Fear for a Lost Economic Decade

Economics / Great Depression II Jun 16, 2009 - 02:14 AM GMTBy: John_Mauldin

Before we get into this week's Outside the Box, let me give you a few pieces of data that came across my desk this morning, which will help set the stage for the OTB offering. Fitch (the ratings agency), in a downgrade of yet another 543 mortgage-backed securities of 2005-07 vintage, gives us the following side notes: "The home price declines to date have resulted in negative equity for approximately 50% of the remaining performing borrowers in the 2005-2007 vintages. In addition to continued home price deterioration, unemployment has risen significantly since the third quarter of last year, particularly in California where the unemployment rate has jumped from 7.8% to 11%...

Before we get into this week's Outside the Box, let me give you a few pieces of data that came across my desk this morning, which will help set the stage for the OTB offering. Fitch (the ratings agency), in a downgrade of yet another 543 mortgage-backed securities of 2005-07 vintage, gives us the following side notes: "The home price declines to date have resulted in negative equity for approximately 50% of the remaining performing borrowers in the 2005-2007 vintages. In addition to continued home price deterioration, unemployment has risen significantly since the third quarter of last year, particularly in California where the unemployment rate has jumped from 7.8% to 11%...

The projected losses also reflect an assumption that from the first quarter of 2009, home prices will fall an additional 12.5% nationally and 36% in California, with home prices not exhibiting stability until the second half of 2010. To date, national home prices have declined by 27%. Fitch Rating's revised peak-to-trough expectation is for prices to decline by 36% from the peak price achieved in mid-2006. The additional 9% decline represents a 12.5% decline from today's levels."

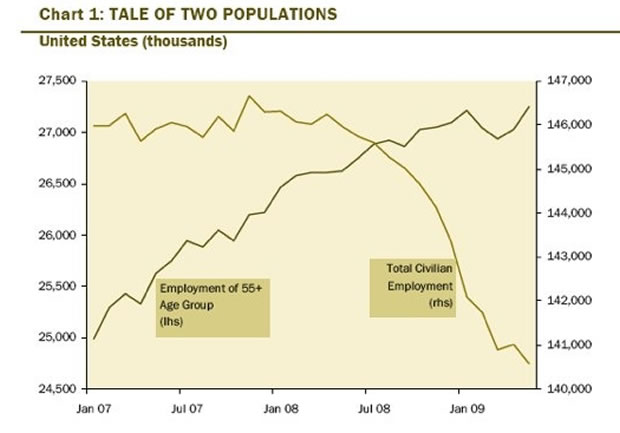

So, what does an aging population do that has seen its retirement nest egg in the form of housing and stocks go literally nowhere for 12 years? You go back to work! David Rosenberg, now with Gluskin Sheff, offers us this insight:

"What really struck us in the employment report of a few weeks ago was the fact that the only segment of the population that is gaining jobs is the 55+ age category. This group gained 224,000 net new jobs in May while the rest of the population lost 661,000. In fact, over the last year, those folks 55 and up garnered 630,000 jobs whereas the other age categories collectively lost over six million positions. This is epic." [See chart below.]

"Moreover, the number of 55 year olds and up who have two jobs or more has risen 1.1% in the last year, the only age cohort to have managed to gain any multiple jobs at all. Remarkable. These folks have seen their wealth get destroyed by two bubble-busts less than seven years apart — the Nasdaq nest egg back in 2001 and the 5,000 square foot McMansion in 2007. Both bubbles ended in tears ... and so close together."

With that as backdrop, what are we to make of the prospects for recovery over the next decade? Not much, if we listen to Professor Paul Krugman of Princeton. He suggests that the developed world could be entering a lost decade, just like Japan after their crash. Let me quickly point out that I routinely disagree with Krugman on a large number of issues. And I usually know why I disagree and believe his policy suggestions are wrong.

That being said, one purpose of Outside the Box is to look at ideas and thinkers that we may not always agree with. Krugman certainly qualifies on that front for me. However, it must be admitted that he is a very smart man. Further, his thinking is important, because it somewhat reflects the thinking of that part of the establishment that is in charge of the Fed and the Treasury. And while we are not getting gloomy long-term forecasts from either the Fed or the Treasury, I find it remarkable that Krugman is less sanguine than his peers. And there is much (certainly not all!) within this interview that I find myself in surprising agreement with. This one made me think as I read and reread it.

