Hyperinflation or Recession?

Economics / Inflation Sep 21, 2007 - 06:14 AM GMTBy: Brian_Bloom

Zimbabwe is a country where hyperinflation is a reality as opposed to a theoretical possibility. The photograph below shows what it looks like to pay for lunch for eight people in that country. It was sent to me in an email dated September 18 th , 2007 . The meal – consisting of fillet steaks and beers – cost six million Zimbabwean dollars. What you are looking at is that amount of money in $1,000 notes being collected by the restaurant manager. I don't know if it included a Z$600,000 tip or not. The restaurant has no menu. Patrons wanting to eat are not offered a choice. They ask “what's left?” Still, they are able to smile. Such is the indomitability of the human spirit.

Zimbabwe is a country where hyperinflation is a reality as opposed to a theoretical possibility. The photograph below shows what it looks like to pay for lunch for eight people in that country. It was sent to me in an email dated September 18 th , 2007 . The meal – consisting of fillet steaks and beers – cost six million Zimbabwean dollars. What you are looking at is that amount of money in $1,000 notes being collected by the restaurant manager. I don't know if it included a Z$600,000 tip or not. The restaurant has no menu. Patrons wanting to eat are not offered a choice. They ask “what's left?” Still, they are able to smile. Such is the indomitability of the human spirit.

Photograph 1

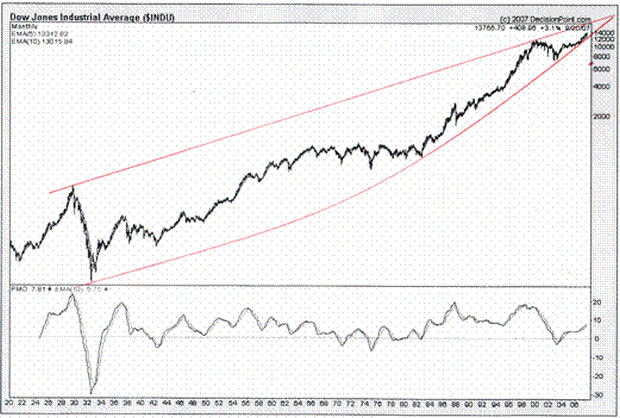

Of course, the above is an extreme case. However, the chart below – courtesy Decisionpoint.com - shows that hyperinflation is a real possibility within the USA if the Fed screws up big time. If the lower curved trendline prevails, and the boundary of the upper trendline is penetrated to the upside, the Dow may very well enter an exponential blow-off. If the above photograph is anything to go by, we absolutely do not want that to happen.

Chart 1

Theoretically, the role of the United States Federal Reserve Board is to balance employment against inflation using money supply, bank lending ratios and interest rates as their weapons. Historically, the target has been less than 5% unemployment rate (of those looking for work) and less than 3% inflation (given a target 3% p.a. growth rate in money supply which should be partially offset by population growth rate). That's roughly how it's supposed to work. Of late, the money supply has been growing at around 15% because the economy has been slowing.

On top of this growth in money supply, the Fed's recent decision to cut its bank lending rate has connotations which demand to be assessed.

Since the 1980s, this analyst has been well served by the mental model that the very raison d'etre of the world's Central Banks is as has been described above. Theoretically, given the weakness of the US Dollar, the Fed should have raised its lending rate. This would have served to protect the US Dollar and, thereby, the US economy in the medium to longer term. However, in light of the number of mortgage refinancing contracts in the pipeline, and the sub-prime mortgage debacle, raising the rate was not an option. Given the available facts, this analyst was of the view that the safest course of action would have been to do nothing. But the Fed cut its rate. This disconnect in logic now demands that I reassess my mental model.

The base assumption of the Central Bank model is that the Central Bank exists to manage the pace of underlying economic activity in the interests of the entire community.

There has been significant discussion on the gold related websites as to whether or not – given the closing of the gold window by Richard Nixon in 1971 – hyperinflation was an inevitability.

To refresh readers' memories, I have reproduced the relevant element of Article1, Section 8 of the US Constitution:

“Section 8 - Powers of Congress

The Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises , to pay the Debts and provide for the common Defence and general Welfare of the United States; but all Duties, Imposts and Excises shall be uniform throughout the United States;

To borrow money on the credit of the United States;

To regulate Commerce with foreign Nations, and among the several States, and with the Indian Tribes;

To establish an uniform Rule of Naturalization, and uniform Laws on the subject of Bankruptcies throughout the United States;

To coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures;

To provide for the Punishment of counterfeiting the Securities and current Coin of the United States;” (my italics)

It is my understanding that the underlying rationale of those who drafted the US Constitution was that “money supply” should be controlled by the Congress of the United States (as opposed to Private Enterprise). The coining of money (i.e. the reliance of silver and gold standard) was incidental to this overriding principle. That is why counterfeiting was to be regarded as a punishable offence.

