Financial Markets, Economic Forecasts and Investing Strategies for 2010, What to Buy and Sell

Stock-Markets / Financial Markets 2010 Jan 18, 2010 - 05:12 PM GMTBy: John_Mauldin

This week I am really delighted to be able to give you a condensed version of Gary Shilling's latest INSIGHT newsletter for your Outside the Box. Each month I really look forward to getting Gary's latest thoughts on the economy and investing. Last year in his forecast issue he suggested 13 investment ideas, all of which were profitable by the end of the year. It is not unusual for Gary to give us over 75 charts and tables in his monthly letters along with his commentary, which makes his thinking unusually clear and accessible. Gary was among the first to point out the problems with the subprime market and predict the housing and credit crises. His track record in this decade has been quite good. I want to thank Gary and his associate Fred Rossi for allowing us to view this smaller version of his latest letter.

This week I am really delighted to be able to give you a condensed version of Gary Shilling's latest INSIGHT newsletter for your Outside the Box. Each month I really look forward to getting Gary's latest thoughts on the economy and investing. Last year in his forecast issue he suggested 13 investment ideas, all of which were profitable by the end of the year. It is not unusual for Gary to give us over 75 charts and tables in his monthly letters along with his commentary, which makes his thinking unusually clear and accessible. Gary was among the first to point out the problems with the subprime market and predict the housing and credit crises. His track record in this decade has been quite good. I want to thank Gary and his associate Fred Rossi for allowing us to view this smaller version of his latest letter.

If you are interested in his letter, his web site is down being re-designed, but you can write for more information at insight@agaryshilling.com. If you want to subscribe (for $275), you can call 888-346-7444. Tell them that you read about it in Outside the Box and you will get the full 2010 forecast with price targets, but an extra issue with his 2011 forecast (of course, that one will not come out until the end of the year. Gary is good but not that good!) I trust you are enjoying your week. And enjoy this week's Outside the Box....

If you are interested in his letter, his web site is down being re-designed, but you can write for more information at insight@agaryshilling.com. If you want to subscribe (for $275), you can call 888-346-7444. Tell them that you read about it in Outside the Box and you will get the full 2010 forecast with price targets, but an extra issue with his 2011 forecast (of course, that one will not come out until the end of the year. Gary is good but not that good!) I trust you are enjoying your week. And enjoy this week's Outside the Box....

John Mauldin, Editor

Outside the Box

2010 Investment Strategies: Six Areas To Buy, 11 Areas To Sell

(excerpted from the January 2010 edition of A. Gary Shilling's INSIGHT)

Our investment strategies for 2010 follow from our forecast of continued economic weakness and deflation, as discussed earlier in this report and in previous Insights, especially our Dec. 2009 edition. We see the 2010 investment climate dominated by weak economic growth here and abroad, led by U.S. consumer retrenchment. More government fiscal stimulus and continuing Fed policy ease are likely in this setting. So is low inflation or deflation.

INVESTMENTS TO BUY

1. Buy Treasury Bonds. Long-term Insight readers know we started recommending long Treasury bonds back in 1981 when we forecast secular and huge declines in inflation and interest rates. So we declared back then that "we're entering the bond rally of a lifetime." The yield on 30-year Treasurys was 14.7% and our eventual target was 3%. Last year, yields blew through 3% to reach 2.6% at year's end, so in our Jan. 2009 Insight we declared "mission accomplished" and removed Treasury bonds from our recommended list.

But then Treasurys sold off, pushing the yield on the 30-year bond to 4.7% at the end of 2009. So we've reactivated the strategy with our forecast of a return in yields to 3.0% or lower. Treasurys will continue to be a safe haven in a troubled world and benefit from deflation as well as their three sterling features. They are the best credits in the world. They are highly liquid. And they generally can't be called by the Treasury, and calls limit price appreciation when interest rates fall.

A decline in yields from 4.7% at present to 3.0% may not sound like much, but the bond price would appreciate over 34%. If it occurs over two years, then two years' worth of interest is collected, and the total return on the 30-year Treasury would be 44%. On a 30-year zero-coupon Treasury, which pays no interest but is issued at a discount, the total return would be about 64% -- most attractive! Recall that in 2008 when 30-year Treasurys rallied from 4.5% to 2.7%, their total return for the year was 42%..

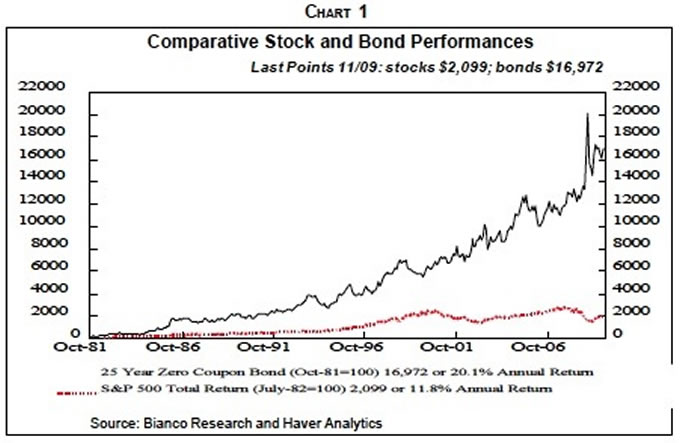

Treasury bonds way outperformed equities in the 1980s and 1990s in what was the longest and strongest stock bull market on record. The superiority of Treasurys has been even more so since then. Chart 1, our all-time favorite graph, shows the results from investing $100 in a 25-year zero-coupon Treasury bond at its yield high (and price low) in October 1981, and rolling it into another 25-year Treasury annually to maintain that 25year maturity. In November 2009, that $100 was worth $16,972 with a compound annual return of 20.1%. In contrast, $100 invested in the S&P 500 at its low in July 1982 was worth $2,099 in November for an 11.8% annual return including dividend reinvestment. So Treasurys outperformed stocks by 8.1 times!

