Credit Crisis Bank Stress Tests: If You Believe the Banks are Recovering...

Politics / Credit Crisis Bailouts May 01, 2009 - 01:45 AM GMTBy: James_Quinn

Hey Andy, did you hear about this one? Tell me, are you locked in the punch?

Hey Andy, did you hear about this one? Tell me, are you locked in the punch?

Hey Andy, are you goofing on Elvis? Hey baby, are we losing touch?

If you believed they put a man on the moon, man on the moon

If you believe there's nothing up my sleeve, then nothing is cool

Man on the Moon – REM

The conspiracy theorists of the world believe the U.S. government faked the landing of Apollo 11 on the moon. They also believe 9/11 was an inside job, ordered by operatives within the government. The rationale of these acts was to distract the masses from the disastrous Vietnam War and the plummeting stock market, while escalating their control over the American people. I believe I have uncovered the largest conspiracy in history. The government wants you to believe that banks are recovering, housing has bottomed, stimulus works, borrowing leads to prosperity and war leads to peace. President Obama and his cronies at Treasury and the Federal Reserve are trying to mislead the public regarding the health of our banking system. If you believe their spin on these issues, I have a structurally deficient bridge in Brooklyn I’d like to sell you.

The government has something up its sleeve this time. They are perpetrating the greatest fraud in the history of the world. The conspirators are Barack Obama, Timothy Geithner and the Treasury Department, Ben Bernanke and the Federal Reserve, Sheila Baer and the FDIC, and Barney Frank and the Democratic Congress. They have colluded to commit taxpayer funds to enrich bankers that brought down the financial system, without getting Congressional approval. They have delayed foreclosures and have tried to artificially prop up the housing market. They have poured billions of stimulus pork into the states praying for some of it not to be wasted. They have confiscated billions in taxpayer funds, bestowed them on reckless banks and forced them to lend it to anyone with a pulse, again. The outrage from the public during the TARP confiscation, made it crystal clear to courageous Congressmen they didn’t want to vote on something requiring fortitude and bravery again. They have outsourced their obligation to safeguard their citizen’s tax dollars to unelected bureaucrats at Treasury and the Federal Reserve. They have already sacrificed their obligation to declare war to the Presidential branch. What is the point of having a Congress?

Nothing Up Their Sleeve

Hey Andy, did you hear about this one? Tell me, are you locked in the punch?

Hey Andy, are you goofing on Elvis? Hey baby, are we losing touch?

If you believed they put a man on the moon, man on the moon

If you believe there's nothing up my sleeve, then nothing is cool

Man on the Moon – REM

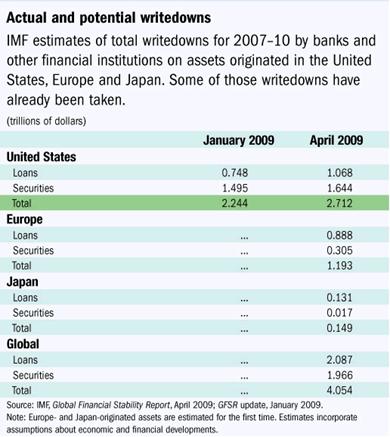

Barack Obama and his henchmen in Treasury and the Federal Reserve have chosen to play for time, pretend the banking system is solvent, and hope that the average American doesn’t care. As long as the ATM still spits out $20 bills, everything is OK. The International Monetary Fund has estimated total credit write-downs of $4.1 trillion, with $2.7 trillion in U.S. institutions. McKinsey has concluded that there are still $2 trillion of toxic assets sitting on the books of U.S. banks. Nouriel Roubini, who has been correct from the beginning, estimates total losses on loans made by U.S. financial firms and the fall in the market value of the assets they are holding will reach $3.6 trillion ($1.6 trillion for loans and $2 trillion for securities). The U.S. banks and broker dealers are exposed to half of this figure, or $1.8 trillion; the rest is borne by other financial institutions in the US and abroad. With $2 trillion of write-offs to go, how could Treasury Secretary Timothy Geithner make the following statement to a Congressional panel last week, “Currently, the vast majority of banks have more capital than they need to be considered well capitalized by their regulators.”? Is he lying or shading the truth? Does it matter?

