The U.S. Fed Wants an Inflation Boom

Economics / Quantitative Easing Oct 12, 2010 - 05:12 AM GMTBy: John_Mauldin

As long time readers know, I am a big fan of Greg Weldon. This week he has very graciously allowed me to reproduce his client letter from last Thursday on some of the issues of Bernanke and Quantitative Easing 2. It prints a little longer than usual because of his format and all the charts, but this is one letter you should take the time to read.

As long time readers know, I am a big fan of Greg Weldon. This week he has very graciously allowed me to reproduce his client letter from last Thursday on some of the issues of Bernanke and Quantitative Easing 2. It prints a little longer than usual because of his format and all the charts, but this is one letter you should take the time to read.

You can get a free trial (his service is not cheap but if you are a global macro fund or trader, you really should have it!) by going to www.weldononline.com.

Sadly, this weekend was not a good time for Dallas. The Rangers dropped two and now have to win in Tampa Bay and the Cowboys were simply awful. The first time in 50 years that I get season tickets and they are just not fun. I was thinking they get to the Super Bowl and it is in Dallas this year and the tickets get me in. Clearly, I need to keep my day job.

Oh, well, the Mavericks are in town and the NBA will soon crank up. Oh, wait a minute. Everyone we wanted went to Miami. We are not that much better than last year. Sigh. Oh, well. It could be worse. I could be in Cleveland. (Sorry, Mike!)

Your hoping Cliff Lee pitches a shut-out analyst,

John Mauldin, Editor

Outside the Box

Time Loves a Hero By Greg Weldon

WELDON"S MONEY MONITOR

I was fortunate to have met the late Lowell George, lead singer of "Little Feat", prior to the band"s performance at Colgate University in 1979. The band was using the men"s basketball locker room as their "hospitality suite", relegating the team to the local high school. As we returned from practice to store our gear, George was in the room, and he asked us if anyone could use the pair of size 21 basketball sneakers that a fan had tossed on stage during the previous night"s gig at Cornell.

We note lyrics from Little Feat within the context of today"s macro-monetary focus on the US ...

"Well they say time loves a hero.

But only time will tell.

If he"s real, he"s a legend from heaven.

If he ain"t, he was sent here by hell."

Markets are praying that time will tell us ... that Ben Bernanke was a monetary legend from heaven, and a hero to the masses who are starving for a macro-reflation, specifically as it relates to the housing and labor markets.

But, if the "cost" of creating jobs is a price-inflation spiral ... then there could be "hell-to-pay" in the markets, particularly in the fixed-income arena, and Boom-Boom"s legacy could be one of the "anti-hero".

Of course, there is a decent chance that even the most heroic of efforts by the Federal Reserve could FAIL to generate the "desired" outcome, leading to an increasingly "devilish" debt-deflation.

Or, things could just stay ... sideways, with both an upward tilt, AND a downward skew.

Thus, the odds of the Fed looking heroic ... 2:1 ... against ... with one scenario considered a draw (status quo), while two of the other three potential "scenarios" (hyper-inflation, or a debt-deflation) leading to some kind of hellacious reaction in stock, bond, and currency markets.

Indeed, we do NOT envy Ben Bernanke, and his "job".

Frankly, few do it better than Boom-Boom, who has managed to create a most unique "circumstance" with his pledge to monetize as much US Treasury debt as necessary, to insure that an overt debt deflation does not become "the" dominant macro-force. Ben has fostered an environment where BOTH bond prices AND inflation expectations, are on the rise.

The Fed has made it crystal clear ... they are pursuing higher inflation.

Five years ago, in my book "Gold Trading Boot Camp" we discussed at length the conundrum currently facing the Fed, stating that the Fed would, someday, be forced to acquiesce to higher commodity-price inflation, (particularly Gold) in order to circumvent a deepening macro-deflation.

Bingo, this is EXACTLY what is happening.

This is WHY Gold is screaming to the upside.

This is WHY the TIPS are screaming to the upside.

This, thanks to the fact that the Fed has orchestrated a PLUNGE in US short-term interest rates, US Treasury Note yields, and US Treasury Bond yields ...

... in synch with a massive COMPRESSION in the Yield Curve.

We have been discussing the Yield Curve for months since our March-18th Money Monitor entitled "March Madness", in anticipation of the compression we are now seeing ... and we focused on the intensifying flattening taking place in the mid-curve, within the 2-Year, 3-Year, and 5-Year maturities, as recently as our September 24th Monitor, "Dancing with the Devil."

