Silver set to Soar as it did in the 1970’s

Commodities / Gold & Silver 2009 Nov 03, 2009 - 10:32 AM GMTBy: GoldCore

- Silver Remains Very Undervalued

- Silver Remains Very Undervalued

- Why Silver is in a Bull Market & How High Could it Go?

- Is Silver about returns or a hedge against inflation & systemic risk?

- Silver: Declining Supply

- Silver: Increasing Industrial Demand

- Silver: Increasing Investment Demand

- Silver Undervalued Versus Gold

- A Picture is Worth a Thousand Words

- Conclusion

http://www.coinlink.com/..

Silver Remains Very Undervalued

Silver remains very undervalued on an historical basis (charts below) and is undervalued even against gold (chart below). While gold has begun to receive some interest from a small minority of retail investors, silver remains the preserve of relatively few contrarian investors and the media and financial press rarely if ever covers silver. And yet silver is quite likely in the intermediate stage of a bull market that will rival or surpass that of the 1970’s.

Silver is currently worth less than $17.00 per ounce. Silver rose to a recent nominal high $20.88/oz in March 2008. After an 18 month period of correction and consolidation, silver looks set to challenge that high in the coming months. We continue to be bullish on gold and particularly silver and believe that silver will likely surpass its non inflation adjusted high of $48.70 per ounce and its inflation adjusted high of some $130 per ounce in the coming years.

Why Silver is in a Bull Market and How High Could it Go?

Precious metals has been the best performing asset classes in recent years with gold and silver outperforming equities, property and most asset classes over a 3, 5 and 10 year period. This outperformance looks set to continue in the coming months due to the very bullish fundamentals. The primary reason for our bullish outlook on silver is due to the continuing and increasing global macroeconomic, currency and geopolitical risks; silver’s historic role as money and a store of value; the declining and very small supply of silver; significant industrial demand and perhaps most importantly significant and increasing investment demand.

Gold, oil and nearly every major commodity, stock indices and property market surpassed their record highs in recent years. Favourable supply and demand factors, continuing global macroeconomic and geopolitical risk and concerns regarding the emergence of inflation and stagflation as the massive global monetary and fiscal reflation affects the value of fiat currencies all point to higher silver prices in the long term.

In the 1970’s silver rose from under $1.50/oz in 1970 to nearly $50/oz in 1980. Thus, silver rose by more than 25 times or by more than 2,400%. Were silver to replicate its performance in the 1970’s, it would have to rise by more than 25 times again. The average price of silver in 2001 was $4.37/oz and 25 fold increase would result in silver rising to over $110/oz. While this price target may seem outlandish to some, it is worth remembering that silver’s record high in 1980 adjusted for inflation (according to US government inflation figures) was some $130/oz.

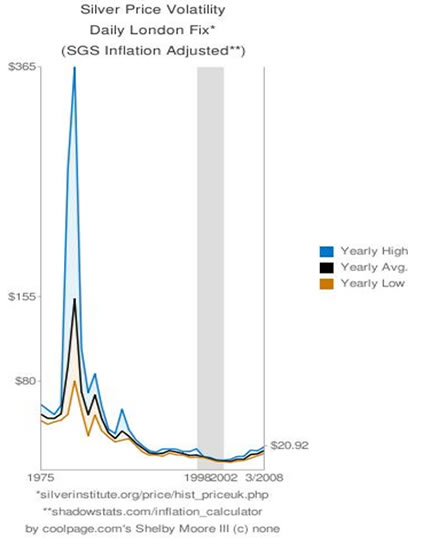

SGS Inflation Adjusted Silver Price (using more accurate government

methodology of measuring inflation that was used in 1980)

Admittedly, the final phase of the silver blow off was a speculative bubble as the billionaire Hunt brothers attempted to corner the silver market. Unlike in 1979, today there are hundreds of billionaires, some multi billionaires, thousands of millionaires, hedge funds and many sovereign wealth funds. Small allocations by any of these will see sharp moves up in the price. Indeed, the silver market is so small that it could very easily be cornered again (as appears to be happened in the tin market in recent weeks).

