Stocks Secular Bull and Bear Markets and the Dark Side of Budget Deficits

Stock-Markets / Stock Markets 2010 Aug 28, 2010 - 01:05 PM GMTBy: John_Mauldin

Secular Bull and Bear Markets

Secular Bull and Bear Markets

It's Not the (Stupid) Economy

The Consequences of a Credit Crisis

The Dark Side of Deficits

In the pre-crisis days, I used to write about things like P/E ratios, secular bull and bear markets, valuations, and all of the things we used to think about in the Old Normal. But what about those topics as we begin our trip through the New Normal? It's time to reconvene class and think through what might change and what will remain the same. I think this will be a fun read - and let me tip my hand. I come out on the side of a new secular bull that gets us back to trend - but not just yet. The New Normal has to have its turn first. (Note: this will print out longer than usual, as there are a lot of charts.)

And speaking of first, I once again need some help from readers. I will be in "jail" next week for the Muscular Dystrophy Society. I need you to help bail me out. You can go to https://www.joinmda.org/downtowndallas2010/johnm and make a donation to help kids and families who really need help in these difficult times, and also help sponsor research that will eventually cure this disease. If you follow the link, you can see a cute video - and then make your donation!

I thank you and I am sure Jerry's kids thank you too!

Secular Bull and Bear Markets

Market analysts (of which I am a minor variety) talk all the time about secular bull and bear cycles. I argued in this column in 2002 (and later in Bull's Eye Investing) that most market analysts use the wrong metric for analyzing bull and bear cycles.

(For the record, even though I am talking about the US stock market, the principles apply to most markets everywhere. We are all human.)

"Cycles" are defined as events that repeat in a sequence. For there to be a cycle, some condition or situation must recur over a period of time. We are able to observe a wide variety of cycles in our lives: patterns in the weather, the moon, radio waves, etc. Some of the patterns are the result of fundamental factors, while others are more likely coincidence. The phases of the moon occur due to cycles among the moon, the earth, and the sun. In other situations, though, apparent patterns are no more than the alignment of random events into an observable sequence.

All cycles have several components in common. Cycles have a start and an end, they have characteristics that repeat from cycle to cycle, and they often have an explainable cause.

Stock market observers have identified what they believe to be scores of cycles, patterns, correlations, and relationships that have spawned a seemingly endless inventory of predictions and trading schemes. Every trader has his favorite system, well-fortified with back-tested "research" and "facts." These systems all work fine until you begin to use them with real money.

The patterns are so numerous that some market experts discount all theories and acquiesce to a philosophy of randomness (that would be you, Burt!). However, just because we don't understand it, doesn't mean there's not useful information contained within a pattern.

I argue that we should use valuations and not prices as the criterion for determining secular bull and bear cycles. If you use valuations, the cycles jump off the page at you. Using prices, it is very difficult. Let's look at a table prepared by my good friend Ed Easterling of Crestmont Research. Ed co-authored the two chapters in Bull's Eye Investing on stock market cycles and has a treasure trove of charts and tables on a wide variety of investment topics at www.crestmontresearch.com. And his book Unexpected Returns is a must-read for anyone who manages money, whether their own or someone else's.

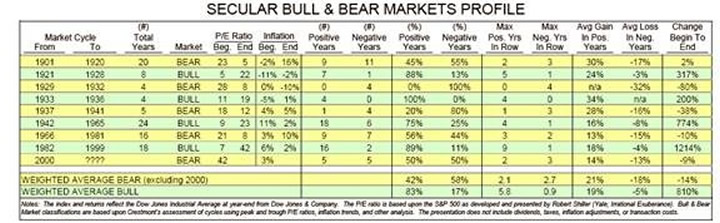

OK, the following chart shows secular bears in terms of valuations. There have been four bulls and five bears (we are in one now) since 1900. (You can see a larger chart at Ed's site, under secular cycles.)

Secular bulls begin with low valuations and continue until valuations get "too high" in terms of P/E ratios. The opposite for secular bears. The average cycle over the last 110 years lasted about 13 years. These are not short-term phenomena.

Within those longer-term secular cycles you can have so-called cyclical swings based on price, and some of those counter-trend cycles can be quite large!