Doubters

Many believe Treasury yields are headed up, not down. They think that all the bank reserves created by the Fed that have not generated bank loans will do so, flooding the economy with money and then create excess demand and inflation. They also think the continual heavy issuance of Treasurys to fund the nonstop federal deficits will push up yields. In contrast, we don't foresee the rapid economic growth needed to induce chastened banks to lend and cautious creditworthy borrowers to borrow. And if we're wrong, it will take at least several years to eat up global excess capacity during which the ever-inflation-wary Fed will no doubt remove the excess bank reserves, as Fed officials have already indicated.

We do expect large federal deficits for many years, in part because of pressure on government to create jobs and restrain unemployment in a slow growth economy. But those deficits will increasingly be funded by U.S. consumers as their saving spree continues. Although stock market bulls salivate over the prospect that increased saving will mean more equity purchases, we believe most of the money will continue to reduce the immense debt consumers have accumulated in recent decades.

Repaying debt will be attractive to many Americans in 2010 and beyond as they shun many investments after their huge losses in stocks throughout this decade and their shocking setbacks in real estate. A number will want to be less leveraged as slower economic growth makes employment less stable and unemployment more likely. Chastened lenders, pressed by regulators, will be pushing individuals to lower their leverage by repaying debt.

Another concern for Treasury bonds is that continued huge federal deficits and the required Treasury financing will erode confidence in these issues by Americans and foreigners, as noted earlier. This seems unlikely, especially before the end of this year. Also, as U.S. consumers save more and curb spending on domestic products and imports, the trade and current account deficits will continue to shrink.

Earlier federal deficits were financed by foreigners as they recycled back to the U.S. the dollars gained from their trade and current account surpluses. The growing U.S. current account deficit measured the increasing gap between domestic saving and investment, or, in effect, and the need for foreigners to not only finance government deficits but also make up for declining U.S. consumer saving.

But now, the current account and trade deficits are shrinking, and further declines will accrue in future years if, as we forecast, exports grow faster than imports. So foreigners will have smaller American current account deficits to finance. At the same time, much more of federal deficits will be financed by rising U.S. consumer saving.

With 3-month treasury bills yielding 0.046%, we've moved out on the yield curve for what is essentially cash positions in some cases. Sure, 5-year obligations are much more volatile than 3-month bills and do have risk of loss if interest rates rise. But we think the direction is down in that part of the interest rate curve, and 2.6% returns vs. 0.046% seem enough to offset the risks.

2. Buy Income-Producing Securities. This includes high-quality corporate and municipal bonds as well as stocks of utilities, consumer product companies, health care firms and others that pay meaningful dividends that are likely to rise. Master Limited Partnerships are also possibilities, but only if their underlying businesses are secure enough to continue significant income flows to limited partners and stockholders. Banks used to pay significant dividends but slashed them when their earnings collapsed. Nevertheless, their deleveraging and reversion to safer but less growth-oriented businesses will probably pressure them to again pay attractive dividends.

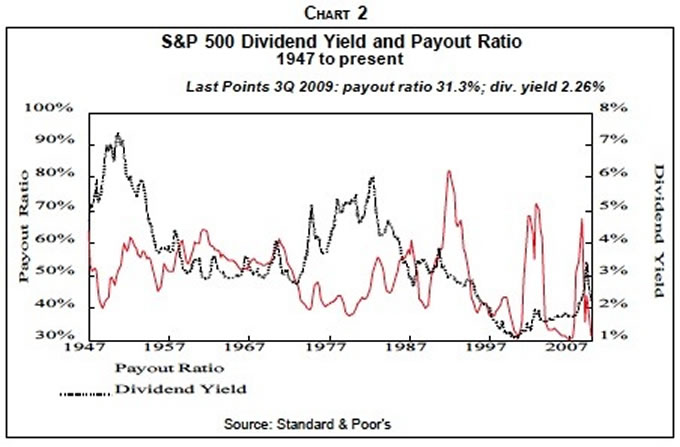

Utilities lagged behind the stock market last year, but at the end of November, the dividend yield on utilities averaged 4.5% compared to 2% for the S&P 500 index. That low return compares with 3%, which used to be the floor (Chart 2). Payout ratios recently have been essentially meaningless with the collapse in corporate earnings, but low, 31% in the third quarter of 2009. Under pressure from stockholders, dividend yields are likely to return to 3% or more. The current high level of corporate cash will also encourage dividend paying.. Also, the S&P utility sector has returned 53%, including dividends, since 2000 while the total return on the S&P 500 index has been a minus 11%.

With stocks likely to be weak this year, dividend yields may constitute 100% or more of total returns. Note, however, that although the prices of utility and other defensive stocks sometimes rise in bear markets associated with recessions, that's not always the case. That was clearly true in 2008 when virtually every stock sector went down. Utility and other dividend-paying stocks and ETFs based on them, however, can be hedged against general stock market declines.