Yes, the Fed has offered the "soul" of the US currency, in return for a monetization-derived "reflation", in the hope that an asset-price-reflation will, somehow, finally, spillover into the "real" underlying macro-economy.

But only time will tell. If he"s real, he"s a legend from (monetary) heaven.

The problem is, that the Fed may have been "too heroic", by talking-the-talk, without really "walking-the-walk", not yet anyway, not to the degree to which their TALK has sparked a feeding frenzy ...

... one that is "validated" by the horrific scene in the macro-economy ...

... and yet one that is "refuted" by the price action in Gold, the US Dollar, along with emerging market equity indexes and currencies.

For sure, without much actual debt monetization by the Fed over the last six months, things in the markets are looking increasingly "bubblicious".

The Fed is NOT directly responsible for the "froth".

But their "talk" is, as investors, banks, and global central banks have snapped up Treasury debt as if the Fed did offer a "put option", by which it would be willing to step in as the buyer-of-last resort, in the event that owners of Treasuries stopped buying ...

... or ... worse yet ... gasp ... if they started to sell.

The "odds" lengthen, when we contemplate the following thought process:

--- IF there is in fact a BUBBLE in the Treasury market, and IF that bubble is "pricked", the FEDERAL RESERVE will be EXPECTED to buy as MANY BONDS AS IT TAKES, to stop the escaping air from deflating the bubble.

The Fed has put itself in a VERY tough spot, and when (not if) they are finally required to walk-the-monetary-walk, all hell could already be breaking loose.

Indeed, for this reason, we believe that the odds stack up against a Fed strategy that implicitly (as suggested by many, including the St Louis Fed President) seeks to monetize Treasury debt slowly, over a longer-time frame and in "smaller" increments, than was the case in the 2009-10 experience.

To date, the Fed has NOT been leading the charge.

As we detailed in our Dancing with the Devil Monitor of September 24th, US Households, US Commercial Banks, and Foreign Official Accounts (ie: Central Banks) have purchased, in total, MORE than $2.5 trillion in Treasury debt since the beginning of 2008 ... whereas the Federal Reserve has purchased only ONE-PERCENT as much (more on this, later).

Indeed, Treasury Note Yields are plummeting to record lows, and the Fed has only JUST STARTED "talking-the-talk", as evidenced by a plethora of comments on the offer from Fed officials since the middle of last week.

We note the following quotes ...

... starting with the would-be-hero, maybe-headed-for-monetary-hell, Fed Chairman, Ben Boom-Boom Bernanke himself ...

... "I do think that additional purchases, although we do not have precise numbers for how big the effects are, I do think they have the ability to ease financial conditions."

Next we note commentary that sparked Monday"s extension lower in US Treasury Note yields, from New York Fed President William Dudley ...

... "Fed action is likely to be warranted unless the economic outlook evolves in a way that makes me more confident that we will see better outcomes for both employment and inflation before too long."

Indeed, the Fed will keep pumping, until it sees the proverbial "whites-of-their-eyes, as it relates to inflation, and job growth.

More from Dudley ...

... "The outlook for US job growth and inflation is unacceptable. We have tools that can provide additional stimulus at costs that do not appear to be prohibitive."

Indeed, when we first used the word "deflation" in the Money Monitor, back in the nineties, and into the first part of the last decade, people scoffed, as this was a word equated to "monetary blasphemy" ...

... and I might have been "charged" as a "heretic" for suggesting that, someday, the Fed would PURSUE INFLATION as a POLICY GOAL.

Now, the New York Fed President openly states that subdued inflation is ...

... "UNACCEPTABLE" !!!!

Welcome to the new world order, where deflation is openly discussed, and inflation is, in fact, pursued by the Federal Reserve, as a policy goal.

Check out comments from Chicago Fed President Charles Evans ...

... "We appear to have lost some of our forward momentum in recent months.

..."The size of the employment gap, combined with the fact that inflation has been running below the level I consider consistent with long-term price stability, suggest that it would be desirable to increase monetary policy accommodation to boost aggregate demand. Inflation could stay below desirable levels for the foreseeable future."

Something few have considered ... what if the Fed does NOT fulfill their implied pledge, and does NOT purchase "as many bonds as needed".

What if ... the amount the Fed would be "required" to monetize, is SO LARGE, that they fail to garner the political and monetary "will" to actually enact those purchases, persistently.

