Elements of Deflation and the Super-Trend Puzzle

Economics / Deflation Jul 24, 2010 - 04:55 PM GMTBy: John_Mauldin

Some Thoughts on Deflation

Some Thoughts on Deflation

The Super-Trend Puzzle

The Elements of Deflation

The debate over whether we are in for inflation or deflation was alive and well at the Agora Symposium in Vancouver this this week. It seems that not everyone is ready to join the deflation-first, then-inflation camp I am currently resident in. So in this week's letter we look at some of the causes of deflation, the elements of deflation, if you will, and see if they are in ascendancy. For equity investors, this is an important question because, historically, periods of deflation have not been kind to stock markets. Let's come at this week's letter from the side, and see if we can sneak up on some answers.

Even on the road (and maybe especially on the road, as I get more free time on airplanes) I keep up with my rather large reading habit. This week, the theme in various publications was the lack of available credit for small businesses, with plenty of anecdotal evidence. This goes along with the surveys by the National Federation of Independent Businesses, which continue to show a difficult credit market.

Businesses are being forced to scramble for needed investments, generally having to make do with cash flow and working out of profits. This is an interesting quandary for government policy makers, as 75% of the "rich" that will see the Bush tax cuts go away are small businesses.

There was a great graphic (that I now cannot find) showing that all net new jobs of the past two decades have come from small businesses and start-ups. And yet as of now, when structural employment is over 10% (if you count those who were considered to be in the work force just a few months ago), we want to reduce the availability of revenues to the very people we want to be hiring new workers, and who are cash-starved as it is.

It is not just that taxes will go from 35% to just under 40%. It is the increase in Medicare taxes coming down the pike, too. We are taking money from private hands, where it has the potential to increase productivity, and putting it into government hands, where it will do nothing for growth of the economy. There is no multiplier for government spending. And tax increases reduce potential GDP by a multiplier of at least 1 and maybe 3, depending on which study you want to cite.

I understand that taxes have to go up. I get it. But we would be better off having a discussion of where we want to tax dollars to come from before we risk hurting an economy that will barely be growing at 2% in the 4th quarter, and may be well below that. It is the increase in taxes that has me concerned about a double-dip recession.

That being said, the announcement by several prominent Democratic senators that they think we should extend the Bush tax cuts is significant. As I said a few weeks ago, we should not experience a double-dip recession absent policy mistakes. A slow-growth world, yes. But an actual double dip is rare.

If Congress were to extend the Bush tax cuts for at least a year, until the presidential commission on taxes is done with its work and THEN have the debate, it would make me far more optimistic. And it would be quite bullish for stocks, I think. Businesses would know how to plan, at least, for a year, and the economy would be given more time to actually recover. I am not ready to channel my inner Larry Kudlow, but from what we see this summer it would make me more optimistic and reduce the chances of a double-dip recession significantly.

Some Thoughts on Deflation

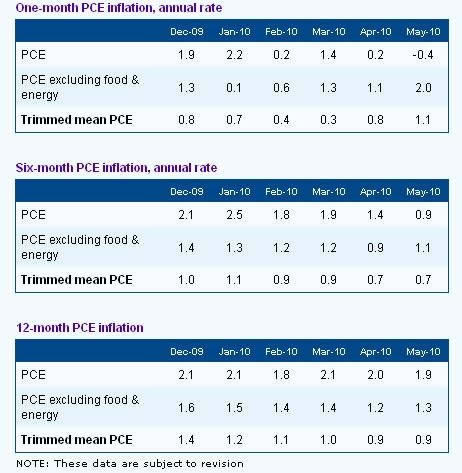

Inflation in the US is now just below 1%, whether you look at the CPI, the Cleveland Fed's measure, or the Dallas Trimmed Mean CPI. The Fed's favorite, the PCE, is also approaching 1%. The Dallas numbers are a little behind, but they are at all-time lows.

The classic definition of deflation is an economic environment that is characterized by inadequate or deficient aggregate demand. Prices in general fall, and normal economic relationships start to fall apart.

