The Independence of the Fed?

Politics / Central Banks Mar 19, 2010 - 05:05 AM GMT

There is a thesis that the banks are in control of the Fed and as a result have gained control over the issuance of the currency of the United States. This thesis is based on the fact that the shares of the Federal Reserve Bank are held by these private banks. Does that mean that the private banks own the Fed?

There is a thesis that the banks are in control of the Fed and as a result have gained control over the issuance of the currency of the United States. This thesis is based on the fact that the shares of the Federal Reserve Bank are held by these private banks. Does that mean that the private banks own the Fed?

The short answer is yes, but it is a hollow ownership with very restricted rights. This ownership basically exists to give credence to the claim that the fed is independent. It is appropriately described as follows in the Fed's own publication "Federal Reserve System Purposes & Functions":

The short answer is yes, but it is a hollow ownership with very restricted rights. This ownership basically exists to give credence to the claim that the fed is independent. It is appropriately described as follows in the Fed's own publication "Federal Reserve System Purposes & Functions":

The holding of this stock, however, does not carry with it the control and financial interest conveyed to holders of common stock in for-profit organizations. It is merely a legal obligation of Federal Reserve membership, and the stock may not be sold or pledged as collateral for loans. Member banks receive a 6 percent dividend annually on their stock. (p. 12)

This is exactly the manner in which Special Purpose Vehicles (or Special Purpose Entities) are created in the corporate world. There is usually a promoter who does not wish to be seen to own an entity but who wishes to derive some benefit from the existence of such an entity. Usually, overt ownership would adversely impact the presentation of the promoter's financial reporting.

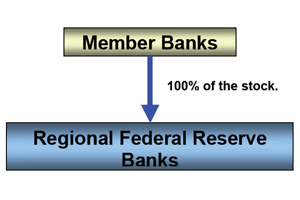

The authorities and regulators, including the Fed, are very aware of these Special Purpose structures, as is the accounting profession. Rules have been devised and implemented to assess any such arrangement in order to establish its true nature. It is therefore appropriate to assess the Fed's independence — or, alternatively, interdependence — according to the very rules that it uses to assess Special Purpose Entities. First, let's draw the simple ownership structure.

The authorities and regulators, including the Fed, are very aware of these Special Purpose structures, as is the accounting profession. Rules have been devised and implemented to assess any such arrangement in order to establish its true nature. It is therefore appropriate to assess the Fed's independence — or, alternatively, interdependence — according to the very rules that it uses to assess Special Purpose Entities. First, let's draw the simple ownership structure.

Anyone with a rudimentary knowledge of accounting principles would know that ownership of an entity without control over that entity requires further investigation. Consolidation of a group of companies can become complex when ownership and control are split. The GAAP (Generally Accepted Accounting Principles) method in this case disregards ownership and focuses on control.

For example, a right to appoint the majority of the board of directors even in the absence of ownership would trigger a consolidation of that entity. Thus the controller and the entity would be seen as part of a group and collectively as a single interdependent consolidated entity. It follows that the simple structure of the Federal Reserve Banks drawn above is a split structure, where "ownership" is of limited significance and "control" must be established. Control will tell us whether the entities are independent or interdependent.

All regulation targets "control," not just the legal form of ownership. Accounting principles of consolidation have evolved from Special Purpose Vehicles, to Special Purpose Entities, and very lately — with the revision in June 2009 for implementation in January 2010 of Financial Accounting Standard 46(R) ("FIN 46(R)") — they have evolved into the concept of a "Variable Interest Entity."

In effect, the test of whether one organization is a "Variable Interest Entity" controlled by another organization is similar to a DNA test to determine whether two people are members of the same family. FIN 46 (R) defines a "variable interest" as follows:

The enterprise with a variable interest or interests that provide the enterprise with a controlling financial interest in a variable interest entity will have both of the following characteristics:

a. The power to direct the activities of a variable interest entity that most significantly impact the entity's economic performance

b. The obligation to absorb losses of the entity that could potentially be significant to the variable interest entity or the right to receive benefits from the entity that could potentially be significant to the variable interest entity. (par. 1A)[1]

The first test is to check for "the power to direct the activities." Who exactly holds that power?