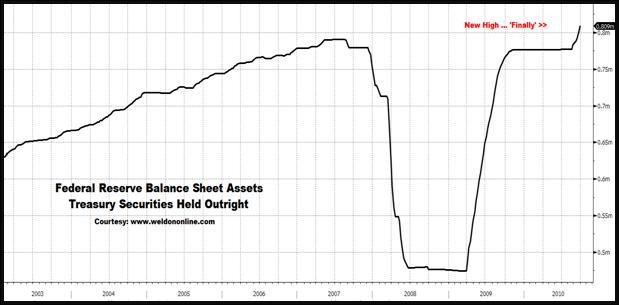

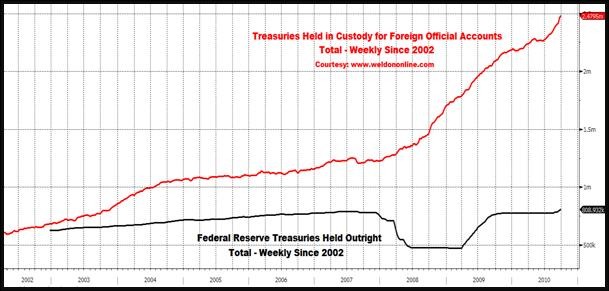

Only time will tell, given that the Fed has only just started to accumulate "new" Treasury debt, as evidenced in the chart on display below, revealing the increase in the amount of Treasury Securities Held Outright by the Fed. Recall, of course, that the Fed SOLD Treasuries at the onset of the credit crisis in 2007, to raise cash used to provide "stimulus". Then, in March of 2009 the Fed announced "purchases" of $300 billion in Treasuries (in addition to MBS and Agency debt), which brought total "holdings" back to where they started, just under $800 billion. Only now are they rising, relative to 2007.

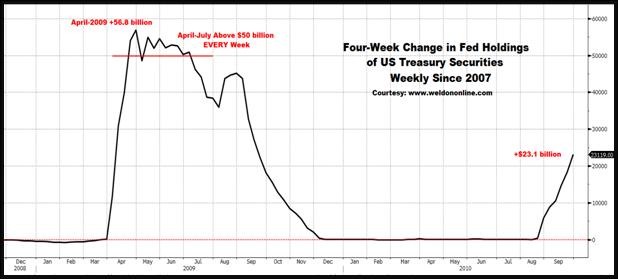

While much of the monetization is linked to the "roll-off" of Mortgage-Backed-Securities from the Fed"s Balance Sheet ... we note that Boom-Boom"s crew has taken-down nearly $25 billion in Treasuries over the last four weeks. Still, this pales in comparison to the 4-months in 2009 when the 4-week "average" accumulation was consistently greater than $50 billion.

But Fed purchases are MINISCULE ... compared to the accumulation of US Treasury debt by Foreign Official Accounts (ie: Central Banks). In fact, while the US Fed was "busy" buying $23.1 billion in US Treasury paper over the last four weeks ... Foreign Official Accounts have purchased $85.69 billion.

Indeed, over the previous four-week period, while the Fed was purchasing NOTHING, Foreign Central Banks took-down $71.07 billion in UST debt.

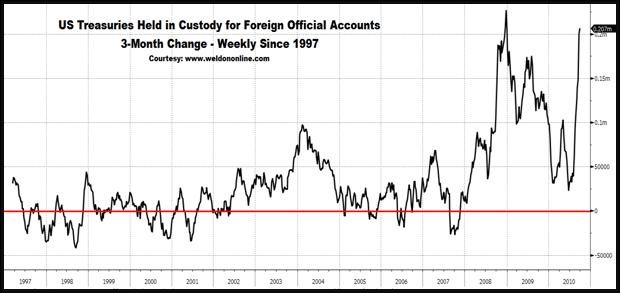

In fact ... over the last nine weeks Foreign Official Accounts have seriously stepped up their purchases, perhaps with knowledge that the Fed was preparing to move (ie: insider trading) ... accumulating an eye-opening $163.663 billion since the first week of August. Evidence the chart below plotting the 3-Month Change in Treasuries Held in Custody for Foreign Official Accounts ... revealing that the recent accumulation represents the second largest ever, for a three-month period.

