Gold Imminent Breakout and Investment In Failure

Commodities / Gold and Silver 2010 Sep 01, 2010 - 03:48 PM GMTBy: Jim_Willie_CB

Many observers to the wild gyrations, deep contortions, extreme measures, and other bizarre activity in the government and banking arenas are suffering from severe confusion. The public is alarmed, even frightened, by the sequence of events, without much benefit of comprehension of what is happening or which clans are in control. The degree of deception hit a peak during the TARP Fund creation and disbursement, done behind private closed doors for the replenishment of sacred preferred stock, that bridge between corporate bonds and stock equity. The deception hit a very high pitch with the financial titan failures, the entire string of them. It has never stopped since.

Many observers to the wild gyrations, deep contortions, extreme measures, and other bizarre activity in the government and banking arenas are suffering from severe confusion. The public is alarmed, even frightened, by the sequence of events, without much benefit of comprehension of what is happening or which clans are in control. The degree of deception hit a peak during the TARP Fund creation and disbursement, done behind private closed doors for the replenishment of sacred preferred stock, that bridge between corporate bonds and stock equity. The deception hit a very high pitch with the financial titan failures, the entire string of them. It has never stopped since.

The economic data and promising forecasts (mere marketing group propaganda) featured Green Shoots, Jobless Recovery, and the totally vacant Second Half Recovery that is useful every initial six months to sway the ignorant masses. Just what is happening is difficult to describe succinctly. But the main description reads like an obituary. The most recent and visible distortion is not of price inflation, which has zoomed at 7% annually for a couple years, but rather the Institute of Supply Mgmt. The ISM index has somehow registered a slight increase from July to August, despite almost every single regional index faltering badly. See the careening Philly Fed, from plus 5.1 to minus 7.7 in the latest month. They ignore the weak components and present a distorted aggregate, much like retail sales.

The US banking sector died in September 2008. It has not acted like a credit distribution apparatus in two years. The US Federal Reserve has served almost the complete function, filling the gap like with the decaying commercial paper market. Its several dozen liquidity facilities testify to its urgent need to act as banking system substitute, since the real portion lies in the morgue. The major 100 banks in the US are almost without exception insolvent, and thus do not lend. Sure, they boast a positive book value, but only after given permission to use phony FASB accounting rules. They can declare their assets at any value they wish. In fact, on many debt securities, they actually declare unrealized losses as gains. See the Credit Value Adjustment scheme, an utter travesty and shameful practice mocked by accounting professors. The FDIC came out this week to announce the Q2 list of problem banks went from 775 in number to 829, from Q1. Hardly evidence of a recovery. The USEconomy suffers from a credit strangulation since the banking system at the upper levels is dead, simply stated. The main thrust of the limp activity is monetary creation, banker welfare, absurd programs, and war spending. The more money the clownish hapless awkward leaders throw at the problem, the more the Gold price will rise. Each quantum policy step lifts the potential Gold price another $1000 per ounce.

This article is an attempt to briefly describe what is happening to the United States, from an aerial perspective, regarding the foremost poorly told events, better description of critical event factors, the lost generation of industry, the official investment by the USGovt in profound failure, the confusion from broadening collectivism, the absence of a solution toward restructure and remedy, and what actual solution might include. The popular debate once centered on the banks too big to permit a failure, but that debate became distracted by the flow of events. Only liquidation of the biggest banks can enable a recovery, period!! Of course, the process is complicated, especially politically. Actually, it is more than political, since the big banks control the USGovt. The response reaction from gold & silver will give loud messages to systemic failure, as money is wasted, invested in failure, and directed to the elite troughs. One can argue that no remedy or restructure is even attempted!!

REAL STORY BEHIND FOUR FAILURES

The Bear Stearns episode was the prelude to the failure story, the opening act, the clue for the death of the US banking sector. Its story was a mere partial truth, one that avoided all the inner circle rivalries and hate relationships. The firm did not participate in the general rescue program for LongTerm Capital Mgmt in 1998. It was singled out for execution, a kill at a later date. The Bear Stearns failure was a murder execution for its long gold position and short USDollar position, if truth be told. Wall Street never enjoys or benefits from telling the truth. Deception is its calling card. The Gold price was prevented from finding a much higher legitimate value, from continued control after Bear Stearns was removed from the clique.