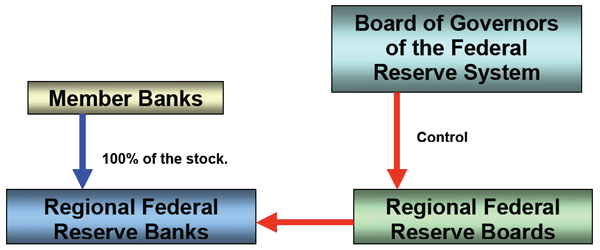

Here we turn to the Federal Reserve Act, which instructs the Regional Federal Reserve Banks to each elect their own board of directors, of which the chairman and vice chairman of the regional board will be appointed by the Board of Governors of the Federal Reserve System. The regional boards must have nine directors in three classes of three each (A, B and C directors): three A directors chosen by the stockholders; three B directors to represent the "public"; and three C directors to be appointed by the Board of Governors of the Federal Reserve System. The Board of Governors of the Federal Reserve System will appoint the chairman and vice chairman from the ranks of the three C directors.

The Board of Governors of the Federal Reserve System seems to have powers that could indicate "control," including the appointment of the power positions of chairman and vice chairman. However, we must also ask whether the regional boards have the independent powers normally associated with ownership and control, or if their powers are restricted and controlled in any manner.

The answer again lies in the Federal Reserve Act:

Said board of directors shall administer the affairs of said bank fairly and impartially and without discrimination in favor of or against any member bank or banks and may, subject to the provisions of law and the orders of the Board of Governors of the Federal Reserve System, extend to each member bank such discounts, advancements, and accommodations as may be safely and reasonably made with due regard for the claims and demands of other member banks, the maintenance of sound credit conditions, and the accommodation of commerce, industry, and agriculture. The Board of Governors of the Federal Reserve System may prescribe regulations further defining within the limitations of this Act the conditions under which discounts, advancements, and the accommodations may be extended to member banks. (section 3, par. 8)

The regional boards are limited in their ability to perform the primary functions of the Regional Federal Reserve Bank by the terms of the act and by the control of the Board of Governors of the Federal Reserve System. It is clear from the Federal Reserve Act that control does not rest in the Regional Federal Reserve Boards, nor are they independent, but they take instruction and are controlled by the Board of Governors of the Federal Reserve System.

It is now appropriate to update the simplified structure drawn above, in order to add these two steps of control.

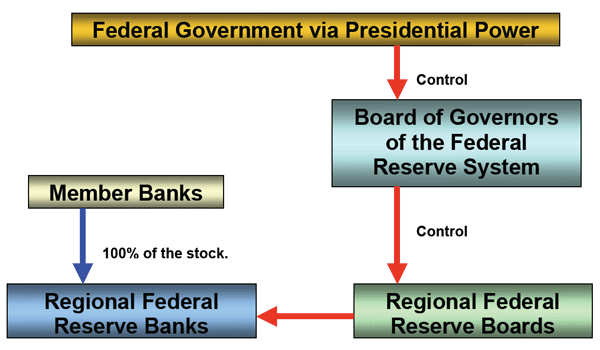

The question of who has control is not yet resolved; the nature of the Board of Governors of the Federal Reserve System must be investigated next. Is the Board of Governors of the Federal Reserve System an independent body or beholden to another entity?

The "Purposes & Functions" document describes the nature of the Board of Governors of the Federal Reserve System:

The Board of Governors of the Federal Reserve System is a federal government agency. The Board is composed of seven members, who are appointed by the President of the United States and confirmed by the U.S. Senate.

The Chairman and the Vice Chairman of the Board are also appointed by the President and confirmed by the Senate. The nominees to these posts must already be members of the Board or must be simultaneously appointed to the Board. (p. 4)

The Board of Governors of the Federal Reserve System is a federal government agency. The power to appoint its members, chairman, and vice chairman is vested in the president of the United States, with the Senate having a veto power over any appointment.

