Market Barotrauma - Disconnect From the Reality of the Business Cycle

Economics / Inflation Oct 26, 2007 - 09:47 AM GMTBy: Brian_Bloom

There has been a disconnect in logic which has been seriously bothering me in recent weeks. Everything in my training has taught me that ‘the market' ultimately exerts a discipline on speculative excess, and ‘the market', being the sum of all players, is more powerful than any one player or set of players. Conceptually, therefore, whilst the Central Banks might ‘manage' the markets, the very idea of their being able to eliminate the business cycle has always struck me as being a nonsense. The longer the contraction phase of a business cycle is postponed, the worse will be the excesses that build up, and the more painful will be the rectifying contraction phase.

There has been a disconnect in logic which has been seriously bothering me in recent weeks. Everything in my training has taught me that ‘the market' ultimately exerts a discipline on speculative excess, and ‘the market', being the sum of all players, is more powerful than any one player or set of players. Conceptually, therefore, whilst the Central Banks might ‘manage' the markets, the very idea of their being able to eliminate the business cycle has always struck me as being a nonsense. The longer the contraction phase of a business cycle is postponed, the worse will be the excesses that build up, and the more painful will be the rectifying contraction phase.

From another perspective, throughout history, the lesson of the markets has been that anyone who tries to “corner a market” will need to get his exit timing right. In a market which has been cornered, short term forces act in favour of the person doing the cornering. But, in the longer term , the market adapts. The shortage represents an arbitrage opportunity. Entrepreneurs react to this opportunity, organise their affairs, and supply comes flooding in. Usually too much supply comes in, because ‘everyone' can see the opportunity, and prices adjust downwards again.

That, in essence, is how market cycles work. Prices and volumes adjust and flex – from shortages to excesses and back again. The market breathes in and out – like a pair of lungs.

…. which brings us to the concept of barotrauma of the lungs.

Whilst I am not a doctor, a client of some years ago was a manufacturer of anaesthesia ventilators. It became necessary for me to understand the process of anaesthesia, which, in layman's language, works something like this:

When a patient is in an operating theatre pending surgery, he/she is typically rendered unconscious by the administration of a drug, and is also rendered ‘paralysed' by another drug. The purpose of inducing this paralysis is to avoid the possibility of involuntary movement whilst the surgeon is performing whatever intricate task he is doing. It is to avoid the ‘oops' factor.

The problem with paralysing the patient is that he is thereby rendered incapable of breathing for himself, so artificial ventilation is administered. A mixture of gases, including oxygen is ‘pumped' into the lungs. The lungs expand and the oxygen is thereby absorbed via the alveoli which are ‘forced' to open. Once this objective has been achieved, the lungs are allowed to contract again, like a deflating balloon, and carbon dioxide is expelled. During this artificially aided process, extreme caution needs to be taken in respect of the volume of air pumped into the lungs, and the pressure at which it is pumped. Too much volume at too high a pressure can give rise to rupturing of the lungs, and death of the patient.

Like the lungs, the economy absolutely needs to be allowed to breathe out. The economy needs to be allowed to contract, so that excesses might work their way through. If this were not so, excesses would build up ad infinitum. The way this contraction would happen – if there was no Central Bank – is that surpluses (say of speculatively built houses) will build up. The speculators will get stuck with them. The prices will fall. There will be some insolvencies. There will be some bad debts. Some capital will be wiped out. This will lead to a relative shortage of capital. The price of money will rise. Velocity of money will slow. The ‘recession' will feed on itself until the excess have all been washed out. Shortages will manifest. And the cycle will begin again.

Now think of a Central Bank as you would a ventilator, and ‘money' as the oxygen.

When there is a Central Bank waiting to ‘artificially interfere' with the natural breath expulsion process, ‘money' is pumped into the economy to keep it from collapsing and, theoretically, to allow it to deflate slowly and painlessly.

But what happens when you pump too much money in? What happens when, instead of allowing the economy to deflate slowly, the Central Bank tries to keep the economic cycle running at a ‘permanent' peak?

There should be price inflation.

Then, what should happen, is that the price of money should rise – to allow the money-lender the ability to earn a net positive return on his money. No one in his right mind will lend money at (say) 5% if the rate of inflation is (say) 6%. You would have to be insane to do that.

And yet, that is what seems to be happening. That is what has been seriously bothering me. Why have interest rates not been rising in the face of inflation?

The Government published numbers on inflation are a crock. You know that and I know that because we live in the real world. Petrol prices have risen. Grocery prices have risen. Rates on my property have risen. My electricity bill has risen. My contribution to medical aid insurance has risen and, last but not least, the politicians have voted themselves increases in salaries of greater than 5% in order to compensate for all this real world inflation that they tell us is under tight control.