The American Intl Group episode was disguised from its true nature as a Goldman Sachs bailout. In fact, the record has been somewhat clearly told that the AIG nationalization enabled GSax to be first in line for credit default contract redemptions, at full price. They saved $11 billion in the nationalization and butting in line. There are advantages to acting as the USDept Treasury administrator. Many other big banks had favorable redemptions on similar insurance contracts. The wreckage of the entire US banking sector was thus covered up from the insurance perspective, preventing a credit derivative blowup. The Gold price did not react from a failure motive, as much as a perceived systemic risk motive. The over $100 billion in covered losses to AIG so far is just the beginning of investment in failure. The USGovt is managing the credit derivatives from under its rickety broken rotten wing. But Gold does react to the waste of money, the debasement of money, and not so much from inflation entering the system. That comes later.

The Fannie Mae episode was one best described as averting either a mortgage bond default or a severe jump in mortgage rates emanating from the sewage treatment plant. In pulling off the nationalization of the wretch, the Wall Street controllers thus placated a crucial angry mortgage creditor. China had been selling all summer long in 2008 its Fannie Mae and other GSE bonds. China forced the USGovt hand as they made it explicit from nationalization. Rumors had been flying in late 2007 and early 2008 that China was accumulating USAgency Mortgage Bonds as part of some contract toward colonization. No more! The USGovt guarantee was implicit but soon made more explicit. The $170 odd billion in covered losses so far is just the beginning of investment in failure. But Gold does react to the waste of money, the debasement of money, and not so much from inflation entering the system. That comes later.

Lehman Brothers was an unwilling sacrificial lamb for its prominence in the mortgage arena. They were an important player that got in the way. The Lehman killjob created a dustup distraction in which JPMorgan was funded $138 billion in a grand reload with USGovt money, to maintain its commodity stranglehold. They were running low on funds to defend the system and to keep America strong, the envy of the world, the beacon of hope. Also, Lehman owned a significant silver position that had gone out of control, in danger of being the object of a critical short covering event that would have rendered huge damage to JPMorgan. Therefore, JPMorgan took it over and assumed its responsibility. They drove the silver price down from $19 to $10 in the ensuing months, with no objection, criticism, or suspicion of impropriety from regulators, legal authorities, or anybody residing in South Manhattan. However, the Silver price returned to face the same $20 level, which it will easily overcome and penetrate in the next few months. Smart investors bought the silver offered at discounted price for several consecutive months.

INVESTMENT IN FAILURE

For vivid indications of failure, notice the slide into recession even after 20 months of near 0% official interest rate. The USFed has no more weapons except the Printing Pre$$, which it will reluctantly use, perhaps somewhat aware of the dire immediate consequences. Central bankers are soiling their skivvies, in utter fear. For vivid indications of failure, notice that the housing sector and commercial property sector do not respond to record low mortgage rates. The average 30-year mortgage rate across the land stands at 4.40%, silly low but uselessly low. Refinance is not an option, given the valuation declines in loan collateral. The ultimate problem is insolvency laced like cancer throughout the entire system, from housing, to households, to banks, to government fiscal situation, even to industry (long gone). The USFed cannot treat insolvency. Only liquidation can. The human toll has been great, from chronic joblessness, to mortgage delinquencies, to home foreclosures, to lost pensions, to vanished financial security. For vivid indications of failure, notice the 2.5% to 2.6% long bond yield in USTreasurys, the last bubble. The US bankers who have run the land for two decades have run out of asset bubbles to blow. Each growth period of 5 to 7 years has been driven by the next asset bubble in sequence, not industrial development or output. Money is being ruined at a rapid rate, and precious metals indicate the pace and severity. As the great bond bubble dissipates from whatever pinprick, the gold rally will move from quiet bullish to monster bullish, complete with a skyrocket event. In the next phase, do not be surprised to see the Gold price rise over $100 on a single day. The financial networks will be bug-eyed and speechless.

Plain language works best at this point. The USGovt, as demonstrated by its nationalizations, big bank rescues, grand aid packages (car industry), and support of extreme measures, has invested heavily in failure, fraud, and banker elite welfare otherwise called pillage. They also has invested in sacred wars at great cost. The USGovt has not invested much at all in business, jobs, family, and life. The flimsy shallow vacant home loan programs exemplify the lack of support and aid for the public. In fact, an argument can be made that the government and banking leadership (tightly twisted together) have contempt for the People. The current administration features a return of failed policy makers, as seen in Robert Rubin, the modern day Rasputin in control of puppet strings. His past failures qualified him for near total banking policy control. As a result, the public harbors growing resentment from the inequality of bailouts and benign neglect to households. The failure to individuals is stark with pink slips and job loss. As long as weekly jobless claims exceed 450 to 470 thousand, nobody will give much credence to any USGovt verbage about a recovery. Failure is in the wind.

