Greek Debt Wildfire Engulfs the Euro in Flames, Boosts Gold

Interest-Rates / Global Debt Crisis May 13, 2010 - 11:08 AM GMTBy: Gary_Dorsch

It takes a lot more time to safely extinguish a fire than it does to start it. There’s an important lesson to be learned from a sad story of a homeowner, who had been burning debris in the backyard of her home, and thought she had put the fire out. She later found out the fire had spread and was burning grass underneath her deck porch, which soon engulfed her two-story brick frame home in flames.

It takes a lot more time to safely extinguish a fire than it does to start it. There’s an important lesson to be learned from a sad story of a homeowner, who had been burning debris in the backyard of her home, and thought she had put the fire out. She later found out the fire had spread and was burning grass underneath her deck porch, which soon engulfed her two-story brick frame home in flames.

The woman tried to put the fire out and called her 14-year-old son to help. Unable to extinguish the blaze, the woman finally called 911 for help. However, by the time fire officials arrived, the fire had burned most of the backyard and the home was fully engulfed in flames. The incident is a reminder of the importance of calling authorities early when fires occur, instead of trying to put them out your-self.

“If we had gotten there early on, we could have gotten the fire taken care of. You can’t dilly-dally. It was an unfortunate situation,” the Fire Department explained. Similarly, a brushfire fire that starts in a dry area can quickly turn into a wildfire, spreading out from its original source at rapid speed, and bring about devastating conflagrations, if not contained early, and extinguished. While some fires are caused by natural factors, the biggest causes are man-made.

For most of this year, traders’ radar screens have been focused on the raging wildfire engulfing the Greek bond market, which became the flashpoint for unleashing a replay of a worldwide, Lehman Brothers style meltdown. The wildfire in the Greek bond market was ready to blaze widespread destruction throughout the European banking system, and is still engulfing the Euro currency in flames.

For most of this year, traders’ radar screens have been focused on the raging wildfire engulfing the Greek bond market, which became the flashpoint for unleashing a replay of a worldwide, Lehman Brothers style meltdown. The wildfire in the Greek bond market was ready to blaze widespread destruction throughout the European banking system, and is still engulfing the Euro currency in flames.

Over the past several months, Euro zone politicians underestimated the destructive power of the tiny tinderbox – the Greek bond market, with Athens’ ability to redeem bondholders, including major European and US banks, growing increasingly in doubt. Token bailout packages were grudgingly offered by French and German politicians, but weren’t sufficient in quantity to put out the flames. Instead, while Bonn and Paris fiddled over the details of the wage cuts and tax hikes for Greece’s 11-million citizens, - the streets of Athens were burning in rage.

When the wildfire in the Greek bond market began to wreck havoc on the Portuguese and Spanish markets, EU politicians hastily arranged an emergency meeting, to devise a rescue from the brink of Armageddon. “In the night, when the markets are opening, we cannot afford a disappointment,” said Finance Minister Anders Borg of Sweden. “We now see herd behavior in the markets that are really wolf-pack behavior. If we will not stop these wolf-packs, even if it is self-inflicted weakness, they will tear the weaker countries apart,” Borg warned.

“The situation in the financial markets has gone in a very bad direction, even though the Greek situation was brought under control,” added Finnish Finance chief Jyrki Katainen. Facing a most desperate situation, - a systemic seizure of the European financial system, - the ECB “crossed the Rubicon,” and unleashed its nuclear option, – “Quantitative Easing,” (QE), printing vast quantities of Euros to douse the fire. The EU put up a staggering 750-billion Euros in loan guarantees to contain its spreading.

Origin of Greek debt Crisis,

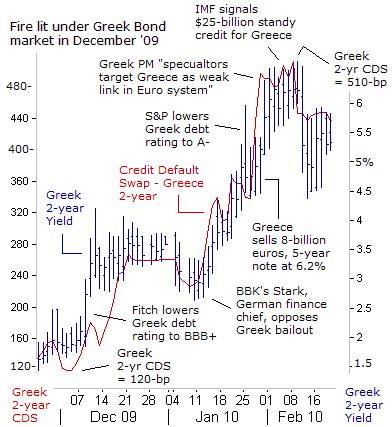

Quite often, major forest fires begin with a careless throw of a cigarette. There was a trail of smoke rising from the Greek credit default swap (CDS) market in December 2009, - and where there is smoke, there is fire. The interest rate spread between Greek and German 10-year bond widened by 200-basis points, yet Euro-zone politicians and ECB central bankers didn’t sound the alarms. But this brushfire would eventually morph into a raging wildfire, wiping out $3.7-trillion of global stocks markets in a three-day plunge. The most notable fallout was a 1,000-point intra-day meltdown in the Dow Jones Industrials on May 6th.

