Systematic Threat to Global Financial System - The Fingers of Instability, Part 9

Stock-Markets / Credit Crunch Oct 16, 2007 - 09:49 AM GMTBy: Ty_Andros

In This Issue – 3 Fingers of Instability

- Marking to Myths!

- Keeping the Illusions Front and Center

- Bodies Beginning to Float to the Surface…And They Are WHALES!

Series Introduction – Click Here

Things are unfolding in an interesting manner and it is the ebb and flow of the issues into and out of the financial Media's reporting of them that provide us with the true picture as it merges. This week several VERY INTERESTING articles allowed us a better picture on the enormity of this Systemic threat to the global financial systems of the G7. The enormous lengths the authorities are going to in order to keep the enormity of the problem from hitting “THE HEADLINES”. It is now becoming clear that new cockroaches are emerging in the biggest money center banks in the world and they are “STUCK” in the “ROACH MOTELS” (see Ted bits archives at www.TraderView.com ) of their own making.

Things are unfolding in an interesting manner and it is the ebb and flow of the issues into and out of the financial Media's reporting of them that provide us with the true picture as it merges. This week several VERY INTERESTING articles allowed us a better picture on the enormity of this Systemic threat to the global financial systems of the G7. The enormous lengths the authorities are going to in order to keep the enormity of the problem from hitting “THE HEADLINES”. It is now becoming clear that new cockroaches are emerging in the biggest money center banks in the world and they are “STUCK” in the “ROACH MOTELS” (see Ted bits archives at www.TraderView.com ) of their own making.

The solutions they are proposing are to allow the roach motels to survive by creating a “SUPER” Roach motel to service the existing ones. The participants are doing so in an act of self preservation. These activities are creating opportunities of enormous proportions, are you prepared to benefit from them?

For greater insight into our publication, have a look at the Overview of Tedbits . It helps current and potential subscribers understand our mission in serving you. It also gives a broad description of what's unfolding globally and what you can expect from Tedbits as a regular reader.

Marking to Myths!

As Alan Greenspan created the greatest bubbles in history during his tenure as Federal Reserve Chairman there was one consistent element common to them all. “FIAT CURRENCIE AND CREDIT CREATION” in accordance with the public servants who wished to MILK the citizens of their money through the printing press and through the improper “Asset” inflation which generated always increasing tax revenue from inflation of incomes and investments. This fueled their reelections and allowed them to grow government far in excess of its benefits under the cover of these activities.

We all aware how financial “PAPER” based wealth has skyrocketed during the last 7 years. This is a direct result of the need to create “INVESTMENTS” for all the money that was created to prevent deflation resulting from the bear stock markets of 2000-2002, (and previous money printing exercises such as Y2k, the Russian debt crisis and ad infinitum during the career of Alan Greenscam, er Greenspan). This demand is what fueled the development of the “OVER THE COUNTER” derivatives and structured products that are “part and parcel” of the biggest investment portfolios in the world. It not only the G7 banking systems that are in trouble, but the institutions, pension funds, and investors which bought the products and face losses of up to 100% on investments they were told were of high quality. The only solution for the problem is what else? Printing money faster than it can DISAPEAR! I hope you all have some gold in your portfolios.

First let's define the amount of investments which can't be priced, are illiquid and have very few places, if any, where you can exit them. These investments have a wide variety of quality, but mainly are the progeny of the largest money center and investment banks in the world. These investment houses and banks have gone through the greatest bull markets in the history of their businesses and a bear market is directly in their futures. This is an overview of the “Dollar Value” of the products they have created to overcome the loss of their IPO revenue streams which were losses when the 1982-2000 Bull market ended:

![[Chart]](../images/Ty_Andros_16_10_07_image001.gif)

Notice when the issuance of these investments began to skyrocket? Just as the Federal funds rate was nearing 1% in 2001. At that point a fine arbitrage opportunity was set to begin as banks and investment managers were able to buy long duration investments such as mortgages and bonds and finance them with very short borrowing from money markets.