Have a close look at the chart below, which is a chart of the yield on 30 year Treasury Bonds, courtesy decisionpoint.com :

Note how, in January 1999, both the yield chart and the PMO chart bottomed. Then, in early 2003, although the yield fell to a lower low, the PMO chart showed a non-confirming rising bottom. What it was showing was that the “rate” of decline in yields was slowing. Then, in mid 2005, the yield hit what was effectively a double bottom, and the PMO showed continuing rising bottoms. This was an indication that long dated yields should have begun their long march upwards in order the correct the prior excesses. The market was behaving in a healthy and normal fashion. It was positioning to allow for a healthy contraction in the economy.

Indeed, the 30 year yield did start to rise from that point. But look at how the PMO is rolling over again now – four months after the yield broke up through its 20 year downtrend line. That is not a healthy sign!

Now, let's take a step back. A 4.655% yield means that if you lend money to the US Government for thirty years , you will earn a return of 4.655% p.a. on that loan.

At last count (a month or so ago) the Federal Reserve Board of the USA was increasing money supply at the rate of 14% - 15% p.a. Inflation has to be running at higher than 5% p.a. Why would anyone lend at that rate?

Now, I would like to take the reader down another medical path; that of sleep. (No, I don't want to put you to sleep. J )

The following is a direct quote from an article that appeared in this morning's media

“WASHINGTON (Reuters) - A few nights without sleep can not only make people tired and emotional, but may actually put the brain into a primitive "fight or flight" state, researchers said on Wednesday.

Brain images of otherwise healthy men and women showed two full days without sleep seemed to rewire their brains, re-directing activity from the calming and rational prefrontal cortex to the "fear center" -- the amygdala.”

Source: http://news.yahoo.com/s/nm /20071024/hl_nm/sleep_emotions _dc_3;_ylt=AsprYyGRHO5u5kwKcInW F1hmMfQI

What's the relevance of this?

Well, quite by coincidence, here is another quote from another article in today's media:

“Forty-eight percent of Americans say they're more stressed now than they were five years ago, and the same percent report regularly lying awake at night because of stress, according to a new study by the American Psychological Association.

"Stress continues to escalate, and it's affecting every area of people's lives," said Russ Newman, a psychologist and executive director of the APA.

So what is it we're worrying about while we stare at the ceiling all night? Primarily two things: money and work, the main woes for nearly 75 percent of Americans. That's way up from 59 percent of us stressed out over those two things a year ago.”

Source : http://www.nypost.com/seven /10252007/news/nationalnews /stress_mess_in_u_s_.htm

So, we know that 48% of Americans are losing sleep over money, and we know that loss of sleep makes you irrational. And we also know that this irrationality is tightly related to “fear”. And we also know that when you are afraid, you are faced with two choices: Run away, or fight.

So, now the question can be asked:

If the general psyche of the market place is one of fear, and 75% of the American public is worried about money, what will investors be more likely to do? Will they aggressively throw money at the market, or will they run away from it, and towards safety?

To my way of thinking, if the fear that is welling up inside of sleepless Americans is going to suddenly morph into “irrational exuberance” as manifested by a third exponential blow-off leg in stock prices as “the market” clamours for stocks, then I would have to be a monkey's uncle.

The one thing we will not have is an exponential blow-off. I am now prepared to dig my heels in, and make that as a categorical statement. There will be no third up-leg of irrational exuberance.

So what will there be?

That leaves two choices.

- Orderly movement from high risk (high fear) to low risk (low fear).

- Panic movement from high risk to risk free (no fear).

The high risk markets (equities, property, commodities) will either move sideways to down, or straight down. Those are the two choices.

… which brings us back to barotrauma. If the Central Bank pumps too much money into the economy at too high a pressure, the economy may very well rupture.

What are the risks?

If people are becoming cautious, and they move their capital into Treasuries, and the Central Bank floods the markets with money that no-one wants, then interest rates must fall (along with the US Dollar). The Dollar must fall under circumstances where there is no incentive for foreigners to invest.

But this will cause inflation to escalate inside the US.

Thus, falling interest rates will be accompanied by rising prices, and the sleepless consumers will start to experience waking nightmares. Velocity of money will, of necessity slow down within the world's largest economy.

So, what is the ultimate “safety haven?”

Right now, the jury is out. But the chart below (courtesy stockcharts.com ) is starting to look suspiciously like it wants to break up through a triple top.

Should it do so, the measured move target based on horizontal count is 202 – which will be a new high. (This chart is a ratio of gold to the Commodities Index, $CCI).

But the irony is that gold seems to breaking down relative to oil.

