Global Geopolitical Dislocation and the Worldwide Financial Crisis

Politics / Global Debt Crisis Nov 17, 2010 - 10:45 AM GMTBy: Global_Research

As the LEAP/E2020 team anticipated in its open letter to the G20 leaders published in the international edition of the Financial Times of 24 March 2009, on the eve of the London Summit, the question of a fundamental reform of the international monetary system is central to any attempt to solve the current crisis.

As the LEAP/E2020 team anticipated in its open letter to the G20 leaders published in the international edition of the Financial Times of 24 March 2009, on the eve of the London Summit, the question of a fundamental reform of the international monetary system is central to any attempt to solve the current crisis.

But sadly, as was demonstrated again at the failure of the G20 summit in Seoul, the window of opportunity for achieving such a reform peaceably closed at the end of summer 2009 and will not open again before 2012/2013 (1). The world is indeed in the throes of the global geopolitical dislocation that we had announced as beginning at the end of 2009 and which can be seen, less than a year later, in the proliferation of movements, the economic woes, the fiscal deficits, the monetary disagreements, all setting the scene for major geopolitical shocks. With the G20 summit in Seoul, which signalled to the planet in its entirety the end of US domination of the international agenda and its replacement by a generalised mood of “every man for himself”, a new phase of the crisis has begun, prompting the LEAP/E2020 team to issue a new warning. The world is about to breach a critical threshold in this phase of global geopolitical dislocation. And as with every breach of threshold in a complex system, this will generate, as from the first quarter of 2011, a suite of non-linear phenomena: developments that do not conform to the usual rules and the traditional projections, be they economic, monetary, financial, social or political.

In this GEAB N°49, in addition to the analysis of the six main steps marking the breach of this critical threshold of the global geopolitical, our team presents numerous recommendations to help cope with the consequences of this new phase of the crisis. They address, for example the currency/interest rates/gold and precious metals group; wealth preservation and the replacement of the US dollar by another measure of net worth; the bubbles in asset classes denominated in US dollars; and the stock markets and the most vulnerable corporate categories in this phase of the crisis. The LEAP/E2020 team also presents the “three simple reflexes” to adopt to understand and anticipate better the new world taking shape. Also in this issue, our team describes the double Franco-German electoral shock in store for 2012/2013. And we also present an excerpt from the Manual of Political Anticipation, written by the president of LEAP, Marie-Hélène Caillol, and published by Anticipolis in French, English, German and Spanish.

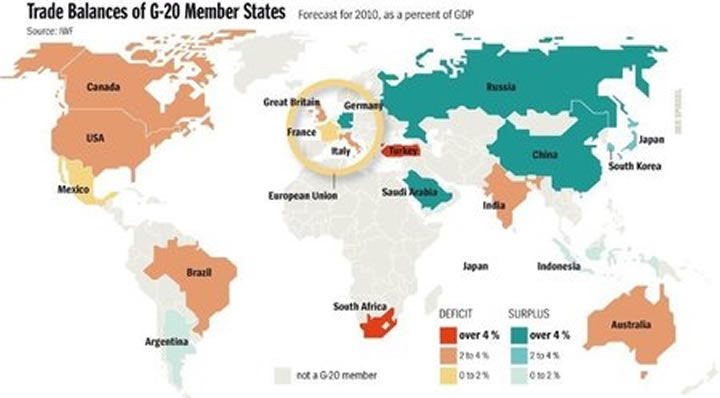

Trade balances of the G20 countries (forecast for 2010) - Source: Spiegel, 11/2010

