The Deflation/ Depression Economic Recovery Plan

Economics / Recession 2008 - 2010 May 29, 2009 - 03:40 AM GMTBy: Mick_Phoenix

Well, well, well. Here at the Agency we have spent a couple of years waiting for the US economic establishment to go public with the Deflation / Depression Recovery Plan, what we call The Eggertsson Theory and this week we got it.

Well, well, well. Here at the Agency we have spent a couple of years waiting for the US economic establishment to go public with the Deflation / Depression Recovery Plan, what we call The Eggertsson Theory and this week we got it.

Lucky subscribers can now take solace in the fact that the author was right and the small quarterly payments were worth the effort. I can take great pleasure in saying "I told you so", not because I want to inflate my ego but because I know some people took note of what I said and prepared their portfolio accordingly. That gives me a warm feeling inside, unlike Gordon Brown I didn't "save the world" but I did help some individuals.

Enough of the touchy feely stuff and back to the subject at hand, the public announcement that you, the public, will accept the threat of inflation because it's "less painful" than any other solution.

- "May 19 (Bloomberg, Rich Miller) -- What the U.S. economy may need is a dose of good old-fashioned inflation.

So say economists including Gregory Mankiw, former White House adviser, and Kenneth Rogoff, who was chief economist at the International Monetary Fund. They argue that a looser rein on inflation would make it easier for debt-strapped consumers and governments to meet their obligations. It might also help the economy by encouraging Americans to spend now rather than later when prices go up. "I'm advocating 6 percent inflation for at least a couple of years," says Rogoff, 56, who's now a professor at Harvard University. "It would ameliorate the debt bomb and help us work through the deleveraging process." "Anybody who has been a central banker wouldn't want to see inflation expectations become unhinged," says Marvin Goodfriend, a former official at the Federal Reserve Bank of Richmond.

-

"The Fed would have to create a recession to get its credibility back," adds Goodfriend, now a professor at Carnegie Mellon University's Tepper School of Business in Pittsburgh. Bernanke, 55, said the risk of deflation was receding and that the Fed was ready to reverse course when needed to maintain stable prices and prevent an outbreak of undesired inflation. The Fed has implicitly defined price stability as annual inflation of 1.5 percent to 2 percent, as measured by a price index based on personal consumption expenditures. Given the Fed's inability to cut rates further, Mankiw says the central bank should pledge to produce "significant" inflation. That would put the real, inflation-adjusted interest rate -- the cost of borrowing minus the rate of inflation -- deep into negative territory, even though the nominal rate would still be zero. If Americans were convinced of the Fed's commitment, they'd buy and borrow more now, he says. Faster inflation might be preferable to increased unemployment, or to further budget stimulus packages that push up the national debt, says Mankiw "There's trillions of dollars of debt, in mortgage debt, consumer debt, government debt," says Rogoff, who was chief economist at the Washington-based IMF from 2001 to 2003. "It's a question of how do you achieve the deleveraging. Do you go through a long period of slow growth, high savings and many legal problems or do you accept higher inflation?" John Makin, a principal at hedge fund Caxton Associates in New York, wants the Fed to go further and target the level of prices instead of simply a rate of inflation. Such a policy would mean that if inflation fell short of 2 percent over a period of time, the Fed would have to push inflation above that rate subsequently to make up for the shortfall and keep prices rising on the

-

desired trajectory. While that might sound radical, it's the same sort of policy that Bernanke advocated Japan follow in 2003 to fight deflation. In a speech in Tokyo that year, then-Fed Governor Bernanke called on the Bank of Japan to adopt "a publicly announced, gradually rising price-level target." Warren Buffett, chairman of Berkshire Hathaway Inc. in Omaha, Nebraska, suggested that faster inflation was all but inevitable.

"A country that continuously expands its debt as a percentage of GDP and raises much of the money abroad to finance that, it's going to inflate its way out of the burden of that debt," he told the CNBC financial news television channel on May 4, adding, "That becomes a tax on everybody that has fixed- dollar investments."

Eggertsson Theory shows that the adoption of Quantitative Easing and Zero Interest Rate Policy is not enough to engender a defence against deflationary forces. What is needed is a change in the perceptions of market players, from the top to the bottom, allowing a change in spending and saving patterns.

I refer readers to this excerpt from The Future Actions of The Federal Reserve And US Govt Are Known, An interpretation of The Deflation Bias and Committing to Being Irresponsible by G B Eggertsson, made public in April 2008:

- Let me explain why, for the Fed and Government, there was no "Minsky Moment" but rather a progression of an already foreseen problem. To do this we need to look at why the Japanese Government and Bank of Japan failed to break out of a deflationary scenario. Again I quote from G B Eggertsson:

- "The deflation bias is closely related, and in some sense, a formalization of, a common objection to Krugman's policy proposal for the BOJ. To battle deflation he suggested that the BOJ should announce an inflation target of 5% for 15 years. Responding to this proposal, Kunio Okina, director of the Institute for Monetary Studies at the BOJ, said in DJN (1999): "Because short-term interest rates are already at zero setting an inflation target of say 2% would not carry much credibility." Similar objections were raised by economists such as, e.g., Dominiguez (1998), Woodford (1999), and Svensson (2001)"

- At face value the remarks above would seem to support the Keynesian approach, that at low nominal interest rates, Government deficit spending and quantitative easing failed to ignite the inflation required to break out of a deflationary spiral.