The first cycle of the twentieth century was a bear. It started in 1901 with the market P/E ratio cresting at 23. Twenty years later, with the P/E ratio firmly in single digits at 5, the bear went into hibernation. Over the twenty years of that secular bear, the Dow Jones Industrial Average (DJIA) had managed to tick up from 71 at year-end 1900 to 72 at year-end 1920.

But, during those two decades, the market moves were far from calm. Annual returns from New Years' Eve to New Years' Eve ranged from -38% to +82%! The best-performing three years were +82%, +47%, and +42%. After each of those years I am sure the pundits proclaimed the death of the bear. Yet the three worst years were -38%, -33%, and -31%. As we'll see with most secular bear cycles, the period was as violent and choppy as the high seas in a monsoon. Across the 20 years in this bear cycle, 45% were positive-return years - but never more than two in a row! The 11 down years were generally singles or pairs, with only one three-year stretch at the start of the cycle. Although the average gain was +30% and the average loss was 17%, the change from beginning to end was a paltry +2% in total.

Yet during that secular bear cycle, the economy grew and earnings rose. However, P/E valuations declined and offset virtually all of the economic growth. The market's price (P) was essentially unchanged from start to finish, and E (earnings per share) rose sharply. So with the market price (P) virtually unchanged, it is clear that the decline in the P/E ratio offset the gains in earnings (E). Earnings growth is often strong in bear markets - and that growth is eroded by declining P/E ratios.

Most investors do not think of the years 1933-36 as being part of a bull cycle, as the markets did not make a new high from the 1929 high. We think of those times as the heart of the Depression. But P/E ratios rose from single digits to 19, and the market tripled in just a short time. It behooves those who are genetically predisposed to a bearish position to remember that markets have a logic of their own.

The critical factor is to notice that at the start of each bull cycle, the markets had single-digit P/E ratios, with no exception. NO secular bull market ever began with high P/E ratios, even though significant rallies often started from high P/E ratios. The lesson of history is that all periods of high valuations come to an unhappy end.

And that will be the case for cycles to come. Notice that real secular bull cycles begin with low double-digit or single-digit P/E ratios. Today the P/E on reported earnings is 16.3, down from the 42 at which this cycle started, but still a long way to go until we get to low double digits.

You hear a lot of BS on various media about forward P/E ratios being only 11.5; so if that is the case then stocks are cheap, even by my standards. But those stock touts and shills use operating earnings, something that was really never done until the 1990s, and that is a way for companies and people who want you to buy stocks or mutual funds to maintain that valuations are better than you think. Operating earnings estimates are over 39% higher than estimated as-reported earnings.

Reported earnings are real, in our pockets, what we put on our tax returns. Operating earnings are of the EBIH variety, that is Earnings Before Interest and Hype, or Earnings Before Interest and Bad Stuff (the BS of earnings). Those are the expenses they ignore because they pinky swear those mistakes will never happen again. Anybody using operating earnings on TV should have a flashing warning underneath their picture that says "stock promoter" or "cheerleader" or worse. I lose patience with such pandering.

That being said, using reported earnings estimates, by the end of 2011 stocks may be getting to the place where there is some value in the broad market, based on history. Not by a lot, but enough that the next ten years might not be a write-off, again by historical standards. Enough to make me a bull? No, because we will likely not be down close to single digits. But we will be getting there.

It's Not the (Stupid) Economy

How many times are we told by the financial "experts" that the economy drives the stock market? It's often emphasized that when the economy picks up, the stock market will follow (or even lead).

While this may be true in the short term, the data clearly shows it is not so in the long term. The economy and earnings can be rising even as the market falls or drifts sideways. Over time, the stock market is driven by two major factors: long-term earnings and price/earnings (P/E) ratios. We do recognize that the economy clearly affects long-term earnings. As a matter of fact, research demonstrates a strong relationship between earnings and nominal economic growth.

However, the most significant driver of stock market returns is the valuation embedded in the P/E ratio. Over the past century, P/E ratios have cycled from higher levels to lower levels. The range from high to low has been substantial.

Let's accept that earnings are generally growing, increasing over time. When P/E ratios are rising, the double impact of rising earnings and rising P/E's produces substantial stock market gains - secular bull markets. When earnings are rising yet P/E ratios are declining, the offsetting impact is a choppy, flat stock market with some rather large downdrafts from time to time - a secular bear market.