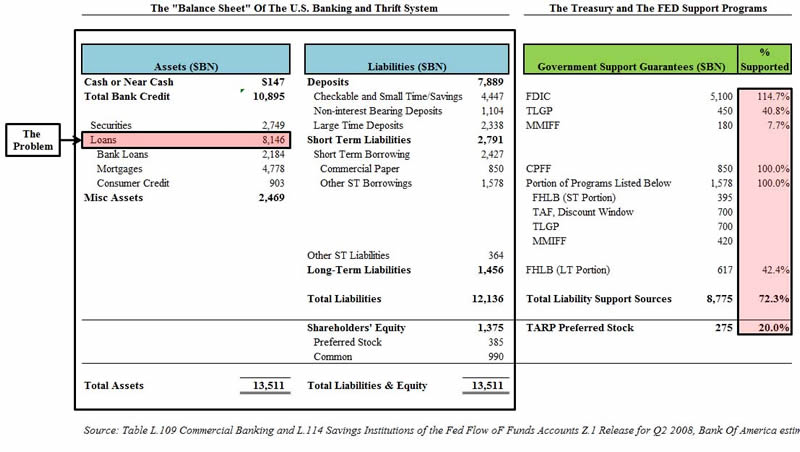

Roubini’s estimate of $1.8 trillion more losses for U.S. banks will cause a slight problem for the U.S. banking system. The entire U.S. banking system has only $1.4 trillion of capital. Therefore, the U.S. banking system is effectively insolvent. Mr Geithner would contend that he was not lying. There are 8,500 banks in the United States. The top 19 banks control 45% of all the deposits in the country. These are the banks that are insolvent. Mom & Pop Bank in Louisville, Kentucky didn’t create toxic loan instruments that infected the worldwide economic system. The vast majority of the 8,500 banks in the country are in good shape. Citigroup, Bank of America, Wells Fargo and the other “Too Big To Fail” banks destroyed the economic system. The Fed, Treasury, and FDIC are already backstopping or supplying 70% of the entire banking system balance sheet. It is time to allow the well run banks to take the deposits of the horribly run banks. The $1.8 billion of future losses do not include the commercial real estate losses, credit card losses and losses from the next wave of mortgage resets in 2010 that will wash over these banks.

Source: Tyler Durden – Zero Hedge

Of course we all know that the “Too Big To Fail” banks all reported profits better than expected in the last two weeks. CNBC said so. Let’s examine these tremendous profits.

Bank of America reported profits of $4.2 billion.

- $1.9 billion came from the gain on sale of CCB shares.

- $2.2 billion came from marking to market adjustments of Merrill Lynch notes.

- Non-performing assets were $25.7 billion compared to $7.8 billion one year ago, a 329% increase in one year.

Without these convenient accounting adjustments, Bank of America would have lost money. Andrew Ross Sorkin pointed out in a recent NYT article:

“With Goldman Sachs, the disappearing month of December didn’t quite disappear (it changed its reporting calendar, effectively erasing the impact of a $1.5 billion loss that month); JP Morgan Chase reported a dazzling profit partly because the price of its bonds dropped (theoretically, they could retire them and buy them back at a cheaper price; that’s sort of like saying you’re richer because the value of your home has dropped); Citigroup pulled the same trick.”

The first quarter bank profits were faked. They were manufactured as a public relations effort to convince the country that the big banks are in fine shape. If the banks are in such good shape why has the government had to use taxpayer funds to rollout the two dozen rescue plans listed below. And now we breathlessly await the results of the stress tests.

Click to Enlarge

Source: Tyler Durden – Zero Hedge

The FSP (Financial Stability Plan for those not in the know) rolled out by Tim Geithner was supposed to save our banking system. The plan was described by Treasury as:

Increased Transparency and Disclosure: Increased transparency will facilitate a more effective use of market discipline in financial markets. The Treasury Department will work with bank supervisors and the Securities and Exchange Commission and accounting standard setters in their efforts to improve public disclosure by banks. This effort will include measures to improve the disclosure of the exposures on bank balance sheets. In conducting these exercises, supervisors recognize the need not to adopt an overly conservative posture or take steps that could inappropriately constrain lending.