The magic of fractional banking and leverage allowed them to borrow “short term” money cheaply and buy/lend Long Term on higher yielding investments. But the Federal Reserve was not the only source of cheap funds for these arbitrage opportunities. The other source was the JAPENESE yen, as interest rates there were effectively “ZERO” as deflation was then, as it is now, firmly entrenched since the last asset backed economy ran off the rails in Japan in 1989-1990! With these two sources of capital “carry trades” have become the main stream investment technique for the “money center and investment' banks of the G7. They quit making money the “OLD FASHIONED” way as Smith Barney used to say and embarked on the STAR TREK model of investing. To go “where no man has gone before” and the hope of financial alchemy “turning lead into gold” was revived for the umpteenth time in the history of man.

When Greenspan and Japan effectively lowered interest rates into negative territory (inflation at 3% and interest rates at 1% = 2% negative interest rates) investment plans around the world were thrown into turmoil. Negative interest rates compounding at a rate of 1 percent a year are very unattractive so it challenges the investors to reach for yields which entail poorer risk return ratios. Investors which had been very comfortable buying highly rated bonds which yielded 6 to 8% over the last twenty years or more suddenly couldn't do it. Using the rule of 72 to determine how long it took to double using compounding we know at 6% an investment doubles every 12 years, at 8% every 9 years, and at 9 it doubles 8 years. For the biggest money in the world such as retirement funds, institutions and insurance companies which only wants the return of their money with a return of 2% after inflation, these bonds represented safe and actuarial predictable returns. With 1 percent interest rates those returns increasingly evaporated, when a government or AAA rated bond only garners 4.5% the time span zooms to 16 years. At first the long end did not crumble, and “Longer term” returns stayed decent, but as the trade and budget deficits of the G7 grew and they printed the money to pay for them, so did the numbers of bidders for the safest categories of investments so the conundrum of low long term bond interest rates was created as it got very crowded as bidders tried to stay safe.

The more billions and trillions were printed and created the lower to return on them as they were widely available. The more money available for capital investment the lower the returns you (or the lender) can expect, when money is scarce returns for capital are higher. These currency holders eventually were forced into riskier investments and Wall Street “ENGINEERED” them due to the incredible demand for them. Structured products were born!

When you solve problems for large numbers of people you get paid a lot. The more problems you solve the more you are paid. It's as simple as that, look no further than Microsoft to see what you are paid for solving problems. The Money center and Investment banks solved the problems for investors who held something widely available “infinite amounts of fiat currencies” and increased the returns on it. They disguised the risks in opacity, illiquidity, complexity and in concert with the ratings agencies which succumbed to the siren song shareholders for “MORE PROFITS”. Real inflation was running away while reported inflation was low so public servants could “COVER UP” their irresponsibility.

The structured products they created were testaments to the power of the personal computer and “MATHEMATICAL” modeling based on assumptions of past behavior. However, the past behaviors were from a time when irresponsible spending by the public and governments were generally regulated by responsible banks and the market place which had to really know who and for what they were lending. Now lending is designed for the lowest common man and the highest return on the lending. So the borrowers are all over the spectrum from responsible to highly irresponsible.

This reduction in lending standards required that they become packaged in securities in which good and bad can be packeaged together, if they couldn't be then the coupons couldn't get to the high level sought after by the lenders. So they created investment sausages which had all ![[chart]](../images/Ty_Andros_16_10_07_image002.gif) manner of loans in them: corporate bonds, Municipals, commercial mortgage backed securities, high yield bonds, mortgage backed securities, leveraged loans, collateralized loan obligations (private equity, share buybacks, M & A, etc.), asset backed securities, credit card receivables, CDO's/structured credits, etc. All of these and more were incorporated in the securitized structured products to blend the yields to higher levels and to disguise much of the “lending” trash being included in them.

manner of loans in them: corporate bonds, Municipals, commercial mortgage backed securities, high yield bonds, mortgage backed securities, leveraged loans, collateralized loan obligations (private equity, share buybacks, M & A, etc.), asset backed securities, credit card receivables, CDO's/structured credits, etc. All of these and more were incorporated in the securitized structured products to blend the yields to higher levels and to disguise much of the “lending” trash being included in them.

These securities were bought by large investors, institutions, pension funds, hedge funds, etc. and off bank balance sheet investment vehicles such as SIV's (Structured Investment vehicles) and Conduits. Most of the buyers bought them for the yield and implied safety of the ratings they were given by the ratings agencies. But many were taken into the carry trade and leveraged for additional returns. The carry trade is where you borrow money at 1 percent and buy an asset that yields 4 to 15% and pocket the difference. It can be done with currencies only or the buy side can include almost anything such as stocks, bonds, structured products, emerging market bonds, corporate bonds, or anything that promises a high rate of return over the low cost of borrowing.