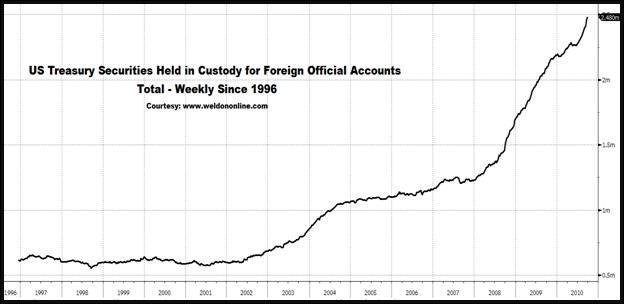

We shine the spotlight on the chart below, revealing the upside acceleration in total Custody Holdings, and the move to a NEW ALL-TIME HIGH in each of the last nine weeks ... not to mention exposing the fact that Custody Holdings have DOUBLED since 2007, and are nearing $2.5 trillion.

Who is the "real" hero ??? ... the Fed ??? ... or ... Foreign Central Banks ???

Observe the perspective offered in the overlay chart on display below in which we plot the total of Treasury Securities Held in Custody for Foreign Official Accounts (red line), against the total of Treasury Securities Held Outright by the Federal Reserve (black line).

The "gap" is WIDE, and worse, it is WIDENING, dramatically, every week.

Boom-Boom wants to be a hero ... but ... would the Fed be willing to buy $1.3-$1.7 trillion of US Treasuries, in ADDITION to the debt it might be required to monetize in line with huge future Treasury funding and re-funding "needs ... IF ... foreigners stopped buying, or, worse, started selling ??

We could argue, from the perspective of being a "hero", Ben is already "falling behind the monetization-curve". This poses a risk to the markets, given the exuberant reaction in anticipation of aggressive Fed monetization.

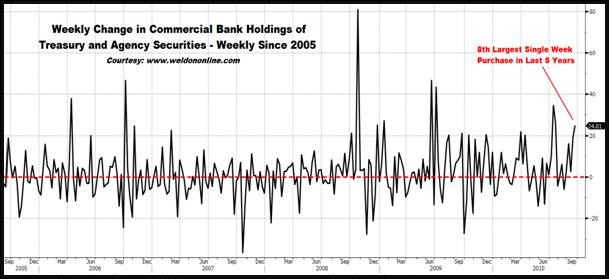

It is within this same context that we note that US Commercial Banks were also HUGE buyers of Treasury debt in the latest reporting week (end-Sept-22nd) ... to the tune of $24.8 billion, a figure that represents the 8th largest single-week purchase in the last decade. Evidence the chart below.

Indeed, US Banks bought as much "paper" in the most recent week, as the Fed has in the last FOUR weeks, and, we note that the most recently reported accumulation of US government paper by Commercial Banks is equal to a +1.5% single-week nominal increase ...

... or ... an +80.5% annualized rate of expansion in total holdings.

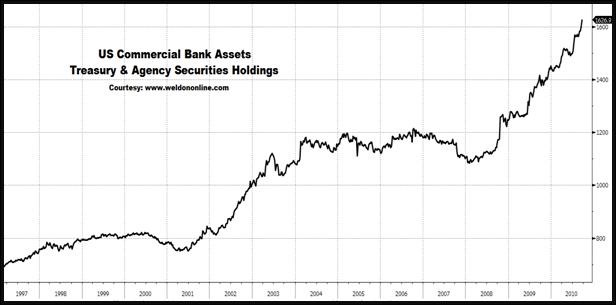

In fact, with total holdings now above $1.6 trillion, as noted in the chart on display below, US Commercial Banks hold TWICE as much as the Fed.

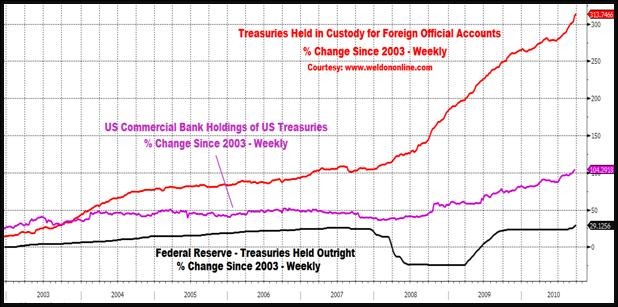

When we compare the "rate of accumulation" of Treasury debt (Commercial Bank data includes Agency debt, but not MBS paper) since 2003, we come up with the overlay chart on display below giving us a sense of the level of aggression that might ultimately be required from the Fed, which "trails" Foreign Central Banks and US Commercial Banks, by a wide margin.