It has been argued by some, including this analyst, that the act of creating the US Fed hijacked the intention, originally espoused by Thomas Jefferson, that Congress should manage the money supply. There is no purpose to be served in rehashing the arguments here, but the bottom line conclusion is that the structure of the US Federal Reserve has inherent conflicts of interest between Government (supposedly representing the people of the USA ) and Private Enterprise, whose parochial interests are now arguably being served by the Fed.

Arguably, the decision of the US Federal Reserve to lower its bank lending rate, announced on September 18th 2007 , is prima facie evidence that the short term interests of Private Enterprise have superceded the longer term interests of US citizens in general.

Shortly after the Fed's announcement, it was made public that the Producer Price Index had fallen. This, at face value, might have been the society wide justification for the cut in interest rates.

However, such an argument is nonsensical. To demonstrate this, it seems appropriate to lead the reader through a case study.

As regular readers know, I have recently completed a novel which is intended for world-wide publication within the next six to nine months following editing. When I commenced drafting the manuscript in October 2005, the target retail price of the novel, Beyond Neanderthal , was to be US$25 plus postage. The rate of exchange between the US $ and the Australian Dollar at that time was around US$0.75:A$1. This implied that Beyond Neanderthal would retail at around A$33.50 a copy in Australia

As the author, I am now facing a dilemma. Costs of printing and binding have risen, whilst the exchage rate as at today's date is US$0.869:A$1. i.e. If I keep the price constant at US$25, I will have to charge A$28.65 (approximately 15% less in the face of higher production costs). Alternatively, if I keep the price constant at A$33.50, I will have to charge US$29 a copy in the USA . The price within the USA will have risen 16%.

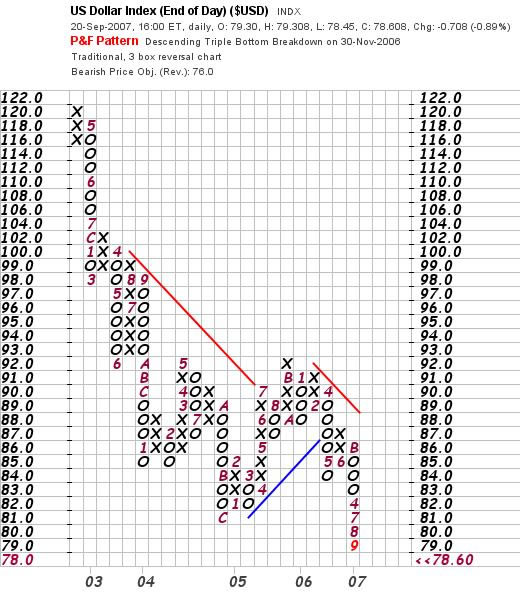

It doesn't end there. If we look at the Point and Figure Chart of the US Dollar Index below (courtesy Stockcharts.com) we see that a target of 76 is being called for

Chart 2

This implies that Beyond Neanderthal will need to be priced at US$29 X (78.6/76) = US$30 plus postage.

We could go on, but you get the drift. In a world that was previously dominated by the US Dollar in international trade, everything was benchmarked against the US Dollar. No longer!

What we are now facing is a world where – because of a single irresponsible decision of the United States Federal Reserve Board – the US Dollar has broken to historical lows, and the centre of gravity of the world's economy has shifted away from the United States.

For the purposes of international trade and commerce this is an extremely important point. As an Australian citizen, I can no longer afford to think in terms of pricing my novel using the US$ as the benchmark. Now take my case, and apply it to:

• The oil industry

• Consumer exports to the USA

• Service exports to the USA

• International capital movements

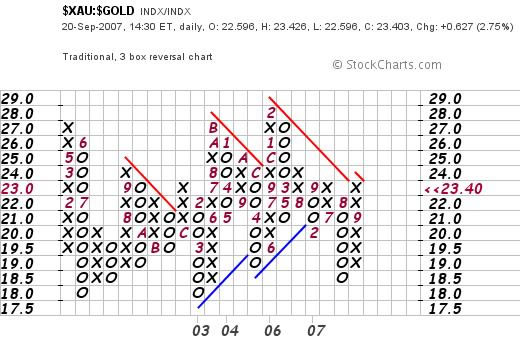

There are those who are excited about the fact that the gold price has broken up to new heights in US$ denominated terms. Typically, those people will be living within the USA.

However, when you look at the gold price from the perspective of a non-US citizen, you see a chart that looks something like the goldollar chart below (courtesy decisionpoint.com)

Chart 3 (Composite of three charts)

![]()

What it shows is that the golodollar index has not yet risen to a new high. i.e. The gold price has been rising in US Dollars primarily to compensate for the fall in the US Dollar.

i.e. Gold has been rising in price to protect US citizens but not yet non US Citizens.

This brings us to the ratio of the Gold Share Index to the Gold Price. The chart below is courtesy of stockcharts.com

This chart shows that, as at September 20th 2007 , the gold shares were still in a bear trend relative to the gold price.