The buy side can have lots of twists and turns as many may be denominated in foreign currencies which may fluctuate, or the buy side can have a lot of capital risk as they could fail and the money to repay the low cost borrowing is lost (this is what's happening now). And that is were we find ourselves now as lending standards have collapsed in New York and the world the value of the products sold are questionable as there is no exchange in which to discover their current value. To see how illiquid and undiscoverable these values are take a look at what investors in these problem products are reporting when they try and establish their value:

The values of these “structured” products is undiscoverable as to price them is impossible. What do you do? Call the bank desks and get a quote? One mans treasure becomes another mans trash during this exercise. However since they vary according to what's in them and that is unknowable they all move into the trash column.

The Wall Street Journal reports (www.wsj.com):

“During this summer's credit crunch, more than 80% of investors in bonds tied to the mortgage market said they had trouble obtaining price quotes from their bond dealers, according to a survey of 251 institutional investors by Greenwich Associates, a Connecticut consulting firm.

J.P. Morgan Chase & Co. analyst Kedran Panageas estimates that 29% of lower-quality "collateralized debt obligations" -- thinly traded investments that package pools of loans -- will eventually lose all of their value due to the recent mortgage shakeout. In the case of quality CDOs, she estimated, 12% will be reduced to zero. The lost value, she says, represents roughly $85 billion of the $475 billion of such securities outstanding. So far, she believes investors have recognized only a fraction of those losses.”

Earlier this year Wall Street saw what was unfolding and created a new way of valuing these products so their malfeasance would be further obscured from the public and investors; they devised the tier system so their values could become more subjective, let's take a look:

This is where they have moved the losses to, level three. This is why the losses have not been reported, in their BEST JUDGEMENT these holdings will recover (p.s. do you believe in the tooth fairy as well). A tsunami of Sub prime bombs er bonds were downgraded by Moody's this week: the Wall Street Journal reports:

“Moody's Investors Service slashed credit ratings on about 2,000 bonds backed by subprime home loans that were originally valued at $33.4 billion, in its largest wave of downgrades. The New York ratings company said it doesn't expect another bigger round of cuts for such bonds unless conditions in the housing market deteriorate significantly.”

Moody's yesterday placed an additional $23.8 billion in first-lien subprime bonds on review for downgrades, including 48 securities that have the top Aaa rating and 529 with the next-highest Aa rating. The rating service said these ratings aren't expected to be lowered significantly.

Nicolas Weill, Moody's chief credit officer for structured finance, said the latest actions were taken after a "complete review" of subprime-mortgage bonds that were issued in 2006, adding that there should be "a fair amount of rating stability going forward."

Moody's said there has been a steady deterioration in the performance of subprime loans that were made in 2006 as home prices have continued to decline. But it noted that as long as home prices don't fall by more than 10%, and the economy remains steady, the bulk of its subprime bond ratings should be stable. According to its data, home prices have fallen 4.5% to 5% from their peak.

The latest cuts are expected to spill over to many collateralized debt obligations, or CDOs, that bought subprime-mortgage bonds last year and repackaged them into new securities that were sold to investors world-wide.

A significant number of CDOs hold mainly subprime bonds that originally had weaker credit ratings of A and Baa. Many of these securities have been downgraded to junk, or high-yield, ratings, and some bonds have suffered principal losses because of high defaults among the underlying loans. Some CDOs are being reviewed for rating downgrades.”

What? As long as home prices don't fall 10%? Improbable? Ask anyone selling a home if they would take a 10% lower price from a year ago. I promise you it would be 100% takers, so the losses have only begun to be realized so….

Keeping the Illusions Front and Center

The minutes of the Federal reserves most recent meeting were released and it is very clear they were heavily scrubbed. They didn't even discuss whether to cut .25%, its clear that in private briefings from the Treasury that they have been told of the coming vaporization of bank reserves. Anyone holding any of the assets listed in the previous Tedbit is heading for a haircut in the value of their holdings and that includes banks and their thinly disguised “OFF BALANCE SHEET” hedgefund operations known as SIV's and conduits. So its man the lifeboats for the Banks, a steepening of the yield curve is exactly what the doctor ordered for lenders who hold assets that yield 4 to 5% and short term rates are above these holdings.

