Credit Default Swaps Threaten the Whole System, Real Financial Form Needed

Stock-Markets / Credit Crisis 2010 Apr 10, 2010 - 03:54 AM GMTBy: John_Mauldin

It's Time for Reform We Can Believe In

It's Time for Reform We Can Believe In

The Fed Must Be Independent

Credit Default Swaps Threaten the System

Too Big To Fail Must Go

And This Thing About Leverage

What Happens If We Do Nothing?

Casey Stengel, manager of the hapless 1962 New York Mets, once famously asked, after an especially dismal outing, "Can't anybody here play this game?" This week I ask, after months of worse than no progress, "Can't anybody here even spell financial reform, let alone get it done?"

We are in danger of experiencing another credit crisis, but one that could be even worse, as the tools to fight it may be lacking when we need them. With attacks on the independence of the Fed, no regulation of derivatives, and allowing banks to be too big to fail, we risk a repeat of the credit crisis. The bank lobbyists are winning and it's time for those of us in the cheap seats to get outraged. (And while this letter focuses on the US and financial reform, the principles are the same in Europe and elsewhere, as I will note at the end. We are risking way too much in the name of allowing large private profits.) And with no "but first," let's jump right in.

Last Monday I had lunch with Richard Fisher, president of the Federal Reserve Bank of Dallas. Mr. Fisher is a remarkably nice guy and is very clear about where he stands on the issues. My pressing question was whether the Fed would actually accommodate the federal government if it continued to run massive deficits and turn on the printing press. Fisher was clear that such a move would be a mistake, and he thought there would be little sentiment among the various branch presidents to become the enabler of a dysfunctional Congress.

But that brought up a topic that he was quite passionate about, and that is what he sees as an attack on the independence of the Fed. There are bills in Congress that would take away or threaten the current independence of the Fed.

I recognize that the Fed is not completely independent. Even Greenspan said so this past week: "There's a presumption that the Federal Reserve's an independent agency, and it is up to a point, but we are a creature of the Congress and if ... we had said we're running into a bubble and we need to retrench, the Congress would say 'We haven't a clue what you're talking about.'"

Long-time readers know I do not have much time for Senator Chris Dodd. He has threatened the viability of the Fed by holding up appointments, actually risking the ability of the Fed to get an emergency quorum if the need arose. His current proposal to give the President the ability to appoint the president of the New York Fed is likewise a wrong-headed political power grab. He has openly proposed to have the presidents of the local districts appointed by the board of governors. These presidents are the only real check on the board.

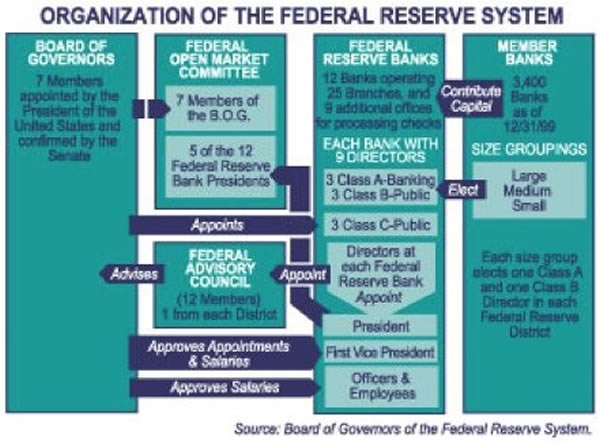

Let's do a brief recap. There are seven Federal Reserve governors, including a chairman and vice-chairman. There are twelve bank districts with independent boards that choose their districy president. The Federal Open Market Committee oversees monetary policy and is composed of the seven governors and five of the district presidents. The president of the New York district is always one of the five, and the other four are rotated among the remaining eleven.

The chart below gives you a visual graphic of how the system is organized.

Note that the seven governors are appointed by the President and must be approved by the Senate. Further, the board of governors appoints three members to each of the nine-member boards of directors of the local districts.

Dodd wants to give the President the right to appoint the president of the New York District. My response is "Not no, but hell no!" The President (from whichever party) gets to appoint a majority as it is. I prefer a small token of independence. And while the selection of a district president is of course political, it is at least now local and not national politics.

Further, when a local board narrows its choices for district president to a few candidates, it submits those choices to the national board of governors for comments, which are of course taken seriously. (There has been at least one occasion when a board submitted only one name and the governors asked for alternatives, and the local board reasserted that this was their only choice. The governors backed down.)

A Fed governor is supposed to serve for 14 years, and the terms are staggered. That way, no President gets to appoint more than a few governors and cannot stack the board in favor of certain policies. That has changed with Obama. Dodd held up two nominations by Bush for several years, and with the resignation of Vice-Chairman Kohn, President Obama now gets to appoint four governors, and he has almost three years left in his term.