Does the economy matter? Yes. Does the stock market necessarily follow the economy? No. The key to knowing the longer-term direction of the market is to know the longer-term direction of the P/E ratio.

Thus, the question of the day becomes: how can we know the direction of P/E ratios?

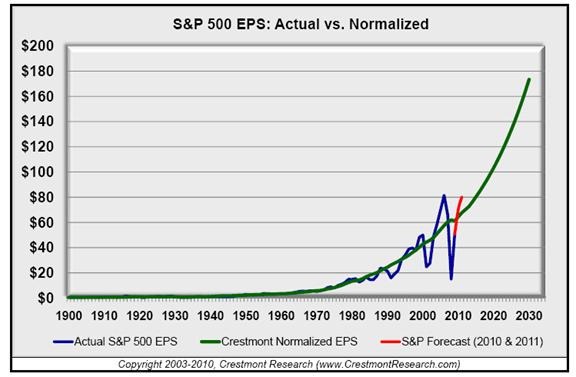

Interestingly, average P/E ratios tend to trend over long periods of time, and markets move around them. Let's look at some charts that Ed sent to me this morning. The first is the move in P/E ratios since 1970, with Ed giving us the trendline as a dotted line. The red portion going into 2011 is based on estimated earnings. Notice that after being way below trend we are on our way (if estimates are right) to being back above.

Now, let go back to 1900 and project forward on that trend line until 2030.

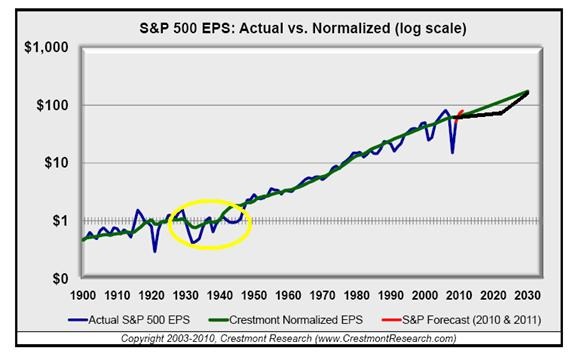

Notice that earnings rise to almost $180 (in real terms), well more than double from where they are today. And that has been the trend for 110 years, so it is fairly well established. But now let's look at this same chart on a log scale, and with me adding a few lines of my own.

Now, let me explain how I have marked up Ed's graph. First, I have circled in yellow the period from about 1930 through 1940. Note that the trend growth in earnings per share was well below the smoothed line we saw in the previous graph. No surprise, we were in a deflationary depression. But the point is that we got back to trend after the war and continued merrily on our way. Those ten years were not fun, but we did recover.

Now fast forward to today. What if something like the same phenomena happened over the next 20 years? I penciled in a black line going sideways (from 2010) for about 7-9 years as earnings rise, but not as fast, and then a true boom back to the "normal" trendline by the end of 2030. And what a boom it would be to get back to the long-term trend!

The Consequences of a Credit Crisis

I have written in numerous letters that the aftermath of a credit-crisis recession is a lengthy period, maybe as much as ten years, where all sorts of markets are more volatile and there are more frequent recessions. By definition, recessions are not good for earnings. We should expect two recessions between now and the end of the decade. That is what comes with the end of a credit crisis and the ensuing deleveraging cycle.

That is going to weigh on corporate earnings. But it will do more. Think about the period from 1966 through 1982. Four recessions, volatility, and P/E ratios ending up at 7, as Business Week famously declared "The End of Equities" on its cover. Who wanted to own stocks? Investors were disgusted.

Could that happen this decade? I think it is very possible. The stock market goes sideways and P/E ratios keep marching right on down, as we go through two more recessions and people get disgusted with stocks, just like in the early '80s. Then, as we (hopefully) get our government fiscal house in order, and as new technologies kick in, we see a true boom in the 2020s! It is once again the Roaring 20s!

