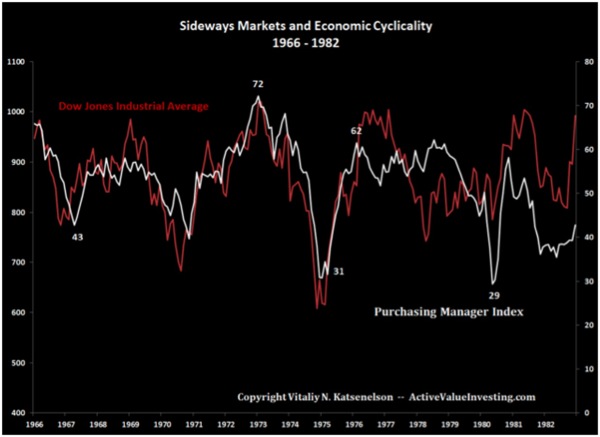

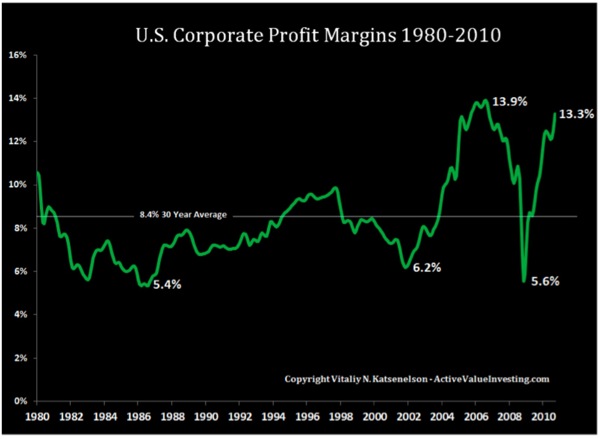

“Here [in the charts below] is PMI vs. Dow 1966-1982 and 2000-today. Also, what worries me is that corporate profit margins are approaching pre-2007-crisis highs (see the third chart). A small slowdown in the economy, or just stagnation, will send profit margins down. Hopefully this helps. Also, as you normalize PEs for high profit margins (i.e., look at 10-year trailing PEs), the market is trading 30%+ above average PE – secular bull markets just don’t start at these types of valuations. In addition, the market did not spend enough time at below-average PE for this move to be the new secular bull market (in the 1966-1982 sideways market, PE was below-average half the time).

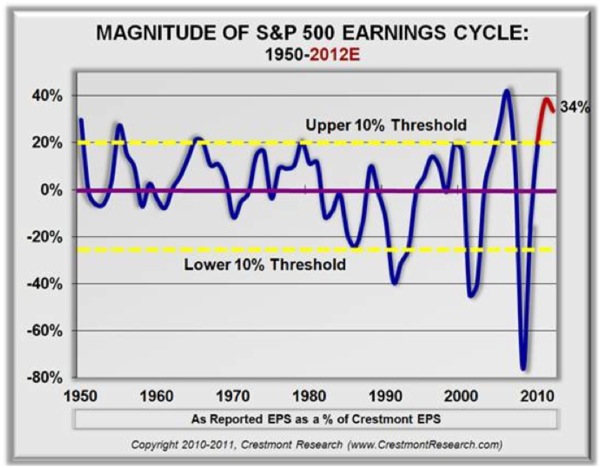

(Ed has his own way of normalizing earnings ( www.crestmontresearch.com). He has developed a methodology – one that is fundamentals-based – that produces similar results to that of a ten-year average, or something like Shiller’s work, yet also provides forward-looking insights. In brief, it uses the close and fundamental (not coincidental) relationship between earnings per share (“E”) and gross domestic product (GDP) to adjust for the business cycle. The baseline E for each period is essentially based on mid-point values for E across the business cycle – peak and trough periods of actual earnings reports are adjusted back to the underlying trend line to reduce the intra-cycle distortions.)

If you use his form of normalized earnings, and use the earnings projections from the S&P website, you find us back in the nosebleed territory of 2007, which is both Vitaliy’s and my worry. Stocks are once again priced for perfection, but I worry that we live in an imperfect world. The markets are assuming a normal business cycle, but as I strongly suggest in Endgame (shameless plug), we are not in a normal business cycle. It is the dénouement – the end of the debt supercycle, which distorts the normal financial physics that markets have come to rely upon. When markets get this distorted, whether to the upside or the downside, a correction of some sort is around the corner.

As both GaveKal and Rosenberg note, a doubling in the oil price is not good for markets. And if we actually do begin to work on the deficit to the tune of $150 billion or so a year in cuts and tax increases, while it may be necessary for the survival of the economy, it will also be a headwind for economic growth and earnings. There is no free lunch. Again, not dealing with the deficit is a “game over” event. There are no choices that do not have some pain involved.

As I wrote a few weeks ago, we are entering a period where recessions are likely to be more frequent and markets more volatile. These are not times for normal buy-and-hold strategies.