About the best thing I can say about Chris Dodd is that he will not be in the Senate next year, since he is not running for re-election, which he could not win anyway.

There are other bills that would subject the presidents of the local districts to Presidential or, even worse, Congressional appointment.

Let me be clear. There are a lot of things not to like about the Federal Reserve System. I think it was Milton Friedman who said we would be better off with a computer determining monetary policy. A quote from an interview with him is instructive. When asked "Do you still think it would be a good idea to have a computer run monetary policy?" he answered:

"Yes. Of course it depends very much on how the computer is programmed. I am not saying that any computer program would do. In speaking of that, I have had in mind the idea that a computer would produce, for example, a constant rate of growth in the quantity of money as defined, let us say, by M2, something like 3% to 5% per year. There are certainly occasions in which discretionary changes in policy guided by a wise and talented manager of monetary policy would do better than the fixed rate, but they would be rare.

"Yes. Of course it depends very much on how the computer is programmed. I am not saying that any computer program would do. In speaking of that, I have had in mind the idea that a computer would produce, for example, a constant rate of growth in the quantity of money as defined, let us say, by M2, something like 3% to 5% per year. There are certainly occasions in which discretionary changes in policy guided by a wise and talented manager of monetary policy would do better than the fixed rate, but they would be rare.

"In any event, the computer program would certainly prevent any major disasters either way, any major inflation or any major depressions. One of the great defects of our kind of monetary system is that its performance depends so much on the quality of the people who are put in charge. We have seen that in the history of our own Federal Reserve System. Surely a computer would have produced far better results during the 1930s and during both world wars.

"That raises a question about the desirability of our present monetary system. It is one in which a group of unelected people have enormous power, power which can lead to a great depression or which can lead to a great inflation. Is it wise to have that power in those hands?

"An alternative would be to eliminate the Federal Reserve System; to reduce the monetary activities of the federal government to the provision of high-powered money, that is, currency and bank reserves, and to constitutionalize, as it were, what is to be done with high-powered money. My preference is simply to hold it constant and let financial developments produce the growth in the quantity of money in the form of bank deposits, a process that has been going on for many decades. But that is, of course, politically impossible."

(http://www.opinionjournal.com/extra/?id=110009561)

As much as I acknowledge how intriguing an idea the above is, in the end Friedman is right; it is politically impossible. We are stuck with this system. But what would be far, far worse is a system that was directly controlled by Congress or the President, whether Republican or Democrat. Politicians think in very short election cycles.

I do not want the same people who gave us Freddie and Fannie and now $400 billion in taxpayer losses, who pass entitlement bills that we cannot pay for, to have the power of the printing press. "Roll the dice," said Barney Frank, on Freddie and Fannie and low-income loans. How did that work out? Monetary policy is not something you roll the dice on.

Giving politicians the ability to print money has always eventually been a disaster for any nation that did so. The temptation is just too great. Down that road lies inflation (maybe hyperinflation) and currency destruction. Just as Congress had good intentions to make home ownership more attainable, the good intentions of printing money to help pay for programs that help the poor or education or whatever is just too much for politicians to resist.

If I could change the Fed system in any way, I would add four more district presidents to the FOMC, to put the majority on the Federal Open Market Committee out of the hands of political appointees. That won't happen, of course, but we all have dreams. The key here is that any attempt to politicize the Fed any more than it already is must be resisted. (That does not mean, however, that they should not be more transparent, along the lines of my friend Ron Paul's bill. Sunshine is a good thing.)

(Mark Thomas wrote a very good piece awhile back, for those who want to dig deeper on this issue. http://moneywatch.bnet.com/economic-news/blog/maximum-utility/the-dodd-proposal-to-restructure-the-federal-reserve-system-concentrates-power-and-politicizes-district-bank-governance/230/.)

Credit Default Swaps Threaten the System

We will get into banks being too big to fail in a minute, but the first problem to be dealt with is credit default swaps. What happened in the last credit crisis was that interlocking credit default swaps among so many banks made the ENTIRE system too big to fail. AIG basically sold naked options in the form of credit default swaps to all and sundry (in a unit basically created after Elliott Spitzer forced Hank Greenberg out, which allowed the unit to get out of control, yet another reason to not like Spitzer).

And nothing has changed. We again have credit default swaps (CDS) growing, and no one knows who could be overextended. Once again, everyone could be dependent on everybody else, and we have no idea if there is a Bear, Lehman, or AIG in these woods.

As I have been pounding the table about for years, we need to put CDS on an exchange. ASAP. I am not against CDS, per se. CDS are good things, just like futures. But they must go to a transparent exchange. There need to be position limits, just as there in futures and commodities. There needs to be very transparent pricing and commissions. And someone needs to monitor who owns them and what risks they are taking.