If he is correct, the rosy recovery assumptions built into the already bloated budget projections are going to be far too optimistic, not just for the US, but throughout Europe as well. Krugman is interviewed very capably by Will Hutton, a veteran writer and economist for the UK Guardian (a bastion of liberal politics). The direct link is http://www.guardian.co.uk/business/2009/jun/14/economics-globalrecession.

Green shoots? Really? I invite you to read and think about what this interview means for the road to recovery. I will take this up more in next Friday's missive. (Note, I did not write a letter last week. There was a new Mauldin grandchild on Friday, and I decided that some things just take precedence.) Have a great week.

John Mauldin, Editor

Fear for a Lost Decade

As analysts and media hailed the tentative emergence of green shoots last week, Nobel Prize-winning economist Paul Krugman caused international shock with a prediction that the world economy would stagnate just as badly, and for just as long, as Japan's did in the 1990s. In an exclusive interview, he talks to Will Hutton about his anxiety for the future.

Will Hutton: You are warning that what happened to Japan could happen to the whole world. Japan's GDP at the end of this year will be no higher than it was in 1992 -- 17 lost years. You are saying that this is an ongoing risk, certainly for the North Atlantic economy – – maybe the world economy.

Will Hutton: You are warning that what happened to Japan could happen to the whole world. Japan's GDP at the end of this year will be no higher than it was in 1992 -- 17 lost years. You are saying that this is an ongoing risk, certainly for the North Atlantic economy – – maybe the world economy.

Paul Krugman: Yes. It's not that the risk of the Japan syndrome has receded very much. The risk of a full, all-out Great Depression – – utter collapse of everything – – has receded a lot in the past few months. But this first year of crisis has been far worse than anything that happened in Japan during the last decade, so in some sense we already have much worse than anything the Japanese went through. The risk for long stagnation is really high.

Paul Krugman: Yes. It's not that the risk of the Japan syndrome has receded very much. The risk of a full, all-out Great Depression – – utter collapse of everything – – has receded a lot in the past few months. But this first year of crisis has been far worse than anything that happened in Japan during the last decade, so in some sense we already have much worse than anything the Japanese went through. The risk for long stagnation is really high.

WH: So what is the heart of your pessimism? The bust banking system? A critic would say: "Hold on, Paul Krugman. Japan is a special case. It had an overblown export sector that had become too large for an American market it had saturated. The yen was very, very overvalued. And this interacted with a credit crunch and bust banking system. Its policy response was consistently behind the curve. That's not the story of the United States or the United Kingdom."

PK: The thing about Japan, as with all of these cases, is how much people claim to know what happened, without having any evidence. What we do know is that recessions normally end everywhere because the monetary authority cuts interest rates a lot, and that gets things moving. And what we know in Japan was that eventually they cut their interest rates to zero and that wasn't enough. And, so far, although we made the cuts faster than they did and cut them all the way to zero, it isn't enough. We've hit that lower bound the same as they did. Now, everything after that is more or less speculation.

For example, were the problems with the Japanese banks the core problem? There are some stories about credit rationing, but they are not overwhelming. Certainly, when we look at the Japanese recovery, there was not a great surge of business investment. There was primarily a surge of exports. But was fixing the banks central to export growth?

In their case, the problems had a lot to do with demography. That made them a natural capital exporter, from older savers, and also made it harder for them to have enough demand. They also had one hell of a bubble in the 1980s and the wreckage left behind by that bubble – – in their case a highly leveraged corporate sector – – was and is a drag on the economy.

The size of the shock to our systems is going to be much bigger than what happened to Japan in the 1990s. They never had a freefall in their economy – – a period when GDP declined by 3%, 4%. It is by no means clear that the underlying differences in the structure of the situation are significant. What we do know is that the zero bound is real. We know that there are situations in which ordinary monetary policy loses all traction. And we know that we're in one now.

WH: So your point is that the crisis in Japan was about excess debt, excess leverage and lack of demand – – reinforced by the fallout from the asset bubble collapsing. They didn't have credit contraction on anything like our scale, but even so, zero interest rates were just unable to turn the economy around.