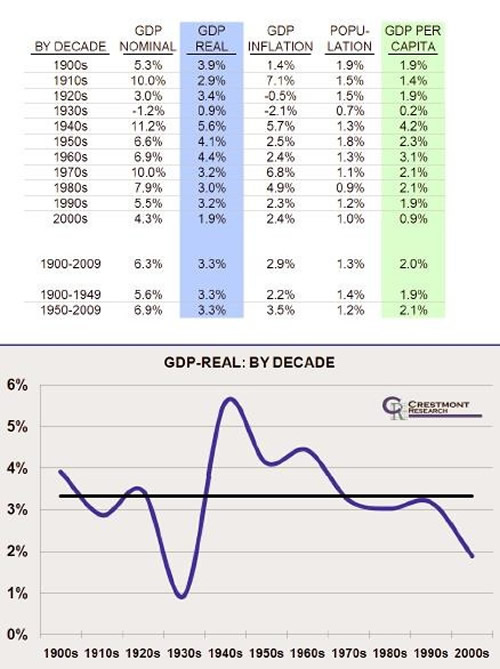

The Dark Side of Deficits

Two last charts from Ed. The first is the average GDP for the last 110 years, and the next is a graph of real GDP above and below that average of 3.3%. Note that GDP per capita in the 2000s was the second lowest for the last 110 years. Also that real GDP was the second lowest. Not pretty.

One could take comfort from the long perspective that the US will get back to trend GDP growth of 3.3% and that earnings will go back to trend, as I illustrated in a previous chart. That would require a decade well above trend growth to balance things out. And that is what SHOULD happen.

There is one caveat. The research of Reinhardt and Rogoff demonstrates that when the government debt-to-GDP level gets to about 90%, trend growth seems to drop by about 1%. They do not offer an explanation, just an observation. My speculation is that it might be government spending and debt crowding out private savings, not leaving enough for productive private investment.

But whatever - if we do not get control of our deficit spending, we (in the US) risk putting our growth in jeopardy. If we do indeed see trend growth slip to 2.3%, then my optimistic "we get back to trend earnings by 2030," along with a roaring bull market, is at serious risk.

Let me jump on Paul Krugman again. He writes a great op-ed in the NY Times today questioning whether we are in recovery, and then pounds the table for more stimulus money. He (and all neo-Keynesians everywhere, with too many in the government) only see the next 6-12 months. Running up debt today? No problem.

Yet we risk our future potential growth if we continue on our present track. The research is clear. If we wish avoid some pain today, we create even more pain, and not that far in the future. There are those among us who are like teenagers, wanting to make the easy choice and avoid the pain today, not worrying about the consequences down the road. Not getting our fiscal deficits under control risks the whole economy.

Let's summarize. We are still in a secular bear market. Valuations, while lower, are still not at what could be called historical cyclical bottoms. Patience is the order of the day. We will get there.

And for the record, I will probably become a bull way too early and have to endure some pain on the way to profit. Such is life.

And we risk that ultimately positive scenario if we do not get our federal fiscal house in order. If that does not happen, all bets are off. ALL BETS.

LA, Europe, Kansas City, and Houston

I was going to comment on Bernanke's speech, but this letter is near its end. Besides, what is there to really say? I have often complimented Bernanke on giving very clear speeches. This was not one of them. He was a three-handed economist (on the one hand, but on the other hand, and then on the other!) He covered every possible scenario, so no matter what happens he will have had something in the speech that was right. Oh, and he did say that more quantitative easing is on the table, even though the FOMC is deeply divided on that topic. Oh well.

I (and Tiffani, Ryan, Lively, and the nanny) have to fly to LA on Tuesday for two days of previously unscheduled meetings, and then it's back to Dallas for a speech to the local Tiger 21 group. Then, starting September 11, I fly to Amsterdam for the International Broadcasting Conference, then to Malta, Zurich, Mallorca, Denmark (speech open to public), and London, home for one day, and then off for a speech to Cambridge Brokers on the 24th. Then I'm in Houston on October 1 for another public speech.

And speaking of October, I turn 61 on the 4th. Where did the year go? It seems like we were just having my 60th birthday party a few weeks ago!

I am experiencing an interesting new period of life. Tiffani has the nanny bring Lively (now 9 months) to my home office 2-3 days a week for the day, plus at lots of other times. I had forgotten what it is like to watch a baby grow up so fast - that first crawl, the first time she pulls up, first a lot of things. I am so lucky to be able to see all that! She recognizes my voice and gives me the biggest smile. And then Lively goes home and I don't have to change diapers. Is life great or what?

Time to hit the send button. A late happy hour awaits. Have a great week. Henry turns 29 this weekend, so some of the kids will gather to wish him the best. They just keep growing up.

Your waiting to channel his inner bull analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.