The crisis that we are experiencing is characterised by developments on a planetary scale, taking place at two levels that, while correlated, are different in nature. On the one hand, the crisis is symptomatic of the profound changes to our world’s economic, financial and geopolitical reality. It accelerates and amplifies the underlying trends that have been at work for several decades, trends that we have described regularly in the GEAB since its launch at the beginning of 2006. On the other hand it reflects the steadily increasing collective awareness of those changes. This growing awareness is in itself a phenomenon of collective psychology on a global level and it influences the way the crisis develops and triggers sharp bursts of speed in its evolution. Several times in recent years, we have anticipated “inflexion points” in the crisis, corresponding to “sudden leaps” in this collective awareness of the changes under way. And we consider that all the pre-requisites for “rupture” crystallised around the G20 summit in Seoul, enabling a crucial advance in collective awareness of the global geopolitical dislocation. It is that phenomenon that led LEAP/E2020 to identify the breach of a critical threshold and to issue a warning about the consequences of that breach as from the first quarter of 2011.

Around the date of the G20 summit in Seoul, LEAP/E2020 identified a build-up of events likely to lead to “rupture”. Let us examine the main events concerned (2) and their chaotic consequences.

Concluding the quantitative easing: the Fed placed under “house arrest”

The Federal Reserve’s decision to launch “QE2” (by purchasing USD 600 billion of US Treasuries from now to 2011), triggered an outcry, for the first time since 1945, amongst almost all the other global powers: Japan, Brazil, China (3), India, Germany, the ASEAN countries (4), …(5) It is not the Fed’s decision that marks a rupture: it is the fact that for the first time, America’s central bank had its ears boxed by the rest of the world (6), and in a very public and determined manner (7). This is certainly not the cosy atmosphere of Jackson Hole and the central bankers’ meetings. It seems that Ben Bernanke’s threats to his colleagues, conveyed to our readers in GEAB No. 47, did not have the effect that the Fed’s chairman had hoped. The rest of the world made it clear in November 2010 that it had no intention of letting the US central bank continue printing US dollars at will in an attempt to solve America’s problems at the expense of every other country on the globe (8). The dollar is now getting back to being what every national currency is supposed to be: the currency and thus the problem of the country that prints it. In fact, in these last weeks of 2010, we have witnessed the end of an era where the dollar was the currency of the US and the problem of the rest of the world, as John Connally put it so neatly in 1971, when the US unilaterally terminated the convertibility of the dollar into gold. Why? Simply because from now on the Fed must take into account the opinion of the outside world (9). It is not yet under guardianship, but it is under “house arrest” (10). According to LEAP/E2020, we can already anticipate that there will be no QE3 (11) regardless of the US leaders’ opinions on the subject (12); or it will take place at the end of 2011 to the tune of major geopolitical conflict and the collapse of the US dollar (13).

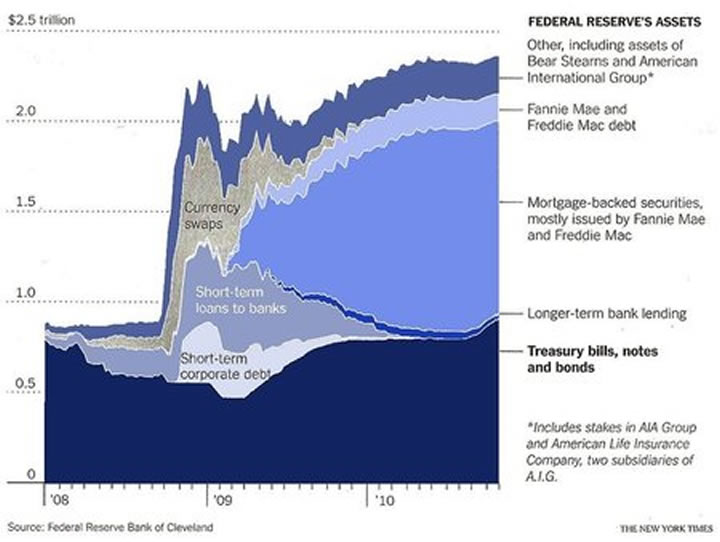

U.S. Federal Reserve’s Assets (2008-2010) – Sources: Federal Reserve of Cleveland / New York Times, 10/2010

