G7 Banana Republics ON the Money Printing Inflation Road to ZIMBABWE!

Economics / Inflation Feb 09, 2011 - 06:54 PM GMTBy: Ty_Andros

The global financial cataclysm is mushrooming with every stroke of the keyboard at a central bank, with the issuance of new debt to cover old debt, and with the illusion of creating money out of thin air. It is all debt, nothing else, with no final settlement…. EVER. You exchange the money you work for and save and buy a government bond; they print the money to pay you back and PRETEND you have been paid. The situation is just as Von Mises outlined:

The global financial cataclysm is mushrooming with every stroke of the keyboard at a central bank, with the issuance of new debt to cover old debt, and with the illusion of creating money out of thin air. It is all debt, nothing else, with no final settlement…. EVER. You exchange the money you work for and save and buy a government bond; they print the money to pay you back and PRETEND you have been paid. The situation is just as Von Mises outlined:

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved” -Ludwig Von Mises

The LEADERS of the developed world have chosen the latter route. This is a currency and financial-system extinction event, make no mistake. Only the zigs and zags on the path to that destination are UNKNOWN. We’re seeing the most powerful forces on the planet aligned against each other: King Kong (Mother Nature and Darwin) versus Godzilla (public servants, banksters, elites and crony capitalists).

(Tedbits thanks Lampoon the System for this cartoon, they employ political satire in the fight for liberty and freedom. Check out their website, animation, and cartoon book at www.LampoonTheSystem.com)

Mother Nature and Darwin may lose a skirmish, but they have NEVER lost a war, in all of history.

As the New Year opens and the global financial crisis INTENSIFIES, the INVESTING public and main-stream financial industry are exhibiting superhuman optimism about a perceived one-way bet (HIGHER) with quantitative easing II (QE II) by the Federal Reserve and others as the driver.

The investing public is going to be taken out and shot SOON. Once the deadwood (the public and weak-hand investors) is carried out on a stretcher, the advances in many markets can be expected to continue, supported by inconceivable amounts of monetization of the insolvencies throughout the G7 financial systems and sovereigns.

The G7 economies are AFLOAT on a sea of MONEY printed out of thin air. Not a day goes by when some previous liability rears its ugly head demanding payment or a government GUARANTEE for new BORROWING, which requires new MONEY PRINTING OUT OF THIN AIR in inconceivable sums. Most public servants and Keynesian economists EXPECT a recovery to unfold. Don’t hold your breath, as NOWHERE are policies being implemented to FOSTER a recovery: INCOME and ECONOMIC growth.

The only thing growing in the developed world is GOVERNMENT, debt and IOU’s, known as G7 currencies, the welfare state and unfunded entitlements, NEW regulations and unfunded PUBLIC SECTOR pensions. Every other measure of growth and employment is a statistical illusion, courtesy of politically-correct and practically-incorrect inflation measures.

This is their recipe for INCOME and ECONOMIC growth. The bottom line is that these things that are growing are all liabilities of the PRIVATE sector since that is the only economic activity which produces wealth. Not to mention the piles of paper and electronic IOU’s known as developed-world currencies, as they roll off the presses and keyboards at the respective central banks. These are not money; they are IOU’s and credit, and credit is not money, thus the insolvencies are DEEPENING not receding with these actions.

(Authors note: At no time have the investing opportunities been greater than they are today. Volatility is set to EXPAND as surprises appear… and “Volatility is Opportunity” for the prepared investor. Gold and Silver-backed absolute-return alternative investments with the potential to thrive in up down and sideways markets should be a part of any portfolio plan. This is what I do…)

These are promises to pay by sovereign and financial-system debtors who have NO ABILITY to repay previous borrowing, let alone NEW funds. Who guarantees this debt, past and present? You and me and the private sector and whatever purchasing power is left in your FIAT currencies and PAPER financial assets. The G7 governments and financial systems are careening out of control with a ship of fools (public servants, crony corporatists, elites and banksters) as drivers. PREDATORS on the private sector, with the public as their patsies.