The first fire-alarm bells began to ring in early December, when Fitch, a credit-rating agency, downgraded its rating of Greece’s bonds from A to BBB+. As a consequence, the interest rate that Athens was forced to pay for two-year notes, jumped 200-basis points to 3.50-percent. The situation worsened when Greek Prime Minister George Papandreou admitted that the previous administration had understated the figures on its budget deficits. Papandreou revealed that Greece’s debt had mushroomed to €300-billion, or 115% of the size of its annual economic output.

There was very little appetite in the wealthier Euro-zone nations to bailout Greece, which is famous for a political system rife with fraud and corruption, in which top officials routinely dole-out public money to special interests, engage in tax dodging, and are protected by laws shielding them against prosecution. “Greece’s problems are entirely home-made and do not meet the terms required to trigger the rescue mechanism under EU treaty law,” warned Jurgen Stark, the ECB’s chief economist and a member of the Bundesbank’s inner council.

“The Treaties set out a no bail-out clause, and the rules will be respected. This is crucial for guaranteeing the future of a monetary union among sovereign states with national budgets. Markets are deluding themselves if they think that other member states will at a certain point dip their hands into their wallets to save Greece,” Stark told the Italian daily Il Sole. “The country has not kept public accounts under control, nor worked to improve competitiveness,” thus, pouring more fuel on the fire.

“The Treaties set out a no bail-out clause, and the rules will be respected. This is crucial for guaranteeing the future of a monetary union among sovereign states with national budgets. Markets are deluding themselves if they think that other member states will at a certain point dip their hands into their wallets to save Greece,” Stark told the Italian daily Il Sole. “The country has not kept public accounts under control, nor worked to improve competitiveness,” thus, pouring more fuel on the fire.

On January 6th, German finance chief Wolfgang Schäuble said Greece would have to find its own “hard way out of the crisis,” distancing himself from the notion that the EU would ultimately bailout the Club-Med laggards. Volker Wissing, chair of the finance committee in the Bundestag, said it should be made clear that “Germany will not take on the burden of Greek debts.” These hard-line comments were music to the ears of raiders in the Greek CDS market, and the cost to insure $10-million of Greece’s bonds, for 2-years, doubled to $480,000 by January 28th.

Yields on Greece’s 2-year note jumped above 6%, amid growing doubts that Athens could service its heavy debt, crushing the Athens stock exchange index. “This an attack on the Euro-zone by certain other interests, political or financial, and often countries are being used as the weak link, if you like, of the Euro zone,” Greek Prime Minister George Papandreou told the World Economic Forum in Davos, Switzerland, “We are being targeted, particularly with an ulterior motive or agenda, and of course there is speculation in the world markets,” hinting at CDS speculators.

On January 30th, firefighters from the IMF tried to narrow the gap between the Greeks and the Germans, by assuring Athens that it would make available a stand-by loan facility of $25-billion. “The IMF stands ready to support Greece in any way we can,” said IMF chief John Lipsky. However, CDS traders were still probing for weak links in the Euro zone, and aiming their guns on Greece, betting it could be the next “subprime” debt bomb, referring to a situation that initially appears to be contained, but that quickly explodes into widespread destruction.

Germany’s Chancellor Angela Merkel was walking a fine-line between letting chronic budget busters such as Greece get-off easy, while making it clear that any bailout would come with stringent austerity conditions attached, in order to finesse the moral-hazard question. On Feb 9th, the leader of Germany’s Free Democratic Party, Frank Schaeffler, was more blunt, “We don’t help the alcoholic by giving him another bottle of schnapps.” Still, amid reports that Bonn and Paris were fashioning a 25-billion Euro loan package for Athens, Greek two-year yields stabilized between 4.50% and 6.50%, lending false hope that the political gambit had worked.