Coordinated, Accurate, and Realistic Assessment: All relevant financial regulators — the Federal Reserve, FDIC, OCC, and OTS — will work together in a coordinated way to bring more consistent, realistic and forward looking assessment of exposures on the balance sheet of financial institutions.

Forward Looking Assessment – Stress Test: A key component of the Capital Assistance Program is a forward looking comprehensive “stress test” that requires an assessment of whether major financial institutions have the capital necessary to continue lending and to absorb the potential losses that could result from a more severe decline in the economy than projected.

It is fascinating that in the first paragraph they specifically state they don’t want to be overly conservative. Which of the top 19 banks in the country have run their businesses in an overly conservative manner in the last ten years? Has the Federal Reserve been overly conservative in the last ten years? Have the SEC and FDIC been overly conservative in the last ten years? Have consumers, homebuilders, credit card companies and retailers been overly conservative for the last ten years? If there was ever a time to be overly conservative, it is now. It is also nice to know Treasury wants accuracy and better disclosure, but then twists the arm of the FASB to relax mark to market rules, so banks can continue to lie about the value of “assets” on their books. They allow Goldman Sachs to bury the fact that they left December out of their financial results deep in their footnotes. Shockingly, Goldman lost $1.5 billion in December. They continue to allow banks to report one time gains as part of ongoing operations, but billions in losses that are recorded quarter after quarter are not from ongoing operations. The morons on CNBC report whatever the banks say, no questions asked.

Stress Test Sham

This brings us to the stress tests for the 19 biggest banks in the land. The most stressful conditions are supposed to be 10% unemployment and a 20% further fall in home prices. That doesn’t sound too stressful to me. Considering the government reported figures are a manipulated lie, we already have unemployment between 15% and 20% in the real world. A 20% further decline in home prices is a given. The Case Shiller futures index forecasts that the New York Metro area will fall by 31% by the end of 2010. The massive overhang of housing inventory, the coming onslaught of mortgage resets in 2010, and the millions of foreclosures in the pipeline guarantee at least 20% further downside in housing prices. I have a feeling these 19 banks are going to need to study a little harder for their test. Professor Geithner is giving them an open book take home exam and gave them the answers. They will still flunk.

William Black is a former senior bank regulator. He is currently an Associate Professor of Economics and Law at the University of Missouri. Mr. Black held a variety of senior regulatory positions during the S&L crisis. He managed investigations with teams of examiners reporting to him, redesigned how exams were conducted, and trained examiners. He calls the stress tests conducted on the 19 biggest banks in the country a complete sham. In his own words:

- If you did a real stress test, as Geithner explained them, you wouldn't just have a $2 trillion hole -- you'd impose regulatory capital requirements of 50%. (FYI, the regulators have the power to set HIGHER individual capital requirements based on unusually large risks at a particular bank.)

- You can't conduct a meaningful stress test without reviewing (sampling) the underlying loan files and it seems likely that the purchasers of securitized instruments (not just mortgages) do not even have the loan file data. Moreover, loss ratios vary enormously depending on the issuer, so even a bank that originates (or has purchased a bank that originates) similar product cannot simply take its own loss rate and extrapolate it to the measure the risk on the value of securitized credit instruments.

- It is vastly more difficult to examine a bank that is engaged in accounting control fraud. You can't rely on the bank's books and records. It doesn't simply take more, far more, FTEs -- it takes examiners with experience, care, courage, and investigative instincts and abilities. Very few folks earning $60K are willing to get in the face of the CEO and CFO making $25 million annually and tell them that they are running a fraudulent bank and they are liars. FYI, this is one of the reasons, why having "resident examiners" never works. The examiners don't even get to marry the natives. They get to worship God's anointed. Effective examination is good for you, but it is very unpleasant, ala a doctor's finger up your rectum. It requires total independence. So, the examination force doesn't have remotely the numbers or the relevant experience and mindset to examine the largest banks with the greatest problems.