PK: That's right, that's right.

WH: But an optimist would say that there are signs all around of the traction that you say doesn't exist is working. The stockmarkets in London and Wall Street – – along with most world markets – – are up a solid 20% to 25%. You've got all these improving business confidence indicators. You've got the first signs of the housing market bottoming in both the UK and the United States. This is what the optimists would tell you.

PK: But all of that points to levelling off, rather than an actual recovery. Britain's looking the best among the major European economies because it's got a PMI [purchasing managers' index, a key measure of economic sentiment] that's just above 50. In other words, Britain actually may have stopped contracting – – that's the most positive thing one can say.

Who knows if the stockmarket makes sense or not? It was pricing in the possibility of an apocalypse a few months ago. That possibility seems to have receded, so it makes sense for the markets to come up, but that's not saying that the economy is going to be great. If you do the comparison not with where they were three months ago, but where they were two years ago, then the markets still seem awfully depressed.

I hope I'm wrong but the question you always have to ask is: where do we think that this recovery's going to come from? It's not an easy story to tell.

WH: In your lectures, you drew attention to the importance of stressed balance sheets holding back consumers and business alike in their likely spending ambitions – – and thus dragging back economic activity. Is this going to be a balance-sheet-constrained recovery?

PK: It's probably true that households have been impoverished a lot by the fall of the housing and stock prices. And that it's likely that households, with all of this debt, are going to have trouble spending. And yes, the North Atlantic economy was supported quite a lot by gigantic housing booms. Here in the UK you have had the house price surge without very much construction. Economists have a well-developed theory about how balance-sheet problems can cause financial and economic crises, but we thought of it in terms of third world countries with foreign-currency debt. We didn't realise that there were lots of other ways in which that can happen.

WH: So, one way to think about it is that self-reinforcing financial crises rooted in overstretched, overborrowed companies and governments in less developed countries – – like those in Argentina and Indonesia, which were amazingly destructive in the 1990s and 2000s, but localised – – are now playing out in the developed world?

PK: There are really two stories. One is the Japan-type story where you run out of room to cut interest rates. And the other is the Indonesia- and Argentina-type story where everything falls apart because of balance-sheet problems.

WH: So in a nutshell your story is ...

PK: The "Nipponisation" of the world economy with a bunch of "Argentinafications" playing a role in the acute crisis. But even after those are over, we have the Nipponisation of the world economy. And that's really something.

WH: What was the heart of the Japanese problem? What was at the heart of their 17 years of going nowhere?

PK: Well, my guess is that it was that the balance-sheet problems took a very long time to resolve. And it is difficult to get enough demand in an economy where you have really very adverse demography ...

WH: So, which countries look closest to being Nipponised – – combining balance-sheet problems and ageing populations?

PK: Well, the US doesn't have the same combination. But in Europe, Germany and Italy look comparable. France is better and Europe as a whole is considerably better.

WH: Germany matches Japan to an uncanny degree. You talk about the Nipponisation of the world economy: I'm not so sure. But I would talk about the Nipponisation of Europe via a German economy at its centre in the grip of the same problem – – and that starts to be a global problem.

PK: Germany has huge inadequacy of domestic demand. Their economic recovery in the first seven years of this decade rested on the emergence of gigantic current account surplus.

How is it possible that Germany, which did not have a house price bubble, is having a steeper GDP fall than anyone else in the major economies?

The answer is that they depended upon exporting to the bubble regions of Europe, so they actually got side-swiped by the loss of those exports worse than the bubble regions themselves got hit.

It's Germany on a global scale that is the concern. We worry about the drag on world demand from the global savings coming out of east Asia and the Middle East, but within Europe there's a European savings glut which is coming out of Germany. And it's much bigger relative to the size of the economy.

WH: And on top there is an unique and unaddressed huge potential banking crisis. The Germans pride themselves on their three-legged banking system, but it is incredibly interlinked. The IMF warns that Germany could have to take at least $500bn of writedowns, which its banks have not begun to recognise. German banks hold a trillion dollars – – maybe more – – of maturing collateralised debt obligations that can only be refinanced by crystallising the losses. We've had RBS and you've had Citigroup. Germany's GDP will fall 6% this year – – before the banking crisis has hit it.