Indeed, the Fed will be "needed" to fill the gap that could be created IF Commercial Bank lending begins to reflate, and they begin selling securities as a result. Only time will tell, if the Fed is going to be a hero.

Indeed, the Fed is NOT "really" directly responsible for the bond bubble, rather, we could point a finger at the LACK of reflation in the underlying macro-economy, as cause for the push to new lows in Treasury yields.

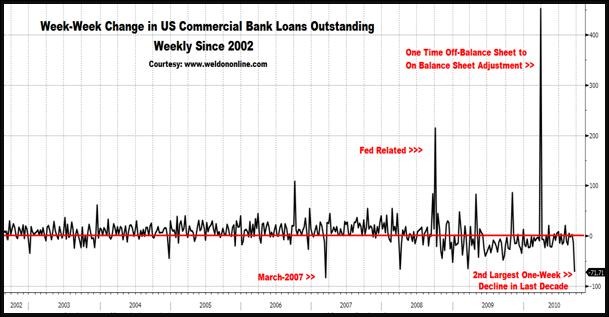

In fact, during the latest reporting week, US Commercial Bank Loans Outstanding FELL by a HUGE (-) $71.8 billion ...

... while their total Securities Holdings and Cash provided a mirror-image, with an equally HUGE concurrent cumulative rise of + $69.4 billion.

Bank Lending remains in the grip of a DEEPENING DEFLATION, with the most recent weekly decline representing the SECOND LARGEST EVER, as evidenced in the chart below.

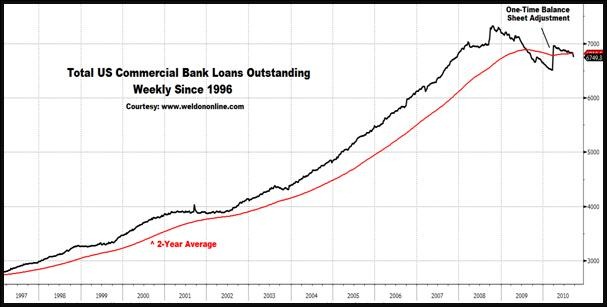

Note chart below, plotting the deleveraging as defined by Commercial Bank Loans Outstanding, which, after a balance sheet adjustment, is deflating, again, with the total of bank loans outstanding plunging back below the long-term trend defining 2-Year Average.

Deleveraging continues, and money that is NOT "needed" by the "real" economy, is flowing into the financial markets. If the macro-lending dynamic manages to reverse itself, the Fed will need to step in, to prevent a rise in interest rates from crushing a fledgling renewed expansion in credit.

Specifically, on the back of continued deflation in jobs, the deleveraging is most intense at the Consumer level ... with the most recently reported single-week decline in Commercial Bank Consumer Loans Outstanding, pegged at (-) $12.5 billion, representing the second LARGEST one-week decline EVER recorded by the Fed. Observe the chart below.

A hero is NEEDED ... specifically, to rescue the labor market.

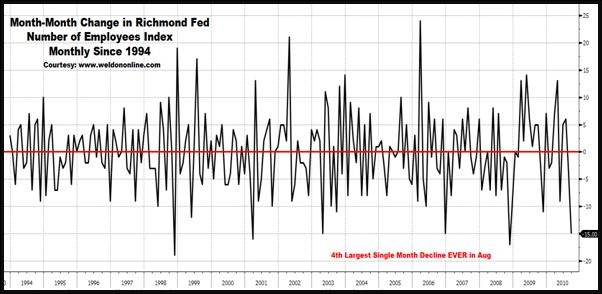

With tomorrow"s release of critical employment data looming, we note labor market data for September on the offer from the Federal Reserve, in the form of the Richmond Fed Economic Conditions Survey ... revealing weakness that must have been "sent by hell". Observe the chart below plotting the monthly change in the Richmond Fed"s Number of Employees Index ...

... and one of the DEEPEST single-month declines in the last decade.

Indeed, observe the raw data details, with focus on the full-circle path taken by the Employees Index, from negative at the beginning of the year, in line with declines in headline US Payroll data ... to a strengthening trend mid-year, synchronized with (alleged) growth in private payrolls ....

... to September, and a renewed, outright, deflation.

This bodes ILL for tomorrow"s Payroll figure.