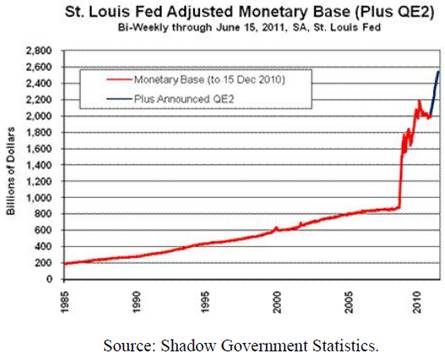

Look no further than this chart of the St Louis Fed Monetary Base Adjusted for QE2, courtesy of www.shadowstats.com :

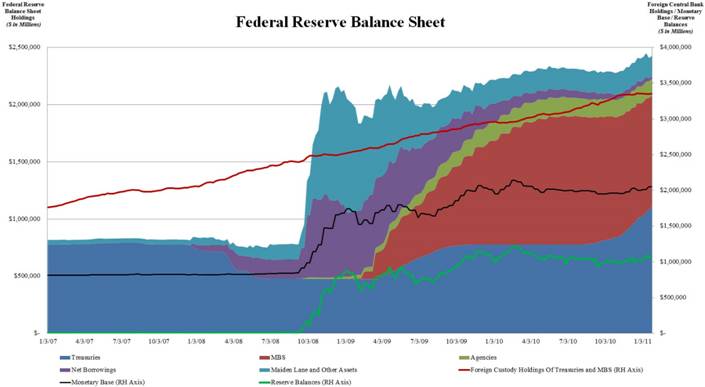

Here is the face of ON-BALANCE-SHEET monetization of Treasury Debt, courtesy of www.zerohedge.com:

While I was on vacation recently, the Federal Reserve released the records of its bailouts in 2008, and the numbers DID NOT ADD UP. They disclosed they purchased approximately $1 Trillion of TOXIC assets at that time. The New data REVEALED that it was almost $3.3 Trillion, extending to institutions (hedge funds, foreign banks, insurance companies, crony capitalists such as GE, etc.) around the world, signifying off-balance-sheet holdings of another $2.3 Trillion. You can bet this off-balance-sheet vehicle is MANY TIMES that which was disclosed in November. Like ALL off-balance-sheet special-purpose vehicles it is used to hide and deceive the public.

"If you look at the firms that came under pressure in that period... only one... was not at serious risk of failure," Mr Bernanke told the commission. "Even Goldman Sachs, we thought there was a real chance that they would go under." Helicopter Ben

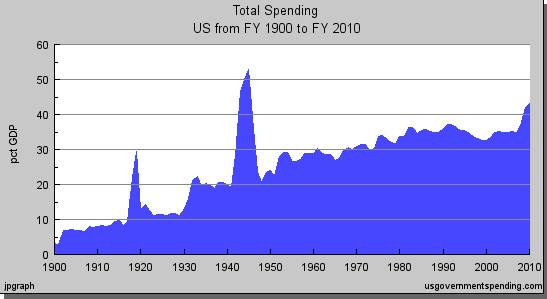

Last year alone, the US government BORROWED approximately $10,624 for every man, woman and child in America – this does not include state and municipal borrowing, on top of that which was paid in income taxes, fees, etc. Obscene and Absurd. Like the cancer it is, government has grown and continues to grow out of control. Spending as a percentage of GDP has been going vertical since 2006 when the progressives captured congress and the chosen one was elected to the highest office in 2008. Take a look at this chart stretching back to 1900 (thanks to www.thegartmanletter and www.usgovernmentdebt.com ):

Nothing in the State of the Union indicated concern over runaway spending, growth of government as a percentage of GDP, or cutting the deficit. IN FACT, the chosen one proposed to INCREASE them.