PK: Yeah, that's the financial view. Its important to keep track of the financial state of the banks. But one always has to keep track of the real side of the economy, too. It is a hypothesis that the problem is essentially financial. But it is by no means a hypothesis that we know is true.

WH: So even after what we've gone through, you say it's just a hypothesis that the cause of the crisis is financial?

PK: That the cause is primarily financial. Certainly, Lehman and all of that alerted us all. And it did trigger an immediate drop in demand. But the housing bust was going to happen regardless.

The fall in business investment is at least to a large degree a response to excess capacity, which is the result of falling consumer demand and the housing bust. So we don't know.

WH: I think we know more than that. The links between bank capital, loan losses, credit availability and economic activity and asset prices have never been clearer. That was why there was a threat of Depression.

PK: Clearly, re-establishing stability in the financial markets is a necessary condition for recovery. But we're not sure it's sufficient.

WH: That's very scary.

PK: Well, that is part of the reason why I am so depressed.

WH: In one of your lecture charts you seemed to be suggesting that we're 12 months into what you think could be a 36-month period of downturn, albeit at a slower rate.

PK: Easily.

WH: It's quite shocking that you think it will be that severe.

PK: If we measure the 2001 US recession by when the labour market finally started to turn around, it was a 30-month recession. It was really 30 months in before you started to see the unemployment rate come down.

WH: In Britain, there is now a new consensus forming that the government's economic forecasts, which were roundly mocked at the time of the April budget for being wildly optimistic, could be right – – that is, growth will start to resume in 2010, albeit at a very low rate.

PK: Well, the UK has achieved a lot of monetary traction in the way that no one else has through the depreciation of the pound. In effect, you've carried out a successful beggar-my-neighbour devaluation.

WH: So, the United Kingdom might actually get through this in reasonably good shape?

PK: Yeah. That's why I've been watching with an outsider's slight puzzlement, your bizarre political circus.

WH: Darling and Brown deserve more credit than they're given?

PK: If the government can hold off having an election until next year, Labour might well be able to run as "we're the people who brought Britain out of the slump".

WH: So your advice to the Labour Party is: hold steady.

PK: Probably.

WH: Probably?

PK: I don't know enough about the other aspects of politics, but I would guess that the option value is quite high that the economy might actually have turned a corner. That's unique. That's a uniquely British thing. None of the other G7 countries has anything like that.

WH: And that's a combination of our big beggar-our-neighbour devaluation, aggressive monetary policy, successfully recapitalising our banks and our fiscal policy.

PK: There hasn't been very much discretionary fiscal expansion when all's said and done.

WH: Well, there was a £20bn temporary cut in VAT.

PK: Yeah.

WH: Which is non-trivial.

PK: Non-trivial. But not much [other spending], as I understand.

WH: Well, there was bringing forward £3-4bn of capital spending. Perhaps together in a full year the stimulus was 1.5% GDP. Maybe 2% at the outside.

PK: Monetary policy has been more aggressive – – though maybe less than the Fed – – and the depreciation of the pound is a nice thing from a UK point of view.

WH: So you remain committed to the key role of fiscal policy?

PK: Yeah. Fiscal policies are best; certainly something to do to mitigate recession. People say that the Japanese fiscal policy on all that infrastructure was wasted. But it did help sustain the economy and avoid a collapse. Fiscal policy can certainly do that: it gives the credit sector time to rebuild its balance sheets. There's every reason to be expansive around the fiscal side now because even if you're not sure that it provides a long-term solution, avoiding catastrophe is a big thing to do.

WH: If you believe that, is Obama doing enough on fiscal policy?

PK: Well we have a stimulus which is a little over 5% of one year's GDP but some of it is not real – something that was going to happen anyway and not very stimulative. So it's really about 4% of GDP of genuine stimulus, but spread over two and a half years. So, it's actually quite a lot less than what I was arguing for.

WH: So, will it be sufficient?

PK: Well, sufficient to actually restore full employment would probably have to be 5% or more. More than we have would certainly be a good thing. It actually might happen. You know, the buzz I'm getting is that a second-round stimulus might well come on the agenda.

WH: Really? When you say "the buzz you're getting", have you been asked?