Richmond Fed - Number of Employees Index

Sep-10 ... (-) 3

Aug-10 ... + 12

Jul-10 ... + 15

Jun-10 ... + 9

May-10 ... + 4

Apr-10 ... + 13

Mar-10 ... zero

Feb-10 ... (-) 7

Additionally, we note a relapsed-collapse in the Average Workweek Index:

Richmond Fed - Average Workweek Index

Sep-10 ... zero

Aug-10 ... + 14

Jul-10 ... + 15

Jun-10 ... + 16

May-10 ... +13

Apr-10 ... + 16

Mar-10 ... zero

Feb-10 ... (-) 4

More telling is the perspective on display within the chart below, plotting the month-to-month change in the Richmond Fed"s Average Workweek Index. We spotlight the fact that September"s deep decline of (-) 14 "points" is one of the worst EVER ...

... and ... suggests that the odds of a "double-dip" are becoming more probable, amid a TRIPLE-DIP in the labor market dynamic.

Again, the results from the Richmond Fed, bodes ILL for tomorrow"s data.

The renewed deflation in the Richmond Fed"s labor-market-linked data comes on the heels of the COLLAPSE in the headline Richmond Fed Business Activity Index since the spring. Evidence the data details:

Richmond Fed - Business Activity Index

Sep-10 ... (-) 2

Aug-10 ... + 11

Jul-10 ... + 16

Jun-10 ... + 23

May-10 ... + 26

Apr-10 ... + 30

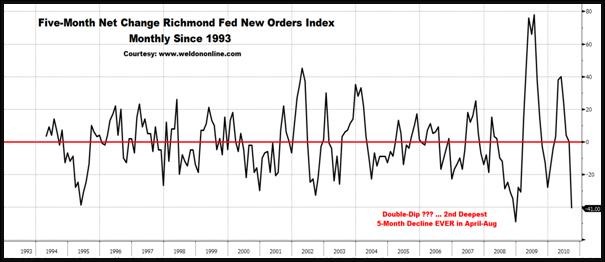

Worse yet, we note that the decline is being "led" by renewed erosion via the final demand dynamic, as reflected by the "sequential" collapse in Order Backlogs, New Orders, and then Capacity Utilization, as the pipeline becomes filled with negative numbers, squelching any chance of a near-term, sustained, macro-expansion in employment.

We start with the utter collapse in the Richmond Fed"s New Orders Index.

Richmond Fed - Volume of New Orders Index

Sep-10 ... zero

Aug-10 ... + 10

Jul-10 ... + 13

Jun-10 ... + 25

May-10 ... + 36

Apr-10 ... + 41

We note that since the mini-recovery peak of +41 set in April, the collapse in the New Orders Index, seen in the chart below, is the second deepest ever recorded by the Richmond Federal Reserve, second only to the decline posted during the 4Q of 2008. Indeed, THIS is WHY the Fed is proposing to become more aggressive.

Next we note the pipeline, as per the collapse in the Order Backlog, and the subsequent plunge in Capacity Utilization.

Richmond Fed - Backlog of Orders Index

Sep-10 ... (-) 11

Aug-10 ... zero

Jul-10 ... + 1

Jun-10 ... + 3

May-10 ... +16

Apr-10 ... + 5

Mar-10 ... (-) 7

Richmond Fed - Capacity Utilization Index

Sep-10 ... zero

Aug-10 ... + 14

Jul-10 ... + 13

Jun-10 ... + 21

May-10 ... +27

Apr-10 ... + 27

Mar-10 ... + 3

Feb-10 ... (-) 3

We have also been specifically focused of late, on an intensifying, "unwanted", build in Inventories, at Producers, Wholesalers, and Retailers. We see more evidence of this within the Richmond Fed"s data, which reveal an accelerating "build" in Inventories of Finished Goods AND Raw Materials.

Richmond Fed - Finished Goods Inventory Index

Sep-10 ... + 15

Aug-10 ... + 11

Jul-10 ... + 8

Jun-10 ... + 7

Richmond Fed - Raw Material Inventory Index

Sep-10 ... + 13

Aug-10 ... + 9

Jul-10 ... + 11

Jun-10 ... + 4

Similarly, we observe data released on Tuesday by the US Commerce Department, revealing significant increases in Manufacturer"s Inventories, as it relates to several key "sectors" and "industries".

