United States Has Caught the Japanese Economic Disease, Who Will buy Our Debt?

Economics / Great Depression II Oct 17, 2009 - 05:31 PM GMTBy: John_Mauldin

Muddle Through, R.I.P?

Muddle Through, R.I.P?

Savings Equal Investments

Japanese Disease

Who Will Buy the Debt?

The New Muddle Through Economy

I first wrote about the Muddle Through Economy in 2002, and the term has more or less become a theme we have returned to from time to time. In 2007 I wrote that we would indeed get back to a Muddle Through Economy after the end of the coming recession. If you Google the term, at least for the first four pages more than half the references are to this e-letter. I get a lot of flak from both bulls and bears about being either too optimistic or too pessimistic. Being in the muddle through middle is comfortable to me.

Last week I expressed my concern that we as a country are taking actions that could indeed "Kill the Goose" of our free-market economy. I rightly got letters asking me how I could maintain Muddle Through in the face of that letter. I have given it a lot of thought and research. How likely are we to muddle through in the face of $1.5 trillion and larger deficits? Today we take another look at Muddle Through. It should be interesting.

But first, two housekeeping items. I want to welcome the 150,000 members of the National Association of the Self-Employed to this letter. They have asked me to be a special consulting economist to their group, and they will send this letter each week to their members. Since its beginning in 1981, the National Association for the Self-Employed has pioneered support for micro-businesses and the self-employed, and been a forceful advocate for small business in this country. (www.nase.org) I am honored. I am pleased to add you to my 1 million closest friends. I hope you find it useful.

Second, I will be going to South America at the end of next week, to Buenos Aires, Montevideo, Sao Paulo and Rio. I will be speaking in those cities and traveling with my new Latin American partner, Enrique Fynn of Fynn Capital (based in Uruguay). If you would like to find out about this tour or what services he can help you with, you can go to www.accreditedinvestor.ws and sign up and Enrique will get in touch with you. And as always, if you are an accredited investor, you can go to that website and one of my partners in the world will get back to you. (In this regard, I am president of and a registered representative of Millennium Wave Securities, LLC, member FINRA.) And now to the letter.

Muddle Through, R.I.P.?

I defined a Muddle Through Economy in the past as one of slow growth (in the area of 1-2%) and a slack employment environment, such as we had in 2002 and the early part of 2003. In early 2007, I suggested we would return at some point to such an environment at the end of the recession I was predicting.

I am not surprised about the response of the Fed to the current recession and credit crisis, whether it's the large monetization of debt or the low interest rates. Assuming they more or less remove the monetary easing in a reasonable manner, there is nothing that would make me think we do not eventually recover, albeit at a very slow Muddle Through pace, with a jobless recovery that lasts for several years. It will not be pleasant, but we'll survive.

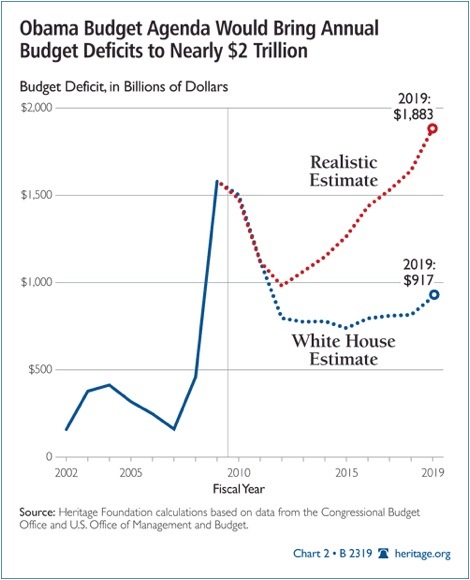

However, gentle reader, never in my wildest dreams did I think we could be looking at government deficits of $1.5 trillion dollars and actually budgeting future deficits of over $1 trillion as far as the eye can see. And there is real reason to think that under current plans, $1 trillion deficits are optimistic. Look at the graph above from the Heritage Foundation. They suggest that current policy would bring us closer to a $2 trillion deficit by 2019.

