Financial Stocks on Tsunami Watch

Stock-Markets / Banking Stocks Sep 02, 2009 - 02:15 AM GMTBy: David_Urban

After seeing quite a large rally from the March lows the market appears to be extended and indicators (stocks above 200 day moving average, market PE, bullish/bearish %'s) are signaling some rough seas ahead. While stock could conceivably move higher there are a few reasons why I am bearish at the present time.

After seeing quite a large rally from the March lows the market appears to be extended and indicators (stocks above 200 day moving average, market PE, bullish/bearish %'s) are signaling some rough seas ahead. While stock could conceivably move higher there are a few reasons why I am bearish at the present time.

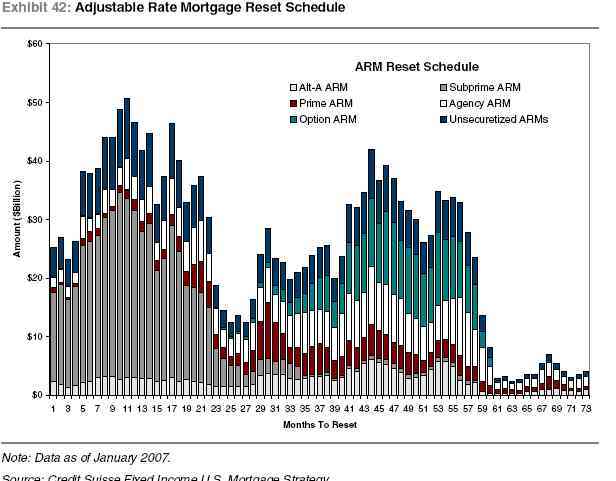

Harkening back to 2007, I would like to give credit and thanks to Credit Suisse for the following graph.

As one can see the initial tsunami of bad loans has receded and financial stocks have been licking their wounds and repairing their balance sheets but we are at the beginning of the second wave. This second wave of option reset mortgages will do more damage because of the already weakened state of banks.

The relaxing of mark to market rules has helped repair balance sheets but there will continue to be problems throughout 2010 and into 2011 until the 2nd wave of resets recede.

As the resets continue, non-performing loans continue to rise, causing additional strain on an already weakened banking sector. It is unlikely that we will see a significant drop off in non-performing loans until the bulk of the option resets are completed.

Bank failures continue on a weekly basis with the problems being felt mainly by small and medium sized institutions. Some larger weakened institutions have succumbed to the pressure as well. Recent comments that the FDIC may need additional capital should sound a warning bell across the financial space.

While the housing data has been bullish due to buyers assistance programs, one needs to keep in mind that the reported figures are month-over-month data, not year-over-year. As we get into the fall and winter months the MoM figures will decrease as seasonal patterns take place.

Housing inventories continue at a high level, with many homes being taken off market and rented until the selling climate improves. As we continue through the resets, it is likely that inventories stay high until the potential overhang from option and agency ARM's clears. Any spurt in new home construction will slow the housing inventories from being worked off in a timely manner.

Retail sales numbers continue to be disappointing, although we are entering a period where comparisons will be much easier. The year over year data shows a 9.4% decline in June and an 8.3% decline in July. Again the YoY data is more telling than the MoM data.

High levels of unemployment will constrain spending and GDP growth into 2010 and later. Government stimulus programs will provide the necessary counterbalance to weakness in consumer spending helping to guide the economy through this difficult period.

This is not an approval for the governments polices but one needs to note that a similar path is followed in every recession. The authors problem lies in the wasteful programs and high deficit levels that state and federal governments carried coming into the recession which only exacerbates the problem going forward. Spending that is targeted at areas to provide future growth is preferred over the construction of dog parks.

So while global economies are likely to come out of the recession without much problem (Japan will be an exception) GDP growth in the US is likely to be below normal levels.

Inventory restocking will give a bump to GDP growth in the coming quarter as will government stimulus programs. This combination will set the stage for renewed consumer and business confidence in the coming years but first we will need to get through the a possible double dip recession in 2010.

So while the market itself may move higher I see better value and higher upsides in the precious metals and agriculture sectors where there are some very interesting values globally. Quite often the best values are off the beaten path.

By David Urban

Communications are intended solely for informational purposes. Statements made should not be construed as an endorsement, either expressed or implied. This article and the author is not responsible for typographic errors or other inaccuracies in the content. This article may not be reproduced without credit or permission from the author. We believe the information contained herein to be accurate and reliable. However, errors may occasionally occur. Therefore, all information and materials are provided "AS IS" without any warranty of any kind. Past results are not indicative of future results.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN THE STOCK, BOND, AND DERIVATIVE MARKETS. WHEN CONSIDERING ANY TYPE OF INVESTMENT, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

Before making any type of investment, one should consult with an investment professional to consider whether the investment is appropriate for the individuals risk profile. This is not intended to be investment advice or a solicitation to purchase any of the securities listed here. I will not be held liable or responsible for any losses or damages, monetary or otherwise that result from the content of this article.

David Urban Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.