U.S. Economic Recovery is Strengthening the Global Economy Against Europe’s Debt Turmoil

Economics / Economic Recovery May 17, 2010 - 06:03 AM GMTBy: Money_Morning

Jon D. Markman writes: Stocks scattered across the capital markets last week like the unwanted children of a terrible divorce, as a blunted rally following a global margin call put a hex on every sector and most commodities - but a U.S. recovery marched on.

Jon D. Markman writes: Stocks scattered across the capital markets last week like the unwanted children of a terrible divorce, as a blunted rally following a global margin call put a hex on every sector and most commodities - but a U.S. recovery marched on.

So far in the ten sessions of May, the Dow Jones Industrial Average is down 3.6%, the Nasdaq 100 is -4.7%, the S&P SmallCap 600 is -3.1% and overseas large-caps are down 8.6%.

That's a whole lot of falling, and for what reason? The headlines tell us that investors freaked out over Greek debt, fear of a contagion effect on Spain, speculation that U.S. earnings have peaked, and worry that the great global capital machine will soon seize up for lack of customers and credit.

But headlines don't always tell the whole story.

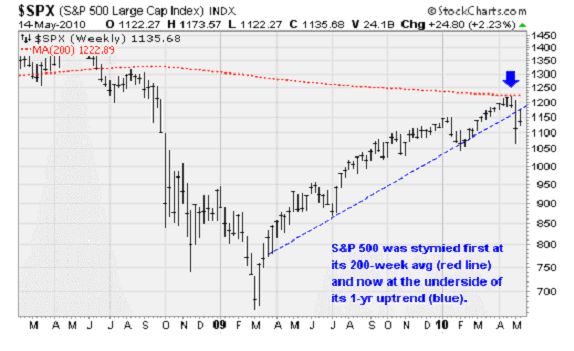

Yet as you can see in the chart above, it is no accident that the advance out of March 2009 halted where it did in late April: It banged right into its 200-week average, which also stymied the benchmark index back in August 2008 before it fell disastrously over the next few months. Then after a brief but furious rally early in the week, the index was thrown back after touching the underside of its one-year uptrend. Not good.

The fact that this decline has occurred against the backdrop of an improving economic and corporate growth recovery is puzzling to many. Perhaps it shouldn't be. Stocks became overbought in April after a fantastic run higher, and traders were ready for an excuse to sell. The selling got out of hand on Thursday -- sort of like a car that almost runs into a ditch but careens back into the road at the last minute -- but it really wasn't because of some brand new discovery by smart equity or credit managers.

There was absolutely nothing in the European, Greek, Asian or U.S. news stream that was any different on Tuesday, Wednesday or Thursday than had been known for weeks and months. So any relationship of the drop last week with news events was almost purely coincidental.

The only element that was new as the Europeans' decision last weekend to cobble together a $1 trillion pile of new debt -- actually mostly guarantees and promises -- to troubled Eurozone countries in coming months. And the European Central Bank said it will purchase bonds to ease the pain of the credit crisis that has flashed across the continent in the past month.

Previous similar announcements have proven to be nonsense, and riots in Greece have shown that people of these countries may not want to make the sacrifices that the loan guarantees would demand. But it looks to me as if the current EU/IMF plan is fundamentally different as it appears to show that Eurozone leaders are desperately trying to create mechanisms of true government-like strength for the euro currency alliance that has been lacking for the past decade.

If the Eurozone is willing to sell bonds and finance these loans itself -- printing money as if it was a real government rather than just a loose band of currency policy elite -- then we will have witnessed a big new step in the history of the unification of Europe. And that will be a very big deal in global capital markets and world history.

If this comes to pass, it would be the sort of development that calls to mind the phrase popularized by Rahm Emanuel of the Obama administration: "Never let a good crisis go to waste." The European currency elite has been wanting to create their own bond-issuance and guarantee facilities for years, and the recent decline appears to have given them their chance. This will create a lot of turmoil in the short run (weeks) but should be stabilizing in the long run (years).

