Quantitative Easing Fuelled Stock Market Recovery

Stock-Markets / Quantitative Easing Sep 16, 2009 - 07:32 PM GMTBy: Mike_Whitney

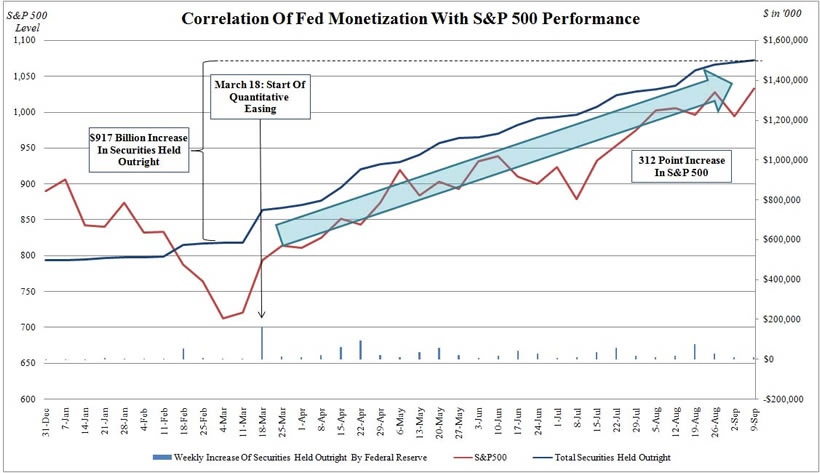

We keep hearing that "The worst is behind us", but the spin doesn't square with the facts. Sure the stock market has done well, but scratch the surface and you'll find that things are not as what they seem. Zero hedge--which is quickly becoming the "go-to" market-update spot on the Internet--recently posted an eye-popping chart which traces the Fed's monetization programs (Quantitative Easing) with the 6-month surge in the S&P 500.

We keep hearing that "The worst is behind us", but the spin doesn't square with the facts. Sure the stock market has done well, but scratch the surface and you'll find that things are not as what they seem. Zero hedge--which is quickly becoming the "go-to" market-update spot on the Internet--recently posted an eye-popping chart which traces the Fed's monetization programs (Quantitative Easing) with the 6-month surge in the S&P 500.

The $917 billion increase in securities held outright equals the Fed's $1 trillion increase to its balance sheet. In other words, the liquidity from the Fed is following the exact same trajectory as stocks, a sure sign that the market is being manipulated. Surprisingly, traders seem to know that the Fed is goosing the market and have just shrugged it off as "business as usual". Go figure? Perhaps it pays to take a philosophical approach to market rigging. Who needs the gray hair anyway? The result, however, has been that short-sellers (traders betting the market will go down) who have placed their bets according to (weak) fundamentals, have gotten clobbered. They appear to be the last holdouts who still place their faith in the unimpaired operation of the free market. (Right) Here's how former hedge fund manager Andy Kessler sums it up in a recent Wall Street Journal article, "The Bernanke Market". Here's a clip:

"By buying U.S. Treasuries and mortgages to increase the monetary base by $1 trillion, Fed Chairman Ben Bernanke didn't put money directly into the stock market but he didn't have to. With nowhere else to go, except maybe commodities, inflows into the stock market have been on a tear. Stock and bond funds saw net inflows of close to $150 billion since January. The dollars he cranked out didn't go into the hard economy, but instead into tradable assets. In other words, Ben Bernanke has been the market."

So, the Fed has given a boost to stocks while keeping the bond market priced for deflation. That's quite a trick. One market is flashing "recovery" while the other is signaling "contraction". Bernanke has worked this miracle, by simply changing the definition of "indirect bidders" (which used to mean "foreign buyers" of US Treasuries) to mean just about anyone-anywhere. Here's an explanation of this latest bit of chicanery from the Wall Street Journal in June:

"The sudden increase in demand by foreign buyers for Treasuries, hailed as proof that the world's central banks are still willing to help absorb the avalanche of supply, mightn't be all that it seems.

“When the government sells bonds, traders typically look at a group of buyers called indirect bidders, which includes foreign central banks, to divine overseas demand for U.S. debt. That demand has been rising recently, giving comfort to investors that foreign buyers will continue to finance the U.S.'s budget deficit.