The Super-Trend Puzzle

I am a big fan of puzzles of all kinds, especially picture puzzles. I love to figure out how the pieces fit together and watch the picture emerge, and have spent many an enjoyable hour at the table struggling to find the missing piece that helps make sense of the pattern.

Perhaps that explains my fascination with economics and investing, as there are no greater puzzles (except possibly the great theological conundrums, or the mind of a woman, about which I have only a few clues).

The great problem with the economic puzzles is that the shapes of the pieces can and will change as they rub against one another. One often finds that fitting two pieces together changes the way they meld with the other pieces you thought were already nailed down, which may of course change the pieces with which they are adjoined; and suddenly your neat economic picture no longer looks anything like the real world.

(Which is why all of the mathematical models make assumptions about variables that allow the models to work, except that what they end up showing is not related to the real world, which is not composed of static variables.)

There are two types of major economic puzzle pieces. The first are those pieces that represent trends that are inexorable: they will not themselves change, or if they do it will be slowly; but they will force every puzzle piece that touches them to shift, due to the force of their power. Demographic shifts or technology improvements over the long run are examples of this type of puzzle piece.

The second type is what I think of as "balancing trends," or trends that are not inevitable but which, if they come about, will have significant implications. If you place that piece into the puzzle, it too changes the shape of all the pieces of the puzzle around it. And in the economic super-trend puzzle, it can change the shape of other pieces in ways that are not clear.

Deflation is in the latter category. I have often said that when you become a Federal Reserve Bank governor, you are taken into a back room and are given a DNA transplant that makes you viscerally and at all times opposed to deflation. Deflation is a major economic game changer. You can argue, as Gary Shilling does, that there is a good kind of deflation, where rising productivity and other such good things produces a general fall in prices, such as we had in the late 19th century. And as we have experienced that in the world of technology, where we view it as normal that the price of a computer will fall, even as its quality rises over time.

But that is not the kind of deflation we face today. We face the deflation of the Depression era, and central bankers of the world are united in opposition. As Paul McCulley quipped to me this spring, when I asked him if he was concerned about inflation, with all the stimulus and printing of money we were facing, "John," he said, "you better hope they can cause some inflation." And he is right. If we don't have a problem with inflation in the future, we are going to have far worse problems to deal with.

Saint Milton Friedman taught us that inflation is always and everywhere a monetary phenomenon. That is, if the central bank prints too much money, inflation will ensue. And that is true, up to a point. A central bank, by printing too much money, can bring about inflation and destroy a currency, all things being equal. But that is the tricky part of that equation, because not all things are equal. The pieces of the puzzle can change shape. When the elements of deflation combine in the right order, the central bank can print a boatload of money without bringing about inflation. And we may now be watching that combination come about.

The Elements of Deflation

Just as every school child knows that water is formed by the two elements of hydrogen and oxygen in a very simple combination we all know as H2O, so deflation has its own elements of composition. Let's look at some of them (in no particular order).

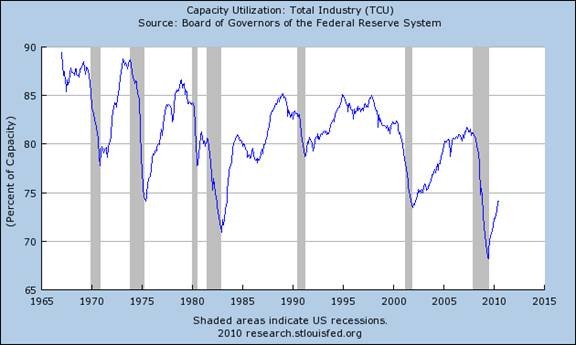

First, there is excess production capacity. It is hard to have pricing power when your competition also has more capacity than he wants, so he prices his product as low as he can to make a profit, but also to get the sale. The world is awash in excess capacity now. Eventually we either grow the economy to utilize that capacity or it will be taken offline through bankruptcy, a reduction in capacity (as when businesses lay off employees), or businesses simply exiting their industries.