Jobs, Jobs, Jobs

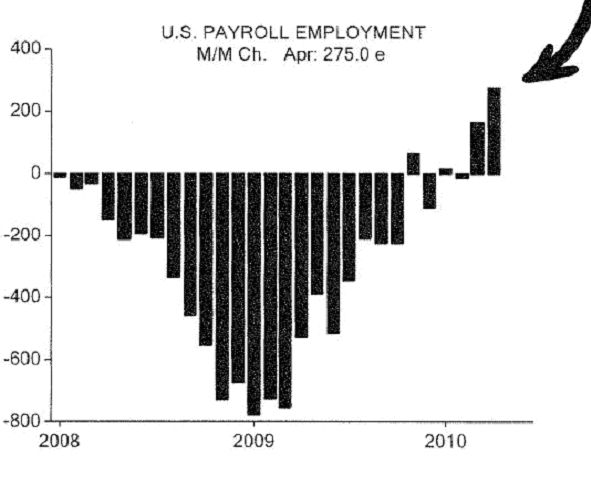

The good news for the economy started on the first Friday of May after the government reported a much better-than-expected jump in payrolls for April: The United States added 290,000 jobs when consensus was expecting 190,000 as private employers ramped up hiring. March payrolls were also revised to the upside for a gain of 230,000 versus the previously reported 162,000 rise.

The gains were broad-based. In other words, it wasn't all government hiring related to the 2010 Census. Overall, the private sector added 231,000 positions. Manufacturers was particularly strong: It added 44,000 jobs in what was the third-best monthly gain in percentage terms since 1984.

The unemployment rate did increase slightly, from 9.7% to 9.9%, but it happened for a good reason. Discouraged laborers are returning to the workforce. Those classed as not in the labor force fell by 635,000. In the words of Philippa Dunne of the Liscio Report, "Clearly the gloom is lifting among the working and want-to-be working population."

This was fantastic news. It shows that the economic recovery that started last summer has finally started to generate new jobs over the last few months. Looking back, this was the best month of job creation since March 2006. So much for the jobless recovery.

The team at Capital Economics Ltd. in London chimed in on the results in a note to clients. In their words the payroll report "is a strong signal that the economic recovery is becoming self-sustaining." In short, "it could well be a game changer."

So, what's next? Deutsche Bank AG (NYSE: DB) economists led by Joseph LaVorgna believe the focus will now turn to initial weekly jobless claims -- which remain troublingly high near 444,000. LaVorgna notes that the 400k level on claims has "been the critical threshold for sustained payroll gains." So now, we will need to see how quickly claims fall under 400k as the next measure of job market health.

In his words: "Assuming that stock gyrations and sovereign risk developments do not derail economic confidence in the coming weeks -- which could be a bold assumption given the intra-day move in US equities yesterday -- the economic fundamentals (including slowing productivity growth, large non-financial corporate cash holdings and accommodative monetary policy) support continued acceleration in hiring."

This is the opposite of the tone during the worst of the recession and bear market. Stocks can still go down in the face of rising employment, but it will be much harder for sellers to get much traction.

More Optimism On the Economy

Two years ago when the market was falling apart, sales and earnings at large companies were crumbling. Now we're looking at an 18.6% annualized increase in sales over the last three quarters, which is a big number.

This recovery is led by technology companies in some ways. Real technology equipment capital expenditures in the first quarter were up 13.8% year-over-year. ISI Group reports their survey of tech company executives' optimism for near-term sales is near the highest in ten years. That's supported by the national manufacturing Purchasing Managers' Index, which is at its highest level in 16 years.

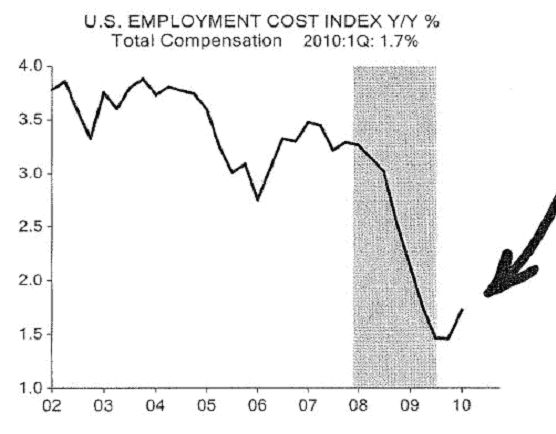

I keep harping on the fact that the recovery is broad-based because it's important. ISI points out that their surveys of retailers, airlines, credit card companies, truckers, restaurants, tech and temp agencies' optimism and results are all still increasing. As the battle to acquire more employees has accelerated in recent months, so has wages, as you can see in the U.S. Employment Cost Index, a proxy for wage growth, above.

This is why nominal gross domestic product (GDP) moved above its 2008 peak in the first quarter, which means the economy has ended its "recovery" phase and entered a real expansion. I've mentioned this before but I'll say it again: It took 15 years in the 1930s for real GDP to make a new high after its sharp downshift, and it was around the same for Japan in the 1990s and early 2000s. But for the recent recovery it has occurred in less than two years -- a remarkable achievement, whether from government stimulus or not.