Let me offer a brief commercial plug for my US partners who specialize in alternative investments. Whether you are an individual or an investment professional, you should call them and see what they can do to help hedge your portfolio against the type of volatility I have discussed above. In general (and with some exceptions), Altegris Investments deals with accredited investors whose net worth is above $1.5 million. They are specialists in hedge funds, commodity funds, and other types of alternative portfolios. You can call them at 1-800-828-5225 and tell them I sent you.

My friends at CMG generally work with investors whose net worth is smaller. They have a platform of active managers who run liquid discretionary accounts. With either firm, you can choose among managers that make sense for your personal situation and needs. You can reach CMG at 800-891-9092.

If you are outside the US, or would rather register online, you can go to www.johnmauldin.com and click on The Mauldin Circle, and one of my partners, either in the US or around the world, will call you. (In this regard, I am president and a registered representative of Millennium Wave Securities, LLC, member FINRA.)

My Strategic Investment Conference

I want you to mark your calendars for April 28-30, when I will host, along with my partners at Altegris Investments, what I think will be the single best investment conference of the year. It will be the 8th annual Strategic Investment Conference in La Jolla. Let me give you the Killer’s Row line-up of speakers, in alphabetical order: Martin Barnes (Bank Credit Analyst), Marc Faber, Niall Ferguson (author and Harvard professor), George Friedman of Stratfor, Louis-Vincent Gave of GaveKal, Neil Howe (The Fourth Turning), Paul McCulley (if he ever surfaces from his fishing vacation), David Rosenberg, Dr. Gary Shilling, Jon Sundt (of Altegris) and, of course, your humble analyst. I mean, really. Most conferences have one or two top-tier headliners. We have nothing but the best. These guys are all great speakers, but getting them on panels together? Way cool. Plus some of the best hedge-fund managers (personal opinion) show up to give you their thoughts. And maybe a surprise last-minute guest or two. If this conference lineup were a baseball team, they would sweep the World Series. Oh, and the best part? Your fellow conference attendees. The interaction among them is what truly makes this conference the best.

You can still register today at http://hedge-fund-conference.com/2011/invitation.aspx?ref=mauldin. Sadly, the conference is limited to accredited investors with a net worth of more than $2 million, as there are funds presenting that require that minimum (and some even more). Those are the rules we have to live with, whether I like them nor not (I don’t, as long-time readers know). But we follow them religiously.

Every year the conference sells out. Every year some of you wait to the last minute, thinking we can “always take one more.” We can’t. There is a limit to the space. We are getting close to capacity. If you have attended in the past, call your Altegris representative and make sure you get on the list. Do not procrastinate. (1-800-828-5225)

Don’t Miss This Speech

Pat Cox is one of my real “go-to” guys when it comes to finding life- and economy-changing new technologies. He writes Breakthrough Technology Alert, which is one of my true must-reads and a solid source for investment ideas. I am a huge fan. He did a speech in Vancouver last year that simply blew me away, and the PowerPoint was awesome. I finally got his publisher to let me post it for a few weeks – at least until March 15. You really should take the time to hear how the ideas of Schumpeter and others feed into opportunities today. The presentation is at http://www.johnmauldin.com/outsidethebox/special/complimentary-investment-presentation-by-patrick-cox/

(As part of the deal with his publisher to get the speech on my website for free, there is an offer to subscribe to Pat’s letter at a substantial discount. For those interested in new tech, you really should consider it.)

Media, La Jolla, London, Malta, Milan, Zurich, and New York

Next Friday Tiffani and I fly to La Jolla for one night to be with my partner and friend Jon Sundt of Altegris Investments as he celebrates his 50th birthday. I can guarantee he will do it in style! Then back home to watch the Mavericks take on the LA Lakers. Now that will be a rocking weekend.

The next weekend I head to London, where I will be the guest host on Squawk Box on CNBC in London, then head off to Malta for meetings of some funds I serve on the boards of, then it’s Milan for a public speech, and then Zürich on Friday and back the next Saturday. Lots of planes, trains, and automobiles.

My other US partner, Steve Blumenthal of CMG, also turns 50 on April 2, so I will head to Utah for his gala bash, then dash back to New York (April 4-6, right now) for a few days to talk about my book wherever I can. Next week I open on Monday morning on the Ron Insana radio show, then Tuesday at 10:15 Eastern on Bloomberg, that afternoon on Fox Business with Liz Claman, and later on Canadian channel BNN. On Thursday I will be on MSNBC with Dylan Ratigan, sometime in the 4-5 pm EST time slot.

I remember a time in my life when, even though I had multiple businesses and seven kids, I had time to watch TV and take naps on Sunday. Life seemed slower, as I look back on it, than it is now, although I remember feeling quite busy at the time. Lately, I feel as though I am drinking life through a fire hose. That is not a complaint, understand, as I am enjoying every day and the opportunities I have. I am grateful.

This weekend is filled with family and the gym, as I fight the good fight with aging. My youngest son needs a new phone and I need to get on the list for the new IPad. There is an Irish Festival and my kids are insisting I go with them (I taught them young to enjoy Celtic music). So maybe there is time to slow down after all. Have a great week, and remember to buy my book on Tuesday!

Your hoping for a fourth best seller analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.