3. Buy Consumer Staples and Foods. Items like laundry detergent, bread and toothpaste are basic essentials of life that are purchased in good times and bad. In fact, as we've seen lately, consumers are buying more of their calories in supermarkets and they economize by eating at home rather than in restaurants. Note, however, that they are downgrading from national brands to cheaper house brands, and likely will continue to do so as a weak economy and high unemployment persist. Among retailers, the winners may continue to be discounters. Producers of national brands will need to continue to adapt to consumer downgrading by emphasizing cheaper "value" products.

4. Buy Small Luxuries. This is an investment concept we developed years ago. Consumers, especially when they're hard pressed, tend to buy the very best of what they can afford, even if it's within a low-priced category. We first noticed this tendency years ago, before apartheid ended in South Africa. We read that urban blacks there often carried the elegant, slim and expensive umbrellas typical of investment bankers in London. They couldn't afford cars or maybe even taxi fares, but did achieve status and satisfaction with fine umbrellas. We also learned of a currently unemployed man who enjoyed the status of morning coffee at 7-Eleven six days a week. By reusing his cup and the one he takes home to his wife, he gets a 32-cent discount per $1.37 serving and saves $655 a year on this small luxury.

Companies are adapting to small luxury modes in various ways. Some are offering the same products with lower cost and selling prices. Coach is cutting ladies handbag prices and working with suppliers to reduce costs. Neiman Marcus is pressing suppliers for lower-cost versions of designer styles.

Others are putting their prestigious names on different products. C.F. Martin reintroduced its stripped down 1930s guitar for under $1,000. Average prices were in the $2,000 to $3,000 range and its top of the line guitar sells for $100,000. California winemakers are emphasizing cheaper wines as sales of those over $25 per bottle slump. Consumers are retrenching and dining out less at upscale restaurants where fine wines are sold. Tiffany sales of products over $50,000 are weak, but high-quality small items continue to sell well--always in its trademark blue box. Procter & Gamble has not cut prices on its top of the line products that sell at premiums but carry high-quality images. Consumers still splurge on such small luxuries as Gillette's five-blade Fusion razor and Olay's Pro-X moisturizer. But P&G has introduced cheaper "value" versions of Tide and other products to compete with the growing consumer interest in lower-cost national and house brands.

5. Buy The Dollar. Dumping on the dollar was the favorite sport of investors and the financial media until very recently. The financial meltdown in 2008 drove investors to the dollar as the global safe haven, but in early 2009 that status faded as fears of financial collapse melted. Buck-busters cited the record low short-term interest rates, with the fed funds target rate at 0-0.25%, even lower than in Japan.

This made the greenback the preferred funding currency for the carry trade in which it is borrowed and then sold for other higher yielding currencies with rising interest rates. The falling dollar against those currencies enhances the profitability of those trades. Buck dumpers also emphasized the tremendous amount of dollars being pumped out by the Fed and the Treasury 70 in their attempt to revitalize the economy 68 and the Fed's clearly-stated commitment to keep short-term interest rates low for an extended period.

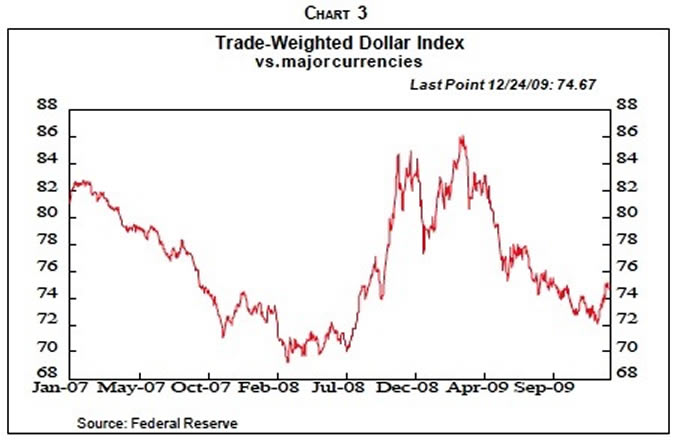

Despite all its drawbacks, however, the dollar remains the world's reserve currency and safe haven, regardless of suggestions by the Chinese and others that the dollar should eventually be replaced by a global currency. This status for the buck appears to be reemerging and will grow if we're right and hopes for a rapid economic recovery are dashed. Furthermore, almost everyone was on the dump-the-dollar side of the boat, a situation similar to early in 2008 that preceded the dollar's jump starting in mid-year (Chart 3). History suggests that when that happens, the winds often shift and all those folks will get tossed into the water as the boat sails in the reverse direction.

We favor selling British sterling since the U.K. economy remains in deep trouble, with even higher external debt than in the U.S.-- a ratio to GDP of 404% in 2008 compared to 95% in this country, which has caused bond rating agencies to threaten a downgrade of U.K. government debt. Also, the troubled British financial sector accounts for 21% of total jobs compared with 14% in the U.S. The U.K. was almost alone among advanced countries in suffering a falling economy in the third quarter of last year.

The euro is vulnerable, in our view, because the eurozone has a one-size-fits-all monetary policy but its economies vary in strength from Germany and the Low Countries at the top to Portugal, Italy, Spain, Greece and Ireland at the bottom. Those lands can't use independent monetary policies to stimulate their economies since that's the providence of the European Central Bank. So they need to resort to fiscal stimuli and increasing government borrowing to finance the resulting deficits. A number have suffered sovereign debt rating downgrades, which increase their borrowing costs, and more are likely. This could spark renewed threats that one or more countries will withdraw from the eurozone and go back to using drachmas, draculas or whatever as their currencies. That probably won't happen as the ECB will do all it can to prevent dissolution, but serious discussion of the likelihood could depress the euro considerably against the dollar.