As a result, corporate profits will make a new high in the third quarter. So the first quarter results just concluded are very unlikely to be the peak of the cycle, as the bears would have you believe.

ISI analysts thus suggest it's time to stop talking about the shape of the recovery, i.e. U-shaped, L-shaped, V-shaped or W-shaped, because it's already behind us. Now we are looking at an expansion, and the average one has lasted five years.

Some of the companies that have announced hiring plans in the past week alone are Caterpillar Inc. (NYSE: CAT), General Motors Co. and Whirlpool, while other companies like Tyco International Ltd. (NYSE: TYC), DuPont (NYSE: DD), 3M Company (NYSE: MMM) and Cummins Inc. (NYSE: CMI) reported stronger than expected sales and upbeat outlooks.

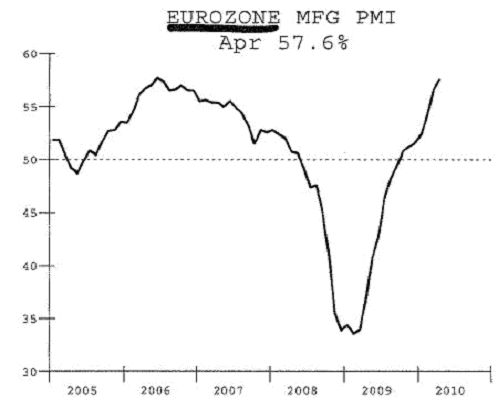

Meanwhile, we're seeing the same overseas. China may be tightening, but its companies' sales are surging. Elsewhere, Korean GDP in the first quarter was 7.8% year-over-year, while Hong Kong imports are up 38.5% annualized and German machinery orders are up 21% this year -- a fact that will be helped by the recent plunge in the euro. As you can see in the chart above, the manufacturers' Purchasing Managers' Index has surged in recent weeks despite the Greek debt fears.

In short, the global economy is probably healthy enough to resist much of the predations of European credit weakness unless the continent's leaders really blow their chance. My expectation is that the recent declines will actually boomerang on credit bears and increase the institutions' appetite for bonds and equities.

Week in Review

Monday: No major economic releases. However, over the weekend Federal Reserve chairman gave a commencement address at the University of South Carolina in which he outlined part of his philosophy of life. It was pretty deep stuff. An excerpt:

"But even though GDP or income should not be the only goal of our strivings, we can go one step further and recognize as well that happiness itself, at least to the extent that the term is associated with immediate rather than long-lasting feelings and emotions, should not be our only goal either. Remember that I began by distinguishing between happiness and life satisfaction. Happiness is just one component of the broader, longer-term concept of life satisfaction, and only one indicator of how the fabric of our lives is being shaped by our choices and circumstances."

Tuesday: Same-store sales date from the International Council of Shopping Centers indicated strong retail traffic over the Mother's Day holiday.

Wednesday: The March trade deficit widened less than expected (which is a good thing for GDP growth) despite big increases to both the price and quantity of energy imports. Exports increased especially industrial supplies and consumer goods.

Thursday: Initial weekly jobless claims remain troublingly elevated, but showed some improvement last week. The four-week average dropped 9,000 to 450,500 -- the lowest level since late March and the second best level of the recovery thus far.

Friday: A batch of solid economic reports. Retail sales increased 0.4% in April, building on March's awesome 2.1% surge. On an annual basis, retail sales are now up nearly 9% over the same period last year. Industrial production increased 0.8% in April, beating the consensus estimate of 0.6%. And consumer sentiment continued to climb. With all the troubles in Europe, it's easy to forget that a powerful economic expansion is currently underway.

The Week Ahead

Monday: We'll get an update on the manufacturing sector form the Empire State Manufacturing Survey.

Tuesday: An update on housing starts and an update on inflation when the latest Producer Price Index numbers are reported.

Wednesday: The Federal Reserve concludes its policy meeting. Also, another read on inflation as the Consumer Price Index is reported.

Thursday: Initial weekly jobless claims and the latest data on the economic leading indicators will be released.

Friday: No economic releases.

[Editor's Note: Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today's markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what's been the toughest market for investors since the Great Depression, it's time to sweep away the uncertainty and eradicate the worry. That's why investors subscribe to Markman's Strategic Advantage newsletter every week: He can see opportunity when other investors are blinded by worry.

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.]

Source : http://moneymorning.com/2010/05/17/u.s.-recovery-2/

Money Morning/The Money Map Report

©2010 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or 72 hours after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.