And that assumes nominal growth that is north of 3% and unemployment dropping back below 5% in reasonably short order. If you make less optimistic assumptions, the number can become much larger rather quickly. Where do we find that much money to finance that large a deficit? We will look at what might be the answer, but first we need to look at a basic concept in economics.

Savings Equal Investments

GDP (Gross Domestic Product) is defined as Consumption (C) plus Investment (I) plus Government Spending (G) plus [Exports (E) minus Imports (I)] or:

GDP = C + I + G + (E-I)

(For the wonks out there, GDP is usually termed "Y".)

You can calculate national savings as GDP minus consumption and government spending. That means that investment equals savings plus net exports. If there are no net exports, then money must come back into the US from outside the country to finance investments, along with savings.

This equation is known as an identity. An identity is an equality that remains true regardless of the values of any variables that appear within it. That means it is not a guess or an approximation. It is simple reality.

Thus, if there is a government deficit, there must be savings by both consumers and businesses, plus capital flows from outside the country, to offset that deficit in order for there to be any money left over for investments.

In the short run, an increase in government spending can offset a decline in consumption (a recession), but absent savings a government deficit crowds out investment in the long run. There must be savings in order for there to be investment. And without investment, you do not get job growth or economic growth.

Japanese Disease

Some readers wrote this week telling me I am far too worried about a rising government deficit. Right now we are at roughly 42% of debt to GDP. In 1989, at the start of the lost decades, Japan had a debt-to-GDP ratio of 51%. Now it is at 178%, and the world has not come to an end for them. In fact, they are running massive government deficits today and plan to do so for a long time. Why, I am asked, can't we be like Japan? And my answer is that it is possible, but the cost that Japan has paid has been high.

In 1989, private Japanese debt (businesses and consumers) was at a debt-to-GDP ratio of 212%. Now it is at 110%. And the total of both government and private debt is roughly the same (within 5%) of where it was 20 years ago. Along with running large trade surpluses, private debt has been exchanged for government debt. Savings have fallen from the mid-teens to about 2% today, as the country is rapidly aging and now using its savings to live on. And how much has all that government spending helped the country? Before I answer that, read these paragraphs from Hoisington Asset Management's latest letter (last week's Outside the Box):

"The federal government's promise to extricate the U.S. economy from this recession involves more spending (increasing public debt) and more subsidies for consumers, such as car rebates and home buying incentives (more private debt). In other words, more debt is supposed to solve the problem of over-indebtedness. The truth is that this policy merely indentures its citizens further without providing any income for repayment of debt. In previous letters we have discussed the fact that the government spending multiplier is zero (read Professor Robert Barro's book, Macroeconomics - a Modern Approach, p. 370).

"This means there is no long term income benefit from stimulus programs. According to the latest academic research, the most recent $800 billion stimulus plan will boost economic activity in the short run, but will surely depress economic activity over time. The government problem is complicated by the fact that the tax multiplier is 3, meaning that a 1% change in taxes will change GDP by about 3% over time. More recent research (Barro & Redlick, September 2009, "NBER Working Paper 15369") suggests that a 1% cut in the marginal tax rate would raise GDP in the ensuing year by 0.6%. With the deficit rising due to a zero spending multiplier, the tendency will be to try to raise taxes to pay for this higher level of expenditures, which will further depress aggregate spending and output."

For all intents and purposes, Japan has had no growth for almost two decades. Their nominal GDP is where it was 17 years ago, and the number of employed people is at 20-years-ago levels. An aging population has masked their unemployment problems, as older citizens retire. Their savings went to government debt. Taxes were raised numerous times. Since government deficit spending has no long-term multiplier effect, growth has been nonexistent. (By the way, that research about multiplier effects has also been done by Christina Romer, the chairman of the current President's Council of Economic Advisors, and further explored by European economists. There is general agreement on these facts.)