From Paris to Berlin (14), Lisbon to Dublin, Vilnius to Bucharest, London to Rome,… the protest marches and strikes are spreading. The social dimension of the global geopolitical dislocation is clearly visible in the Europe of end-2010. While these events have not yet managed to disrupt the austerity programmes planned by the European governments, they point to a significant collective development: public opinions are emerging from their torpor at the beginning of the crisis, suddenly aware of its duration and cost (social and financial) (15). So the next elections should prove costly for all the current political teams who have forgotten that without fair treatment, austerity will never win popular support (16). In the meantime, the teams in office are still applying the recipes of the pre-crisis period (i.e. neo-liberal solutions based on tax cuts for the richest households and an assortment of higher indirect taxes). But the rise in social disputes (inevitable according to LEAP/E2020) and the policy changes that will emerge in the next national elections, country by country, will lead to a questioning of those solutions; and a dramatic strengthening of the populist and extremist parties (17): Europe is going to get politically “tougher”. In parallel, in view of what looks increasingly like an unconscious desire on the part of the baby-boomers to have younger citizens shoulder their costs, we can expect to see an increase in violent reactions from the rising generations (18). According to our team, they will probably become more radical if they feel that the situation is hopeless, unless a compromise can be reached. But without an improvement in tax receipts, the only compromise credible in their eyes would be cuts in existing pensions, rather than higher education costs. Today is always a compromise between yesterday and tomorrow, particularly when it comes to taxes. And the most likely fiscal consequences of these developments are higher taxes on high earnings and capital gains, a new bank tax and a new, community-wide drive to protect the borders (19). The EU’s trade partners should take rapid note (20).

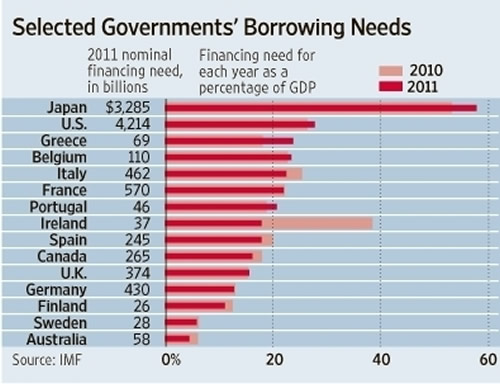

Selected governments’ borrowing needs (2010-2011) - Sources: FMI / Wall Street Journal, 10/2010

Japan: the latest efforts to resist China’s power

For several weeks now Tokyo and Beijing have been locked in a diplomatic dispute of rare intensity. Under various pretexts (a Chinese trawler about to enter Japanese territorial waters (21), massive Chinese purchases of Japanese assets, causing the yen to appreciate) the two powers exchanged harsh words, suspended their high-level talks and appealed to international public opinion. To the countries in the region, the international visibility of this Sino-Japanese spat is especially revealing because of a glaring absence –that of the US. While these quarrels clearly illustrate Beijing’s growing determination to be recognised as the dominant power in East and South-East Asia and Japan’s bid to oppose that regional Chinese hegemony, there is no denying that the power supposed to dominate in this region of the world since 1945, namely the US, is strangely absent from table. We can therefore assume that what we are witnessing is a real-life test on China’s part to measure its new influence on Japan; and on Japan’s part to evaluate how much scope for action the US still has in Asia, faced with China. The events of recent weeks have shown that, hampered by political paralysis and its economic and financial dependence regarding China, Washington prefers not to get involved. No doubt throughout Asia this spectacle serves to accelerate the awareness that a new milestone has been passed in terms of regional order (22); and that in Japan, mired in an endless recession (23) the economic interests linked to the Chinese market have not been strengthened by the experience.