I could load the rest of the letter with charts showing how low world capacity utilization is, but let's just take one graph, from the US. Notice that capacity utilization is roughly in an area that we associate with the bottom of past recessions (with one exception).

Deflation is also associated with massive wealth destruction. The credit crisis certainly provided that element. Home prices have dropped in many nations all over the world, with some exceptions, like Canada and Australia. Trillions of dollars of "wealth" has evaporated, no longer available for use. Likewise, the bear market in equities in the developed world has wiped out trillions of dollars in valuation, resulting in rising savings rates as consumers, especially those close to a wanted retirement, try to repair their leaking balance sheets.

And while increased saving is good for an individual, it calls into play Keynes' Paradox of Thrift. That is, while it is good for one person to save, when everyone does it, it decreases consumer spending. And decreased consumer spending (or decreased final demand, in economic terms) means less pricing power for companies and is yet another element of deflation.

Yet another element of deflation is the massive deleveraging that comes with a major credit crisis. Not only are consumers and businesses reducing their debt, banks are reducing their lending. Bank losses (at the last count I saw) are over $2 trillion and rising.

As an aside, the European bank stress tests were a joke. They assumed no sovereign debt default. Evidently the thought of Greece not paying its debt is just not in the realm of their thinking. There were other deficiencies as well, but that is the most glaring. European banks are still a concern unless the ECB goes ahead and buys all that sovereign debt from the banks, getting it off their balance sheets.

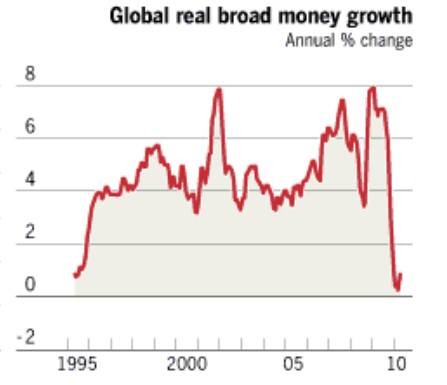

When the money supply is falling in tandem with a slowing velocity of money, that brings up serious deflationary issues. I have dealt with that in recent months, so I won't bring it up again, but it is a significant element of deflation. And it is not just the US. Global real broad money growth is close to zero. Deflationary pressures are the norm in the developed world (except for Britain, where inflation is the issue).

Falling home prices and a weak housing market are one more element of deflation. This is happening not just in the US, but also much of Europe is suffering a real estate crisis. Japan has seen its real estate market fall almost 90% in some cities, and that is part of the reason they have had 20 years with no job growth, and that the nominal GDP is where it was 17 years ago.

In the short run, reducing government spending (in the US at local, state, and federal levels) is deflationary in the short run. Martin Wolfe, in the Financial Times, wrote the following last week (arguing that that the move to "fiscal austerity" is ill-advised):

"We can see two huge threats in front of us. The first is the failure to recognize the strength of the deflationary pressures ... The danger that premature fiscal and monetary tightening will end up tipping the world economy back into recession is not small, even if the largest emerging countries should be well able to protect themselves. The second threat is failure to secure the medium-term structural shifts in fiscal positions, in management of the financial sector and in export-dependency, that are needed if a sustained and healthy global recovery is to occur."

Finally, high and chronic unemployment is deflationary. It reduces final demand as people simply don't have the money to buy things.

Deflation that comes from increased productivity is desirable. In the late 1800's the US went through an almost 30-year period of deflation that saw massive improvements in agriculture (the McCormick reaper, etc.) and the ability of producers to get their products to markets through railroads. In fact, too many railroads were built and a number of the companies that built them collapsed. Just as we experienced with the fiber-optic cable build-out, there was soon too much railroad capacity, and freight prices fell. That was bad for the shareholders but good for consumers. It was a time of great economic growth.

But deflation that comes from a lack of pricing power and lower final demand is not good. It hurts the incomes of both employer and employee, and discourages entrepreneurs from increasing their production capacity, and thus employment.