These concerns are not new for us. Just as the euro was being launched 10 years ago, we wrote in our Dec. 1998 Insight that with a common currency, individual countries would be forced to rely on fiscal policy to deal with local business conditions and "the limit on fiscal stimulus will be default risks. Government bond investors and rating agencies will become the policemen and will blow the whistle.... It's even possible that economic differentials among countries may be so great that the common currency doesn't hold together, especially in the next European recession when unemployment leaps...."

Commodity-driven currencies like the Canadian, Australian and New Zealand dollars are also likely to weaken against the greenback as commodity prices fall. The Japanese economy remains weak and back in deflation, but the yen's involvement I the carry trade makes it a tricky currency for investment.

6. Buy Eurodollar Futures. In most markets, traders want to be where the action is, where liquidity is the greatest even though that's where competition is the strongest. Years ago, a jeweler in New York City complained to us about how fierce the competition was in his location. His shop was on 47th Street between Fifth and Sixth Avenues, the heart of the jewelry district. We asked why he didn't move to a less competitive area. He shrugged and said, "This is where the action is." In the case of short-term credit instruments used in futures trading, eurodollars are where the action is.

Our interest is in eurodollar futures contracts. Eurodollar futures are a way for companies and banks to lock in an interest rate today, for money it intends to borrow or lend in the future, and for investors to bet on the future direction of short-term interest rates. Each Eurodollar futures contract has a notional or "face value" of $1 million, though the leverage used in futures allows one contract to be traded with a margin of about $1,000. Trading in Eurodollar futures is extensive, and the market for them tends to be very liquid. The prices of Eurodollars are quite responsive to Fed policy, inflation, and economic indicators. It's ironic that eurodollar futures markets dominate trading, not those for Treasury bills or federal funds on which eurodollars are essentially based.

Eurodollar futures prices are determined by the market's forecast of the 3-month US$ LIBOR interest rate expected to prevail on the settlement date. Eurodollar futures contracts extend out for 40 quarters or 10 years, so they can be used to bet on interest rate movements many quarters ahead.

Long positions in eurodollar futures have been one of our most successful investments in recent years. Earlier, the futures market did not price in the full extent of the Fed-engineered decline in short-term interest rates. With our forecast of the financial crisis and the worst recession since the 1930s, however, we believed that the Fed would ease dramatically. So we reasoned that eurodollar futures prices would rise as they reflected the Fed's action. So far, they have.

Now the futures market assumes that the Fed will raise its target rate in the course of this year, so the LIBOR rate on which eurodollar futures settle will increase by 1.22 percentage points between January and December. We, however, believe that a weak economy will keep the Fed on hold throughout this year, so the interest rate implied by the December 2010 contract will fall by 1.22 percentage points. That would result in a $3,050 profit on a $1 million futures contract. That's a mere 0.3% gain. This is hardly worth the investment without leverage. But with only a $1,000 margin requirement on the futures contract, well, you do the math.

INVESTMENTS TO SELL OR AVOID

We hope these six investment strategies for 2010 that involve buying or being long securities are useful. But given our forecast that, at best, the U.S. and global economies will be sluggish this year, it won't be a surprise that we have a longer list of strategies that involve selling or avoiding various sectors. In fact, there are 11, or nearly twice as many.

7. Sell U.S. Stocks in General. The S&P 500 index in late December was selling at 19 times top-down Wall Street strategists' operating earnings estimate of $60.59 per share for this year, as noted earlier. That's an historically high P/E to start with that makes stocks vulnerable going into the year. Even more so because it assumes a steep economic recovery in 2010. And even more so if our forecast of continuing recession or sluggish recovery at best proves out. Our $50 estimate of operating earnings, down 11% from estimates for 2009, puts the S&P 500 index P/E at a nosebleed 22.5 level, as noted earlier.

Selling stock indices short, either through futures contracts or ETFs, strikes us as a prudent idea. Index shorts can also hedge long positions in utilities or other long strategies we discussed earlier.

Be well aware that our forecast of a declining U.S. stock market is critical to many other strategies we'll discuss later that involve selling or avoiding equity sectors here and abroad. We believe they all will perform worse than the stock market overall, but if we're wrong and the stock market leaps this year, we'll probably also be wrong on many of these other strategies.

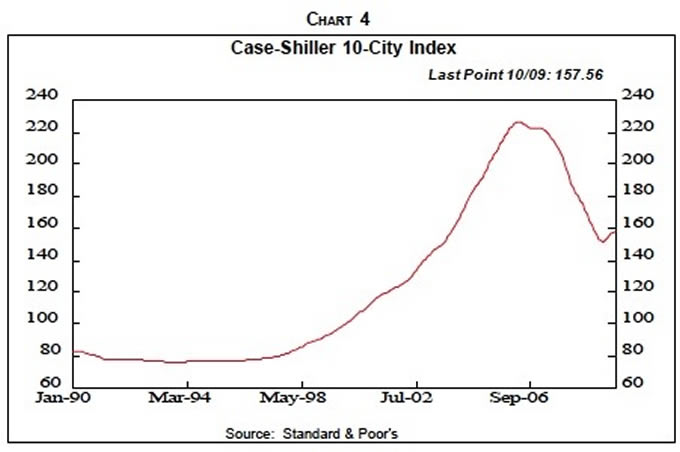

8. Sell Homebuilder and Selected Related Stocks. Homebuilder stocks rebounded sharply from their March 2009 lows, along with stocks in general, but peaked in September with a slight downward trend since then. This may be beginning to reflect our forecast of another 10% decline in house prices (Chart 4). Excess inventories of houses for sale, the mortal enemy of prices, remain huge. And inventories may rise, even with housing starts at very low levels, as people foreclosed out of their houses double up with family and friends.