“But in a little-noticed switch on June 1, the Treasury changed the way it accounts for indirect bids, putting more buyers under that umbrella and boosting the portion of recent Treasury sales that the market perceived were being bought by foreigners." ("Is foreign Demand as Solid as it Looks, Min zeng)

Pretty clever, eh? So, if the Treasury doesn't want dupes like us to know when foreign demand drops off a cliff, they just twist the definitions to meet their needs. My guess is that the Fed is building excess bank reserves (nearly $1 trillion in the last year alone) with the tacit understanding that the banks will return the favor by purchasing Uncle Sam's sovereign debt. It's all very confusing and circular, in keeping with Bernanke's stated commitment to "transparency". What a laugh. The good news is that the trillions in government paper probably won't increase inflation until the economy begins to improve and the slack in capacity is reduced. Then we can expect to get walloped with hyperinflation. But that could be years off. For the foreseeable future, it's all about deflation.

No matter how you look at it, the economy is on the ropes. Yes, there should be a rebound in the next few quarters, but once the stimulus wears off, its back to the doldrums. According to David Rosenberg of Gluskin Sheff, "All the growth we are seeing globally this year is due to fiscal stimulus.... For 2010, the government’s share of global growth, by our estimates, will be 80%. In other words, there are still very few signs that organic private sector activity is stirring."

The question is, how long can the Obama administration write checks on an account that's overdrawn by $11 trillion (The National debt) before the foreign appetite for US Treasuries wanes and we have a sovereign debt crisis? If the Fed is faking sales of Treasuries to conceal the damage--as I expect it is--we could see the dollar plunge to $2 per euro by the middle of 2010. Imagine pulling up to the gas pump and paying $6.50 per gallon. Ouch! That should be revive the economy.

For the next year or so, the demon we face is deflation; a severe contraction exacerbated by household deleveraging and massive financial sector defaults. The Fed's money-printing operations just can't keep pace with capital-hole that continues to expand from delinquencies, foreclosures, and failed loans. Workers have seen their credit lines cut and their hours reduced, households are $3 trillion above trend in their debt-to-equity ratio, and unemployment is soaring. Industry analysts expect a $1.5 trillion cut-back in credit card spending. That's why Bernanke is firehosing the whole financial system with low interest liquidity, to stimulate speculation and reverse the effects of a slumping economy.

Here's a clip from an article in the UK Telegraph:

"Both bank credit and the M3 money supply in the United States have been contracting at rates comparable to the onset of the Great Depression since early summer, raising fears of a double-dip recession in 2010 and a slide into debt-deflation...

Similar concerns have been raised by David Rosenberg, chief strategist at Gluskin Sheff, who said that over the four weeks up to August 24, bank credit shrank at an "epic" 9pc annual pace, the M2 money supply shrank at 12.2pc and M1 shrank at 6.5pc.

"For the first time in the post-WW2 [Second World War] era, we have deflation in credit, wages and rents and, from our lens, this is a toxic brew," he said. (Ambrose Evans-Pritchard, "US credit shrinks at Great Depression rate prompting fears of double-dip recession", UK Telegraph)

The Fed has pumped up bank reserves, but the velocity of money has sputtered to a standstill. There won't be an uptick in economic activity until consumers reduce their debt-load, rebalance their personal accounts and find jobs. That's a long way off, which is why San Francisco Fed chief Janet Yellen sounded more like Nouriel Roubini in this week's presentation "The Outlook for Recovery in the U.S. Economy" in S.F.:

"With slack likely to persist for years, it seems likely that core inflation will move even lower, departing yet farther from our price stability objective. From a monetary policy point of view, the landscape will continue to present challenges. We face an economy with substantial slack, prospects for only moderate growth, and low and declining inflation. With our policy rate already as low as it can go, it’s no wonder that the FOMC’s last statement indicated that “economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period.” I can assure you that we will be ready, willing, and able to tighten policy when it’s necessary to maintain price stability. But, until that time comes, we need to defend our price stability goal on the low side and promote full employment."

That's from the horse's mouth. Recovery? What recovery?

The consumer is maxed out, private sector activity is in the tank, and government stimulus is the only thing keeping the economy off the meat-wagon. Bernanke might not admit it, but the economy is sinking into post-bubble malaise.

zero hedge chart http://www.zerohedge.com/..

By Mike Whitney

Email: fergiewhitney@msn.com

Mike is a well respected freelance writer living in Washington state, interested in politics and economics from a libertarian perspective.

Mike Whitney Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.