Within the quote though is the important point of inflation expectations. It is here that the importance of Bernanke's discussion of a targeted inflation rate and subsequent Fed warnings about inflation expectations remaining anchored becomes central to the main thrust of policy direction."

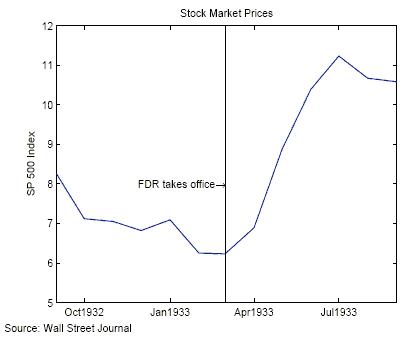

- "As FDR took office, there was a noticeable turnaround in expectations. Firstly, lets see what the baseline was, according to Eggertsson:

- "The reason for the collapse is that the central bank cannot lower interest rates enough to accommodate deflationary shocks, due to the zero bound on interest rates and is unable to change expectations about future policy. This creates a strong deflation bias. The deflation bias helps explain the severity of the Great Depression, because real interest rates were excessively high in 1929-33 due to double digit deflation. This choked spending, especially investment. "Money was king" during this period. Nobody was interested in investing when the returns from stuffing money under the mattress were 10-15 percent in real terms. People gained more, in other words, from holding money than spending it."

- Or as I said, why spend today when it will be cheaper tomorrow? It is clear that to make the Eggertsson Theory work, the baseline conditions of the economy should be depressed before allowing the already prepared stimulus to be released. Compare the conditions in 1933 to those today:

- "The short-term nominal interest rate was close to zero during the Great Depression. The yield on three month Treasuries, for example, was only 0.05 percent in January 1933. Further interest rate reductions were clearly not feasible. Open market operations, in themselves, had no effect, since money and government bonds were perfect substitutes. This explains why several observers at the time were skeptical of the effectiveness of monetary policy and believed that open market operations were just like "pushing on a string".

- Despite this, however, monetary policy was far from powerless. While increasing the money supply at zero interest rate has no effect, expectations about higher future money supply (once deflationary pressures have subsided and interest rates are positive again) have large effects because they change people's expectations about the future price level, thus reducing real interest rates. What was needed to end the Depression was a regime shift that changed expectations about future policy in a credible way. This is precisely what FDR achieved."

With current 3 month yields at at 1.13% and inflation measures well above, it can be seen why the Fed/US Govt fear a deflationary scenario. The requirement for a credible policy that will result in rising inflation expectations is absolute, to ensure that neither the consumer or business is discouraged from spending or investing. (This has far-reaching consequences, for instance it would not be in the Fed interest to suppress the price of gold

-

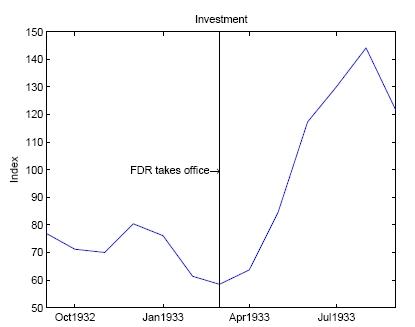

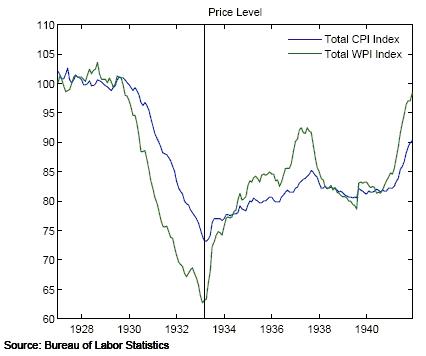

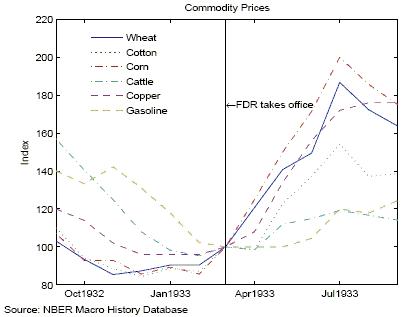

With this in mind, let us look at some of the effects that FDR policy regime change had post 1933:

Dow Futures June 09:

Bonds issuance:

CPI - All Urban Consumers (B of LS):

Continuous CRB Index (CI ICE / NYBOT) - TFC charts:

Are we seeing the "FDR effect" take hold? It's an important question, remember back in 1933 the problems were not over for the general economy but that didn't stop the reflation of various markets. We are seeing a very similar pattern today which must be due to the same reason as the rise in 1933, the result of a credible expectation of future inflation.

It is no wonder we are seeing so many articles on blogs, sites and now in the main stream media talking of inflation.

Right now, for the medium term, I am looking for a higher low (a downturn this summer would do the trick) and on a breakout of the recent high I would look to take a position. However, if the Fed move to a tightening stance in the future I would return to capital preservation mode, anticipating a 1937 scenario.

By Mick Phoenix

www.caletters.com

An Occasional Letter in association with Livecharts.co.uk

To contact Michael or discuss the letters topic E Mail mickp@livecharts.co.uk .

Copyright © 2009 by Mick Phoenix - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Mick Phoenix Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.