Also, a quarter of homeowners with mortgages are under water, 40% of those who took out mortgages in 2006. Increasing numbers of these people are convinced that they'll never regain positive home equity and are abandoning their abodes in favor of renting other houses at lower monthly costs. Still, the subsequent foreclosures on their mortgages will keep them from qualifying for a government-guaranteed mortgage for three to five years and will stay on their credit records for seven years.

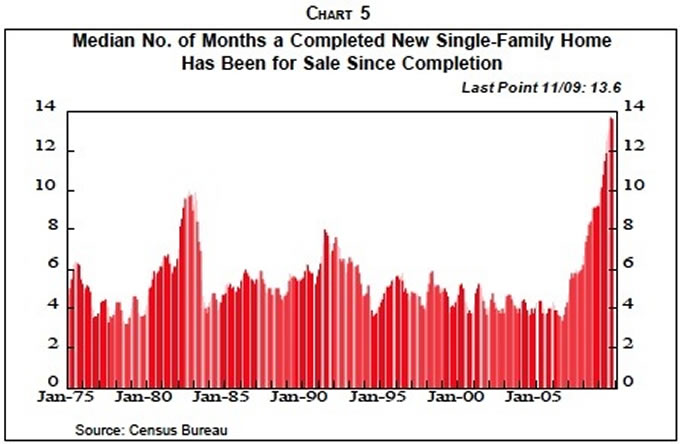

Despite leaping mortgage delinquencies, federally-mandated but mostly unsuccessful mortgage modification programs are keeping many houses, especially middle- and higher-priced homes, from being foreclosed and sold--temporarily. Furthermore, the investment tax credit for new and some existing home buyers, which was extended beyond November 2009, is scheduled to expire in April. The overhang of aging new single-family homes available for sale is huge (Chart 5 ). Also note that new residential mortgages are almost entirely dependent on guarantees from government entities such as Fannie Mae, Freddie Mac and the FHA, and they are tightening their credit standards.

Low mortgage rates are a plus, but are only meaningful to those who qualify for loans as lending standards tighten. Most now need to meet the old conservative standards of 20% down, good credit, full documentation of income and assets, etc. And lower borrowing rates don't help underwater homeowners either refinance or buy other houses. Furthermore, rates on large "jumbo" mortgages remain high.

Finally, lower house prices don't induce buyers who expect the downward trend to continue and hold out for even-lower prices.

9. Sell Selected Big-Ticket Consumer Discretionary Equities--for two powerful reasons. First, as consumers persist in their saving spree they'll continue to curtail spending on expensive postponeable items. Second, as widespread price declines persist, they will be anticipated. Prospective buyers will wait for lower prices. As a result, excess inventories and unused capacity will mount, forcing prices lower. That will confirm prospective buyers' suspicions so they'll wait for still-lower prices in a self-feeding downward spiral.

Deflationary expectations are clearly at work in the vehicle market. The cash-for-clunkers program generated one-time sales as buyers viewed it as just one more rebate inducement in a never-ending stream. But who would dare announce to a friend that he paid the full sticker price for any car? Of course, deflationary expectations don't work for small, inexpensive items. Suppose you know for sure that toothpaste will be cheaper next month. If you run out, you won't brush your teeth with Ajax while waiting for lower prices before buying a tube.

Even the rich, normally immune to recessions, are cutting back and downgrading. Note the weak sales at Tiffanys, Nordstrom and Saks Fifth Avenue and the poor auction results for Sotheby's and Christie's. A Merrill Lynch study found that the number of people in the world with $1 million or more in investable assets fell from 10.1 million in 2007 to 8.6 million in 2008. Those assets dropped from $40.7 trillion to $32.8 trillion. Their equity holdings fell in step with the S&P 500, about 40%, and their real estate also dropped in value.

Ever since the data series began in 1967, the share of income of the top 20% has trended up while all other shares fell. Note that these are shares, not income levels--which have grown on balance for all quintiles. Studies have found considerable rotation in and out of the various quintiles, with many of those in the top bracket in a given year absent from it in earlier and later years. Still, the drop in purchasing power for many middle-income people in the last year in addition to the collapse in their homes' values has created considerable anger at those at the top.

The equities of most producers of big-ticket consumer discretionary goods and services collapsed in the 2007-2009 bear market, reflecting consumers' buying strike, but have recovered somewhat since March. With our conviction that American consumers have reached a watershed and switched from a quarter century borrowing-and-spending binge to a decade or longer saving spree, we are very suspicious of the sustainability of any rebound in stocks of producers of major consumer discretionary products such as cruise lines and airlines.

10. Sell Banks and Other Financial Institutions. During the financial free-for-all days, large banks moved well beyond traditional spread lending--taking deposits and then lending them with interest rate spreads to cover their costs, loan risks and reasonable profits. They hyped their leverage--and their risk--as they set up off-balance sheet vehicles, engaged in proprietary trading and in the origination of and investment in derivatives. Regulators stood by under the theory that free markets would discipline excessive risk-taking. Both the big banks and the regulators, however, knew or should have known that those institutions were too big to fail and could take the financial system down with them. So those financial institutions were really playing a game of, heads we win, tails we get bailed out.