GOLDEN RESPONSE TO FAILURE

The failure pertains to the US financial sector in its entirety, from banking system to credit market. The failure is exacerbated by wasted expenditures toward what are called rescues and stimulus, but is actually banker welfare payouts, their toxic bond redemption, and nationalization of failed entities. Worse, the key nationalized firms are laced with $trillion fraud. Fannie Mae remains the central clearing house for several $trillion fraud schemes. In the wake of failure has come round after round of badly spent funds. It is hard to call it money when it pours off the Printing Pre$$ without recourse, without disclosure, and without accountability. Naked bond shorting, failures to deliver bond sales, and extreme interest rate swap enforcement made for a witch's brew of grand market interference, ruin, and fraud. A prevailing sentiment persists. The consensus lunatic misguided notion is that when the volume of stimulus and rescues is sufficiently higher than a certain threshold level, that recovery follows, especially after a certain period of time. Almost no thinking takes place. The leaders are simply throwing money at the problem and crisis, responding to the next critical focal points. Never has policy been so absent, misguided, and bereft of the thought process. We are witnessing a syndicate in survival mode, in a desperate quest to save the system they exploit so thoroughly.

In response, the Gold price potential rises as USGovt funds are wasted without any path to remedy or recovery. The extreme usage of the Printing Pre$$ in the next round of Quantitative Easing, dubbed QE2, will set up crippling explosions. Each round of stimulus or bank rescue or Dollar Swap Facility setup actually puts the potential Gold price another $1000 higher. The future years will see at least $3000 Gold price, all in time. The 1980 peak Gold price, adjusted by an accurate price inflation accounting, like the Shadow Govt Statistics series, is more like $7000 per ounce. My $3000 forecast figure is a conservative number. Anyone who disputes and challenges this forecast, must provide evidence that remedy, restructure, and reform are anywhere present in the current landscape. They are not. Money is being created and wasted at a colossal pace, and while it is wasted, the Gold price in increasingly debased US$ terms rises.

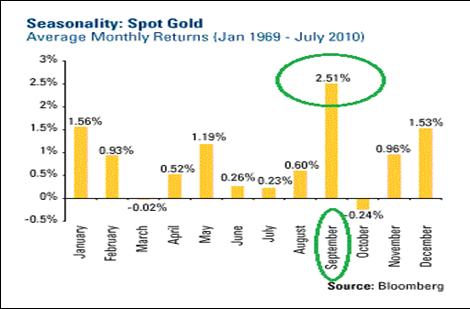

Favorable upcoming months for the Gold price are finally upon us, especially September. We are at its doorstep of a strong season. A major upward thrust is likely as a holiday present before January. The pattern is even stronger with silver. The month of September is especially strong, almost twice as much gusto packed into it as any other month, the next being December and January. In a five-month stretch, three of the 12 best months are lined up, directly ahead. Last year, the 2009 gold price jumped from $950 to $1200 between late August and end December. Expect something similar this year. Also, institutions like the JPMorgan monster queen might face a date with the guillotine in their silver trading desks. If the ultra-strong seasonality for silver does not catapult its price over $20 by January, it will be a big surprise.

SUPERIORITY OF GOLD AMONG COMMODITIES

Prepare for a breakout in the Gold price, fully forecasted, fully forewarned. A tremendous upleg move comes. The consolidation between the $1065 and $1250 prices has taken nine months. The range between $1175 and $1250 has been tighter in the last two months. A big move is indicated, as the seasons offer a firm wind from behind. Notice the MACD crossover, as moving averages are aligned nicely, but calmly, certainly forcefully. A global recognition of monetary system breakdown is in progress. The QE2 launch, complete with further ruinous debasement of money, is imminent. The unexpected effect that will take inept myopic central bankers off guard is the powerful rise in the Gold price. It foretells of the next powerful phase of the financial crisis that has been covered in detail in the Hat Trick Letter, gory detail. Dan Norcini, the gold, currency, and commodity analyst, put it so well. He said, "What we are witnessing is the death throes of a debt based monetary system, of which those presiding over it apparently have come to believe their own delusions. The US public is learning what our grandfathers learned as a result of the Great Depression. Debt is something to be avoided, not heaped up and accumulated... Yet, all of this is lost upon the monetary lords who have their noses so close to the ground sniffing out the scent that they cannot see that the path ahead leads off the edge of an abyss, from which there is no escape."