Nothing in the State of the Union indicated concern over runaway spending, growth of government as a percentage of GDP, or cutting the deficit. IN FACT, the chosen one proposed to INCREASE them.

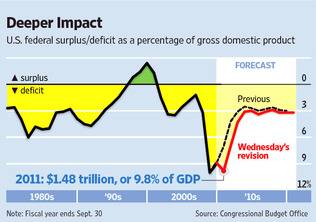

On the same day, the Social Security Administration announced that the Social Security receipts are $50 Billion LESS than the amount paid out THIS YEAR. Just add it to the deficit which was announced at a new high of $1.5 trillion for 2011. The projected recovery in revenues and decline in deficits are proving to be the mirage that all Congressional Budget Office projections are (hopeless assumptions are in them). Take a look:

You can expect the deficits to move horizontally as far as the eye can see; the recovery will never MATERIALIZE. The new republican congressional majority just unveiled their BUDGET cuts; it’s like bringing a SQUIRT GUN to a FOREST FIRE. BIG government progressives. This is the third year running of trillion-dollar-plus deficits and they can be expected to be that high for another 3 years at least. Who could be expected to BUY all that junk paper? Who else…

You can expect the deficits to move horizontally as far as the eye can see; the recovery will never MATERIALIZE. The new republican congressional majority just unveiled their BUDGET cuts; it’s like bringing a SQUIRT GUN to a FOREST FIRE. BIG government progressives. This is the third year running of trillion-dollar-plus deficits and they can be expected to be that high for another 3 years at least. Who could be expected to BUY all that junk paper? Who else…

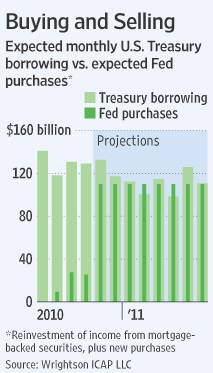

The Federal Reserve is now buying virtually ALL NEW ISSUANCE of treasury debt and has now become the largest holder of US debt in the world (what they hold OFF balance sheet nobody knows). Foreign central banks in Asia may roll existing treasuries, but they want NO MORE US dollars/treasuries. The US government is also the holder of 95% of the mortgage markets; as home values are dropping, NO ONE else will lend against them, the falling-knife trade.

The Federal Reserve is now buying virtually ALL NEW ISSUANCE of treasury debt and has now become the largest holder of US debt in the world (what they hold OFF balance sheet nobody knows). Foreign central banks in Asia may roll existing treasuries, but they want NO MORE US dollars/treasuries. The US government is also the holder of 95% of the mortgage markets; as home values are dropping, NO ONE else will lend against them, the falling-knife trade.

“US government debt is a safe haven the way pearl harbor was a safe haven in 1941” -Niall Ferguson, Harvard University

As interest rates decline to nearly zero bound, it is classical Keynes who postulated that buyers of government bonds would disappear and retreat to cash as the returns in the bonds could not justify the risk in holding them. This appears to be taking place, and once WASHINGTON and the Fed become the whole market (which they now are), how will they get private investors to return after they withdraw -- this is the question. As anyone can see, NO ONE has returned to the mortgage market since the government took over. Can you say QE 3, 4 and forever until the collapse? Take a look at this chart from www.zerohedge.com :

The Federal Reserve is now the biggest holder of treasury debt and its balance sheet of treasury debt is compounding at approximately 8.8% MONTHLY (not yearly) and will RISE by approximately 90% by June 2011. Who do you think is master when Helicopter Ben and the chosen one (Ob@m@) get together?

“Let us control the money of a country, and we care not who makes the Laws” -Amschel Rothschild, original head of the House of Rothschild.