That is why it will be important to watch the CPI numbers even more closely in the coming months. The trend, as noted above, is for lower inflation. If that continues, the Fed will act. I did a summary of Bernanke's 2002 speech on deflation a few weeks ago. For those who didn't read it, here is the link.

If the US gets into outright deflation, I expect the Fed to react by increasing their assets and by outright monetization, buying treasuries from insurance and other companies, as putting more money into banks when they are not lending does not seem to be helpful as far as deflation is concerned. More mortgages? Corporate debt? Moving out the yield curve? All are options the Fed will consider. We need to be paying attention.

One final thought before I hit the send button. Recessions are by definition deflationary. One of the things we learned from This Time is Different by Rogoff and Reinhart is that economies are more fragile and volatile and that recessions are more frequent after a credit crisis. Further, spending cuts are better than tax increases at improving the health of an economy after a credit crisis.

I think we can take it as a given that there is another recession in front of the US. That is the natural order of things. But it would be better to have that inevitable recession as far into the future as possible, and preferably with a little inflationary cushion and some room for active policy responses. A recession next year would be problematic, if not catastrophic. Rates are as low as they can go. Higher deficits are not in the cards. Yet unemployment would shoot up and tax collections go down at all levels of government.

That is why I worry so much about taking the Bush tax cuts away when the economy is weak. Now, maybe those who argue that tax increases don't matter are right. They have their academic studies. But the preponderance of work suggests their studies are flawed and at worst are guilty of data mining (looking for data that supports your already-developed conclusions.)

Professor Michael Boskin wrote today in the Wall Street Journal:

"The president does not say that economists agree that the high future taxes to finance the stimulus will hurt the economy. (The University of Chicago's Harald Uhlig estimates $3.40 of lost output for every dollar of government spending.) Either the president is not being told of serious alternative viewpoints, or serious viewpoints are defined as only those that support his position. In either case, he is being ill-served by his staff."

As noted at the beginning of this letter, I find it very encouraging that there is a movement among Democrats to think about at least postponing the demise of the Bush tax cuts until the economy is in better shape. Those who advocate letting them lapse are in effect operating on our economic body without benefit of anesthesia. If they are wrong, the consequences will be most severe.

We need to think any tax increase through very thoroughly.

Maine, New York, Turks and Caicos, and Europe

Vancouver was a lot of fun. The Agora Symposium had some very good speakers, and if they invite me back again some time, I intend to stay for the whole event. The Whiskey panel on Wednesday night was a hoot. The opinions shared were quite varied, with a lot of humor and some good-natured arguments. And I am going to try and get a link to some of the speaker presentations, if they will let me post a few.

I am rounding the corner and seeing the home stretch on my book. I hope to have a first draft in a few weeks, and then not take more than a month on edits and rewrites. I need to get it done, because my travel schedule the first part of August is hectic. I go with son Trey to the annual Shadow Fed fishing trip in Maine, which this year will be covered by Bloomberg TV and radio, then I'm back to New York for an evening , on to DC for some consulting for the Defense Department, and then off for five glorious days in the Turks and Caicos, courtesy of Barry Habib and his family (of Mortgage Market Guide fame). I am sure I will get a little work done, but I intend to spend lots of time pleasure reading.

Then in mid-September I go to Europe. We are still finalizing the details and will let you know the schedule soon.

I took the Agora team at their word and brought a bottle of chardonnay to the panel with me, sharing some of the precious liquid. (It was a Kistler given to me by my Canadian partner, John Nicola.) Of course, it was soon gone. Some considerate attendee brought me another large wine glass filled with chardonnay, evidently worried about the arduous, thirsty work I was doing arguing with Porter Stansberry. I really did want something to drink, and for whatever reason did not sip but just took a big gulp. Turns out it was pure scotch, not chardonnay. I did keep from choking, but I decided that discretion being the better part of valor, I'd better share the scotch as well. And next time, I will sip first.

Your just enjoying life now while I worry about the future analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.