Chart 4

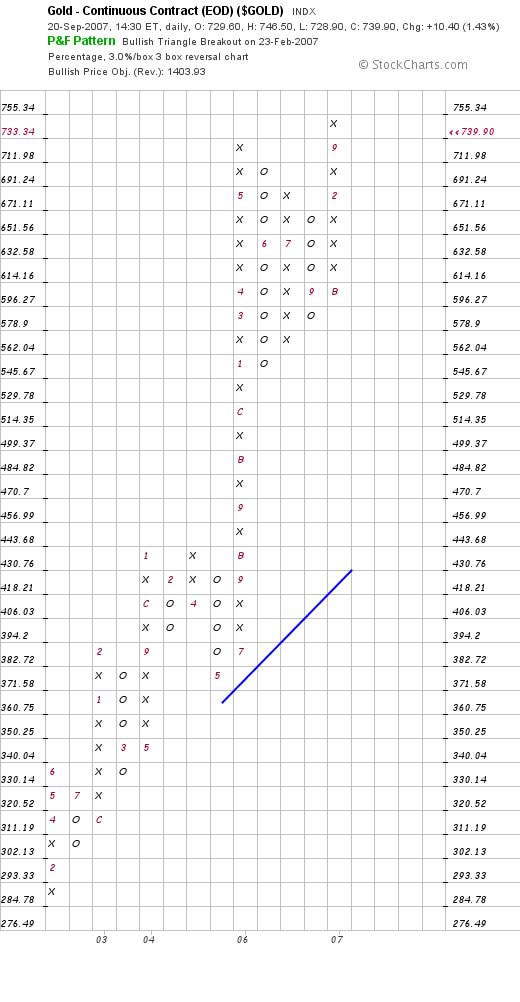

Frankly, I am personally being guided by the chart below – which is a 3% X 3 box reversal chart of the US$ denominated gold price (courtesy stockcharts.com)

Chart 5

Having broken to a new high, I can now believe the $1400 price target and, as a result of this believability, I have bought back into some gold shares. The “cost” to me of doing this was a loss of 7% profit, including brokerage.

Having said this, now let's look at the downside again. If the Gold Price in US$ doubles, and the US Dollar Index halves, it is likely that I will have made a mistake – because the costs of operating a gold mine (in the USA) will rise in proportion to the price the mine receives. i.e. Profits will not rise in proportion to the rise in the gold price.

What seems more likely to happen, though, flows from the discussion on the pricing of Beyond Neanderthal . At a price of US$30 a copy I am likely to sell fewer copies within the USA than if I charged US$25. Indeed, the volume of gold sales might even fall – because (for example) Indians may buy less gold to celebrate their weddings if they are selling fewer services to the USA . Take the argument across the entirety of the world economy and, what we seem to be facing is the threat of a world-wide recession as the volume of commercial transactions by foreigners with the USA shrinks.

Conclusion

The decision by the US Fed to reduce its bank lending rate – ostensibly to counteract a reduction in the producer price index – was probably a seminal development in the history of the world's economy. If the end result is that this rate reduction gives rise to a continuing fall of the US Dollar index, then inflation within the USA will likely rise strongly, and volumes of transactions will likely fall.

Paradoxically, the cut in interest rates seems likely to have the opposite effect of its stated intent. It seems more likely to give rise to an acceleration of the arrival of recessionary conditions – having bought sufficient time to allow maintenance of the status quo until after the US Presidential Elections.

Sadly, we are living in an extraordinarily cynical world where the parochial interests of the few now patently transcend the interests of the many.

By Brian Bloom

www.beyondneanderthal.com

Since 1987, when Brian Bloom became involved in the Venture Capital Industry, he has been constantly on the lookout for alternative energy technologies to replace fossil fuels. He has recently completed the manuscript of a novel entitled Beyond Neanderthal which he is targeting to publish within six to nine months.

The novel has been drafted on three levels: As a vehicle for communication it tells the light hearted, romantic story of four heroes in search of alternative energy technologies which can fully replace Neanderthal Fire. On that level, its storyline and language have been crafted to be understood and enjoyed by everyone with a high school education. The second level of the novel explores the intricacies of the processes involved and stimulates thinking about their development. None of the three new energy technologies which it introduces is yet on commercial radar. Gold, the element , (Au) will power one of them. On the third level, it examines why these technologies have not yet been commercialized. The answer: We've got our priorities wrong.

Beyond Neanderthal also provides a roughly quantified strategic plan to commercialise at least two of these technologies within a decade – across the planet. In context of our incorrect priorities, this cannot be achieved by Private Enterprise. Tragically, Governments will not act unless there is pressure from voters. It is therefore necessary to generate a juggernaut tidal wave of that pressure. The cost will be ‘peppercorn' relative to what is being currently considered by some Governments. Together, these three technologies have the power to lift humanity to a new level of evolution. Within a decade, Carbon emissions will plummet but, as you will discover, they are an irrelevancy. Please register your interest to acquire a copy of this novel at www.beyondneanderthal.com . Please also inform all your friends and associates. The more people who read the novel, the greater will be the pressure for Governments to act.

Brian Bloom Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.