Germany’s Chancellor Angela Merkel was walking a fine-line between letting chronic budget busters such as Greece get-off easy, while making it clear that any bailout would come with stringent austerity conditions attached, in order to finesse the moral-hazard question. On Feb 9th, the leader of Germany’s Free Democratic Party, Frank Schaeffler, was more blunt, “We don’t help the alcoholic by giving him another bottle of schnapps.” Still, amid reports that Bonn and Paris were fashioning a 25-billion Euro loan package for Athens, Greek two-year yields stabilized between 4.50% and 6.50%, lending false hope that the political gambit had worked.

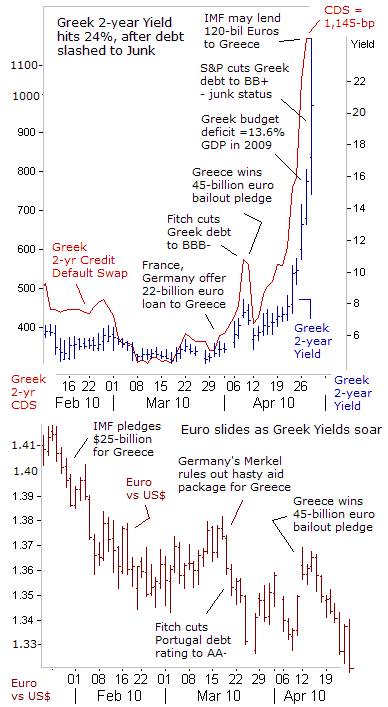

On March 17th, the Euro began a five-day slide from $1.3800 towards $1.3300, after Merkel, facing fierce voter opposition to any bailout, said any aid mechanism for Greece could only be used as a last resort, in case of imminent insolvency. On March 19th, Bundesbanker Thilo Sarrazin told the Austrian paper Salzburger Nachrichten, “We cannot possibly say right now that Greece has exploited all means to fix its budget problems over the next few years. That means that there is no need to think about aid.” Asked what Greece should do if it could not refinance its debt, “It should do what every defaulter has to do and file for insolvency,” Sarrazin replied.

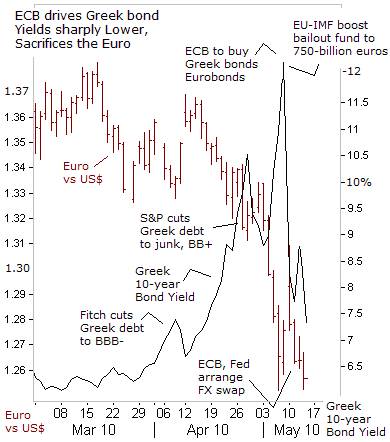

On April 9th, Fitch shaved Greece’s debt rating to BBB-, one level above junk, causing Greece’s two-year yield to jump 2% higher to 8.25%. European politicians quickly responded on April 12th, by upping the ante, and offering Athens a bigger bailout worth 45-billion Euros at below-market interest rates of 5%, in a bid to restore confidence in the Euro. But trading volume was still soaring in one of the most speculative forms of derivatives, - credit default swaps (CDS), - which played a key role in driving Lehman Brothers, Bear Stearns, and AIG into bankruptcy.

The 45-billion Euro bailout package, offered by the Euro-zone politicians, still wasn’t high enough to douse the flames in the Greek CDS market. Athens would need to raise €50-billion ($68-billion) for each of the next five-years, in order to roll over existing debt and pay interest. The rescue package would only buy a year’s worth of time and bond vigilantes weren’t impressed by short-term quick fixes.

