What PIMCO's Bill Gross Doesn’t Want You to Know (Part 1)

Interest-Rates / US Bonds Jun 27, 2009 - 06:25 AM GMTBy: Mike_Stathis

I’ve sat by now for about ten years now, waiting for someone from the financial industry to point out what I am about to reveal. I meant to write about this but I kept forgetting.

I’ve sat by now for about ten years now, waiting for someone from the financial industry to point out what I am about to reveal. I meant to write about this but I kept forgetting.

I have to conclude that no one has written or spoken in the media about what I’m about to reveal because many simply are unaware of what I deem to be obvious. Others don’t want to go against their colleagues in the financial industry. But what these guys seem to forget is that their first loyalty should lie with the investment public.

I feel the need to point out what I feel to be very disturbing facts behind PIMCO’s Total Return Fund. In short, I feel the fees charged are excessive by any reasonable measure. And when you consider the size of the fund (being the largest mutual fund in the world) this should be further evidence that you can’t win with Wall Street.

The scary part is that you have some really large investors in this fund; investors that are supposed to be “sophisticated;” even investors with a fiduciary responsibility to their clients.

First of all, let me dish out my own personal opinion. Very rarely would I deem an investment in open-end investment-grade bond fund to be prudent from the standpoint of the cost structure. And you certainly won’t receive the type of asset and risk management services relative to the fees charged.

Support for my view can be found upon examination of PIMCO’s Total Return Fund, managed by Mr. Bill Gross, the highly touted bond fund manager. Historically, this fund has focused on managing mainly AAA and other investment grade bonds.

Generally speaking, managing investment grade bonds isn’t something particularly difficult for a professional bond manager to do. Granted, during the current economic catastrophe, this task is a bit more challenging. But what we are experiencing is extraordinarily rare. Gross’ fund has been charging excessive fees for many years. And the SEC allows it. Gross is by no means alone, as other bond fund managers do the same.

Generally speaking, managing investment grade bonds isn’t something particularly difficult for a professional bond manager to do. Granted, during the current economic catastrophe, this task is a bit more challenging. But what we are experiencing is extraordinarily rare. Gross’ fund has been charging excessive fees for many years. And the SEC allows it. Gross is by no means alone, as other bond fund managers do the same.

It’s not an issue with Gross. The problem is with the mutual fund industry itself.

Now, the Total Return fund has some risky bonds as well, but the majority are investment grade. You can imagine the temptation to delve into more of these risky “junk” bonds when interest rates are low, so as to increase the returns. As such, Gross does this, as it is listed as a minor part of the investment strategy.

But again, Total Return is primarily for investment-grade bonds. The problem is that under normal circumstances, investment-grade bonds have very limited upside potential, unlike non-investment grade or junk bonds, which can pay off big. Of course, investment in junk bonds are highly risky and don’t offer the liquidity of investment-grade bonds.

The point is that due to the limited upside of investment-grade bond funds (since your returns come mainly in the form of dividends), the total fees should be very minimal in order to comply with any standards set forth by the financial regulatory authorities.

Let’s have a look at one of the many share classes of the Total Return Fund. The total (disclosed) fees are close to 2% (management and 12b-1 fees). Of course, these fees would vary depending on which share class you bought.

But there are additional fees as well, such as auditing fees, record-keeping fees, ticket charges and many others. But we do not know what these amount to because they’re not reported. You can be assured that once all fees have been accounted for, they come in at well over 2% of your investment assets annually.

In the end, the only real way to determine how much you’ve been nailed in fees is to look at your account and subtract what you started with from the current balance and do some simple math.

Of course, if you contribute regularly to your funds, it’s virtually impossible to determine these calculations. Mutual fund companies not only know this, they intentionally set it up this way (i.e. fail to provide you with complete and clear disclosure) so you won’t realize how terrible the funds are and how high the total fees really are.

Chances are, when all fees have been adequately accounted for, you’ll be looking at close to 4% for the average equity mutual fund, no or no-load. This, my friends is one of the main reasons why most mutual funds cannot bet their appropriate index. This Random Walk theory is not the reason. In my opinion, Random Walk is a bunch of trash.

