Is the Fed's Money Pumping Inflationary?

Economics / Economic Theory Sep 17, 2009 - 03:31 AM GMTBy: Frank_Shostak

Given the recent, massive increase in commercial banks' excess reserves, many commentators are of the view that banks will sooner or later start employing these reserves in lending and thus cause an increase in the inflation rate.

Given the recent, massive increase in commercial banks' excess reserves, many commentators are of the view that banks will sooner or later start employing these reserves in lending and thus cause an increase in the inflation rate.

Even former Federal Reserve Chairman Alan Greenspan is alarmed by the massive pumping by the Fed and other central banks. Speaking via satellite to a conference in Mumbai on September 8, 2009, Greenspan said that central banks need to defuse the large increases in their assets.

Even former Federal Reserve Chairman Alan Greenspan is alarmed by the massive pumping by the Fed and other central banks. Speaking via satellite to a conference in Mumbai on September 8, 2009, Greenspan said that central banks need to defuse the large increases in their assets.

He stated that failing to shrink central-bank balance sheets could lead to very high price inflation: "I am not talking 3–5 per cent inflation; I am talking double-digit inflation in the US."

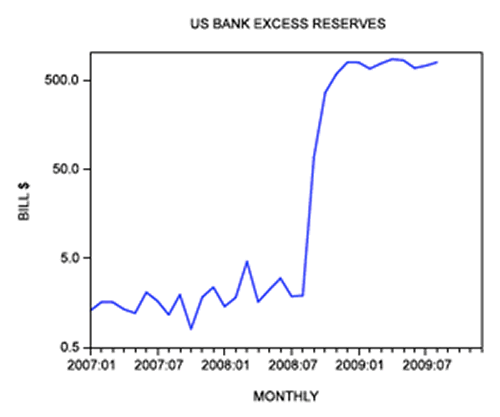

In August 2008, excess reserves stood at $1.9 billion. At the end of August 2009, excess reserves stood at almost $800 billion. By early September 2009, they had reached $823 billion.

Some other commentators hold that banks' decision to sit on their massive surplus cash rather than lend it out raises the likelihood that the Fed's loose monetary policy remains ineffective. They argue that if the policy had worked, banks would have used the pumped reserves to make loans by now.

But a view is emerging from academics, Fed economists, and Fed officials that the massive buildup in reserves points to a great success in Fed monetary policy.[1]

These proponents believe that the critics have overlooked an important change since October 2008 regarding the conduct of the Fed's monetary policy. This change, they claim, has not only saved the US monetary system from a severe calamity, but will also prevent the eruption of the inflationary menace. So what is it all about?

The Old System and Its Limitations

The standard monetary policy tool of the Fed involves setting a target for the federal-funds rate. By varying the target whenever they deem necessary, Fed officials say they can bring the economy onto a path of sustainable economic growth with very little inflation. However, Fed officials like New York Fed President William Dudley, note that various shocks could undermine Fed policy makers' efforts to do this.

Dudley and other proponents of the Fed's massive pumping argue that until October last year, Fed policy makers didn't have adequate means to counter disruptive shocks in a quick and effective way. If the Fed had aggressively pumped money to soften the effect of a given shock, it would have almost instantly pushed the federal-funds rate strongly below the target.

Obviously this would have clashed with the Fed's objective to navigate the economy towards the growth path of economic stability. This means that the Fed couldn't change the size of its balance sheet without causing a large deviation from the federal-funds–rate target.

The New Tool and the Aspirations for It

Based on the work of some academic economists, the current US Federal Reserve chairman, Ben Bernanke, concluded that the link between the central bank balance sheet and the policy rate could be broken by paying banks interest on their reserves (set at the level of the federal-funds–rate target).[2] In this setup, banks would have no incentive to lend below the interest rate that they would receive on their reserves. As a result, the Fed could pump as much reserves as it thought necessary without upsetting the target. It could thus expand its balance sheet without any restraint.

After some persuasion by Bernanke, in October 2008, Congress gave the Federal Reserve the authority to pay this interest.