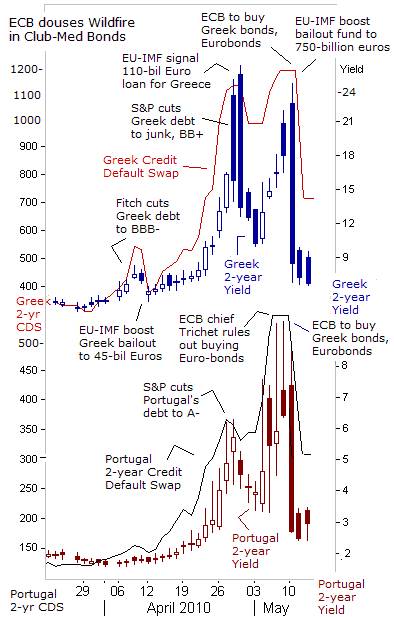

On April 27th, S&P unleashed a bombshell, pouring combustible fuel on the house of cards, by slashing Greece’s sovereign credit rating three notches to BB- or “junk” status, sending its two-year yields spiraling upwards to as high as 25.8-percent. Equally significant, S&P warned bondholders that in the event of a debt restructuring or payment default, they could only expect to recover 40% of their invested capital. This followed demands from German lawmakers that bondholders share the costs of any bailout. Contagion sales quickly hit the Portuguese bond markets, where yields on its 2-year note zoomed to as high as 6.25%, up sharply from around 1.75% a month earlier. S&P cut Portugal’s debt rating two notches to A-.

On April 28th, the EU quickly raised the ante again, saying it wouldn’t blink in its determination to bailout French and German banks holding $635-billion of Club-Med bonds. “The figure of 45-billion Euros that has been mentioned is just the first tranche of aid this year. On top of that, there will unavoidably be tens of billions of additional Euros,” Rehn told Finland’s YLE’s television news. IMF chief Dominique Strauss-Kahn said the eventual bailout would be 100-billion Euros over three years.

On April 28th, the EU quickly raised the ante again, saying it wouldn’t blink in its determination to bailout French and German banks holding $635-billion of Club-Med bonds. “The figure of 45-billion Euros that has been mentioned is just the first tranche of aid this year. On top of that, there will unavoidably be tens of billions of additional Euros,” Rehn told Finland’s YLE’s television news. IMF chief Dominique Strauss-Kahn said the eventual bailout would be 100-billion Euros over three years.

Rehn added, “It’s very important to solve the Euro-zone’s most difficult crisis as soon as possible. The most important thing is to put out this brush fire in Greece before it spreads as a forest fire to the whole Euro zone.” Upon hearing that the size of EU-IMF bailout for Greece was boosted to 110-billion Euros, the yield on Greece’s 2-year note quickly plunged from as high as 25.8%, to as low as 9.50%, within three-trading days. Yet the 2-year Greek CDS rate refused to buckle under, and stubbornly stayed above the psychological 1000-bps level. With the CDS rate refusing to budge under 1,000-bps, the yield on Greece’s two-year note did an abrupt U-turn, and soared to as high as 24.5% over the next five-days.

A coincident surge in Portugal’s 2-year yield to 9.50% on May 6th, helped trigger a stunning 1,000-point meltdown in the Dow Jones Industrials, to as low as 9,960, as computer geeks gleefully gunned sell-stops. The Euro plunged by more than 10-yen in a knee-jerk reaction to 110-yen, after 2-year Greek CDS rates soared to 1,190-bps. In a chain reaction, the soaring yen sent Japan’s Nikkei-225 stock index futures in Chicago reeling by a similar 1,000-points to as low as 9,670.

The US-Treasury’s “Plunge Protection Team,” (PPT), quickly joined the EU’s battle, purchasing huge quantities of stock index futures contracts, in order to prevent the implosion of the 13-month old “green shoots” rally. A few hours later, the Bank of Japan pumped 2-trillion yen into the Tokyo money market to weaken the yen against the Euro and US-dollar. The three-month Tokyo interbank offered rate, or Tibor, fell to 0.395% following the BOJ’s operation, hitting the lowest level since July 2006.

The BoJ’s injection of 2-trillion yen, combined with ultra-low Tibor rate, helped to propel Tokyo Gold to an all-time high of 116,500-yen /oz. Instability in sovereign bond markets in Club-Med nations, awakened the CDS vigilantes in Tokyo, where the cost of insuring $10-million of Japanese government bonds (JGB’s) from default for five years, rose to as high as $90,000 last week, from $57,000 in late March. Japan’s debt is projected to be 246% of gross domestic product in 2014, the IMF said.

EU Leaders Rescue European bankers

With the wildfire blazing through the Greek, Portuguese, and Spanish and European junk bond markets, German Chancellor Angela Merkel warned of a battle between governments and speculators. “To some degree, this is a battle between the politicians and speculators. I am firmly resolved to win this battle,” she warned.