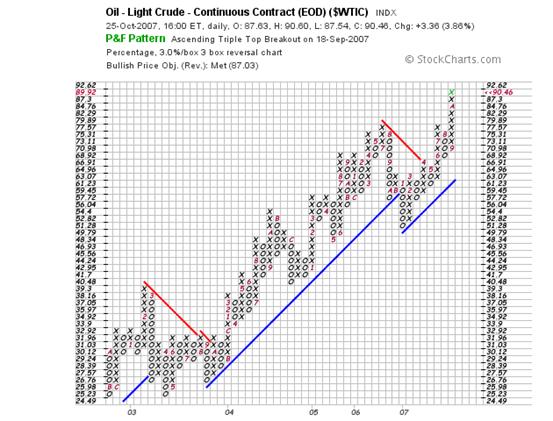

Notwithstanding this, readers are advised to be cautious here. As can be seen from the chart below, the oil price has reached its vertical count measured move, and has overshot its horizontal count measured move by 100%. Oil may be due for a pullback, and it may well be this pullback that causes gold to break out.

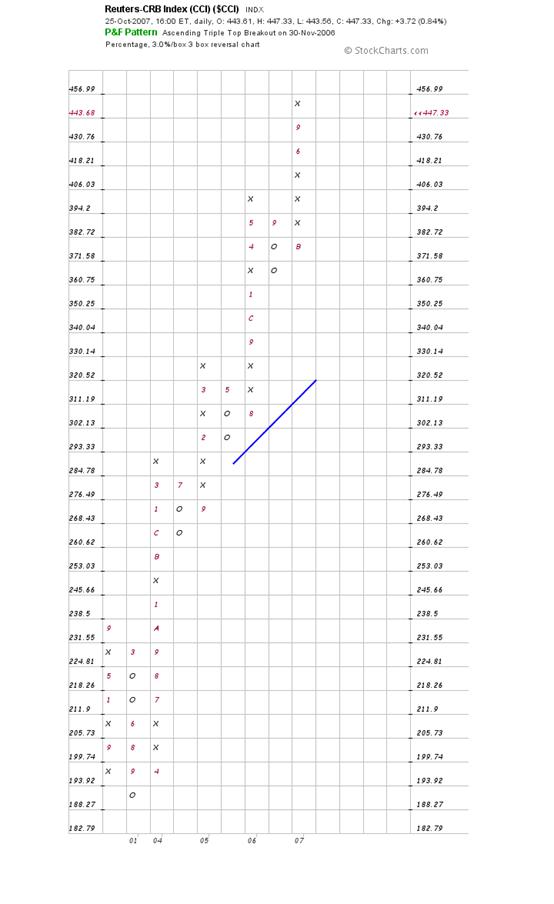

The chart below (of the $CCI on its own) has also reached 100% overshoot of its measured move count.

Finally, the chart below has given an unequivocal buy signal, which is showing evidence of investors having possible second thoughts.

Summary and Conclusions

Concurrent with market research which shows that the predominant emotion amongst US consumers is very likely to be fear, a move to investor safety seems to be occurring – given that long dated yields have been softening in the face of rising inflation.

The property markets are known to be softening. Further, it may well be that the commodity markets are reaching for a peak. Further, although the Dow Jones Industrial Index has recently given a buy signal, the market seems to be having second thoughts about this. (even though no signals have yet been given).

The definitive signal will likely be whether or not gold breaks up relative to commodities.

If gold does break up relative to commodities, this will be a negative development from the perspective of world economic health. It will likely demonstrate an emerging view that gold is “the” safe haven in turbulent economic times.

All of the above may ultimately reflect market barotrauma – caused by a pig headed insistence on the part of the Fed to keep pumping monetary oxygen into an economy which wants to breathe out.

The bottom line of all of this is that, except for special situations, I personally would not go anywhere near industrial equities.

By Brian Bloom

www.beyondneanderthal.com

Since 1987, when Brian Bloom became involved in the Venture Capital Industry, he has been constantly on the lookout for alternative energy technologies to replace fossil fuels. He has recently completed the manuscript of a novel entitled Beyond Neanderthal which he is targeting to publish within six to nine months.

The novel has been drafted on three levels: As a vehicle for communication it tells the light hearted, romantic story of four heroes in search of alternative energy technologies which can fully replace Neanderthal Fire. On that level, its storyline and language have been crafted to be understood and enjoyed by everyone with a high school education. The second level of the novel explores the intricacies of the processes involved and stimulates thinking about their development. None of the three new energy technologies which it introduces is yet on commercial radar. Gold, the element , (Au) will power one of them. On the third level, it examines why these technologies have not yet been commercialized. The answer: We've got our priorities wrong.

Beyond Neanderthal also provides a roughly quantified strategic plan to commercialise at least two of these technologies within a decade – across the planet. In context of our incorrect priorities, this cannot be achieved by Private Enterprise. Tragically, Governments will not act unless there is pressure from voters. It is therefore necessary to generate a juggernaut tidal wave of that pressure. The cost will be ‘peppercorn' relative to what is being currently considered by some Governments. Together, these three technologies have the power to lift humanity to a new level of evolution. Within a decade, Carbon emissions will plummet but, as you will discover, they are an irrelevancy. Please register your interest to acquire a copy of this novel at www.beyondneanderthal.com . Please also inform all your friends and associates. The more people who read the novel, the greater will be the pressure for Governments to act.

Brian Bloom Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.