Evidence some of the data samplings offered below, starting with the surge in Inventories as measured by the year-year percent change of Total Manufacturer"s Inventories:

Year-Year % Change in Total Manufacturing Inventories

Sep-10 ... + 3.5%

Aug-10 ... + 2.5%

Jul-10 ... + 0.9%

Jun-10 ... (-) 0.8%

May-10 ... (-) 1.7%

Apr-10 ... (-) 3.4%

Mar-10 ... (-) 5.4%

Feb-10 ... (-) 7.9%

More specifically, we observe rising inventories of Consumer Goods, across a wide range of "types" of goods.

Consumer Durable Goods Inventories ... rose by +1.4% in August, marking the fourth consecutive month-month build to exceed +1.0%., taking the year-year rate of inventory expansion to +7.2%, a WILD reversal from the decline of (-) 17.7% yr-yr seen in February.

Furniture Inventories ... rose by +1.1%, marking the seventh monthly increase in a row, with 4 of the last 5 months posting a build in excess of +1.0%

Apparel Inventories ... rose +2.3%, the fourth consecutive increase of more than +1.0%, including a massive +5.7% increase in June. Subsequently, the year-year rate spiked to +6.6%, a complete reversal from the (-) 15.5% yr-yr rate of drawdown posted in Feb

Electronics Goods Inventories ... rose +1.7% in August, the sixth consecutive monthly build, with five of the six months posting an increase of more than +1.0%. Moreover, inventories of Home Appliances soared to a +17.2% yr-yr rate of "build" during August, a complete reversal from the (-) 1.1% yr-yr pace of decline in Feb.

Light Truck (SUV) Inventories ... rose +4.0%, following hard on the heels of an equally HUGE monthly increase of +5.5% in July, and +4.4% in May. Indeed, the year-year rate of build in the Inventories of Light Trucks has EXPLODED to an unbelievably high +50.7%, up from +37.0% yr-yr build in July, and a complete reversal from the year-year rate of decline, (-) 14.2%, seen in February.

Worse yet, from the future labor market perspective, we note that inventories of Capital Goods are on the rise as well, as businesses begin to reign in capital expenditures, a move likely to further inhibit new hiring.

Year-Year % Change Non-Def Cap-Goods Inventories

Sep-10 ... + 3.9%

Aug-10 ... + 1.3%

Jul-10 ... (-) 0.7%

Jun-10 ... (-) 3.9%

May-10 ... (-) 6.2%

Apr-10 ... (-) 7.7%

Mar-10 ... (-) 9.3%

Feb-10 ... (-) 10.4%

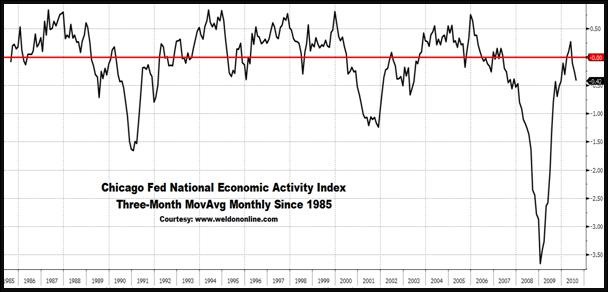

Indeed, most all of the macro-economic data released in the last week within the US, speaks ILL of the top-down picture. Within that context we note the Chicago Fed"s very reliable National Economic Activity Index, which plunged to (-) 0.53 in August, down from (-) 0.11 in July, and, is down from the most recent positive reading of + 0.36 posted in April. More pointedly, the Chicago Fed"s 3-Month Average slid deeper into negative territory, as noted in the chart below. The renewed plunge implies that the odds of a double-dip are on the rise, and is thus seen by the Fed as "cause" for a more aggressive monetary approach.

At the end of the Fed remains a 2:1 underdog, as it relates to time telling us that Boom-Boom was a hero, sent from monetary-heaven ... with the two outliers, or "tails", scenarios in which the Fed is viewed over time, as being sent from monetary hell, wherein they FAIL to stimulate reflation, and the macro-deflation becomes dominant ... or ... they go too far, and spark a hyper-price-inflation episode.

