Rightwing columnists stuff up labour market reform debate

Politics / Social Issues Oct 17, 2007 - 12:08 AM GMTBy: Gerard_Jackson

What gives with our so-called rightwing columnists? John Buchanan from the University of Sydney's Workplace Research Centre wrote, along with another lefty, a seriously flawed study on the alleged detrimental effects of government legislation that loosened our labour markets. So what did our intrepid conservative columnists do? They mocked Buchanan and his co-author and sneered at their politics. In brief, they attacked the man instead of the argument.

What gives with our so-called rightwing columnists? John Buchanan from the University of Sydney's Workplace Research Centre wrote, along with another lefty, a seriously flawed study on the alleged detrimental effects of government legislation that loosened our labour markets. So what did our intrepid conservative columnists do? They mocked Buchanan and his co-author and sneered at their politics. In brief, they attacked the man instead of the argument.

The brilliant Janet Albrechtsen started the ball rolling by exposing Buchanan's extreme leftwing views and his exhortation to Howard-haters “to take some inspiration from how Mao confronted a similar dilemma in the 1920s and early 1930s…” ( The Australian , Biased? Don't take our word for it 6 October 2007). If one really wanted the info on Mao Tse Tung's tactics then reading Mao: The Unkown Story would be the way to go. (Written by Jung Chang and Jon Halliday, Jonathon Cape, London, 2005). But it seems that Albrechtsen, like so many on our right, is really not that keen on homework.

Albrechtsen was no sooner off the mark than Andrew Bolt joined in the fun game of kicking lefties. Unfortunately, he, like Albrechtsen, only succeeded in revealing his total ignorance of the subject . (Bolt's Blog, Saturday 6 October). On the same day The Australian published an anonymous attack on Buchanan, the content of which did nothing to raise that paper's intellectual standard. ( It's hack-ademic: Comrade Buchanan's long march back to the red zone 6 October). Three days later Imre Salusinszky waded in with is two-pennies worth of observations. ( The intellectuals have gone too far , The Australian , 9 October). His contribution turned out to be on the same shoddy level as that of his mates Albrechtsen and Bolt.

So what is the subject to which I earlier referred to? Simple: It's called economics. This means that whenever a lefty makes an economic statement it should be met with economic theory. In the case of Buchanan we must ask one essential question: on what premise did he build his argument? Once again the answer is pretty straightforward: He built it on the notion of indeterminacy. Now indeterminacy is the belief that there exists a range of wage rates that would not influence the demand for labour. In other words, demand is inelastic. (In graphic form the demand curve would be vertical for the given rang).

Be that as it may, as journalists they are supposed to do their homework. As they seem somewhat retarded in this field allow me to help. (See, I'm not such a bad sort after all). Back to wage rate determination and economics as it really is. More than 100 years ago the eminent economist Phillip Henry Wicksteed wrote:

In like manner the individual entrepreneur, if he contemplates taking on or discharging a workman, will ask himself whether that workman will be worth his wage or not, i.e., whether he will increase the product, other factors remaining constant, at least to the extent of his wage; and he will take on more men as long as the last one earns at least as much as his wage, but no longer. The man, on his side, can insist on having as much as the marginal significance of his work, i.e., as much as the difference to the product which the withdrawal of his work would make. ( Essay on the Co-ordination of the Laws of Distribution , Macmillan & Co., 1894, p. 9).

This explanation is called marginal productivity theory and will be found in every economics textbook and every introductory course in economics. (Strictly speaking the wage rate is set at the point where the demand curve is crossed by the supply curve). What is not generally known is that the actual theory is more than a 170 years old. It was the brilliant Irish lawyer and economist Mountifort Longfield who first explained how capital accumulation raised real wages rates. As he put it:

...if a spade makes a man's work 20 times as efficacious as it would be if unassisted by any instrument, 1/20 only of his work is performed by himself, and the remaining 19/20 must be attributed to capital. And this is the measure of the intensity of the demand for such an instrument. A labourer working for himself would find it for his interest to give up 19/20 of the produce of his labour to the person who would lend him one, if the alternative was that he should turn up the earth with his naked hands; or if he worked for another, his employer might pay a similar sum for the purpose of supplying him with an instrument. But this profit [rate of return] is not paid, because on account of the abundance of capital in the country… ( Lectures on Political Economy , Richard Milliken and Son, 1834, p. 195)

Then there came Nassau William Senior who openly repudiated Ricardo's theory that wages were determined by the price of corn, preferring, and correctly so, a productivity theory., stating that

...the extent of the fund for the maintenance of labour depends mainly on the productiveness of labour. (Nassau William Senior, Political Economy , Richard Griffin and Company, 3rd ed. 1851, p. 183).