Of course, the Federal Reserve is a holding of that same banking family. A MONOPOLY on MONEY, run not for BENEFIT OF THE COUNTRY but for the benefit of the BIG BANKS! Keep in mind that Central Banks PRINT money to buy each other’s bonds; a liability of one bank is an asset to another. This is the greatest check kiting scheme in history, run by the developed-world governments and banksters, with the public as PATSIES. US Treasury auctions will NEVER fail as foreign central banks will ALWAYS print the money to prevent a failure and the collapse in the value of their reserves.

This is why central bank reserves are up 300 to 500% since 2000; they are MONETIZING each other’s debts and they do it REGULARLY. Just look at the indirect bidders at the Treasury auctions and how their percentage has exploded; that is the growth of monetization. It is ALWAYS growing and NO ONE ever gets PAID BACK, it only grows, like the cancer it is.

“World needs $100 Trillion more credit, says World Economic Forum” -The Telegraph

The MORAL and FISCAL bankruptcy of the G7 welfare states is on PLAIN display as they SINK into death…. er, debt spirals and ultimately BANKRUPTCY. The developed world has now become a BANANA republic in everything but name only. Frantically rearranging deckchairs on the Titanic, as sovereigns and their banking systems slowly sink and take their financial systems and currencies with them.

As the main-stream press misleads the public to support PUBLIC servants and central bankers in raping the public and their creditors at large with the soft default of the printing press. The printing press looms LARGE in 2011, as the maturity wall of PAST borrowing (which is requiring the rolling forward of previous borrowing) joins with current requirements for NEW borrowing to create the perfect storm for developed-world governments and financial systems.

In the United States the amount required has BALLOONED to almost 28% of GDP, totaling approximately $4.2 Trillion. Just doing the math tells us this will require a US Bond issuance of one maturity or another of almost $16 Billion A DAY (260 weekdays in 52 weeks). Since these sums are unconceivable to me and you, let me take it to a number you may be able to grasp: take $1 Million and multiply that by 16,000 A DAY! How absurd. This is being loaded onto the US public’s back as DEBT slaves to pay for the follies (i.e. redistribution, expansion of government and funding of politically-correct schemes such as CLEAN energy, ethanol, etc. -- boondoggles all) of morally-bankrupt public servants, banksters, crony capitalists and elites.

In the United States the amount required has BALLOONED to almost 28% of GDP, totaling approximately $4.2 Trillion. Just doing the math tells us this will require a US Bond issuance of one maturity or another of almost $16 Billion A DAY (260 weekdays in 52 weeks). Since these sums are unconceivable to me and you, let me take it to a number you may be able to grasp: take $1 Million and multiply that by 16,000 A DAY! How absurd. This is being loaded onto the US public’s back as DEBT slaves to pay for the follies (i.e. redistribution, expansion of government and funding of politically-correct schemes such as CLEAN energy, ethanol, etc. -- boondoggles all) of morally-bankrupt public servants, banksters, crony capitalists and elites.

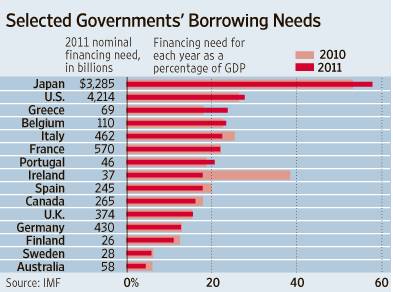

In the developed world the total required is $10.2 trillion for the year, or $39 billion (39,000 million) a day. These sums are SIMPLY INCONCEIVABLE, and of course do not include all the debt these rascals have either GUARANTEED, promised to pay in future entitlements or hold off their balance sheets, especially including that of their financial systems. And that is before even one company tries to raise money in the bond markets; but what will be left to borrow? Take a look at the bloody details as compiled by the IMF:

This is the boat the developed world’s economies and public servants find themselves in, and it is sinking FAST. What a maturity wall, will they hurdle it? When looking at Ireland, that number is now almost another 20% of GDP for 2011 -- not including the bailout of 82 billion Euros in 2010. That is 28,533 Euros ($38,947) per person in Ireland (now debt slaves to foreign banksters in the eurozone). Including interest, principle and compounding, every man, woman and child will pay MANY TIMES MORE than this. This is not a rescue, this is a crime against the public.