PK: Well, it's what you hear from people who talk to people who talk to people.

WH: Who would argue for that? Would it be Larry Summers [director of the US National Economic Council]?

PK: I think Larry. I'm not sure Tim Geithner [US treasury secretary] would be opposed to it. Nor would Chrissie [Christine Romer, director of the Council of Economic Advisers] I'm sure they would be making similar judgements. It is actually a little spooky.

WH: They're all people you know pretty well, who look at the world the same way, use the same tools and framework ...

PK: Yeah. They may be sitting where they are, having some differences. Larry's always more conventional than I am. Sometimes rightly. Sometimes wrongly. But they do operate in the same framework.

WH: How seriously do you take the argument that the growth of public debt on this scale will crowd out the spontaneous amount of growth of corporate and private debt? Is this already happening with the rise in long-term interest rates in the US?

PK: The thing about long-term interest rates is that they are a weighted average of future expected short-term interest rates. Movements in long-term rates are mostly about what people think the short rates are going to be. Look, real rates are barely up at all. What seems to have moved up is the expected rate of inflation, which is still below the Fed target. So it's more like what the markets are doing is reducing their discounting of deflationary catastrophe.

WH: how do you see the politics working out in the States and in the UK now? Your praise of Gordon Brown after the banks in October were recapitalised was front-page news. Are you still as well disposed?

PK: I still think his economic policies have been pretty good. They really kind of lost their nerve on fiscal policy, but I do understand it's harder to do it here. I think the UK economy looks the best in Europe at the moment. I have no position on all of the crazy stuff. But I think the policies are intelligent. The fact of the matter is that Britain did manage to stabilise the banking situation. I'm not ecstatic, but I'm not sure I know what I could have done better.

WH: So where are you on the debate about various shape recoveries? V-shaped? L-shaped ? A W-shaped recovery?

PK: There is a possibility that we get some perk-up as the stimulus dollars start to flow and an almost mechanical bounceback in industrial production as inventories are built up. But then we slide down again. The idea that we sort of bounce along the bottom is all too easy to imagine.

WH: Is it just a story about the right dose of fiscal policy? What structural change would you advocate in the economy, to support recovery?

PK: Financial regulation. Rein in that monster. The huge increase in general private-sector leverage is at the core of how we got so vulnerable. We went for 50 years after the Great Depression without any major financial crises, and that, I think, was because we had a financial sector that didn't let people get as deeply into debt as they have now.

WH: So rein in the financial monster and give a fiscal stimulus. So you would leave the American way of doing capitalism untouched?

PK: I'm not that cosmic in this stuff. But it is true that Gordon Gekko [the anti-hero of Oliver Stone's film Wall Street, motto: Greed is Good] went hand in hand with the wave of financialisation. Corporations got more brutal and fiercer.

WH: But it is all connected. Without the leverage, there would have been no Gordon Gekkos. And leverage meant that predator companies had the firepower to launch contested hostile takeovers. The only way to fend off attack, or to make the sums work after an attack, was for companies to be more brutal and fierce – often breaking the promises to staff and suppliers that kept commitment and trust.

PK: All of that is true. I have a more mundane view about what we do. I just want a stronger welfare state and a little bit more social democracy. And some restoration of the labour movement as a counterweight.

I'm not sure – maybe I'm just not thinking about it deeply enough. I guess I've got the same attitude Keynes had, which was he was looking for almost technical fixes. You're looking for ways to fix the parts that have gone wrong rather than replace the whole thing.

You know the human cost of this crisis is vastly worse in America than it is on this side of the Atlantic. So this is a good time to push for a better US social safety net too.

WH: And lastly – you've been critical about Obama. Your view now?

PK: I'm increasingly happy with him. I was unhappy; I think they could have gotten a bigger stimulus coming out the gate. But they've become more forceful. I would have been more aggressive on the banks; we'll see if we need to re-fight that battle later on.

Healthcare is looking really good. I'm getting increasingly optimistic on healthcare reform. Climate change looks like it's going to happen. So my odds that this will in fact be the kind of New Deal I was hoping for are rising. I had my scepticism, but he is smart. He's impressive. And it is such a relief to have somebody whom you can respect in the White House.

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.