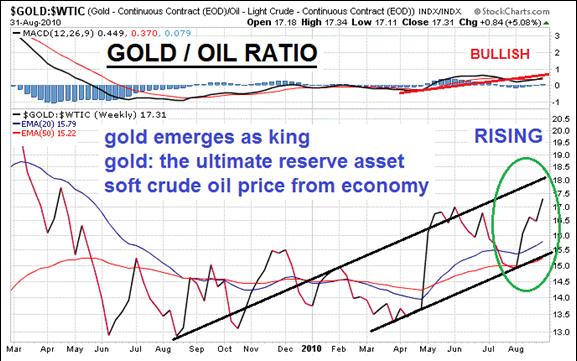

The Gold & Silver charts are both bullish, but in different ways. Gold is lifting off a base, while silver has surged upward out of a pause pattern, as described last week. Distrust for the monetary system has gone global. Gold & Silver are accepted as reserve assets, the best safe haven not tied to counter-party debt risk. Watch the Gold/Oil Ratio, which is poised to rise noticeably. Gold is the commodity king, namely it is money. The worldwide recession will keep the crude oil price subdued until the USTreasury bubble pops. Then, at that time, several major commodity hedges will jump in price, rendering a cost shock to the USEconomy. It is broken to the core, broken at the foundation, broken from grotesque imbalances, broken from vast pervasive insolvency. An inflationary depression lies dead ahead! Notice the recognition of Gold, its distinction as the king of commodities. The usual accepted hedge against the USDollar in Wall Street and London accounts has traditionally been crude oil.

After the severe damage done to sovereign debt in Europe, a wave comes steeped in crisis. Governments erroneously believe that they can inflate their way out of the crisis that has roots firmly connected to debt inflation. This is folly, as they will learn. Notice the King Gold, which is out-performing crude oil. The Gold/Oil Ratio has turned up strongly since the spring months. Deflation Knuckleheads will find they made serious analytic errors, when they grouped King Gold with the commodities. What folly. Gold is money, and money is becoming scarce. The current monetary system is debt in denominated form. The ratio will rise toward 20:1 in the coming months. The USEconomy in struggle, clear deterioration, even possible collapse, will keep the energy prices down generally. The global monetary virus outbreak will lift the Gold price to the heavens.

FROZEN REACTION FROM POLICY

Much of the business sector is frozen. Executives and managers are frozen in inaction from inability to anticipate what comes next. The landscape of regulations and official programs is too rapid, unpredictable, and illogical. We see stupid stuff like Clunker Car Programs. We see disruptive stuff like the Health Care Program. We see unpredictable stuff like the Home Purchase Credit Program. We see uncertainty, like with the home tax credit return. The biggest obstacle to business seems to be the Health Program monstrosity. It forces higher costs upon businesses while officials claim the exact opposite. Nowhere is the confusion greater than the housing and mortgage finance markets. Investors are front running the bond trade, with anticipation of USGovt monetization of more USTreasury Bonds and more USAgency Mortgage Bonds. The prospect of QE2 has brought about a perception that lower mortgage rates could come, and continue to come. The business sector cannot readily hire in this uncertain illogical environment in flux, where leadership is constantly being questioned. The home buyer demand was drawn forward, leaving a late summer and autumn vacuum. See the 27% decline in existing July home sales. The investment community is buying the USGovt guaranteed bonds, ahead of the QE2 launch. Investment in business equipment and capital formation is nearly non-existent. The USEconomy is frozen by erratic policy. In fact, the Gross Domestic Product is negative, once 3% is subtracted from the official downward revised 1.6% growth in 2Q2010. The subtraction is required for entrance into the world of reality, where hedonic and other productivity fudges must be removed.

A GENERATION OF LOST INDUSTRY

This is not a lost decade upcoming. The United States has suffered an entire generation of lost industry from its systematic dismantling, forfeit, and abandonment. The migration of industry began with Japan and the Pacific Rim in the 1980 decade. It continued in the 1990 decade, along with the NAFTA experiment with Mexico. Those border factories were removed with the advent of China. It culminated in the 2000 decade, with the death blow from the Chinese industrial expansion, often dubbed the Low Cost Solution. The entire generation, especially since the Chinese climax, replaced US factory income with service sector income, which included the finance sector from mortgage processing, credit derivatives, leveraged structured finance, and other financial engineering vehicles & structures. The emphasis on clean industry and sophisticated economical development was nothing more than a deceptive billboard to conceal the near total devotion to and dependence upon inflation for economic growth, which backfired and killed the system. The financial engineering offered no legitimate advancement to the society, and certainly not to the USEconomy, except the automatic teller machine, an observation made by former USFed Chairman Paul Volcker. His tenure was ended by the way, as a result of vicious rumors of a cancer debilitation, completely false stories spread by proponents of Alan Greenspan, a syndicate priest of high order. The Greenspan Era justified the virtues of risk offloaded in credit securities, hailed the sophistication of the system, and heaped praise upon each other's priests, right before the system collapsed from a flimsy and fraudulent foundation, leveraged inflation engines, and absent industry.