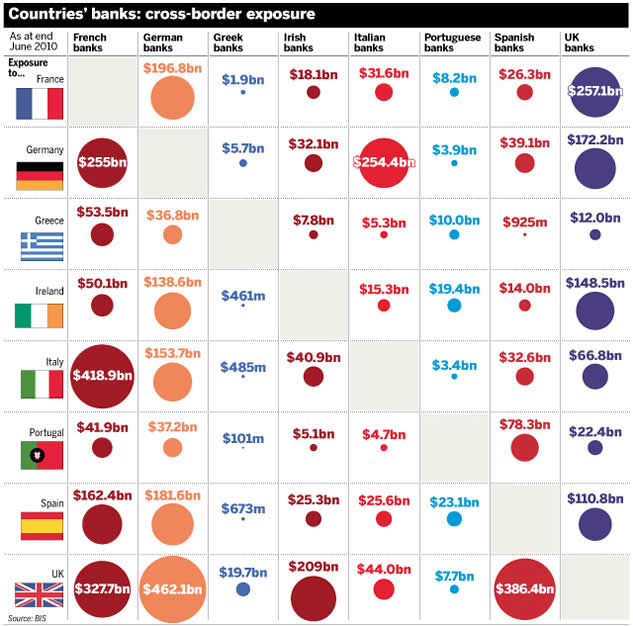

The Irish bailouts are FAR FROM OVER, billions more unpayable IRISH BANK obligations are still sitting within the EU banks and have yet to be dealt with. To see just a hint of what’s to come, take a look at this illustration of Crossborder Holdings of the PIIGS (Portugal, Ireland, Italy, Greece and Spain) to see the enormity of the current challenges – and but a small portion of the TOTAL European Union’s challenges:

This is why they are furiously REFORMING the European Bailout Bunds, which is a dwarf when considering the true size of the problem. Banksters in DAVO’s have made the case for massive new funds to BAIL THEM OUT.

“Europe is testing the limits of REACTIVE incremental..strategy… The laws of economics, like the laws of physics, DO NOT respect political constraints” –Larry Summers

The EU governments just LIED to the PUBLIC and then KICKED the can down the road. Political lies about the SOLVENCY of the European Soveriegns and financial systems will ultimately FAIL. These are not bailouts of the banks, they are bailouts of the lenders… This is the public servants and elites SELLING OUT their constituents to RESCUE banksters who printed the money they lent the Irish banks: OUT OF THIN AIR.

Just last week it was disclosed that an additional €51 Billion where printed OUT of THIN AIR by the Irish central bank, in addition to the bailout figures. Supposedly this was forbidden when the EURO was created; now all that is required is a NOTIFICATION to the European central bank. Expect a lot of NOTFICATIONS this year. The disclosure of the Euros that were printed were hidden in footnotes of the Irish Central bank’s statements. Look for more HIDDEN notes.