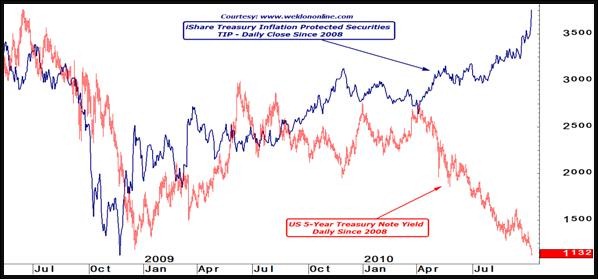

These two "tails" are exhibited in the overlay chart on display below plotting the path of the iShare for the Treasury"s Inflation Protected Securities, or TIPS (symbol-TIP, blue line) ... against ... the yield on the 5-Year Treasury Note (red bars) ... revealing a MASSIVE "divergence", and break in the normally tight positive correlation between the two "markets".

The PROBLEM for the Fed ... can be seen in the width of the disconnect, which represents the level to which Treasury yields "could" rise, if inflation were to become more prominent, with the TIPS implying a 5-Year Note Yield closer to 4%, than the current 1%. We wonder ... how many T-Notes would the Fed need to buy, to keep yields from rising, and crushing the fragile macro-consumer-economy ???

For now, the Fed is able to "float", without getting overtly aggressive on the buy side, as the mere EXPECTATION of Fed bond monetization, in synch with horrific macro-data, has been enough to drive the 5-Year Note yield to a new all-time low, near 1%, as evidenced in the chart below.

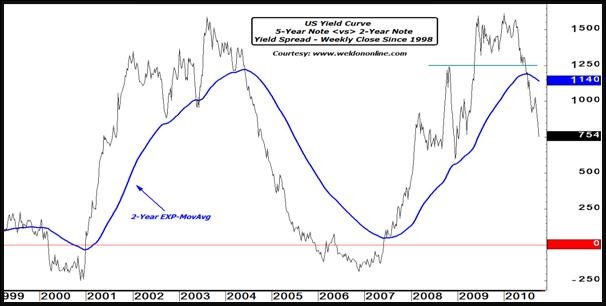

We have been bullish on US Treasuries since March, and we remain bullish, particularly as it relates to the continued "compression" in the US Yield Curve, specifically at the "mid-curve" level.

Thus we shine the spotlight on the longer-term weekly chart on display below plotting the 5-Year Note/2-Year Note spread, and revealing the "compressed" move towards flattening, and the intensifying trend defined by the violation of, and downside reversal by, the secular 2-Year EXP-MA.

BUT there is something else worthy of note. Intensified purchases of Treasury paper by the Fed comes at the expense of a "decline" in holdings of Mortgage-Backed-Securities ... a decline that conflicts with the continued over-reliance of the housing market on mortgage lending originating with the GSE"s, such as Fannie Mae. Subsequently, we are closely monitoring the spread plotted in the chart below, comparing the 5-Year Fannie Mae Yield, to the 5-Year US Treasury Yield. We note the move towards "widening" in this spread, a dynamic that could offset some of the "flat-price" decline in yields, exacerbating the headwinds facing the US Housing market.

Indeed, if Boom-Boom wants to be a hero ...

... he may be forced back to the buy-side, in the MBS market.

Certainly, such an event would be FULLY supportive to our ongoing bullish campaign in the Precious Metals markets, AND, our current bearish stance in the US Dollar.

And the Fed WANTS to be heroic.

Thus, unless the Fed fails to "follow-thru" with "action" ...

... we remain ... bullish on Gold and Silver, along with the precious metals mining share indexes and ETFs ...

... we remain ... bearish on the US Dollar and the British Pound, relative to both the Japanese Yen and the Eurocurrency ...

... while also remaining ... bullish on a host of Asian currencies.

Further, we remain bullish on emerging Asian "tigers", with focus on Malaysia, Indonesia, the Philippines, Singapore, Thailand, and Taiwan.

Also, we remain bullish on select commodities, with focus on Corn, Cotton, Sugar, Copper, and Aluminum

And, of course ... we remain bullish on the US Treasury market, with focus on the "mid-curve" maturities, in line with our expectation that a compression in the Yield Curve will intensify, perhaps dramatically.

Still, in the longer-term, ALL bets are off, since not even Ben Boom-Boom Bernanke can wear a pair of sized-21 basketball sneakers !!!!!

Gregory T. Weldon ---

Subscription Information ... eileen@weldononline.com Or Visit www.Weldononline.com for a free trial.

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

joshua gamen

14 Oct 10, 01:35 |

Now the Fed WANTS inflation...

http://www.youtube.com/watch?v=oSANXDp13Xc http://joshuagamen.wordpress.com/2010/10/13/competition-towards-disaster/ |