THE SOLUTION IS SIMPLE

The secret to a legitimate solution is easy. The big banks must write down their credit portfolios, and accept deep losses. If that results in liquidation, so be it!! Accounting fraud is not a substitute for restructure. Nor is dispatching badly impaired assets to the USFed, whose by all accounts is a Bad Bank Repository. Debate continues on the need to create a bad bank for dead assets, when the USFed is precisely that bank. Toxic assets held by the big banks must be liquidated. The phony propped credit markets must be permitted to fail, and to find proper value via equilibrium processes. Nowhere is equilibrium sought, as everywhere it is avoided. The USGovt should exit and quit the game of stimulus, intervention, and market distortion. The USGovt is delaying the inevitable. The financial markets should seek their bottoms for clearing supply. The bank leaders must be liquidated, removed from power, and face some prosecution. The Too Big To Fail premise must be rejected. The Zombie Big Banks threaten the entire system. If truth be told, they control the leadership of the USGovt itself. Dead entities control the USGovt, lodged in a stranglehold!!

CONSTIPATION WHEN NO LIQUIDATION

This is remarkably simple economics analysis. Without substantial liquidation of the badly impaired assets held in tremendous volume within the big banks, further credit constipation will be the mainstay fixture. That asset clog includes the vast bank owned properties from home foreclosures. The REO count rises about 50 thousand homes per month, a figure roughly double from the January level. Without major liquidation initiatives, expect continued Zombie Big Banks cluttering space. Without major liquidation initiatives, expect continued demands from the Zombies for large tracts of money. Without major liquidation initiatives, expect continued $trillion fraud schemes with Fannie Mae as nexus. Without major liquidation initiatives, expect escalated growth of the USTreasury Bond bubble. In plain terms, the economic landscape and credit system cannot recover without the plowing under of the Big Banks. However, they control the USGovt, its finance ministry in the USDept Treasury, and the USDollar Printing Pre$$ itself. The big banks will NOT order their own death warrant, and face the financial gallows. To think otherwise, even for the national good, is folly. It is like asking a heavily armed bank thief in the middle of a crowded lobby, holding a few dozen hostages, to shoot himself in the head instead, for the good of the people. The credit engines of the USEconomy will not fire much at all unless the big banks are liquidated, or at least much of their balance sheets is liquidated. That would expose their deep insolvency and potentially lead to their failure. A run on those banks by depositors, and a ruinous sale of their corporate bonds by investors, would ensure the big banks death. They belong in the morgue, for the national good. Capitalism demands their plowing under to unleash hidden potential.

The ball & chain dragging down and keeping down the big banks is the housing market. The downward force of gravity is visible in the falling home prices. The deteriorating USEconomy still pulls down the monetary platform, as the credit portfolios are directly attached to the ball & chain. The USEconomy was given the appearance of growth from the housing bubble between years 2002 and 2006. Its asset bubble formed a foundation for the majority of the USEconomy, and whose accompanying mortgage finance bubble provided the liquidity to the system. In fact, the entire boom & bust served as vivid indisputable evidence that the home is not a tangible asset, but rather a financial asset, an abused asset. The mortgage foreclosure process is the final proof. The true tangible assets are crude oil and precious metals. Other commodities will be sacrificed in wholesale form in order to purchase energy and precious metals. Energy is needed for commercial survival, while gold is needed as bonafide safe haven for money.

GOVT DILEMMA

The USGovt finds itself managing a mangled menagerie of frozen fixtures, most of which are totally broken. It is the great investor in failure and fraud. Its actions cover up the fraud, from policy taken in full collusion. Should the leaders give orders that result in formal suicide ceremony of the big banks, a US version of harikari? Should the props be removed and force a USTreasury default? A default will occur anyway in my view, since it is only delayed. The USTreasury default will come as a result of trade war isolation, USDollar vicious cycles in USGovt deficit monetization, a massive sudden USDollar devaluation, or the USFed resignation from its Congressional contract amidst $1 trillion losses. Expect all the above in combination, each linked. The USFed already has compiled close to half a $1 trillion loss on its balance sheet.