In 1998, the US had a total debt- (government plus private) to-GDP ratio of 260%. Today it is 373%. We have added over $15 trillion in debt, yet total employment today is roughly where it was 9 years ago. But the current economic leadership wants to solve the problem of too much debt with even more debt. I am sympathetic with the idea that in the short run the government should step in and the Fed should print (within limits) money to keep us from deflation. But the equation we spent time on earlier suggests that if we continue to run massive deficits, we run the risk of catching Japanese disease - a decade-long (or longer) period of slow growth and high unemployment, especially since our population is growing and our Boomers are going back to work (and surveys suggest they intend to work longer).

Large government deficits choke off the very investment that we need to create jobs. In the name of doing good, the unintended consequence is to make it more difficult for small businesses to start up and create jobs. And we all know that small business is the engine for job creation.

The way out of the current morass is to create jobs and increase productivity. But if the government runs deficits of $1.5 trillion, that means whatever savings (corporate and consumer) we have will not go into the investments we need, but into government debt.

Who Will Buy the Debt?

Now, let's go back to the problem of who will buy the debt. How can we find $1.5 trillion each and every year? Some of it will come from foreign central banks, as we continue to run a trade deficit. Once those dollars leave our shores, they do not disappear. They can only go back into a dollar-denominated investment. Up to now, that has typically been US government debt. If China decides to use its dollars to buy commodities or other assets, whoever sells them the assets now has the dollars and must decide what to do with them. So give or take a few billion, about $400 billion will come back to the US from our trade deficit next year. That still leaves $1.1 trillion.

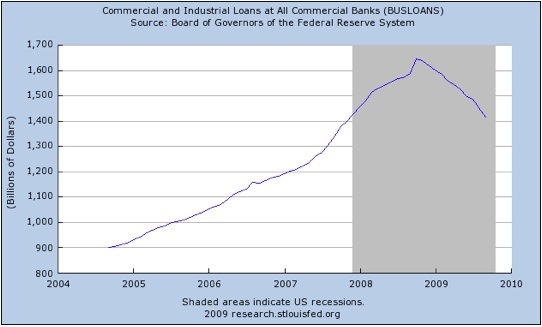

Upon reflection, and cutting to the chase, I think that the buyers of the debt could be US banks for quite some time. The next graph shows commercial and industrial loans at US banks falling precipitously. Banks have (correctly) tightened lending standards, but that means that small and medium-sized businesses, which account for over 85% of all jobs, have been cut off from the life blood of growth. Is it any wonder they are cutting jobs at a prodigious rate?

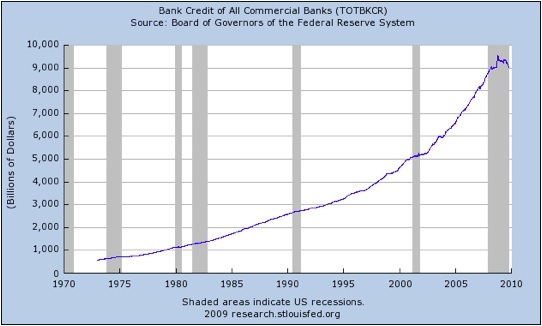

The next graph shows bank credit (of all types), going back to 1974. Notice that even during recessions (gray shaded areas) bank lending either grows or at the most goes flat. But now we are experiencing something new: bank lending is falling. Notice the sharp increase in lending in 2008 as corporations decided to draw down their banks' lines of credit, afraid that the banks might cut back. And with good reason, as banks did exactly that.

So where do banks put their cash and reserves they are not lending? At the Fed and in Treasury debt. If you can leverage capital at ten to one (as banks can) and if you get 2% (for longer-term debt) and if you only have costs of, say, 50 basis points (or 0.5%), you can make a return on equity of 15% with no risk.

And that is what we are seeing. Banks are taking the money the Fed is printing and the government is giving them and putting it back at the Fed. Bank reserves at the Fed are exploding. And they are likely to continue to do so, since bank balance sheets are still deteriorating, especially at smaller and regional banks exposed to commercial real estate loans. Banks own 45% of commercial real estate loans, compared to only 21% of single-family loans. Banks (in general) are going to have to raise capital and reduce their loan portfolios in order to keep within the guidelines for adequate reserve capital. Small wonder that my friend Chris Whalen (one of the real experts on banks) thinks we will see over 400 banks fail in this cycle.