Why hasn't this been done? In a word, money. Banks make huge commissions selling CDS, as much as 2-3%, I am told. If they were on an exchange the commissions would be $10 a round turn. An enormous profit center would get blown up. So, the banks hire lobbyists to persuade Congress not to regulate CDS. Dodd's bill basically says we will deal with them later.

The good news is that there is some effort to regulate these derivatives in Congress. It should have been done a year ago, but the sooner the better. This shouldn't be all that partisan. It is common sense.

Too Big To Fail Must Go

We have large banks that take massive risks, which allow them to pay huge bonuses to management and traders; and then if they have problems the taxpayer has to take the losses. I can see why the banks like it. I don't get this business model from a taxpayer's point of view.

First, let me say that I thought, along with most of the world, that repealing Glass-Steagall was a good thing. OK, we tried that experiment and it didn't work out so well. Where is the movement to separate commercial banks from investment banks? And I must admit, Glass-Steagall is not really the problem. It is just a part of the problem. The problem is that parts of these large banks are essentially hedge funds, working with cheap commercial deposit money and putting the entire bank at risk.

I make a lot of my income helping investors find hedge funds and alternative investments. I like trading and traders, and we have a lot of client money with them. There is good money to be made there, if you are riding the right horse. But we don't put money with big investment banks, just private funds, and there is the difference. If our funds go bad, taxpayers don't bail us out.

When I put on my taxpayer hat, I don't want to be taking the risk so some big bank can have a trading desk and make large profits that only benefit their shareholders and management, and I have to pick up the pieces with my tax dollars when they fail. Separate traditional banking and investment banks. I want my commercial banks to be boring. You know, traditional lending to customers, services, that type of thing.

And This Thing About Leverage

The problem of too big to fail is ultimately one of leverage. If a small bank fails, no one really notices. If a giant bank fails and puts the system at risk, it costs us a lot. I have a simple proposal to mitigate the problem.

Why not reduce the allowable leverage the larger a bank gets? This would clearly reduce their risk and encourage them to only make prudent bets (otherwise known as loans), as their risk capital would be limited. If they wanted to make more loans, then they could raise more capital or retain more earnings. Would that hurt earnings and shareholders and limit share prices? Yes. And I don't care. If I'm not getting the dividends, then I don't want to be made to pick up the tab if there is a crisis. The world of privatizing the gains and socializing the risks must become a thing of the past.

What Happens If We Do Nothing?

What happens when we have the next credit crisis, when a major sovereign government defaults, as I think will happen? It will be a body blow to many banks, especially in Europe. Once again, we could have banks worried about lending to each other or taking letters of credit, which would be a disaster for world trade and the recovery we are now in.

That we (and Europe and Britain) have taken so long to enact real reform has the potential to really put the world at risk. In the next crisis, we will not have the tools available to stem the tide that we did the last time. Rates are already low. Do you think we could pass another TARP? The Fed's balance sheet is already bloated. It could get much worse unless we get financial reforms that have some bite.

All this debating about a consumer protection agency and where it should be and all the other trivia is wasting time. Fix the big things. Credit default swaps. Too big to fail. Leverage. Then worry about the details. And leave the Fed alone.

New York, Media and La Jolla

I wish I had time to write some more, or at least do some edits, but time is pressing. I write this letter at the Torrey Pines Lodge in La Jolla, where the weather is perfect. I am at Rob Arnott's annual Research Affiliates Conference, where for a weekend he brings in some of the best and brightest to talk about the state of the financial world. It is one conference I really look forward to every year. This year features a debate between Princeton professor Burton Malkiel and James Montier on the Efficient Market Hypothesis. They are friends, and it will be good fun to watch them spar. Paul McCulley, Prieur du Plessis, and others are here, and it will be a lot of fun!

And tonight I open a very special bottle of wine. Rob Arnott gave me a 1949 Petrus for my birthday, and I thought it right to bring it here to open with a few friends. I hope it has aged well, as I need some good portents for aging.

I will be in New York next week for a speech on Tuesday morning, then I will be on Bloomberg TV at 2 pm, and spend a whole hour with Liz Claman from 3-4 pm, which will give us time for a real discussion. I will be on Yahoo Tech Ticker Wednesday morning (and maybe Business Insider) and then will tape an interview with Steve Forbes, which will go on Forbes.com. I'll wind up with dinner with Art Cashin that night and be back home on Thursday. Oh, and I'll work in a few meetings with friends like Barry Ritholtz. Catch me if you can!

And now I need to hit the send button. The wine starts pouring in a few minutes and I feel the need for some good vino. Rob always serves the best. Have a great week. I know I have, and will.

Your passionate about the need for real reform analyst,

John Mauldin

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.