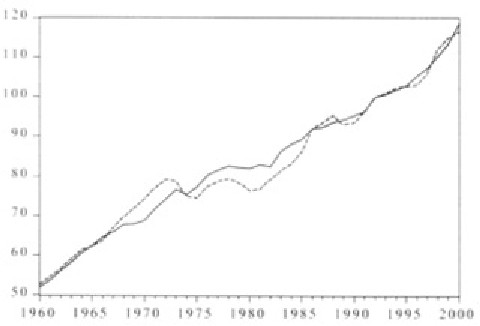

By the 1900s the theory was firmly established. Nevertheless, union advocates still argued, as does Buchanan, along the lines of indeterminacy. But Professor Fetter observed, somewhat sarcastically, that real wages in England had “increased ninety per cent in the thirty years between 1860 and 1891”. He then emphasized that unions could not have been responsible for this increase because in 1900 only about 10 percent of the labour force was unionised: he added, unless union supporters are prepared to argue “that one tenth of the labor supply fixes the value of all”. (Professor Francis A. Fetter, The Principles of Economics with Application to Practical Problems , New York, The Century Co., 1905, p. 130). The following chart clearly shows the connection between productivity and the trend in real wages.

|

| Labor productivivity and labor compensation 1960-2000. Productivity is output per hour of all persons in the business sector. Data from the Council of Economic Advisers 2001, cited in Douglas A. Irwin's Free Trade Under Fire , Princeton University Press 2002, p. 96 |

We can see that the marginal productivity theory of wage rates has a long and honourable lineage. So why does a socialist academic risk ridicule by basically denying the validity of marginal productivity theory? Because to concede to the theory would be to admit that unions cannot raise real wages for everyone. But no economist ever argued that they cannot raise them for their members — or at least those who get to keep their jobs. Arthur Smithies pointed out:

Concerted action by the whole labour movement to increase money wages will leave real wages unchanged. Real wage gains by a single union are won at the expense of real wages elsewhere. (Effective Demand and Employment, in Harris ed., The New Economics , p. 561, cited in Willam H. Hutt's The Keynesian Episode: A Reassessment , LibertyPress, 1979, p. 267).

Therefore, even if Buchanan's figures are accurate they do not support his case against free labour markets. On the contrary, they actually strengthen the free market case. (That our conservative attack dogs failed to spot this leaves me with the thought that they must be getting their economic advice from the discredited H. R. Nicholls Society). The German statistician E. Altschul was surely right when he wrote:

“In economics especially, the final phenomenon can never be left to mathematical and statistical analysis. The main approach to research must necessarily lie through theoretically obtained knowledge”. A. C. Pigou fully concurred when declared: “The absence of statistical correlation between a given series of changes and industrial fluctuations does not by itself disprove — and its presence does not prove — that these changes are causes of the fluctuations”. (F. A von Hayek Monetary Theory and the Trade Cycle , Augustus M. Kelley Publishers, 1975, p. 31).

And economics provides us with the necessary “theoretically obtained knowledge” to expose Buchanan's economic fallacy that wage rates are indeterminate and this means that unions are needed to prevent the exploitation of labour by forcing wages rates up to the maxim point on the demand curve. (The maximum point is the one beyond which demand becomes elastic, ie., sensitive to wage rates).

Firstly, if unions force wage rates above the value of the worker's marginal product unemployment will emerge. However, if there are union-free lines of production then the unemployed will flow into these, thereby exerting a downward pressure on wage rates. If this situation is allowed to continue expect to see a rise in part-time employment and more labour intensive production. Thus the difference in wage rates between the same type of labour can be seen as the result of unions raising wages above their market-clearing rates.

Even if indeterminacy was the norm unions would still not be needed to protect wages. Theory and experience clearly show firms will continue to hire workers until it becomes unprofitable to do so. In a world in which indeterminacy reigned employers would compete against each other for labour until wage rates reached the maximum point on the curve. The reason is simple: the difference between the wage rate and the maximum is profit. By hiring more people capitalists therefore make more money. The idea that a capitalist would turn his nose up at more profits and allow his competitors to price him out of business is something so ridiculous that not even Buchanan would believe it.

Buchan and his lefty mates get away with their nonsense because our conservative columnists are at a complete loss on how to deal with economic arguments. This is why their attacks on Buchanan got very little support from their readers. The problem is that these columnists do not seek advice from outside their own little closed shop. This is why , for example, Andrew Bolt made a ludicrous appeal for ethanol subsidies, a mistake that a first year undergraduate would not have made. And it is why Albrechtsen supported the NSW ALP's attack on free labour markets*. Because of their incompetence Buchanan has been turned into a leftwing martyr.

Things are not going to improve until this bunch of know-alls realise their limitations and start seeking expert advice when it is needed — especially in the field of economics.

* How conservative columnists damage the free market case

Minimum wages and capital accumulation: lefty economists fail again

The Australian Council of Trade Unions gets it wrong on labour market deregulation

The economic illiteracy of the media

By Gerard Jackson

BrookesNews.Com

Gerard Jackson is Brookes' economics editor.

Gerard Jackson Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.