And fail they did, and bailed out they have been. Many investors seem to believe that's the end of the unpleasantness and now it's back to business as usual. The recent big trading profits by some financial institutions certainly point in that direction as did the stock rebounds until recently. We doubt it, though. The financial sector expanded its leverage over about three decades and its deleveraging will probably consume most or all of the next decade. Big risk-taking CEOs like Ken Lewis at Bank of America are being forced out, sending a clear message to the senior officers who remain.

Stringent, probably excessive regulation is replacing the laissez faire model. Higher capital requirements and other limits on risk-taking will curb bank profitability. So will the limits on executive pay aimed at reducing the incentive to take big risks.

Weak Loan Demand

Furthermore, with slow economic growth, consumer zeal to save and repay debts, and weak capital spending this year, loan demand will likely be weak. In addition, the present steep yield curve makes borrowing cheap deposits and lending long-term at higher interest rates very profitable. But it will probably flatten as the year progresses and long rates fall. Banks, of course, can increase fees on checking and other accounts, but are limited by competition from money market funds and other alternatives.

Also, banks' costs of borrowing in the bond market is well off its highs relative to Treasurys, but still elevated compared to pre-crisis years. The spread now runs over three percentage points compared to about one in pre-crisis days. Much of the cheap debt banks acquired from private markets in earlier years and the government more recently will mature in the next several years and need to be replaced at much higher costs. The maturities for U.S. banks have dropped from 7.8 to 3.2 years in the past five years.

Regional and community banks are also likely to be unattractive investments this year. Ironically, in the go-go days, many of them were unwilling to virtually abandon their underwriting standards to compete with nonblank residential mortgage lenders. So they lent to the commercial real estate market instead. That's proving to be a jump from the frying pan into the fire, as discussed earlier, and is shown by weak demand, falling prices and rising delinquencies. Regional banks have more than their share of the $1.7 trillion in outstanding commercial real estate owned by all banks. These loans constitute 35% of regional banks; total loans, up from 25% in 2000.

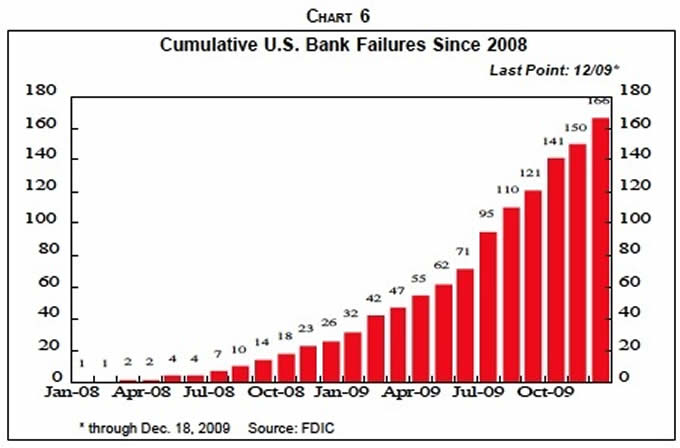

Due to bad commercial as well as residential real estate loans, smaller banks are dropping like flies, 140 so far this year (Chart 6 ). Individually, they aren't too big to fail, but collectively they are since they are the primary financers of smaller businesses. Those businesses don't have access to commercial paper and other credit market vehicles and must rely on their local banks for loans--or on the personal credit cards of their owners.

11. Sell Consumer Lenders' Stocks. Consumer lenders' stocks have also rebounded sharply from their March 2009 lows. We were wrong on our strategy of selling them last year, but believe it will work in 2010.

Consumer lenders had their hey day during the long consumer borrowing-and-spending spree. Consumers were trained--and we use that word deliberately--to believe they deserved instant material gratification. Buy now, put it on the plastic card and pay later-- much later--became the norm. And creditworthiness was no problem for credit card issuers and other consumer lenders. They sliced and diced consumers' financial statuses, used sophisticated models to determine payment risks and charged fees and interest rates to fit any risk category.

But their models and analyses inherently assumed that the borrowing-and-spending binge, as well as the ability to repay, would last indefinitely. But then consumers suddenly switched to a saving spree and started to pay down credit card and other debts. Also, heavy layoffs, leaping unemployment and collapsing house prices and inadequate consumer incomes spiked credit card delinquencies. Congress last year restricted credit card fees and interest charges. Also, consumers went on a buyers strike a year ago and cut back on their use of credit, debit and charge cards.

Recent developments are virtually all negative for the credit card business now and for years to come. The cottage industry to help these people deal with their huge credit card debts is exploding in size. As noted earlier, charge cards and debit cards are replacing credit cards as consumers realize they can't trust themselves to restrain debt and need to pay off monthly or accumulate the money in a bank account before spending it. Layaway plans are replacing the buy now-pay later approach. With the switch from a quarter century consumer borrowing-and-spending binge to a long run saving spree, the credit card business has moved from a growth industry to a laggard.

12. Sell Many Low and Old Tech Capital Equipment Producers. Low and old tech producers will remain depressed in a world of chronic excess capacity. When operating rates are low, producers don't need more capacity and worry that revenues, prices and profits won't be adequate to justify even existing capacity. And note that the volatility of the producers of equipment is much greater than that of the users. Auto sales declined by over 47% from their peak in July 2005, but orders for machine tools, automatic transfer lines and other equipment fell much more as auto assemblers and parts makers almost froze orders. Recall as well how the recession-sired excess capacity in airlines has caused massive cancellations and postponements of orders for Boeing's Dreamliner.