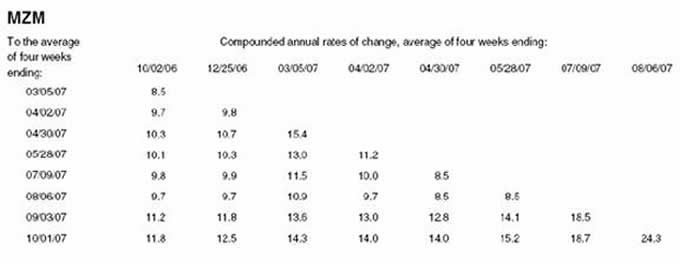

If you wish to know why the stock market is still rising look no further than MZM and its rate of growth:

Wow, 24.3% growth in Money with zero maturity over the last 4 weeks? And 18.7% for the 3 rd quarter. Can you say money printing and plunge protections team ammunition? The reason is simple, it is becoming quite obvious that the biggest bank in the world is….

Bodies Beginning to Float to the Surface…And They Are WHALES!

Floating to the surface, as they are leading to form a consortium to meet the short term funding needs of their off balance sheet Conduits and SIVs. Who is this behemoth with branches on every street corner around the globe? CITIGROUP!

This is the stuff of crashes as the world grapples with the illiquid mess that is OVER THE COUNTER “structured products”, we learn that Citigroup does not have the capacity to meet the needs of its SIV's and Conduits. So it is leading an effort to create a “SUPER CONDUIT” called the “master liquidity enhancement” fund to meet the funding needs of these poorly structured carry operations and their bank sponsors. Here's a small glimpse of bank conduits and SIV's that are out on the limb together, as the buy side of their holding are crumbling and they can't access the critical ![[table]](../images/Ty_Andros_16_10_07_image007.gif) short term funds they need:

short term funds they need:

There are dozens of hedge funds operating with the SIV and conduit business model enhanced with leverage. The Wall Street Journal Reports:

In a far-reaching response to the global credit crisis, Citigroup Inc. and other big banks are discussing a plan to pool together and financially back as much as $100 billion in shaky mortgage securities and other investments.

The banks met three weeks ago in Washington at the Treasury Department, which convened the talks and is playing a central advisory role, people familiar with the situation said. The meeting was hosted by Treasury's undersecretary for domestic finance, Robert Steel, a former Goldman Sachs Group Inc. official and the top domestic finance adviser to Treasury Secretary Henry Paulson. The Federal Reserve has been kept informed but has left the active role to the Treasury.

The new fund is designed to stave off what Citigroup and others see as a threat to the financial markets world-wide: the danger that dozens of huge bank-affiliated funds will be forced to unload billions of dollars in mortgage-backed securities and other assets, driving down their prices in a fire sale. That could force big write-offs by banks, brokerages and hedge funds that own similar investments and would have to mark them down to the new, lower market prices.

The ultimate fear: If banks need to write down more assets or are forced to take assets onto their books, that could set off a broader credit crunch and hurt the economy. It could make it tough for homeowners and businesses to get loans. Efforts so far by central banks to alleviate the credit crunch that has been roiling markets since the summer haven't fully calmed investors, leading to the extraordinary move to bring together the banks.

Secret meetings? Three weeks ago? Two days before the FOMC meeting! Scrubbed FOMC minutes. Connect the dots… Can you say government condoned and facilitated cover up? Of course they are only planning to rescue the banks. Now we know how Bear Stearns and Lehman brothers miraculously had very few losses to report. People who bought and hold the CDO's, CMO's, MBS's, and other structured products also face huge write downs as well. Remember Enron, Refco, and MCI? Their bankruptcies were all centered around OFF BALANCE SHEET operations. Think of it, an off balance sheet entity to hide losses of an off balance sheet entity, only in the land of Georg e Orwell and the G7 could things like this be created. A super conduit to hide the walking dead Mortgage backed securities, why? So they can have the time to find some other poor fool to buy them and hopefully restart the money “printing” train aka securitized products of all types.