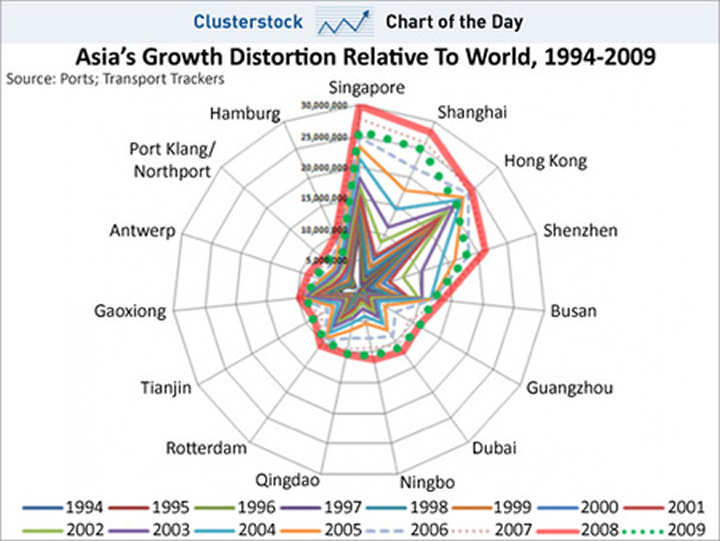

Global changes under way – massive growth in world port traffic, benefiting Asia (1994-2009) - Sources : Transport Trackers / Clusterstock, 10/2010

Notes:

(1) These dates correspond particularly to the period when most of the leaders of the major G20 countries are renewed. This is a necessary condition (though clearly not sufficient, since nothing is guaranteed, even after 2012/2013: it will simply be a new window of opportunity) if there is to be any hope of achieving a concerted approach and commitment to reforming the global monetary system. In the meantime, according to LEAP/E2020, we shall see nothing more than failed attempts and/or tests of unrealistic ideas prior to this virtually total overhaul of the world’s leadership. And amongst the ideas that will never get off the ground is a proposal to regulate exporting countries’ surpluses. It comes from a country in dire commercial straits, or more precisely, in a position of weakness, and so without any chance of being heard. Its relevance (highly doubtful, as the Asia Times of 27/10/2010 emphasises) is apparently not the point. Concerning the 2012/2013 window of opportunity, see the previous GEABs and the anticipations and scenarios outlined in Franck Biancheri’s « World crisis, the path to the world afterwards » for more on this theme. Source: Anticipolis.

(2) GEAB subscribers had already anticipated these for several months.

(3) With inflation officially rising to 4.4% (setting a two-year record), Beijing is not going to sit back and accept the inflation risks exported by the Fed. Sources: China Daily, 27/10/2010; China Daily, 11/11/2010

(4) Even the Philippines, a former US colony controlled direct from Washington, have made their displeasure clear. President Begnino Aquino went as far as to say that along with the Philippines, even Singapore and Thailand were suffering the negative effects of the Fed’s decision. Source: BusinessInquirer, 05/11/201

(5) The other European partners remained eloquently silent faced with this flood of criticism. Indeed, that is another lesson to be learned from the sharp reaction to the Fed’s decision: even America’s traditional allies reacted negatively, and some of them, such as Germany and the ASEAN countries, were actually amongst the most aggressive. As a result, even the editorial staff on the UK’s Telegraph, a paper very attached to its “big American brother”, now allow themselves to speak out about their doubts concerning the wisdom of the Fed’s decisions and are predicting the end of the dollar era. Sources: Telegraph, 04/11/2010; Telegraph, 05/11/2020

(6) Like many economies in danger of overheating, Australia continues to raise its interest rates to combat the “Fed effect” of strengthening the Australian dollar against its US counterpart. Similarly to the Canadian dollar and the Swiss franc, the Australian currency has breached parity with a US currency in freefall. India echoed Australia’s approach. Sources: Telegraph, 02/11/2010; Wall Street Journal, 02/11/2010

(7) This is a perfect illustration of Michael Hudson’s fine article in CounterPunch dated 11/10/2010 entitled “Why the US has Launched a New Financial World War – and How the Rest of the World Will Fight Back”.