A grand game of chicken by the USGovt and Wall Street control panel is taking place. All official plans are predicated upon an economic recovery in the United States. A great fan blows fake acidic money into the bankers trough, but the monetary system erodes as its pillars suffer continued gradual deep damage. The new debt, delivered as fresh paper, acts like acid on the capital base of the entire USEconomy. As described in previous articles, the United States possesses the worst economists in the world. They have no concept of capital formation, no concept of what constitutes money, no concept of legitimate income, and no willingness to liquidate the toxic assets that prevent a restructure and recovery. The big hairball in the system is the big banks. The American public cannot survive on a limited credit diet due to big bank hairballs clogging the system.

HEIGHTENED RISK OF USTREASURY BUBBLE

A growing risk is palpable of migration away from USTBonds. It could come very soon. After the housing & mortgage twin bubbles and consequent bust, the last asset bubble has a little more ways to go. The last asset bubble is the USTreasury Bond, the entire complex. In fact, the bubble extends to the Fannie Mae bonds as well, since under USGovt guarantee. Perhaps a 2.0% long bond yield will be the sentinel signal to abandon and sell, setting up a bond bust. An extreme risk is present for the next important event to frighten the horses that prop USTBonds. What will be the rattlesnake in the sand? Foreign creditor sales in volume? A ramped up trade war? Harsh criticism for improper USDollar printing in monetization schemes, finally in the open? Recognition of a $1 trillion tab in war spending? A river of hyper-inflation is lodged in the USTBond dam, whose walls are nothing more than paper reeds held together by bad verbal glue, uttered by bank leaders who increasingly lack credibility.

Witness the failed central bank franchise system, and USFed Chairman Bernanke without any tools left. Witness the systemic failure of the USEconomy (and Mexico too). All USFed recovery scenarios depend upon a USEconomic recovery, which itself is completely dependent upon a US housing market recovery and a US banking system recovery. No recovery will come, since no Big Bank liquidation will be permitted. Therefore the USFed will walk the pirate plank to a great death of insolvency and ruin, which will spawn a USTreasury default, my forecast made two years ago. It is more certain than ever before. The safe haven is gold & silver. The USTreasury Bond grand dissipation, the long bust process, will catapult the Gold price toward $3000, and suddenly. The gold community will find great amusement in watching the reaction to the naysayers and critics, except the world will change into something hardly recognizable. It will turn into an ugly version of Mad Max, the movie. Shortages and crises will abound. Chaos will reign. A form of darkness will befall the earth.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

At least 30 recently on correct forecasts such as the Lehman Brothers failure, numerous nationalization deals such as for Fannie Mae, grand Mortgage Rescue, and General Motors.

“You freakin rock! I just wanted to say how much I love your newsletter. I have subscribed to Russell, Faber, Minyanville, Richebacher, Mauldin, and a few others, and yours is by far my all time favorite! You should have taken over for the Richebacher Letter as you take his analysis just a bit further and with more of an edge.” - (DavidL in Michigan)

“I used to read your public articles, and listen to you, but never realized until I joined what extra and detailed analysis you give to subscription clients. You always seem to be far ahead of everyone else. It is useful to ‘see’ what is happening, and you do this far better than the economists! I can think of many areas in life now where the best exponent is somebody not trained academically in that area.” - (JamesA in England)

“A few years ago, I was amazed at some of the stuff you were writing. Over time your calls have proved to be correct, on the money and frighteningly true. The information you report is provocative and prime time that we are not getting in the news. I was shocked when I read that the banks were going to fail in one of your prescient newsletters.” - (DorisR in Pennsylvania)

“You seem to have it nailed. I used to think you were paranoid. Now I think you are psychic!” - (ShawnU in Ontario)

“Your unmatched ability to find and unmask a string of significant nuggets, and to wrap them into a meaningful mosaic of the treachery-*****-stupidity which comprise our current financial system, make yours the most informative and valuable of investment letters. You have refined the ‘bits-and-pieces’ approach into an awesome intellectual tool.” - (RobertN in Texas)

by Jim Willie CB

Editor of the “HAT TRICK LETTER”

Home: Golden Jackass website

Subscribe: Hat Trick Letter

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by compromised central bankers and inept economic advisors, whose interference has irreversibly altered and damaged the world financial system, urgently pushed after the removed anchor of money to gold. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.