- Examiners certainly can't do the stress testing that Geithner describes or evaluate the reliability of a large bank's proprietary stress test. If they were serious about constructing reliable stress tests, which they aren't, you'd require their analytics to be made public. You'd have the industry fund independent investigations by rocket scientists chosen by a committee selected by the regulators of the soundness of the analytics. You'd also have the industry fund competitions to rip them apart (a bit like we hire legit hackers to test security by trying to defeat it) and show where they produce absurd results. The geeks would have a field day (that would probably last a decade). There are probably zero examiners that have the modeling skills required to evaluate the most sophisticated stress test models. The concept that there are 100 examiners with these skills, suddenly freed up from all other duties, assigned to CONDUCT stress tests is a lie.

On Monday we will see how much transparency and disclosure the Treasury and Federal Reserve will provide regarding the not so stressful tests. Obama’s minions have been hinting that six banks have failed. Sheila Baer stated that the $110 billion left in the TARP kitty should be enough to cover the capital shortfalls. This is a lie. As we saw previously, the U.S. banking system will need close to $1 trillion more capital to stay viable. If the Federal Reserve was so keen on disclosure and transparency, why haven’t they released the names of the banks that have borrowed from them, and the collateral provided for the loans? Because the Fed has taken worthless toxic paper onto their books and loaned newly printed dollars against the worthless paper. The taxpayers are on the hook.

Fraudulent Fed

Ben Bernanke has a number of obligations as head of the Federal Reserve. Among his mandates are:

To strike a balance between private interests of banks and the centralized responsibility of government

- To supervise and regulate banking institutions

- To protect the credit rights of consumers

To manage the nation's money supply through monetary policy to achieve:

- maximum employment

- stable prices, including prevention of either inflation or deflation

To maintain the stability of the financial system and contain systematic risk in financial markets

Let’s assess how Helicopter Ben Bernanke and Mad Dog Alan Greenspan have fulfilled their mandates. They were supposed to supervise and regulate banking institutions. They apparently slipped up slightly on this mandate. It appears that letting banks regulate themselves was a slight miscalculation on Mr. Greenspan’s part. The man who never saw a bubble in his life had this to say:

“The presumption that you could incrementally defuse a bubble was a fantasy. Clearly, you cannot defuse these things, unless you hit them right on the head and break the economy. Essentially, break the potential profitability that is engendering that sort of stuff. We could have basically clamped down on the American economy, generated a 10 percent unemployment rate. And I will guarantee we would not have had a housing boom, stock market boom or indeed a particularly good economy either.”

So, Greenspan stepped aside as banks sold adjustable rate negative amortization loans to subprime borrowers with no proof of income or assets required. The job of an independent responsible Central Banker is to take the punch bowl away before the party gets out of hand. The politically connected fawning Greenspan chose to spike the punch bowl with 1% interest rates and exhorting the party goers to take out adjustable rate mortgages. Free market capitalism with no rules was the path to prosperity in his mind. The Greenspan Put was in place. Party like it was 1999 and he’d clean up afterwards. Instead, the American taxpayer is stuck with the bill and Greenspan gets $100,000 per self serving speech.

Mr. Greenspan made his biggest mark with his hands off attitude regarding derivatives. His quote from May 2005 will get him into the Federal Reserve Hall of Fame:

"The use of a growing array of derivatives and the related application of more-sophisticated approaches to measuring and managing risk are key factors underpinning the greater resilience of our largest financial institutions .... Derivatives have permitted the unbundling of financial risks."

Would you pay this dude $100,000 for his words of wisdom? Didn’t this man have hundreds of PhDs gathering wads of information about the practices of our biggest financial institutions? He was either the most incompetent Federal Reserve Chairman in history, or he was in the back pocket of the banking cartel. Take your choice. The major banks became gambling casinos run by multi-millionaire MBAs, tooling around in their private jets, using derivatives as the chips in their trillion dollar game of craps. When these Masters of the Universe MBAs rolled snake eyes, the world wide financial system collapsed. Mandate #1 was not a success story.

Mandate #2 was to protect the credit rights of consumers. Considering Americans have lost $10 trillion of net worth in the last 18 months due to the Federal Reserve mismanaging interest rates, failing to properly regulate banks, and allowing mortgage brokers to mislead millions of immigrants into mortgages they didn’t comprehend, it appears they may have failed on mandate #2. Now, Ben Bernanke has lowered interest rates to 0% in an attempt to enrich the major banks at the expense of senior citizens living on a fixed income. Investors who were receiving 5% on their money market deposits in 2007 are now receiving less than 0.5%. Ben would prefer that 85 year old grandmothers invest in high yield bonds. He is systematically stealing from the poor to give to the rich.

