Consumer Debt Financed Demand Deleveraging Reality Check for Retailers

Companies / Sector Analysis Sep 09, 2010 - 04:41 AM GMTBy: James_Quinn

Having worked for a big box retailer for 14 years, I understand the dynamics of a high growth rollout of stores as a key to increasing market share and profits. Some of the best retail names in the US have practiced the identical strategy of concentrating many stores in each market to drive the small competitors out of business. This strategy worked wonders for Lowes, Wal-Mart, Target and Kohl's during the early part of this decade. The combination of solid same store sales and opening new stores is a fantastic combination during good times. The results actually make the CEOs of these companies think they are brilliant. Their store expansion models based on rosy assumptions are followed like they can't go wrong.

Having worked for a big box retailer for 14 years, I understand the dynamics of a high growth rollout of stores as a key to increasing market share and profits. Some of the best retail names in the US have practiced the identical strategy of concentrating many stores in each market to drive the small competitors out of business. This strategy worked wonders for Lowes, Wal-Mart, Target and Kohl's during the early part of this decade. The combination of solid same store sales and opening new stores is a fantastic combination during good times. The results actually make the CEOs of these companies think they are brilliant. Their store expansion models based on rosy assumptions are followed like they can't go wrong.

What these CEOs didn't realize was that their expansion plans were based on lies and frauds. If they had advisors who could give them a reality check, they could have avoided the massive downsizing that awaits them. Their hubris didn't leave room for a reality check. The population of the US has grown from 281 million in 2000 to approximately 308 million today. We've had a 10% population increase in 10 years. Consumer expenditures have grown from $6.7 trillion in 2000 to $10.3 trillion today. This is a 54% increase over the course of the decade. Amazingly, real average weekly earnings have only gone up by 6% in the last decade.

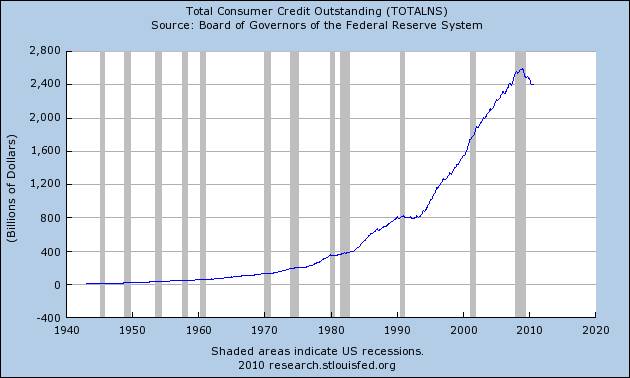

The chart below tells the story that retail CEOs have been ignoring for a decade. Consumer credit has advanced from $1.5 trillion in 2000 to $2.4 trillion today. This 60% increase in consumer debt has allowed workers who have barely increased their earnings to spend like they made a lot more money. This debt fueled consumption binge led major retailers to expand in order to keep up with the delusional consumers.

Retail America has run directly into a brick wall. Below are charts detailing the expansion history of four of the most admired retailers in America. Lowes grew their store count from 600 to 1,700 over the course of the decade, a 183% increase. Wal-Mart grew their store count from 4,000 to 8,500, a 113% increase. Target grew their store count from 1,000 to 1,750, a 75% increase. Kohl's grew their store count from 300 to 1,050, a 250% increase. Same store sales are the true measure of a retailer's health. When comp store sales are +5% or better, retailers make substantial profits and confidently build new stores. As the charts below clearly show, comp store sales have been in a substantial downtrend since 2006. The new stores that have been built in existing markets are over cannibalizing their existing stores.

Lowes has 500 more stores today than it had in 2005, $4 billion more sales, and $1 billion less profits. Target has 340 more stores today than it had in 2005, $12 billion more sales, and the same profit. Kohl's has 240 more stores than it had in 2006, $1.6 billion more sales, and $100 million less profit. Only Wal-Mart has kept the profits flowing, mostly due to its international expansion. The tough times have only just begun for these retailers.

The American consumer is still heavily indebted. Much of the retail spending in the last decade came from mortgage equity withdrawals. Using your home as an ATM is history. Home equity is at an all-time low and 25% of homeowners are underwater. Home prices are destined to fall another 20%. There are 15 million people unemployed. Consumer expenditures still account for 70% of GDP. In order for the US economy to achieve equilibrium, consumer spending will need to regress back to 65% of GDP. This will require an annual reduction in consumer spending of $800 billion. The CEOs of these retailers have not grasped the implications of this coming adjustment in our consumer society.

There are three major errors that have been committed by every retailer in America. They failed to recognize that the spending per household was 30% over inflated due to debt financed demand. They then extrapolated the spending per household using a 5% to 10% growth rate. Lastly, they ignored the fact that their competitors had the same strategy. There are 1.5 million retail establishments in the US. Thousands of these stores are going out of business every year.

Lowes, Wal-Mart, Target, and Kohl's have yet to recognize their predicament. They are still blinded by their hubris. The point of recognition will occur within the next year. Each of these retailers will be closing hundreds of underperforming stores in the next two years. Time for a reality check.

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2010 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.