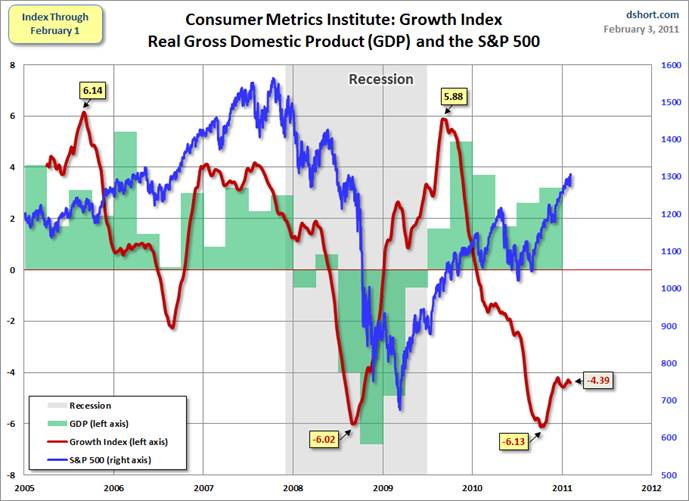

Just now I received an email from the Federal Reserve bank of New York announcing another $8.87 billion ($8,700 Million) PRINTED OUT OF THIN AIR. I get them DAILY. It is a tsunami of cash, rolling into already overpriced markets, and they are floating higher as this mountain of money seeks shelter from the PRINTED money coming right behind it. Assets of all types except treasuries are repricing to reflect the lower purchasing power of the currencies in which they are denominated. Look closely at this next chart as it ILLUSTRATES how money creation since the 2009 lows have caused the markets and GDP to DIVERGE from the Consumer Metrics Tracking Index of Consumers from the past correlation:

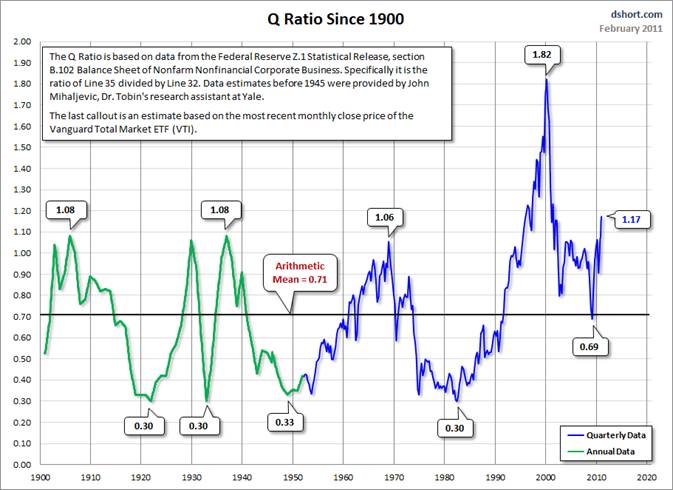

Consumer spending peaked mid 2009, and has plummeted to 2008 lows, but QE II has levitated the markets and GDP since mid 2010. That is a RUBBER BAND and at some point soon it can be EXPECTED TO SNAP! Either the consumer will start spending and borrowing again or the stock market and GDP will PLUMMET to reflect the real levels of consumer activity. Once QE II ends expect the latter. It is quite clear that Helicopter Ben is trying to inflate OVERLEVERAGED financial and real estate assets… he has succeeded, as reflected by this chart, courtesy of (www.dshort.com ):

(The Q Ratio is a popular method of estimating the fair value of the stock market developed by Nobel Laureate James Tobin. It's a fairly simple concept, but laborious to calculate. The Q Ratio is the total price of the market divided by the replacement cost of all its companies. Fortunately, the government does the work of accumulating the data for the calculation. The numbers are supplied in the Federal Reserve Z.1 Flow of Funds Accounts of the United States, which is released quarterly. The first chart shows Q Ratio from 1900 to the present. I've extrapolated the ratio since the latest Fed data (through 2010 Q3) based on the price of VTI, the Vanguard Total Market ETF, (Thank you www.dshort.com )

WOW, the stock market is the second most OVERVALUED since 1900. It is an almost UNANAMOUS BUY by the main stream financial press. To be able to understand the enormous amount of money creation driving these markets.

WOW, the stock market is the second most OVERVALUED since 1900. It is an almost UNANAMOUS BUY by the main stream financial press. To be able to understand the enormous amount of money creation driving these markets.