Citigroup looks like it wants to join this hall of shame. But, they have one big thing on their side. They are TOO BIG to fail. They are in virtually every country in the world. They would make Northern Rock a foot note. Can you imagine seeing bank runs in every major city in the world? Well, the financial authorities can so they will do what else? THEY WILL PRINT THE MONEY.

In conclusion: The credit crunch continues and the only solution they (G7 financial authorities) know is printing the money. It is inculcated into their DNA. This is a fabulous opportunity for those investors that play in the tier one playing field and a night mare for those who inhabit tier three. The 100 billion dollar super fund will just allow the biggest players to POSTPONE paying the price for their previous follies (but it is not going to recover the losses, those will not disappear, those people who owe the money in those products WILL NOT PAY, reckoning day will arrive). As we all know the Money and Investment banks have friends in high places. But that is only the banks, as Moody's and S&P are FORCED to write down the value of the securitized products: institutions, pension funds, insurance companies, mutual funds, etc. will all have to write down the value of their investment holdings, and the write downs look to be enormous. The next reflation of the financial system has commenced in size, the “Crack up boom” (see archives at www.TraderView.com ) is still in the long term horizon.

Citigroup has just announced its earnings and abra cadabra, they beat the street at .47 cents versus .44 cents, is anyone surprised? Tier three massages any and all financial shenanigans and investors are turned into mushrooms in the dark and fed BULL****! Crude oil is at $85 dollars a barrel and Turkey is about to invade northern Iraq . Do you think there may be a little volatility emerging? Volatility is opportunity for the prepared investor.

Think of Moody's statements about losses, these people are in on the gaming of the expectations. Is this an opportunity or a pitfall for your portfolio? Currencies, interest rates, stock indexes, commodities, precious metals will all offer opportunities to the prepared as this unfolds. These assets are all examples tier one markets, liquid, transparent, and well regulated exchange traded markets.

This is an enormous “Finger of Instability”, but will move many markets and provide lots of opportunities, are you ready to capture them or be victim of them? This has been a great mental exercise, just like CSI (crime scene investigation) but in real life: the world economy and financial community is the crime scene. We see its fingerprints in the markets we have outlined and I promise you its fingerprints are written in many other markets. Ask yourself, am I going to be a victim of what's unfolding or are these opportunities that I am prepared to catch in my portfolio? If not, why not? Thank you for reading Ted bits, if you enjoyed it send it to a friend and subscribe its free at www.TraderView.com , don't miss the next installment of “Fingers of Instability”.

Ty Andros & Tedbits LIVE on web TV. Don't miss Ty interviewed live by Michael Yorba from Commodity Classics every week discussing this week's commentary and unfolding news. Catch the show every Wednesday at www.MN1.com or www.CommodityClassics.com at 4:15pm Ce ntral Standard Time . Archived video casts are available there as well.

If you enjoyed this edition of Tedbits then subscribe – it's free , and we ask you to send it to a friend and visit our archives for additional insights from previous editions, lively thoughts, and our guest commentaries. Tedbits is a weekly publication.

By Ty Andros

TraderView

Copyright © 2007 Ty Andros

Hi, my name is Ty Andros and I would like the chance to show you how to capture the opportunities discussed in this commentary. Click here and I will prepare a complimentary, no-obligation, custom-tailored set of portfolio recommendations designed to specifically meet your investment needs . Thank you. Ty can be reached at: tyandros@TraderView.com or at +1.312.338.7800

Tedbits is authored by Theodore "Ty" Andros , and is registered with TraderView, a registered CTA (Commodity Trading Advisor) and Global Asset Advisors (Introducing Broker). TraderView is a managed futures and alternative investment boutique. Mr. Andros began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Di ego , and the University of Miami , majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis, creating investment portfolios designed to capture these unfolding opportunities as the emerge. Ty prides himself on his personal preparation for the markets as they unfold and his ability to take this information and build professionally managed portfolios. Developing a loyal clientele.

Disclaimer - This report may include information obtained from sources believed to be reliable and accurate as of the date of this publication, but no independent verification has been made to ensure its accuracy or completeness. Opinions expressed are subject to change without notice. This report is not a request to engage in any transaction involving the purchase or sale of futures contracts or options on futures. There is a substantial risk of loss associated with trading futures, foreign exchange, and options on futures. This letter is not intended as investment advice, and its use in any respect is entirely the responsibility of the user. Past performance is never a guarantee of future results.

Ty Andros Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.