Mandate #3 regarding maximum employment doesn’t seem to be working out too well either. The government massaged numbers show unemployment at 8.5%, the highest rate since 1983. Unemployment will easily reach 10% during 2009 and may reach the highest levels since the Great Depression. It appears the Federal Reserve misunderstood their mandate and is working towards minimizing employment as less than 60% of working age population is employed today. By reducing interest rates to generational lows, the Federal Reserve created the boom that led to the bust. Their interest rate manipulations have led to 13 million Americans being unemployed today, an increase of 6 million in less than two years.

Mandate #4 of stable prices with prevention of inflation and deflation has been somewhat of a challenge for geniuses at the Federal Reserve. Using the non-manipulated consumer price index, inflation has consistently run above 8% since the 1980’s, peaking above 12% in 2008. By falsifying the calculations, Ben Bernanke is able to leave interest rates at 0%. The government reported figures show no inflation. By manipulating the CPI, the government is able to pay senior citizens 1%, while their costs for food and energy and go up 6%. It is good to see the Federal Reserve is looking out for the most susceptible in society.

Lastly, the Federal Reserve was supposed maintain stability in the financial markets. The last 18 months have been the most instable period for financial markets in history. The Federal Reserve allowed at least a dozen financial institutions to become too big to fail. By coming to the rescue of the financial markets every time something bad happened starting with LTCM, the Federal Reserve encouraged excessive risk taking by financial firms. These institutions knew the Federal Reserve would clean up their messes. They were right.

With a perfect record in the mandates they were asked to fulfill, you can see why we would want to give the Federal Reserve more power and more mandates. Paul Volcker, the only decent Federal Reserve Chairman in history, thinks otherwise:

“The Federal Reserve is going beyond the traditional role of central banks here or abroad. At some point it’s reasonable to ask should this particular institution, with its independence very well protected, be allocating so much of what is essentially government money. The inflation problem, which should be a real threat for the future, is not right on the doorstep. But two or three years from now that may be the critical problem, how that’s handled. Because, given what the Federal Reserve has been doing, it’s going to be harder to retrace their steps, so to speak, than it ordinarily would be.”

Goofing on Elvis, Are We Losing Touch?

The stock market has been soaring as banks report fraudulent earnings. These banks are purposely underestimating future losses to make current earnings appear better than they really are. Hank Paulson and Ben Bernanke demanded that Ken Lewis commit fraud by not revealing material information to the public about Merrill Lynch. Why are they not being prosecuted? Bankers protect the members of their bankers club. Dr. John Hussman describes how it works in today’s world:

“That's what these bureaucrats want during their stint in government service, that's how they advise our elected officials, and then their revolving door takes them right back to Wall Street. This thing is run by investment bankers and corporate bondholders for the benefit of investment bankers and corporate bondholders.”

The government is desperately attempting to convince the world that the banking system is sound and recovery is under way. The actions they have taken have not and will not fix the system. The waves have washed away the foundations of sand propping up the U.S. financial system. Instead of learning from their mistakes, officials have decided to rebuild on a new foundation of sand. We are borrowing from foreigners to bailout bankers and handing the bill to future generations. With government dictating the future of our banking system we can count on massive fraud, waste and mismanagement. Dr. Hussman’s frustration is well founded:

“It's frustrating, but we are wasting trillions of dollars that could bring enormous relief of suffering, knowledge, productivity, and innovation in order to defend bondholders of mismanaged financials, and nobody cares because hey, at least the stock market is rallying. If one thing is clear from the last decade, it is that investors have no concern about the ultimate cost of the wreckage as long as they can get a rally going over the short run.”

This public relations effort will fail. There are hundreds of billions of losses left to be recorded by our big bad banks. If you believe this is almost over, you are not paying attention.

If you are seeking the truth, join me at www.TheBurningPlatform.com .

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2009 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Andrew_Butter

01 May 09, 16:06 |

Bank stress tests

So you only just twigged the stress tests were pure theater? It's called "forebearance". |