North America Doesn't Need China's Rare Earth Metals

Commodities / Metals & Mining Jun 21, 2010 - 01:46 PM GMTBy: The_Gold_Report

Everybody's talking about rare earth elements (REEs), but does anyone truly understand them? With nearly 50 years in the industry, independent Metals Consultant Jack Lifton sure does. The educational powerhouse in this burgeoning space returns to The Gold Report with a look toward future trends and a plan to emancipate North America from China's REE monopoly.

Everybody's talking about rare earth elements (REEs), but does anyone truly understand them? With nearly 50 years in the industry, independent Metals Consultant Jack Lifton sure does. The educational powerhouse in this burgeoning space returns to The Gold Report with a look toward future trends and a plan to emancipate North America from China's REE monopoly.

The Gold Report: Jack, since our first interview over a year ago, the rare earth space has received a lot of ink. You were one of the first to talk about these minor metals and their strategic importance to manufacturing and electronics. Could you give our readers a little refresher about some of these metals and their uses?

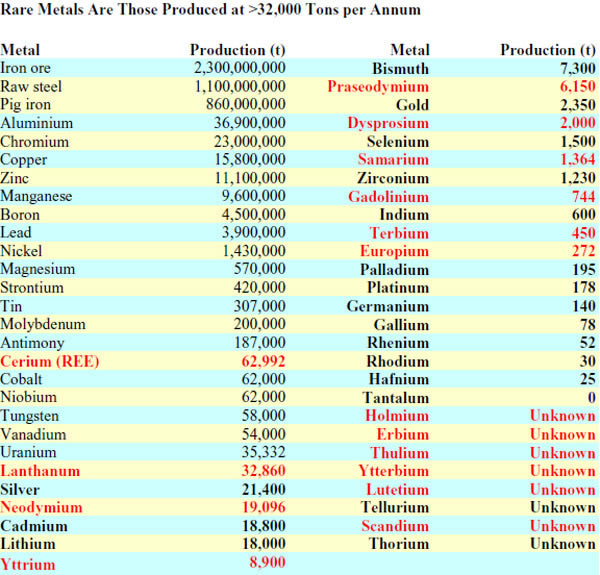

Jack Lifton: I define a rare metal by its production rate, because it doesn't matter how much of a metal there is in the earth's crust—or even how much of it is concentrated enough in accessible ore deposits to be, theoretically, recoverable. The only thing that matters is the amount of metal that is produced each year, because that's all we have available to us use now, period. That production rate depends, of course, on a combination of economics and technology.

The cost of producing the metal from any particular source must be less than its selling price, and the technology must exist before the extraction project (mining) to produce the metal from that particular ore deposit.

The following chart singles out the rare earth metals in red (the lanthanides, plus scandium and yttrium) from all other metals and rare metals by their 2009 production rate. It also identifies the 2010 rare metals as those beginning with, and including, silver, as well as all of those produced at a rate less than that of silver in 2009.

As of today, June 16, 2010, I think the future-use trends for those rare metals critical for mass-produced, consumer-use technology must be differentiated from future-use trends for the rare metals critical for military technology. These future-use trends may be qualitatively alike. For example, they may require small, powerful, permanent magnets; but their quantitative requirements for each category—civilian and military—–are different by orders of magnitude.

Forging technologies for the military, which began in World War II, created a supply chain for the rarest metals critical for military applications. But, once military demand was understood—and, thus, limited—there came into existence a surplus of metals that had never before been available to civilian scientists and engineers. This resulted in a revolution in the creation and miniaturization of technologies for mass-produced civilian (i.e., consumer, markets, etc.).

Today, the quantitative demand for rare metals by the military and civilian sectors of the economy has inverted. The civilian sector dominates the demand for rare metals critical for use in technologies; I call this subset of rare metals technology metals. For now, I'll concentrate on just those selected metals because increasing production from existing mines—or developing new ones—is so extremely capital-intensive and time-consuming, the probability of doing that declines rapidly as costs and expensive-to-fix technological issues mount. In fact, the stock market pundits like to gloss over technological impediments to increasing the supply of technology metals. And the stock market is woefully ignorant of the economic obstacles—from lack of mine profitability to increasing the production of almost any metal other than iron.

You may note from the previous chart that no tantalum was produced in 2009 even though tantalum is a critical technology metal for all electronics. This was an issue of economics and politics largely ignored by the world's stock markets.