With the wildfire blazing through the Greek, Portuguese, and Spanish and European junk bond markets, German Chancellor Angela Merkel warned of a battle between governments and speculators. “To some degree, this is a battle between the politicians and speculators. I am firmly resolved to win this battle,” she warned.

Merkel turned to ECB chief Jean “Tricky” Trichet, to deliver a knock-out blow to the CDS speculators, and extinguish the fires ravaging the Club-Med bond markets, and prop-up the Euro currency. “Tricky” Trichet set a trap for the CDS vigilantes, saying on May 6th, that ECB policymakers didn’t even discuss the idea of buying Club-Med bonds at their Lisbon meeting, despite intense market speculation. Within minutes, CDS rates on Greek, Portuguese, and Euro-zone Junk bonds soared.

Then on May 10th, “Tricky” Trichet made a radical U-turn, and bludgeoned the CDS vigilantes, by revealing a backroom deal with EU finance ministers, central bankers and the IMF, - saying Euro-zone central banks would indeed buy Club-Med bonds in the open market. The “shock and awe” triggered a massive plunge in Greek and Portuguese bond yields and drove CDS rates sharply lower. For their part, the Euro-zone politicians and the IMF upped the bailout fund to a staggering 750-billion Euros, including loan guarantees to be tapped by highly indebted Euro-zone governments shut-out of credit markets. Senior IMF official Marek Belka said the emergency package was “morphine for the markets.”

Like other bailouts before it, this package promises a gigantic transfer of public funds to the European Oligarchic banks. The biggest winners were major banks in Spain, France, and Italy. Banco Santander, BBVA, Société Générale, BNP Paribas, and Unicredit all saw increases of 20% or more in their stock price. Like the $750-billion TARP bailout fund, this money is being handed over to the European Oligarchic banks with no strings attached. Teetering on the edge of default, the banks holding €650-billion of Club-Med government bonds averted catastrophe again, with €550-billion in funding from European governments, and €200-billion from the IMF.

However, EU countries with AAA credit ratings, such as Germany, the Netherlands, or France, would have to borrow hundreds of billions of Euros to fund the bailout, thereby undermining their own creditworthiness. Thus, the next phase of the global debt crisis could be an exodus from AAA-rated sovereign bonds. As for Greece, - higher taxes, fewer welfare benefits, 10% salary cuts and no bonuses for public workers could provoke a catastrophic collapse of its economy.

However, EU countries with AAA credit ratings, such as Germany, the Netherlands, or France, would have to borrow hundreds of billions of Euros to fund the bailout, thereby undermining their own creditworthiness. Thus, the next phase of the global debt crisis could be an exodus from AAA-rated sovereign bonds. As for Greece, - higher taxes, fewer welfare benefits, 10% salary cuts and no bonuses for public workers could provoke a catastrophic collapse of its economy.

The foundation of the Euro rests on the “Stability and Growth Pact” adopted in 1997, by which the signatory countries agreed to enforce strict fiscal policies, including limiting budget deficits to 3% of GDP and public debt to 60% of GDP. But today, only three of the 16 Euro-zone countries are in compliance, casting doubt over the viability single currency experiment. Greece is the worst offender, with a budget deficit of 14% of GDP and total debt equalling 115% of GDP.

The wildfires blazing in the bond markets of Greece, Portugal, and Spain, drove the Euro down sharply to the $1.25-level. ECB chief “Tricky” Trichet came out fighting on its behalf, “I am more than confident than ever in the future of the Euro,” he told France’s radio one on May 11th. However, by shifting to the radical QE-scheme, Trichet has irrevocably tarnished the ECB’s anti-inflation credentials, and set in motion, the eventual disintegration of the Euro.

The ECB won’t reveal the size of its bond-buying spree, because “the information could assist speculators.” However, such secrecy fuels suspicions that the scope of the Euro printing operation is going to be enormous. Speaking to German radio station Deutschlandfunk, Bundesbank hardliner Juergen Stark said the “ECB would hold the Club-Med bonds, until the end of their maturity,” indicating that the massive injections of Euros would be very long-term.

Trichet also denied suggestions that the ECB has adopted the monetary strategy of Zimbabwe. “We have not changed our monetary policy. All liquidity which being put in through these interventions will be taken back. We are not running money printing presses.” But alas, Trichet has already dumped the Euro experiment into the trash heap of history. The only defense for the Euro is a foreign currency swap arrangement with the US Federal Reserve, which can increase the supply of US-dollars in the short-term, and help the ECB to engineer an orderly devaluation of the Euro, and reduce the risk of a frightful free-fall.