The first requirement for a "variable interest," "the power to direct the activities" is fulfilled: the federal government at the presidential level holds "the power to direct activities."

The final version of the structure of control is as follows:

The next requirement that must be met for a "variable interest" is either an "obligation to absorb losses" or a "right to receive benefits."

I would argue that the Fed's right to create currency, together with the vested interests of federal government, are more than sufficient to infer an "obligation to absorb losses." The Federal Reserve Act adds a complication to this argument by holding the shareholders responsible to the extent of their stockholding for the liabilities of the Regional Federal Reserve Banks. However, the "obligation to absorb losses" is not a requirement that needs to be met so long as the alternative, the "right to receive benefits" requirement, is met. Since the obligation is not clear cut, it is better to concentrate on the right. Note that neither the obligation nor the right need to be absolute.

Again we can turn to the two sources, the Federal Reserve Act and the Fed publication "Federal Reserve System Purposes & Functions" for guidance.

Federal Reserve Act:

Dividends and Surplus Fund of Reserve Banks

(a)

After all necessary expenses of a Federal reserve bank have been paid or provided for, the stockholders of the bank shall be entitled to receive an annual dividend of 6 percent on paid-in capital stock.

The entitlement to dividends under subparagraph (A) shall be cumulative.

That portion of net earnings of each Federal reserve bank which remains after dividend claims under subparagraph (1)(A) have been fully met shall be deposited in the surplus fund of the bank.

(b) Transfer for fiscal year 2000.

The Federal reserve banks shall transfer from the surplus funds of such banks to the Board of Governors of the Federal Reserve System for transfer to the Secretary of the Treasury for deposit in the general fund of the Treasury, a total amount of $3,752,000,000 in fiscal year 2000.

Of the total amount required to be paid by the Federal reserve banks under paragraph (1) for fiscal year 2000, the Board shall determine the amount each such bank shall pay in such fiscal year.

During fiscal year 2000, no Federal reserve bank may replenish such bank's surplus fund by the amount of any transfer by such bank under paragraph (1). (section 7)

"Federal Reserve System Purposes & Functions":

The income of the Federal Reserve System is derived primarily from the interest on U.S. government securities that it has acquired through open market operations. Other major sources of income are the interest on foreign currency investments held by the System; interest on loans to depository institutions; and fees received for services provided to depository institutions, such as check clearing, funds transfers, and automated clearinghouse operations.

After it pays its expenses, the Federal Reserve turns the rest of its earnings over to the U.S. Treasury. About 95 percent of the Reserve Banks' net earnings have been paid into the Treasury since the Federal Reserve System began operations in 1914. (Income and expenses of the Federal Reserve Banks from 1914 to the present are included in the Annual Report of the Board of Governors.) In 2003, the Federal Reserve paid approximately $22 billion to the Treasury. (p. 11)

The statement that "about 95% of the Reserve Banks' net earnings have been paid into the Treasury since the Federal Reserve System began operations in 1914" says it well enough. It is an irrefutable fact that the federal government possesses the overwhelming "right to receive benefits."

The outright, indisputable conclusion is that the Fed, when tested against GAAP as the Fed itself uses it in the Fed's assessments of those it regulates, is a Special Purpose Entity of the federal government (or, according to the latest definition, is a Variable Interest Entity of the federal government). The rules of consolidation therefore apply, and the Fed must be seen as controlled by federal government, making it indivisibly part of the federal government. The pretence of independence is no more that that, a pretence.

There is, however, no denying that the banks have tremendous vested interest in influencing the policies of the Fed, nor that the power being so narrowly vested in the president makes him a special target for influence. Still, the power to control the Fed is not in the hands of its "owners" but firmly in the hands of the federal government and the president of the United States.

Sarel Oberholster is a South African living in Johannesburg, Gauteng province. He is an economist by training, a specialist financial engineer by craft, and an inquisitive spirit by nature. He has been involved in banking for over 30 years. His quest for understanding complex economic phenomena is his muse for writing and he shares his insights on his blog. Send him mail. See Sarel Oberholster's article archives. Comment on the blog.![]()

© 2010 Copyright Ludwig von Mises - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.