The world's largest producer, Australia's Talison Tantalum (private company), shut down production in late 2008 because the selling price for its mine concentrates was below its costs. Unethical trading companies covered the shortfalls—demand in excess of inventory—by procuring tantalum ore concentrates from places like the Democratic Republic of the Congo where illegal mining using child, and even slave, labor is rampant. Such ores were 'baptized' as being of ethical origin or disguised as previous inventory to circumvent UN, U.S., European and Chinese laws against the use of materials of such heinous origin.

The total volume of the tantalum trade worldwide is tiny compared to any base metal, such as iron, aluminum, copper, zinc or lead; so markets have generally ignored this issue, but I think it is a major issue. There is a good opportunity here for investing in North American domestic junior tantalum opportunities, such as Commerce Resources Corp. (TSX.V:CCE; Fkft:D7H; PK SHEETS:CMRZF), because the American government is realizing that the only way to ensure the survival of its high-tech industry is to ensure there is a domestic natural-resources supply chain that begins in every instance at the mine. I use tantalum as an example to emphasize that rare earths aren't the only technology metals for which self-sufficiency is important.

Alternate energies for a green future are impossible to build and operate without rare metals. These include cadmium, tellurium, selenium, indium, gallium and germanium for solar; rare earths for wind power and electric cars; and uranium and thorium for nuclear generation of electricity.

Looking at the chart, you can see the total amounts of most of these critical technology metals are small, and some are even so small they're unknown. We need to listen carefully to those miners who tell us they can produce any or all of the technology metals for us domestically (or under the control of friendly nations). Otherwise, the age of technology will stall or go into decline—and the green world will not come about.

TGR: Could you explain to our readers the difference between heavy and light rare earth elements (REEs)?

JL: The rare earth elements, known chemically as the lanthanides, are defined simply as those chemical elements beginning at number 57, lanthanum, on the periodic table, and running consecutively through, and including, number 71, lutetium. The atomic numbers 57–71 are the measurement by which true chemical elements are differentiated from each other. Technically, these numbers represent the quantity of electric charge of the nucleus of each atom; and this number dictates the chemical properties the atom will have.

The rare earths are called "rare" for the historical reason that their chemical properties are so similar, they could not be completely separated and identified individually until the 20th century's rapid growth of chemical separation and identification technology. The commercial separation of the rare earths into individual, high-purity metals is still an expensive, and not always successful, undertaking. In fact, this separation and purification on a commercial basis is the great impediment to increasing rare earth production even today.

Such chemical operations are very expensive and time-consuming, so they restrict new entrants into the field to the well-financed, highly skilled. . .and those lucky enough to have an ore body (always a mixture of ores each with its own problems of concentration and extraction) that can be processed successfully on an economic basis.

All rare earth ores contain all of the rare earths, but in varying proportions. If the contained rare earths are primarily those with an atomic number at or below that of samarium, number 62, the ores are traditionally said to be those of the "light rare earths."

The rare earths known traditionally as the "heavy rare earths" begin with europium, number 63, so anything at or above 63 is considered a heavy REE. Although the "heavies" are found in some proportion in all rare earth deposits, those ores with a significant proportion of the heavies, which are still very small numbers, are known as "heavy rare earth deposits." This confusing terminology has now become fixed in stock-market talk.

Why is this important? Because the most important of all the rare earths are the magnet metals—the big four: neodymium and praseodymium (light REEs) and dysprosium and terbium (heavy REEs). These four metals, in varying proportions, make up the critical materials in 90% of rare earth permanent magnets made and used today. And these will continue to be critical to manufacture the rapidly increasing number of permanent magnets required by today's and tomorrow's technologies.

There is one other magnet metal of somewhat lesser importance—samarium; but, today it is used mostly in military applications or those requiring magnets capable of operating under extreme environmental conditions of radiation or temperature.

Lanthanum is critical for nickel metal hydride-storage batteries, which is the type of storage battery used universally for hybrid vehicle power trains. Lanthanum is also critical for the oil industry, as a component of fluid-cracking catalysts for modifying heavy crude into usable fractions. Some add lanthanum to their list of important rare earth metals to create a list of the rare earth "big five." I reserve judgment on whether lanthanum should be in the same category of importance as neodymium.

TGR: You mentioned earlier that most of the world's supply of these minor metals now comes from unreliable jurisdictions. Besides Commerce Resources, are there other producers or explorers in more politically safe locations?