According to Dudley,

Policymakers now had the capacity to expand the size of the Fed's liquidity facilities and other programs without the threat of compromising the control of monetary policy.

Furthermore, he argues,

This new tool immediately proved enormously helpful. The Fed was able to respond to the deterioration of conditions in the fall of 2008 by sharply increasing the size of its Term Auction Facility program and removing the limits on the size of many of the foreign exchange swap programs. These programs, along with the increased use of the Fed's standing liquidity facilities and the start-up of the Commercial Paper Funding Facility in late October, led to a sharp growth in the Federal Reserve's balance sheet beginning in late September.[3]

This means that Fed policy makers, when required, can assist financial markets whilst maintaining the federal-funds rate at the target.

For instance, if a large bank runs into difficulty, it could pose a threat to the supply of credit and in turn undermine the real economy. Prior to October last year, the Fed would have had difficulties quickly preventing severe side effects without upsetting the federal-funds–rate target. Any support, i.e., pumping money, would push the rate strongly to below the target.

According to proponents like Dudley, in the new setup, the Fed can provide immediate support without upsetting the target.

Indeed, commentators are almost unanimous that the new rapid response of the Fed to various shocks has prevented the US economy from plunging into another Great Depression.

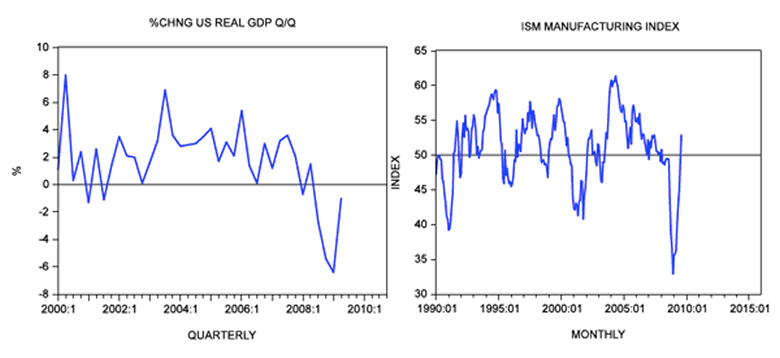

Let us look at some key economic data that seem to indicate that the worst is over: In the second quarter (Q2) of 2009, the annual rate of growth of real GDP jumped to minus 1% from minus 6.4% in Q1. The ISM manufacturing index climbed to 52.9 in August from 48.9 in the month before.

But what about the inflationary threat that all this buildup in bank excess reserves could have at some time in the future?

According to Dudley and other proponents, the new tool will enable the Fed, when the time is right, to raise the interest rate. This will make it less attractive for banks to expand lending and thus fuel the rate of inflation.

It would appear that the new setup not only enables the Fed to quickly neutralize any potential financial crisis but also permits it to counter rapidly and effectively any possible inflationary threats.

Criticism of the Fed and its New Tool

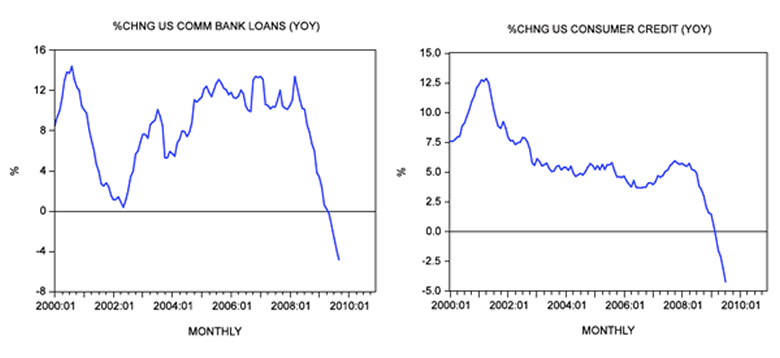

Despite the improvement in some key economic data, one important indicator — commercial bank lending — displays a massive decline. Data for August shows that, year-on-year, lending fell by 3.8% after declining by 2.6% in July. (In early September, the rate of growth stood at minus 4.9%).