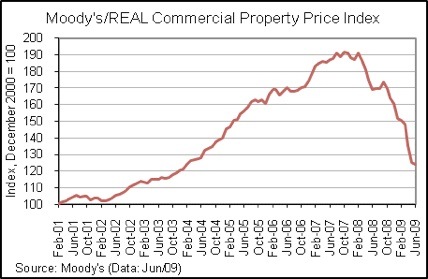

One quick chart to further highlight the problem that banks are facing. I have been writing for several years that commercial real estate loans will be the next shoe to drop. Moody's calculates that commercial real estate prices have dropped 30%. Over a trillion dollars in commercial real estate loans are coming due in the next few years. Banks are going to continue to reduce their loan portfolios in order to deal with the massive write-offs they are going to have to make. And my bet is they put those reserves they are not lending into government debt.

Given that the current Congress is hell bent on massively raising taxes in 2011, we are likely to dip back into recession by then, if not before. Remember, taxes have a multiplier effect of three. That means tax cuts increase GDP (over time) by three times their amount. But tax increases reduce GDP by three times the increase. That will make deficits worse, and unemployment will again start to rise from already high levels. Twenty states have already raised sales taxes, and more are raising other taxes. It is a vicious spiral.

The New Muddle Through Economy

This is not a prescription for a return to normal growth. We are headed for a New Normal that is less than what the market currently believes. Unless the deficit comes under control at some point, we face the real prospect of catching Japanese Disease and suffering yet another lost decade. Can we Muddle Through? We have no choice but to do so. But it will not be fun. It will not be long-term 2% growth and employment going back to 6% any time soon. Can we reverse the course? With a different attitude and leadership in Congress, maybe we can. But it won't happen next year, and it's unlikely in 2011.

I am afraid we will have to put my old friend Muddle Through, as I previously defined him, back in his box for a while. But wait, if my friend at PIMCO, Mohammed El-Erian, can tell us we are going to a "New Normal," then I can decide that we are going to a "New Muddle Through Economy." Just not one as benign as I used to think.

In the end, that is what we will do. We will figure out how to deal with the environment in which we find ourselves. That is what free markets and entrepreneurs do. Things will sort out, but not before we have what could be an even more difficult crisis, which will force us to make hard choices.

As an aside, I am not expecting that we will see the crisis I am thinking of any time soon. We can move along with positive GDP for some time. I am thinking of the longer term, 1-3 years out. We will become complacent. I will get letters telling me I am too pessimistic. Just as I did in late 2006 when I said we would be in a recession by late 2007. But I firmly believe we will see a double-dip recession within another 18 months (at the most). Stock markets drop on average about 40% in a recession. Adjust your portfolios accordingly.

On the Road Again

I am writing tonight from Detroit. Tomorrow I will be in New York watching the Yankees/LA game. I will be the guy in the second row behind home plate in the Dallas Cowboys jacket. I will be on Yahoo Tech Ticker on Monday morning, so you should be able to go to Yahoo and see me later that afternoon. Then Philadelphia on Tuesday, speaking at my partner Steve Blumenthal's CMG conference for investment advisors. They have a very interesting platform of trading advisors. You can see them at http://cmgfunds.net/public/mauldin_questionnaire.asp

I had a great deal of fun at the New Orleans conference, being with old friends and meeting new ones. David Tice (of the Prudent Bear Fund) was an exceptional host for dinner at Emeril's. I was surprised that Karl Rove actually remembered me after nine years. I thoroughly enjoyed spending some quality time with my friend Ron Paul. We share a lot of concerns about the future of the Republic. I was pleasantly surprised by how thoughtful Howard Dean was. And very personable.

I go to Houston on Wednesday, Orlando on Thursday, and then South America on Saturday. I will be doing a lot of writing from hotel rooms, but all in all it will be fun. You have a great week, and remember that in 10 years none of us will look back and want to return to 2009. 2019 will be better than we can possibly imagine. We just have to make sure we all get there!

Time to hit the send button and find an adult beverage. All the best,

Your going to miss the Old Muddle Through analyst,

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.