Earlier, we discussed our statistical models that explained capital spending. They show that in accounting for the year-over-year change in the equipment and software or in equipment and software plus nonresidential structures components of GDP, thelevel of operating rates is far and away the most important explanatory variable, even more so for the year-over-year change in operating rates. This indicates that even if capacity utilization is growing rapidly, if it remains at low levels as at present, the growth in capital spending will be subdued.

Other variables, such as the year-over-year changes in cash flow, profits and interest costs, were statistically significant in our models, but much less effective in explaining the change in capital spending. These findings are important because many believe that the negative gap between capital expenditures and internal funds is sure to generate a capital spending surge. But our models, based on history, say that with huge excess capacity, that cash flow won't burn holes in corporate pockets. And our models don't quantify and add in the extra corporate caution spawned by today's recessionary climate and financial crises.

Besides the depressing effects of excess capacity, low and old tech companies suffer from ongoing problems. Foreign competition continues to grow as their technology is transferred to China and other cheap production locales. Some suffer rising cost pressures due to lack of productivity gains. High-cost unionized labor forces are sometimes a problem. And many sell into saturated, slow growth markets.

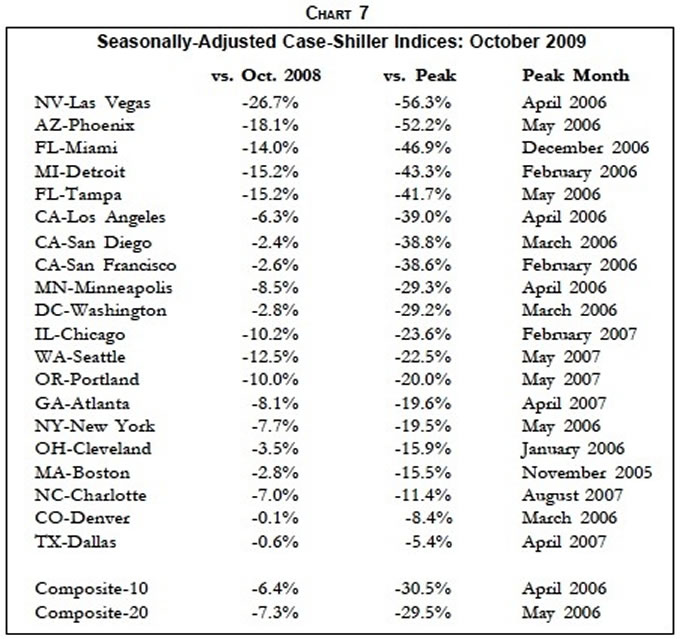

13. If You Plan to Sell Your House, Second Home or Investment Houses Any Time Soon, Do So Yesterday. This strategy has worked for the last two years and will continue to do so if we're correct and house prices nationwide fall another 10%. Sure, prices have been weakest in states like Florida, Arizona, Nevada and California where the biggest bubbles preceded the collapses. But almost every area of the country has experienced price declines (Chart 7 ).

Many owners have tried to wait out the bear market in housing, a technique that worked in earlier years when any price declines were small and short-lived. But huge excess inventories, a flood of distressed sales after mortgage modification attempts are over, depressed incomes and rising unemployment will probably keep sellers plentiful, buyers reluctant and prices falling throughout 2010 and perhaps beyond. In past regional house price collapses, it's taken homeowners a year-and-a-half to give up and throw their houses on the market for whatever they will bring. After the final bottom is reached, house prices will likely mirror inflation, or in future years, deflation as they have historically.

14. Sell Junk Bonds. During the dark days of the financial crisis, the yields on junk bonds leaped to 19.3 percentage points over Treasurys as investors worried about complete financial collapse and widespread defaults among low-grade issues. Triple-C rated bonds, the lowest junk tier, sold at 42.6 cents on the dollar at the beginning of last year.

But the bailout of the big banks and easing of the financial crisis allayed investor fears and junk spreads narrowed. Institutional investors piled in, followed by individual investors, many of whom sought alternatives to low returns on bank deposits and money market funds. So the spread has dropped to 4.6 percentage points, much closer to where it was before the crisis began. Last year, junk bonds returned over 50%, much more than the 25% gain on the S&P 500 index.

Nevertheless, we believe this rally is way overdone. Default rates on junk bonds normally peak late in recessions or in the year after it ends. Also, the default rate may reach or exceed the previous peak in 2002 if the economy remains weak, suggesting major declines in junk bond prices. Furthermore, the value of bonds after default is likely to go lower if the recession drags on, as we forecast. Slow revenue and cash flow growth will make it difficult if not impossible for a number of financially weak and weakening firms to service their bonds and other debts.

15. Sell Commercial Real Estate. As discussed earlier, excess capacity and big refinancing requirements in coming years will continue to plague hotels, malls, warehouses and office buildings. Moody's/REAL Commercial Property Price Index was down 44% last October from its October 2007 peak. Retailers closed 8,300 stores last year, more than the previous peak of 6,900 in 2001. Businesses will continue to cut costs this year, not only by holding down employment and therefore the need for office space, but also by moving in the partitions to fit the remaining people in less space, as mentioned earlier.

Increasing use of telecommuting will also reduce need for office buildings. And more teleconferencing will cut hotel-utilizing business trips, especially after intensified airport security in reaction to the recent terrorist incident in Detroit on Christmas Day. At the same time, frugal consumers will restrain discretionary travel and the hotel and motel use involved. Weak consumer spending will keep mall and warehouse space under pressure.