Consumer credit also had a big fall in July — falling year-on-year by 4.2% after declining by 3.1% in June.

If Bernanke has managed to stabilize credit markets, as the media and most financial experts argue, why is lending by banks displaying large declines? According to Bernanke's way of thinking (the financial-accelerator model), such big declines in lending pose a threat to the real economy.

Is It True that the Fed Creates Money?

Some commentators, including Dudley himself, have suggested that the Fed is not actually creating money. They argue that the so-called pumping doesn't amount to the creation of new money but simply to the employment of commercial banks' existing excess reserves.

This means that the Fed borrows the surplus money from the banks and invests it in Treasury bonds. In an interview with CNBC on August 31, 2009, Dudley said,

The excess reserves are funding the purchases of treasuries and agency debt and agency mortgage backed securities. So right now we're basically — essentially borrowing the money at 25 basis points, a quarter of a percent, and investing in assets that are yielding … three and half, four, four and a half, five percent.[4]

Now, if the Fed were borrowing money from banks, one would think that this would be registered in the Fed's balance sheet. So far we haven't seen anything in this regard.

Also, if the Fed were using the banks' surplus cash, it would increase demand deposits in the economy and thus increase the money supply. (Excess reserves are not part of the existing money supply.) For instance, let us say that the Fed uses one million dollars from banks' deposits to buy Treasuries from nonbanks. The Fed writes checks to the sellers of Treasuries. These checks, once deposited, boost the money supply.

Using banks' surplus cash would boost price inflation at some time in the future. After all, the price of a good is the amount of money paid for the good. The more money is available, the more money will be spent per unit of a good (all other things being equal).

Dudley reaches a different conclusion because he holds that inflation is driven by only two variables: inflation expectations and the degree of pressure on resources. He mentions nothing about money. Somehow in Dudley's world, prices are not related to money.

But is it valid to argue that the Fed borrows money to fund its activities?

The US central bank is the only institution permitted by law to print money. Now if any individual had such a license, would he ever consider borrowing money? The Fed pays for the assets it acquires by writing a check on itself — i.e., creating money "out of thin air."

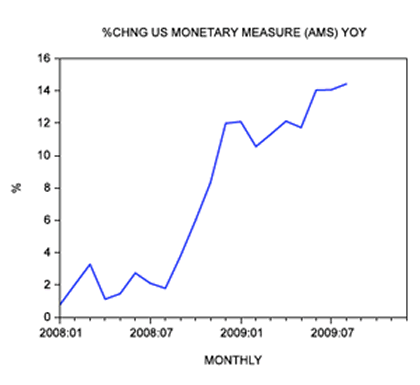

If the Fed's pumping is not inflationary, as Dudley and other commentators argue, why is the growth momentum of the money supply exploding? The yearly rate of growth of our monetary measure AMS jumped from 0.8% in August last year to above 14% in August this year. After a time lag, this explosive growth is going to manifest in the prices of goods and services.

Is There a Link Between the Size of Excess Reserves and Bank Lending?

Despite the increase in excess bank reserves, Dudley and other proponents are of the view that there is no need to be alarmed. In fact, they argue that the textbook economics model, wherein the Fed injects reserves into the banking system and banks then amplify the injection through lending, doesn't apply in reality.

According to Dudley,

If banks want to expand credit and that drives up the demand for reserves, the Fed automatically meets that demand in its conduct of monetary policy. In terms of the ability to expand credit rapidly, it makes no difference whether the banks have lots of excess reserves or not.[5]

Superficially, it does make sense to conclude that central bank policies are of a passive nature: the central bank just aims at keeping the money market in balance. In reality, without the central bank being active, it would be impossible for banks to expand lending, i.e., set in motion the creation of credit out of thin air.

Let us say that banks are experiencing an increase in demand for loans. Also, let us assume that the pool of loanable funds is unchanged. According to Dudley, banks will oblige this increase. The demand-deposit accounts of the new borrowers will then increase. Obviously, the new deposits are likely to be employed in various transactions.

After some time elapses, banks will be required to clear their checks; and this is where problems will occur.