(8) As Doug Noland wrote on 05/11/2010 in his consistently excellent Credit Bubble Bulletin, “Global decision-makers must now be fed up”. And they are. This is far more than the simple Sino-American face-off suggested by this amusing rap clip on the theme of the dollar-renminbi dispute. Source: NMA World Edition, 10/11/2010.

(9) And one must also mention the increasing number of people (including within the Fed) voicing their concern about the US central bank’s deteriorating balance sheet. The chart below shows that its “assets” are more than a little worrying: mortgages issued by Fannie Mae and Freddie Mac, as well as shares in their stock; plus AIG and Bear Stearns shares. These are “phantom assets”, worth virtually nothing. For the rest, if the Fed used simply to ask the advice of its primary dealer when deciding the volume of its Treasury purchases, now it will have to learn to consult the other central banks. Source: Bloomberg, 28/10/2011

(10) As Liam Halligan said so rightly, in the Telegraph of 06/11/2010, using an image that the GEAB wouldn’t have sniffed at: the US is going through its own “Economic Suez”. He is referring of course to events in 1956, when two time-honoured colonial powers, the United Kingdom and France, mounted a military coup to try to prevent nationalisation of the Suez Canal by Colonel Nasser … and had to stop short when America and the USSR, brandishing their new status of world leaders, signalled that they were opposed to the initiative. “Suez” marked the widespread realisation that the colonial era was over and that the powers of the past would not be those of the future. The parallel that Liam Halligan draws with our times is very pertinent.

(11) And they are far from being unanimously in agreement with Ben Bernanke. The chairman of the Federal Reserve of Dallas has said straight out that he finds the Fed’s current policy a mistake. Source: 24/7 WallStreet, 08/11/2010

(12) And Goldman Sachs estimates that USD 4,000 billion of quantitative easing would be needed to compensate for the weaknesses in the US economy. The price of the austerity and the external constraints is going to be huge. Source: ZeroHedge, 24/10/2010

(13) Even within the US, worries are being voiced about the highly dangerous nature of the Fed’s policy, even going as far as asking whether the Fed might not set off a new War of Succession. Source: BlogsTimeMagazine, 19/10/2010

(14) So even in Germany, which is less affected than others by the consequences of the crisis. Source: Reuters, 13/11/2010

(15) This is also the case for the local communities, which, like France with its departments, are starting to find themselves in impossible financial straits. Source: L'Express, 20/10/2010

(16) Our team launched this recommendation in spring.

(17) This GEAB N°49 provides more information in the chapter on the double Franco-German electoral shock of 2012/2013.

(18) Sources: Spiegel, 26/10/2010; MarketWatch, 12/11/2010; RiaNovosti, 10/11/2010; IrishTimes, 11/11/2010; NewropMag, 18/11/2010

(19) Europe will see its score on border protection surge in the very informative ranking based on measures affecting global trade, compiled by Global Trade Alert.

(20) Source: Le Figaro, 11/11/2010

(21) This is the incident that took place near the Senkaku/Diaoyutai islands. Source: Global Research, 06/10/2010

(22) A variety of other symbolic incidents have occurred, going beyond the regional level. For example, China’s recent ranking as no.1 in supercomputers, a position snatched from the US, who had held it from the time of the first computers, after the second world war. Source: Le Monde, 28/10/2010

(23) In October 2010, new-car sales were the worst in 42 years. Source: Asahi Shimbun, 03/11/2010

(24) Based on the purchasing power parity, this analysis concurs with the analyses conducted by the LEAP/E2020 team and stating in GEAB N°47 that US GDP is now overestimated by around 30%.

Global Europe Anticipation Bulletin

Global Research Articles by Global Europe Anticipation Bulletin

© Copyright Global Europe Anticipation Bulletin -, Global Research, 2010

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.