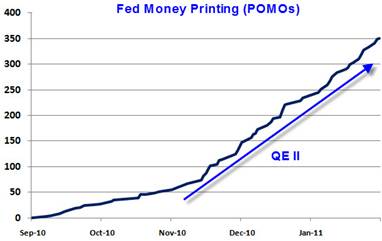

Take a look at this chart from www.ChrisMartenson.com illustrating QE II (350,000 million dollars since SEPTEMBER):

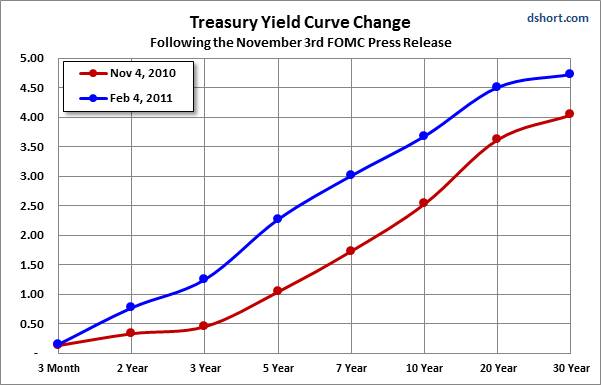

Notice how this resembles the charts of domestic stock, commodities and precious metals markets? This is the INFLATION that the Federal Reserve is DETERMINED to foster. Look what this has FOSTERED in the Yield Curve (courtesy www.dshort.com ):

Since the biggest monetary cannons began in November, the yield curve has widened anywhere from 40 to 150% or more (interest rates have RISEN those percentages), depending on the maturity you are viewing. As this goes to press, yields are aggressively rising again. Look for it to continue until the economy collapses on the rate increases. When this is happening, malinvestments CANNOT INFLATE as the Federal Reserve would like.

The yield curve: 2-year notes versus 10 and 30-year bonds is approaching new record spreads every day as investors abandon the long end and/or demand higher rewards for the inflation risks. As I have said many times, BLOW OUTS equal BLOW UPS, and we are only waiting for the next blow up to arrive.

Keep in mind that these governments have RARELY paid a dime of principle back, ever, in their histories. It has always been the rolling of old debt and new borrowing. This is the definition of JUNK bombs, er….. bonds. But the credit ratings agencies call them mostly RISK FREE. Of course they are, defaults will NEVER occur as payment is as close as the printing press.

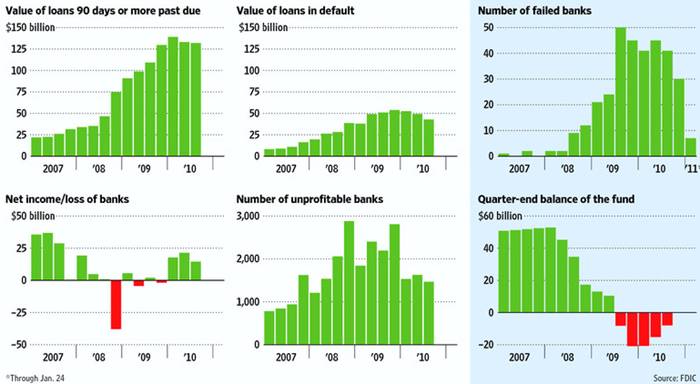

Taking a look at the US banking system provides insights for the G7 in general as a large portion of it is operating in INSOLVENCY:

WOW: Look at that, over 1,300 US banks are unprofitable, aka INSOLVENT. And if they ever ENFORCE FASBY 157 (mark to market of their assets), most of the rest would be revealed as insolvent as well. But this can be extended to Europe as well, such as the Spanish Community Banks known as Caja’s, or the Landesbanken in Germany. NO COUNTRY in the developed world is immune to this picture; it is an epidemic of FINANCIAL SYSTEM and Sovereign INSOLVENCY. Furthermore, it is MUSHROOMING daily, just like the sovereign and financial system NUCLEAR holocaust that IT IS….