Some banks will find that to clear checks they are forced to either sell assets or borrow the money from other banks (remember that the pool of loanable funds stays unchanged). We suggest that all this will put upward pressure on money-market interest rates, and in turn on the entire interest-rate structure. It might also put at risk the survival of some of the banks.

To prevent the overnight interest rate from rising above the interest-rate target, the central bank will be forced to pump money. However, by doing so it will, so to speak, endorse the expansion of credit.

Surely, this accommodation cannot be labeled as passive; it is very much active. To protect the interest-rate target, the central bank is forced to pump money. So the conceptual outcome as depicted by the textbook model remains intact. The only difference is that banks initiate the lending process, which is then accommodated by the central bank, rather than vice versa.

Without the central bank pumping, banks would have difficulty engaging in an expansion of credit. Any attempt at such an expansion would run the risk of going "belly up."

Furthermore, if, as Dudley says, it makes no difference for lending activity how much excess reserves banks have, why was the Fed pumping all that cash into the banking system? Clearly the idea was to enable banks to continue expanding credit.

We also suggest that paying interest on bank reserves is not going to stop banks from expanding credit, as argued by Dudley and others. After all, there are always opportunities to lend money at much higher interest rates than the federal-funds rate.

We can thus conclude that the massive increase in banks' excess reserves is a potential threat for an explosive credit creation some time in the future. Contrary to popular thinking, we suggest that the new setup, which gives the Fed total freedom to pump money, can only destabilize the financial system and the economy. By responding to every shock that in Bernanke's theory could lead to a potential disaster, the Fed is going to severely damage the pool of real savings.

Since lending is currently in free fall, the pool of real savings may already be in serious trouble. If this is the case, then the Fed's pumping is unlikely to revive the credit markets anytime soon. Remember that the essence of lending is real savings and not money as such. It is real savings that imposes restrictions on banks' ability to lend.

In addition to the extremely loose fiscal policy of the Obama administration, any further monetary pumping runs the risk of inflicting more damage on the formation of real savings. Consequently, it can only paralyze the US economy.

Conclusions

Against the background of a massive increase in US banks' excess reserves, we are of the view that some time in the future, banks will start employing these reserves in lending. Such lending runs the risk of igniting strong increases in the prices of goods and services.

Also, the Fed's present monetary policy appears to be ineffective. Despite massive pumping by the US central bank, commercial bank lending displays sharp declines.

However, an emerging view in support of the Fed's recent policy actions holds that critics have overlooked an important tool that the Fed's policy makers now have: paying interest on banks' reserves.

The proponents of this new ability say that the Fed can now rapidly counter any possible shocks that threaten to destabilize the economy, without compromising the macro goals of price stability and full employment. They believe that the new setup has prevented the US economy from plunging into another Great Depression. They are also of the view that it not only enables the Fed to counter various shocks, but also permits a rapid counterattack on inflation.

We suggest that what matters for price inflation is money supply; for the time being, that displays a very strong increase. We also suggest that the Fed's new ability to respond rapidly to any perceived threat is likely to produce very reckless monetary policy, which will destabilize the economy.

Frank Shostak is an adjunct scholar of the Mises Institute and a frequent contributor to Mises.org. He is chief economist of M.F. Global. Send him mail. See Frank Shostak's article archives. Comment on the blog.![]()

Notes

[1] Todd Keister and James McAndrews, "Why Are Banks Holding So Many Excess Reserves?" Federal Reserve of New York Staff Reports, July 2009. Also see Ricardo Reis, "Interpreting the Unconventional US Monetary Policy of 2007–09," Columbia University August 2009, Brookings conference draft.

[2] Marvin Goodfriend, "Interest on Reserves and Monetary Policy," Federal Reserve Bank of New York, April 2001.

[3] William C. Dudley, "The Economic Outlook and the Fed's Balance Sheet: The Issue of 'How' versus 'When,'" Federal Reserve Bank of New York, July 29, 2009.

[4] CNBC Transcript, "Exclusive Interview with William Dudley," August 31, 2009.

[5] Dudley, "The Economic Outlook."

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.