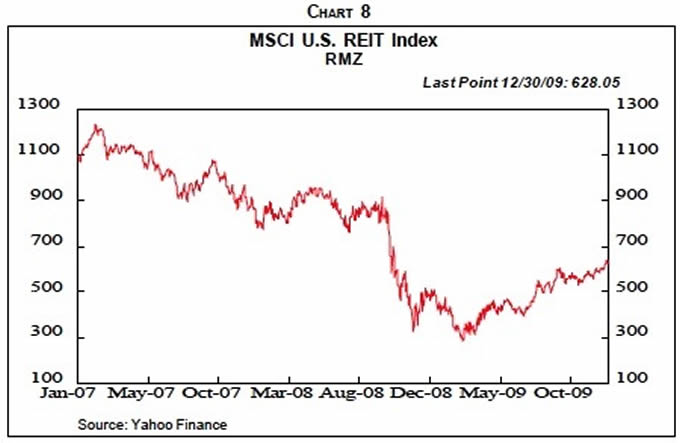

Some believe that commercial real estate woes may exceed the residential collapse, and they may be right. Commercial tends to be less leveraged but if refinancing isn't available, it may note make much difference how leveraged it is. Also, distressed commercial real estate owners definitely don't have the political sympathy and bailout prospects enjoyed by troubled homeowners. The Fed has set high standards for bailout loans on commercial real estate. Commercial real estate REITs rebounded last year along with the overall stock market (Chart 8 ), but strike us as vulnerable. These leaps combined with plummeting real estate prices have pushed REIT prices to a 25% premium over their net asset values.

16. Sell Most Commodities. Commodity prices rebounded last year and benefited from cheap and available money. Some live in their own worlds. Petroleum is not only influenced by fundamental supply-demand conditions, but also by OPEC decisions. Natural gas prices in the U.S. weakened last year with the recession, but also because of new production technology that unlocked abundant shale gas. The prices of agriculture commodities, including honey, are highly dependent on weather.

In any event, we believe that economic supply and demand will rule most industrial commodity prices this year and result in weakness due to sluggish global business conditions. Also, investors put a record $50 billion into commodities in 2008 but then retreated last year after prices nosedived. They learned the hard way that commodities aren't an asset class but speculations, and may be cautious this year. And the strengthening dollar should depress the prices of the many commodities traded worldwide in dollar terms. We look for falling commodity prices this year. Also, we believe that many commodity-producing companies and their suppliers of equipment and supplies will be unattractive investments as weak demand, excess capacity and soft prices persist. The same is true for economies such as Persian Gulf sheikdoms that depend heavily on petroleum, as witnessed by the financial collapse of Dubai.

17. Sell Developing Country Stocks and Bonds. As late as the end of 2007, most forecasters believed in decoupling. Even if the U.S. economy suffers a setback, they said, the rest of the world, especially developing countries like China and India, would continue to flourish. Indeed, the strength of those economies could even aid the U.S. as they bought more American exports.

We disagreed. We did a study two years ago that found that China was not yet developed sufficiently to have enough people with discretionary spending to support the economy domestically. She remained export-led, with most of those exports going directly or indirectly to U.S. consumers. So, with our forecast of a major retrenchment by U.S. consumers, we predicted big trouble for China. Our analysis revealed that in China, it takes about $5,000 per capita to have meaningful discretionary spending power. About 110 million Chinese had that much or more, but they constituted only 8% of the population. In India, that class was a mere 5% of the population. In contrast, it takes $26,000 per capita in the U.S. to have discretionary spending power and 80% of Americans have at least that much.

Well, as they say, the rest is history. The Chinese and most other developing Asian countries nosedived as U.S. consumers retrenched. But in the wake of China's huge $585 billion stimulus program last year, massive imports of industrial materials like iron ore and copper, jumps in construction of cement, steel and power plants and other industrial capacity, and a pick up in economic growth, many forecasters again believe in decoupling.

We continue to disagree. Sure, some countries such as Brazil were not hurt too severely by the global recession, at least so far. Still, most developing economies depend on exports for growth, and the U.S. consumer has been the biggest buyer of those exports and far and away the globe's biggest spenders. As the American consumer saving spree continues to shrink the U.S. trade and current account deficits (Chart 9), those developing economies will be subdued.

China's economy looks like a house of cards. Her most recent fiscal stimulus not only went into industrial capacity-building but also bank lending-spawned stock market and real estate speculation. But what will utilize that capacity and justify those speculations? The usual outlet, exports, is curtailed by retrenching U.S. consumers. And, as noted, China is not far enough down the road to industrialization for local consumers to fill the gap.

We doubt that the rebounds in emerging market stocks and bonds correctly forecast robust, decoupled economic growth that is sustainable. While the S&P 500 now trades at 20 times earnings over the last 12 months, normally cheaper emerging markets are more expensive. Recently, the Shanghai Composite Index sported a 32 P/E while South Korea's was at 35 and Indonesia's was at 29. And note that the 65% jump in emerging market stocks in 2009 only offset two-thirds of the 54% drop in 2008.

Furthermore, as was made clear by the universal weakness in security markets in 2008, bond and stock markets around the world are highly correlated. With globalization, the days are gone when a globe-trotting sleuth can discover gems in the remote reaches of Asia or Latin America. The similarity of bond and stock performance is even greater when adjusted for risk. Emerging market stocks and bonds may climb more in bull markets, but have greater falls when the bear arrives, as we believe he is about to. There's no such thing as free lunch.

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.