In conclusion: Don’t worry. They have been and will continue to PRINT the MONEY. The question is WHEN? Economies and markets APPEAR to be recovering on this gusher of printed money and out-of-control government spending. It’s down a rat hole, so to speak, because once the money is spent on CONSUMPTION, the debt just remains like a millstone around the public’s neck, leaving debt slaves and serfs to leviathan governments, public serpents, er … servants, banksters, crony capitalists and elites. In the old days they would be known as Benedict Arnolds and traitors. The useful idiots known as the public are the dupes of the public school monopolies and main-stream media (both are controlled by the same people).

(Authors note: Do you know how to put gold and silver behind your investments? Or make money in declining or sideways markets in addition to rising markets? At no time have the investing opportunities been greater than they are today. Volatility is set to EXPAND as surprises appear and “Volatility is Opportunity” for the prepared investor. Gold and Silver-backed, absolute-return alternative investments with the potential to thrive in up down and sideways markets should be a part of any portfolio plan. This is what I do…)

What is unfolding in North Africa is soon COMING TO AMERIKA and EUROPE. The death, er…. debt spiral is still in full bloom and growing in intensity every day. Is there ANY country in the developed world PAYING down DEBT? Is there any country not adding to their DEBT? It is compounding at a rate 3 times that of the statistical illusions of GDP that they present as growth!

In order to pay debt you must have income growth, and income growth is nothing but a statistical ILLUSION, courtesy of politically-correct INFLATION measures used to FIX the DATA for PUBLIC consumption. Incomes are in FREEFALL if correctly measured and INFLATION is EATING the middle and lower classes ALIVE. We have a congress doing tax and spend, borrow and spend (40 cents of every dollar spent is BORROWED), and the Federal Reserve is doing print and spend. DITTO EUROPE.

NOWHERE are the policies of growth being considered or implemented, and as growth contracts, the printing press is the only escape route. The only thing holding up the developed world is BEN BERNANKE (Federal Reserve), Jean Claude Trichet (European Central Bank), Mervyn King (Bank of England) and the rest of the G7 central bankers. Soon the illusion of prosperity on the back of printed wealth will be revealed for the fraud it is. Looking at financial assets, stocks, commodities, food and energy, we see the Zimbabwe moment is now arriving. Broad money supplies in Europe have begun to contract AGAIN; it is only a matter of time until they do in the US as well.

Tedbits will be resuming a regular publication schedule going forward; subscribe for free at www.traderview.com/subscribe . We are also developing a relationship and collaboration with Gordon T Long, a brilliant technician and market analyst. Gordon’s most recent work can be found at: http://lcmgroupe.home.comcast.net/.. and I urge you to visit him.

By Ty Andros

TraderView

Copyright © 2011 Ty Andros

Hi, my name is Ty Andros and I would like the chance to show you how to capture the opportunities discussed in this commentary. Click here and I will prepare a complimentary, no-obligation, custom-tailored set of portfolio recommendations designed to specifically meet your investment needs . Thank you. Ty can be reached at: tyandros@TraderView.com or at +1.312.338.7800

Tedbits is authored by Theodore "Ty" Andros , and is registered with TraderView, a registered CTA (Commodity Trading Advisor) and Global Asset Advisors (Introducing Broker). TraderView is a managed futures and alternative investment boutique. Mr. Andros began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Di ego , and the University of Miami , majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis, creating investment portfolios designed to capture these unfolding opportunities as the emerge. Ty prides himself on his personal preparation for the markets as they unfold and his ability to take this information and build professionally managed portfolios. Developing a loyal clientele.

Disclaimer - This report may include information obtained from sources believed to be reliable and accurate as of the date of this publication, but no independent verification has been made to ensure its accuracy or completeness. Opinions expressed are subject to change without notice. This report is not a request to engage in any transaction involving the purchase or sale of futures contracts or options on futures. There is a substantial risk of loss associated with trading futures, foreign exchange, and options on futures. This letter is not intended as investment advice, and its use in any respect is entirely the responsibility of the user. Past performance is never a guarantee of future results.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.