JL: At this time, all of the rare earth metals are mined, refined and purified in Asia or Eastern Europe. More than 95% of this is done within the People's Republic of China, with the balance is done in India, Malaysia, Russia and Estonia. None of these areas is politically reliable in terms putting the needs of the U.S. or the global community on an even par with their own domestic needs.

My view is that narrow-minded politicians in the West have sacrificed our economic and military security on the altar of their own short-term needs—to be re-elected. The U.S. was self-sufficient in REEs and had a complete supply chain for them as recently as 2002. At that time, global economics made Chinese ores cheaper than those produced in the U.S.

After Molycorp Minerals, a private company in California, shut down operations for economic reasons (i.e., inability to compete with low-priced Chinese supply), the rest of the supply chain—purification, metal and alloy production and magnet and battery production—simply moved to China for access to supplies of the rare earths.

Besides the huge deposit of high-grade light rare earth ore (with some europium) at Mountain Pass, North America also has significant REE deposits in Alaska, Idaho, Wyoming and Canada's Northwest Territories, Saskatchewan and Quebec. The Canadian deposits and those in Alaska contain very significant quantities of the heavy REEs.

North America could be completely independent of China—and could, in fact, be a supplier to China—if just a few of North America's deposits were developed.

TGR: A number of companies appear to be popping up that suddenly have REE deposits. Can you share with our readers some of your favorite REE names with real mineable assets?

JL: I'd be glad to list those companies with mineable deposits in North America, so long as you understand that a mineable deposit is just one of the requirements for a successful REE-mining business. It is a necessary, but insufficient, requirement.

The mineable deposits of rare earths in North America are owned by:

- Molycorp Minerals (private company in Mountain Pass, California)

- Avalon Rare Metals Inc. (TSX:AVL;OTCQX:AVARF) (NW Territories, Canada)

- Rare Element Resources Ltd. (TSX.V:RES) (Wyoming)

- U.S. Rare Earths (a private company in Idaho)

- Quest Rare Minerals Ltd. (TSX.V:QRM) (Quebec, Canada)

- Great Western Minerals Group Ltd. (TSX.V:GWG) (Saskatchewan, Nova Scotia)

- Ucore Uranium (TSX.V:UCU) (Alaska)

In order for the U.S. to be self-sufficient and become a net exporter of REEs, some of the above-listed companies must be developed now. Other countries, domestically, and China and Japan, globally, are racing to acquire and develop REE resources outside of North America. It is a global competition, and the other entrants are already well under way.

TGR: Do you see demand for these REEs expanding dramatically in the future?

JL: Demand for rare earths, and particularly for the big-four magnet metals, is growing at a rate that is unsustainable unless new heavy REE production is brought online in the next five years at the most. Due to the nature of REE deposits, this requires that the production of light REEs increase significantly also. Therefore, I believe there is now a window of opportunity for one or two light REE producers and several heavy REE producers to enter the market over the next five years. Anyone whose timeline is beyond that will not likely be successful in this run up of rare earth demand.

TGR: This has been a real education, Jack. Thanks so much for your time today.

Jack Lifton is an independent consultant and commentator, focusing on market fundamentals and future end-use trends of the rare metals. He specializes in sourcing nonferrous strategic metals and due diligence studies of businesses in that space. Jack's work includes exploration and mining, and the recovery of metal values by the recycling of not only metals and their alloys but also metal-based chemicals used as raw materials for component manufacturing.

Jack has more than 47 years of experience in the global OEM automotive, heavy equipment, electrical and electronic, mining, smelting and refining industries. His background includes sourcing, manufacturing and sales of platinum group metal products, rare earth compounds and ceramic specialties used to make catalytic converters, oxygen sensors, batteries and fuel cells. Jack is knowledgeable in locating and analyzing new and recycled supplies of 'minor metals,' including tellurium, selenium, indium, gallium, silicon, germanium, molybdenum, tungsten, manganese, chromium and the rare earth metals.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

DISCLOSURE:

1) Gold Report Publisher Karen Roche personally and/or her family own the following shares of companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Great Panther Silver, Timmins and First Majestic.

3) Sean Brodrick: I personally and/or my family own shares of the following companies mentioned in this interview: None. I personally and/or my family are paid by the following companies: None.

The GOLD Report is Copyright © 2010 by Streetwise Inc. All rights are reserved. Streetwise Inc. hereby grants an unrestricted license to use or disseminate this copyrighted material only in whole (and always including this disclaimer), but never in part. The GOLD Report does not render investment advice and does not endorse or recommend the business, products, services or securities of any company mentioned in this report. From time to time, Streetwise Inc. directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.