Stock Market Pre NonFarm Payrolls Profit Taking Sets In

Stock-Markets / Financial Markets 2009 May 08, 2009 - 05:21 AM GMTBy: PaddyPowerTrader

U.S. stocks fell prey to some pre nonfarm payroll profit taking which is hardly surprising given their recent gravity defying stellar up move. Tech and telecom sectors bore the brunt of the selling pressure while retailers were the sole bright spot. Weak demand at yesterday’s Treasury auction also rattled confidence as traders fretted that a rise in yields could choke off refinancing and increase mortgage costs and resets.

U.S. stocks fell prey to some pre nonfarm payroll profit taking which is hardly surprising given their recent gravity defying stellar up move. Tech and telecom sectors bore the brunt of the selling pressure while retailers were the sole bright spot. Weak demand at yesterday’s Treasury auction also rattled confidence as traders fretted that a rise in yields could choke off refinancing and increase mortgage costs and resets.

Today’s Market Moving News

- U.S. regulators told top banks yesterday to raise $74.6 billion to build a capital cushion officials hope will restore faith in financial firms and set a course out of the deepest recession in decades. Within minutes of release of the bank “stress test” results, which showed smaller capital needs than once feared, several of the 10 firms needing capital immediately issued statements detailing how they planned to raise it. Bank of America, who needs $33.9 billion, said it planned to sell assets, issue $17 billion in common stock, and take other steps to fill the hole.

- Yves Smith of Naked Capitalism, a strong critic of the way the US government has handled the financial rescue, released a critical report about the way The New York Times and other jubilant newspapers covered the stress test results. The newspapers failed to point out the following three important issues: (1) The fact quite a few of the banks negotiated their fundraising requirements down, calling the integrity of the process into question. (2) No mention that the purpose of this exercise from the outset was to prove the banking system to be solvent. What kind of a test is that? (3) No mention that asset sales (the reason Citi was able to negotiate its fundraising down from $10 billion, and presumably others as well) are almost certain to be a non-starter.

- Paul Krugman asks in his New York Times column whether the crisis is over now, and whether we should go back to partying. He says the Obama administration’s strategy is one of muddling through, hoping that an economic recovery would fix the banks. He said it might work, but probably not. He expects a longish period of sluggish growth. Most of all, he is worried about the prospects of deep financial reform, which is fading. He said the stress may be reassuring to the bankers, but the rest of us should be very afraid.

- AIG posts a larger than expected Q1 loss, but beat 2008’s Q1 figures. Reuters reports that they are in talks to sell their once prized Japanese HQ building to Nippon Life.

- Toyota is expected to report a consolidated operating loss of about 500 billion yen for the year ended March 31, due to the worldwide slump in automobile sales and a strong yen. Toyota had earlier projected a 450 billion yen operating loss. The company may also cut its annual dividend for fiscal 2008 to about 100 yen per share, compared with 140 yen in the previous year. Sales for fiscal 2008 are believed to have fallen by about 20 percent to about 21 trillion yen. Despite this the Japanese Nikkei index closed up 4.6% to a six month high.

- Smurfit Kappa Group reported first-quarter results that were broadly in-line with our forecasts. Revenues at €1.5bn were down 18% yoy, reflecting a 12% yoy decline in European corrugated volumes and continued pressure on pricing. In terms of outlook, management indicated that demand and pricing remain under pressure and conditions remain uncertain.

- The Irish Times this morning suggests that the government and the Financial Regulator are looking at whether Anglo Irish Bank can be granted a waiver from capital rules in an effort to reduce its immediate requirement for new capital from the state.

- It seems that the great recession will be bad for teen girl’s waistlines.