The reality is that the SEC should require a detailed and clear statement of fees so investors can determine if they are getting their money’s worth. I advise you not to hold your breath. I’ve specifically addressed these issues with SEC attorneys, and their response has made it clear to me where their loyalty lies.

Let’s glance at the fees for the three most common share classes of Total Return. The total expense ratio is the combination of 12b-1, management fees and other fees. Once again, there are several other fees that are not included in the expense ratio.

PIMCO Total Return A PTTAX

Management Fee 0.25%

Total Expense Ratio:0.90%

Max 12b1 Fee:0.25%

Front End Sales Load:3.75%

YTD Performance as of 04/17/2009 2.08%

1 Year* 2.50%

3 Year* 6.16%

5 Year* 4.43%

10 Year* 5.94%

PIMCO Total Return B PTTBX

Management Fee 0.25%

Total Expense Ratio:1.65%

Max 12b1 Fee:1.00%

Max Front End Sales Load:0.00%

Max Deferred Sales Load:3.50%

YTD Performance as of 04/17/2009 1.87%

1 Year* 1.73%

3 Year* 5.37%

5 Year* 3.65%

10 Year* 5.15%

PIMCO Total Return C PTTCX

Management Fee 0.25%

Total Expense Ratio:1.65%

Max 12b1 Fee:1.00%

Max Front End Sales Load:0.00%

Max Deferred Sales Load:1.00%

YTD Performance as of 04/17/2009 1.87%

1 Year* 1.73%

3 Year* 5.37%

5 Year* 3.65%

10 Year* 5.15%

As you can see, your fees will vary depending on what type of shares you buy and how long you own the fund (due to exit penalties for B shares). I won’t go into the fact that the entire mutual fund industry fee structure needs to be sliced down significantly. The growing ETF industry is helping to take care of that. The point here is that from a comparison basis, the fees charged by bond mutual funds are excessive even when compared to industry standards for equity-based mutual funds.

At least with equity funds, you have the potential to earn double-digit returns. With bond funds, it’s a much different story; that is, unless you’re talking about funds that manage primarily junk bonds.

If we did consider junk bond funds, you should note that the expertise and effort required would be considered much more than for investment-grade funds. But the risk would also be much higher, while the liquidity would be significantly lower.

In contrast, for investment-grade bond, your returns are pretty much constricted to a small range, namely around 5 to 7%, depending on interest rates and how well the bonds are managed.

Ask yourself the following question. With disclosed fees (not total fees) of over 1.5% and net annual returns of around 5-6% (depending on the time span under consideration), doesn’t this seem like a big rip-off? To me it does, especially when you can buy the bonds yourself for as low as a $50 and get 6-8% annual returns.

If you think the SEC would do anything about this rip-off, think again. As mentioned, I’ve made several formal complaints. Their response? “Fees and returns are listed in the prospectus.”

In other words, disclosure is suitable for screwing, you despite the fact that this so-called disclosure is not clear. The fact is that it is very difficult if not impossible for the average investor to truly comprehend the fund stat sheet much less decipher the prospectus. I cannot even determine the total fees based upon the information in the prospectus.

Part of the problem is that the mutual fund industry is allowed to report very confusing and select data which most investors do not fully understand. Ask yourself why these fees aren’t clearly communicated to investors? Then ask yourself just who you think the SEC works for.

Let’s have a look at some additional data. For the A shares (PTTAX), an initial $10,000 investment would rack up $1509, or over 15% in fees (not counting ticket charges) over a 10-year period (Yahoo! Finance). That’s the amount sliced from your gross returns; your “total return” if you will, before capital gains taxes of course. So already, you are paying over 1.6% each year for Mr. Gross to manage investment-grade bonds have typically netted 6% individually.

As data shows, the fund has returned 4.90% annually over the past five years and 5.94% over the past 10 years. But wait a second. What about the fees?

Well, a couple of years ago, the SEC finally started requiring returns to be reported after adjusting for fees. But they did not require funds to also report the gross returns before fees. So you need to do some simple math to determine how much you are really being charged.