“Tricky” Trichet is a crafty poker player. But while he’s rescued the French and German banks, he’s stripped the Euro of its reserve currency allure. “We will mop up this extra liquidity again. We’ve done this in the past,” he said, spewing worthless propaganda about sterilization. As part of its war on the bond vigilantes, the ECB is lending of unlimited amounts of Euros to the banking Oligarchs, at borrowing rates of 1%, encouraging them to buy Euro-zone government bonds – ie backdoor QE. However, central bankers holding roughly $2-trillion worth of Euros in their FX reserves can see through the smoke and mirrors, and they’re nervous.

“Tricky” Trichet is a crafty poker player. But while he’s rescued the French and German banks, he’s stripped the Euro of its reserve currency allure. “We will mop up this extra liquidity again. We’ve done this in the past,” he said, spewing worthless propaganda about sterilization. As part of its war on the bond vigilantes, the ECB is lending of unlimited amounts of Euros to the banking Oligarchs, at borrowing rates of 1%, encouraging them to buy Euro-zone government bonds – ie backdoor QE. However, central bankers holding roughly $2-trillion worth of Euros in their FX reserves can see through the smoke and mirrors, and they’re nervous.

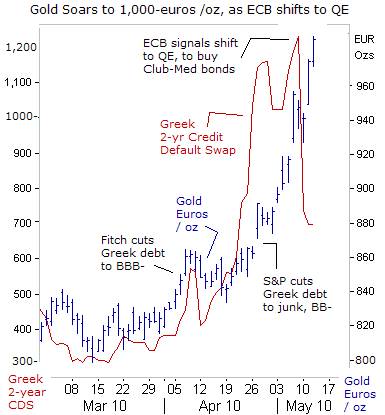

Already, a massive flight for safety from the Euro and into the king of currencies - Gold is underway. Gold has soared in parabolic fashion, up 20% from a month ago, zeroing in on the psychological 1,000-Euro /oz level. After parabolic rallies, gold becomes subject to minor bouts of profit-taking. However, it’s increasingly obvious that all paper currencies are at risk of collapse compared with Gold, due to the extreme abuses of central bankers worldwide.

“What the ECB is doing is a 180-degree about-face,” declared Eurosceptic economist Joachim Starbatty on May 12th, noting Greek bonds were already rated at junk level by ratings agency S&P. “If a central bank buys bonds that international ratings agencies have declared are junk, then it should not be surprised that the Euros it produces are quickly seen as junk as well,” he said. Starbatty said the ECB is “rewarding speculators who are betting on higher inflation.”

The ECB’s shift to “nuclear-QE” is expected to usher in a steady devaluation of the Euro. Already, the German economy is getting a significant boost from the weaker Euro, with its exports surging 10.7% in March to 79.0-billion Euros, the biggest monthly increase since July 1992. Germany earned a trade surplus with the rest of the world of 13.3-billion Euros, and business morale is at its highest in two years. Expectations of a weaker Euro ignited a powerful 500-point rebound in the German DAX Index this week, recouping nearly all of its losses from the Greek wildfire.

However, when measured in “hard money” terms, - compared to the price of Gold, the German DAX’s rebound is simply a monetary illusion, - 1 DAX share fetches 6.4-ounces of gold today, or 13.5% less than a month ago. The ECB’s money printing operation has essentially inflated the German DAX by 500-points. However, a weaker Euro would also increase the cost of raw material imports, and erode the profit margins of DAX exporters over time. ThyssenKrupp, Germany’s biggest steelmaker, said prices for iron ore and coking coal are expected to rise sharply. “The enormous price increases will place significant burdens on the steel industry and its customers, for example, in the automotive and engineering sectors,” it warned.

The ECB is now actively engaged in rigging the stock markets, ready to massively increase the money supply, (QE), at the sight of a significant meltdown in the equity markets. In this regard, stock market indexes are utilized by many European traders as a hedge against monetary inflation and the Euro’s devaluation. However, there is no substitute for the real thing, when operating under a de-facto Gold standard.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2010 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.