Stocks: The Bigger Picture

I would contend the current situation is not dissimilar to the late 2001 experience. For according to most commentary I see, there will be a temporary upturn to growth later this year due to the inventory cycle. Manufacturers have supposedly cut production so deeply that they have run off excess inventory. Hence they will now raise production to match the prevailing lower level of sales. This should temporarily deliver a quarter or two of growth. The question is what happens afterwards? Well, back in 2002 activity dropped back again, triggering a 35% S&P slump to 770 in October 2002. To be perfectly honest, I cannot see any earthly reason why manufacturers might step up production with this excess. Any final demand recovery can surely be met from existing stocks. One thing we know that US businesses have been doing recently is slashing costs. In the current reporting round, profits have been beating expectations at the same time that sales growth has been a major disappointment.

Move Over Stocks - Bonds Force Their Way Into the Limelight

U.S. bond yields have breached major medium-term levels, which is potentially a very big deal in the world of macro. At one level, it looks like the market is thumbing its nose at Quantitative Easing (QE), but rather than being interpreted as a sign of QE failing, it should be read as a reminder of how much higher yields would be if there was no QE. There has always been an internal inconsistency with QE that would be exposed in an economic recovery, where QE money creation is naturally inflationary, but also trying to hold yields down. This is definitely part of the problem if the drift higher in TIPS (inflation inked bonds) based inflation expectations is believed. Unfortunately real yields are also heading higher, which is a perfectly normal event where real rates of return increase with the end of the doomsday scenario for the globe. There is also the pesky problem of supply, which seems never ending at the moment to pay for all these mad cap government bailouts and rescues.

The ECB For Once Surprise The Market

The ECB delivered a 0.25% ease but that does not do justice to what I think is a seminal moment in the current easing cycle:

- The ECB no longer espouses that 1% is the low of the cycle. In fact, Trichet did not even take the opportunity at the Q&A to argue against 0% rates as we have heard in recent months, and we think the market has not fully understood the ECB ability to react to events.

- The extension of operations to 12 months was widely anticipated but is important in maintaining excess reserves. It is also very significant for Euro area government bond spreads i.e. the cost other countries must pay to raise monies above what Germany pays. The ECB is not buying member country government bonds directly but it is aiding deficit financing via banks buying domestic bonds and then funding at the ECB. Note Ireland’s “spread” has narrowed from 2.9% over Germany to 1.75% as of yesterday.

- The decision on asset purchase was a welcome surprise for most of the market. I was looking for asset purchase - after all ECB rates should be negative - but was surprised by the choice of covered bonds given that issuance is concentrated in handful of countries.

Data Ahead Today

At 09:30 UK PPI for April is released, which should be up 0.3% (annual inflation should slow from 2 to 0.8%) reflecting some pass-through from higher oil prices. The core PPI should see another rise of 0.2% (annual inflation should slow from 3.3 to 2.3%).

German industrial production for Mar is out at 11:00. Business surveys have shown some improvement and a 1% rise could happen despite a market consensus of -1.3%.

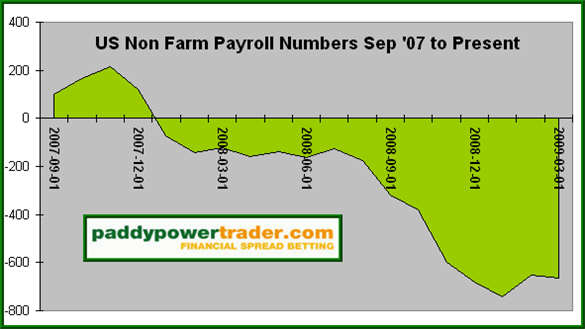

Then the biggies, U.S. non-farm payrolls are released at 13:30. Payrolls should see another big drop of 535K, after a better number from the ADP report. Unemployment should rise to 8.8%.

And Finally… A Stimulus Package Loan Song

Disclosures = None

By The Mole

PaddyPowerTrader.com

The Mole is a man in the know. I don’t trade for a living, but instead work for a well-known Irish institution, heading a desk that regularly trades over €100 million a day. I aim to provide top quality, up-to-date and relevant market news and data, so that traders can make more informed decisions”.

© 2009 Copyright PaddyPowerTrader - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

PaddyPowerTrader Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.