So, take the annual returns reported and divide that number by the total fees; in the case of the A shares, 1.4%. Looking at the 10-year returns, simple math yields around 24%. That is, PIMCO is getting 24% of the annual returns in fees. The fees are even higher if you use the 5-year returns.

But you still haven’t accounted for taxes. Note that while Fannie and Freddie are tax-exempt, when these bonds are sold (as often happens during the management process) you’re responsible for capital gains taxes.

But we still aren’t done. Once again, there are several fees that aren’t disclosed, so you should assume the total fees are higher. I would estimate the total fees to be 30-35% of gross returns. Wow. That sounds like a damn good business to be in (if you want to screw people).

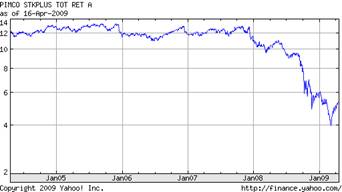

The chart below should give you a pretty good idea about the Total Return fund. Note that the price chart is of the NAV and does not adjust for fees, so it looks a lot better than reality.

For the B shares, we don’t see much difference. A little shifting here and there with fees and we basically get the same situation. Management and 12b-1 fees are 1.65% in total. The deferred sales charge is 3.50% if you exit prior to (typically) five years.

For the B shares, we don’t see much difference. A little shifting here and there with fees and we basically get the same situation. Management and 12b-1 fees are 1.65% in total. The deferred sales charge is 3.50% if you exit prior to (typically) five years.

You see, that’s why the annual fees are higher than with A shares. If you exit before five years, you get dinged with an additional 3.50%. They plan to get big fees from you either way. If you stay in the fund for at least 5 years (or the specific requirement which in some cases is 6 years), they’re nail you with a higher expense ratio than with A shares because the A shares nail you with an upfront sales charge.

To Be Continued

By Mike Stathis

www.avaresearch.com

Copyright © 2009. All Rights Reserved. Mike Stathis.

Mike Stathis is the Managing Principal of Apex Venture Advisors , a business and investment intelligence firm serving the needs of venture firms, corporations and hedge funds on a variety of projects. Mike's work in the private markets includes valuation analysis, deal structuring, and business strategy. In the public markets he has assisted hedge funds with investment strategy, valuation analysis, market forecasting, risk management, and distressed securities analysis. Prior to Apex Advisors, Mike worked at UBS and Bear Stearns, focusing on asset management and merchant banking.

The accuracy of his predictions and insights detailed in the 2006 release of America's Financial Apocalypse and Cashing in on the Real Estate Bubble have positioned him as one of America's most insightful and creative financial minds. These books serve as proof that he remains well ahead of the curve, as he continues to position his clients with a unique competitive advantage. His first book, The Startup Company Bible for Entrepreneurs has become required reading for high-tech entrepreneurs, and is used in several business schools as a required text for completion of the MBA program.

Restrictions Against Reproduction: No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the copyright owner and the Publisher. These articles and commentaries cannot be reposted or used in any publications for which there is any revenue generated directly or indirectly. These articles cannot be used to enhance the viewer appeal of any website, including any ad revenue on the website, other than those sites for which specific written permission has been granted. Any such violations are unlawful and violators will be prosecuted in accordance with these laws.

Requests to the Publisher for permission or further information should be sent to info@apexva.com

Books Published

"America's Financial Apocalypse" (Condensed Version) http://www.amazon.com/...

"Cashing in on the Real Estate Bubble" http://www.amazon.com/...

"The Startup Company Bible for Entrepreneurs" http://www.amazon.com...

Disclaimer: All investment commentaries and recommendations herein have been presented for educational purposes, are generic and not meant to serve as individual investment advice, and should not be taken as such. Readers should consult their registered financial representative to determine the suitability of all investment strategies discussed. Without a consideration of each investor's financial profile. The investment strategies herein do not apply to 401(k), IRA or any other tax-deferred retirement accounts due to the limitations of these investment vehicles.

Mike Stathis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.