Is Silver about returns or a hedge against inflation & systemic risk?

Silver is a hedge against macroeconomic, systemic and inflationary risk with the attractive added potential for significant capital gains. Real asset allocation and prudent diversification would be an important reason to have an allocation to silver. Silver is highly correlated to the safe haven of gold and is in effect a leveraged sister of the precious yellow metal. Thus, informed investors use gold more for wealth preservation purposes and silver in order to make a return.

Silver: Declining Supply

In 1900 there were 12 billion oz of silver in the world. By 1990, the internationally respected commodities-research firm CPM Group say that figure had been reduced to around 2.2 billion ounces of silver. Today, that figure has fallen to less than 1 billion ounces in above ground refined silver. It is estimated more than 90% of all the silver that has ever been mined has been consumed by the global photography, technology, medical, defence and electronic industries.

On current supply/demand trends, the amount of above ground refined silver is projected to shrink to even lower levels in the coming years. Industrial demand has been outstripping mining supply for most of the last 20 years, driving above ground supply to historically low levels. Few in the investment world are aware of this important fact.

Silver production has been flat in recent years while demand has been increasing. This hasn't resulted in significantly higher prices yet because the world has been able to fill the gap from inventories and official government stockpiles.

However, today the U.S. government's stockpile is all but gone, and sales from other official sources, such as China, Russia and India, are declining, too. The decline in refined silver stocks, from around 2.2 billion ounces in 1990 to around 300 million ounces today means that silver stocks are near an all time low.

Very importantly, silver is very unusual as its supply is inelastic.

This means that silver production will not ramp up significantly if the silver price goes up. Supply didn't increase significantly in the 1970’s when silver rose more than 35 fold in price – from $1.40/oz in 1971 to a high of nearly $50/oz in 1980. Importantly, silver is a byproduct metal and some 80% of mined silver is a byproduct of base metals. Higher prices for silver will not cause copper, nickel, zinc, lead or other base metal miners to increase their production. In the event of a global stagflationary or deflationary slowdown, demand for base metals would likely fall thus further decreasing the supply of mined silver.

There are only a handful of pure silver mines remaining – many with depleting reserves. This inflexible supply means that we cannot expect significant mine supply to depress the price after silver rises in price. It is extremely rare to find a good, service, commodity or investment that is price inelastic in both supply and demand. This is another powerfully bullish aspect unique to silver.

Silver: Increasing Industrial Demand

Industrial applications for silver have always been significant but have increased significantly in recent years. Silver is used in film, mirrors, batteries, medical devices, electrical appliances such as fridges, toasters, washing machines and uses have expanded to include cell phones, flat-screen televisions and many other modern high tech devices.

Increasing industrial demand for silver is forecast due to economic growth in China, India, Vietnam, Russia, Brazil and other emerging economies in South America, the Middle East and Asia. Growing middle classes are now demanding the quality of life and standard of living enjoyed by many in the West and thus the demand for silver will likely increase.

Silver is known as the ‘healthy metal’ and has many and increasing medical applications.

In a world that is showing increasing concern about the spread of diseases and pandemics such as swine flu, silver is being increasingly tapped for its biocidal properties. Research is ongoing on the use of silver and its compounds for therapeutic uses and on its potential use as a disinfectant in hospitals and other medical facilities.

Increasingly, silver’s antimicrobial and antibacterial qualities are seeing it being used in all sorts of medical applications and this looks set to become a very significant source of demand in the coming years.

Silver has many unique properties which make it ideal and indeed essential in global industry – especially in the global photography, technology, medical, defence and electronic industries. Yet, silver is a finite resource and the supply of silver is increasing only very incrementally.

It is important to note that silver, unlike gold, is heavily used in industry and because of gold's much higher value, it gets recycled and all the gold mined in the world ever is still with us but a huge amount of silver has been used in photography, mirrors and other industrial uses in the last 200 years. The low price of silver makes recovery and recycling uneconomic.

Unlike gold, silver is like oil – as it is consumed in these many industrial applications it is gone forever.

Silver: Increasing Investment Demand

Investment demand for silver has risen in recent years as investors concerned about the value and safety of property, equities and deposits allocated funds to the finite commodities and currencies of silver and gold. More recently, there are increasing concerns about the value of paper currencies themselves (voiced by many including Alan Greenspan, John Paulson and George Soros) which is leading to further diversification into hard assets and precious metals.

There has been a marked increase in investment demand for silver in recent years. Some of the reasons why this trend is likely to continue are - the introduction of ETFs that track the price of silver, a new global liquidity bubble, the significant growth in the global money supply, the proliferation of millionaires, ultra high net worth individuals and billionaires, the proliferation of hedge funds and the exponential growth in derivatives.

The Bank for International Settlements has estimated that the total value of derivatives contracts was $592 trillion at the end of 2008 (up exponentially from $260 trillion in June 2006). Thus, dwarfing the GDP of the entire world which was estimated at some $61 trillion at the end of 2008.

There is still a debate as to whether derivatives are a good or a bad thing. Alan Greenspan recently warned they could lead to "cascading cross defaults." Warren Buffett is similarly concerned and has warned that they could trigger “serious systemic problems.” Buffet said that “the derivatives genie is now well out of the bottle, and these instruments will almost certainly multiply in variety and number until some event makes their toxicity clear. “

For this reason Buffett presciently called derivatives “financial weapons of mass destruction” in 2003.

Investors in silver bullion coins and bars are hedging themselves against further deflation and falls in property and equity markets. They are further protecting themselves against rising inflation, possible currency devaluations and still very prevalent geopolitical and macroeconomic risks such those posed by the humongous global derivatives market.

Silver Undervalued Versus Gold

Silver is undervalued versus gold with the gold silver ratio at 60:1 ($1050oz/$17/oz) This is particularly the case on a long term historical basis. The long term historical average gold to silver ratio is 15:1 and this is because it is estimated that geologically there are some 15 parts of silver in the ground for every one part of gold. In 1980 the ratio nearly reached 15 ($850oz/$50oz=17) and the average in the 20th century has been around 40:1.

Many analysts believe that silver’s ratio to gold will revert to its mean average in recent years below 40:1. Even if gold only remained at some $1,000/oz this would see silver rise to some $25/oz ($1,000oz/$40oz=25).

A Picture is Worth a Thousand Words

SGS Inflation Adjusted Silver Price (using more accurate government

methodology of measuring inflation that was used in 1980)

A picture or a chart truly is worth a thousand words and the chart above showing silver prices adjusted for inflation shows how seriously undervalued silver remains.

Conclusion

Silver is unique in terms of being both a monetary and an industrial metal. Silver is priced at less than $17/oz today. The average nominal price of silver in 1979 and 1980 was $21.80/oz and $16.39/oz respectively. In today’s dollars and adjusted for inflation that would equate to an inflation adjusted average price of some $60/oz and $44/oz in 1979 and 1980. It is for this reason that we believe silver will be valued at well over $50/oz in the coming years and silver remains the investment opportunity of a lifetime.

GoldCore Recommendation

Prudent Investors Should have an Allocation to Silver

Prudent Investors Should have an Allocation to Silver

Buy Silver Eagles at the Most Competitive Prices for Delivery or Storage in one of the safest international precious metal vaults in the world.

Silver Eagles are the official silver bullion coin of the United States and are guaranteed to contain one troy ounce of 99.99% pure silver. Since 1986 over 70 million American Silver Eagles have been bought by prudent investors and savers. Silver Eagles have become the most popular bullion coins in the world because of their beauty, quality and the assurance of weight and purity by the U.S. Mint.

Silver Eagles are issued by the US Mint and are US dollar legal tender and can thus be imported and stored in many jurisdictions (including with Via Mat Zurich) without any VAT being applicable.

Please call the GoldCore Bullion Services Team on

(Irl)+353 1 632 5010

(UK)+44 203 086 9200

(US) +1 (302)635 1160

By Mark O'Byrne

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.