Bankrupt Banks to be Hit by New Wave of Losses

Stock-Markets / Credit Crisis 2009 Apr 16, 2009 - 02:22 PM GMTBy: Jim_Willie_CB

One must give a tip of the hat to the Wall Street conmen for engineering a reasonably robust stock rally. The Dow and S&P were led by financials. The Financial Times out of London claims ‘no real money’ was behind the stock rally of over 20%. They must mean huge short covering, enhanced by pressure tactics from Wall Street brokerages themselves. They must mean Working Group For Financial Markets putting to work some of their ‘Black Bag’ money. They must mean influenced arbitrage games from preferred versus common shares, which harmed the public but enriched the insiders. Amazing how a better financial journal on US topics comes from outside the Untied States.

One must give a tip of the hat to the Wall Street conmen for engineering a reasonably robust stock rally. The Dow and S&P were led by financials. The Financial Times out of London claims ‘no real money’ was behind the stock rally of over 20%. They must mean huge short covering, enhanced by pressure tactics from Wall Street brokerages themselves. They must mean Working Group For Financial Markets putting to work some of their ‘Black Bag’ money. They must mean influenced arbitrage games from preferred versus common shares, which harmed the public but enriched the insiders. Amazing how a better financial journal on US topics comes from outside the Untied States.

A movement pervaded Lower Manhattan offices to formally call in all Citigroup shorted shares on loan. Whether legal or not, it helped cause a big bank stock rally. Other ‘C’ share games were played that enabled preferred shares to serve as collateral on common share shorts, as the plebeian shares descended to $1/share value. Never lose sight of the fact that Plunge Protection Team funds came in large part from missing $1.5 billion in Fannie Mae funds from 1988 to 2000, specifically out of the HUD offices in Houston (Papa Bush regional home) and in Oklahoma City (Clinton home region), whose funds keep America strong. Then you have all the absurd giant steps backwards to permit big banks to ignore Mark-to-Market and just conjure up asset values from indefensible models, with blessing from Financial Accounting Standards Board and the USCongress. This reform?

As citizens pay their income taxes, and observe the ‘Tea Parties’ around the nation, think deeper than the many plain shallow placards with great intention. The original Boston event prompted a Revolutionary War. The battle cry was over taxation without representation, a tax levy on tea to the colony, without a voice in the King George court. With the USCongress taking orders from Wall Street and having votes bought by lobbyists, the focus should be not on high taxes or low taxes, but taxation without proper representation by members of the USCongress. The august body in the USCongress has received countless million$ from Wall Street firms and Fannie Mae, along with dozens of other firms embroiled in the banking crisis that has destroyed the US banking system. Thousands of lobby groups have taken control of the USCongress, including the Council on Foreign Relations and AIPAC. My firm belief is that bribery is the way of the House & Senate. The people have little or no voice anymore, which is the basis of any charge of tyranny.

In order to remedy the banks and recapitalize them, our banking and government leaders must find more intricate methods with greater confusion and more hidden requirements to enable the big banks to be replenished at federal expense, while the public remains ignorant, and Main Street is directly and plainly neglected. The TARP congame has been discredited. The Public Private Partnership Investment Program is a revamped TARP sham. Listen to the Jackass on a radio interview (CLICK HERE), that covers many aspects of this disguised carry trade program, criticism from watchdog and Nobel Prize winner Stiglitz, the interior battle between the FDIC and Dept Treasury, and how the requirements for its official ‘Fund Manager’ are only met by the five Wall Street banks that committed the majority of the bond fraud. Geithner plans to build a bus to transport capital to big banks, called ‘The Geithner Summers Structured Investment Vehicle’ after the infamous SIVs.

Forget economist forecasts, both inaccurate and old-fashioned. New research shows corporate bonds have been far better at predicting where the USEconomy is headed than one might expect. The great churn to subsidize and redeem the Wall Street banks has brought them off their knees, now ready to lend again at a minimal level after their fraudulent chapter. Their insolvency will remain for another year or more. Signals from the corporate bond spreads suggest strongly that the USEconomy will falter worse. In the autumn of 2007, before conditions began to falter, corporate bond prices raised the red flag. The spread between corporate bond yields and USTreasury yields had begun to widen as the mortgage crisis showed its subprime prima facie that summer in 2007. More declines are coming, signaled by current corporate bond spreads.

GOLD TO RISE ON FURTHER MONETARY DEVALUATION

Staggering additional monetary inflation comes, initially from programs by the USGovt and USFed to date. More monetary debauchery is right around the corner, to be extremely clear by summertime. Bank losses will become a national nightmare, seemingly never ending. Only deception buttresses the bank sector now, their specialty. Both central bank and USGovt funds will become an absolute torrent when they finally come to grips with the bank losses upcoming and the momentum for USEconomic downturn toward depression. Vicious feedback loops at finally in high gear. When the printing press becomes more heavily relied upon, the clarity of USDollar support also coming from USMilitary actions will render the gold & silver assets more desirable safe haven investments. Furthermore, USFed authorities must be deeply worried about the seeds they are planting for future price inflation. The USFed just purchased $1.5 billion in Treasury Inflation Protection Securities (TIPS) in an unprecedented maneuver. No longer does the TIPS tell of inflation expectorations. What on earth is going in on their tiny minds?

The story not told often enough is the utterly huge short gold futures contract positions put on by JPMorgan immediately when the USFed announced its $1 trillion monetization plan in mid-March, and the additional batch of gold short contracts they put on during the G20 Dollar Funeral event in early April. Perhaps the USDept Treasury can access some of the $1.9 billion from the AIG car insurance business unit sale to Zurich Financial to fund more market corruption and interference, with a simple handoff from to their free market brothers at JPMorgan. Still, despite all the harmful, unregulated, and relentless pressure put on precious metals, their prices refuse to be pushed down. The gap between the physical gold price and paper COMEX price continues to widen. The story behind the scenes that captured my attention centered on German demands to return all their gold bullion held in custodial accounts on US soil. The deep source contact said something like, “the German demand is making the US bank nazis sweat bullets. Pressure on COMEX will get much worse.” Expect even more pressure on the June gold contract than was seen with the March gold contract, as far as delivery default is concerned. Deutsche Bank saved the COMEX bacon with a last minute 850,000 ounce delivery, courtesy of the Euro Central Bank at the eleventh hour. Such are the games not told on national financial networks, but which are central to Hat Trick Letter analysis.

The gold price is busy carving out the Right Side Handle to a messy Cup & Handle reversal pattern, one which is testing the patience of yellow metal investors. When the weekly stochastix cycles down a little farther, the consolidation should be at an end. We observe not so much a battle of monetary inflation versus asset deflation, as with free market pricing structures versus disruptive USGovt custodial management that will someday be chronicled as the most corrupt in modern history. Asian and Arab creditors to the USTreasury Bonds are not pleased with what the management of either the USGovt bond securities or gold, and they hold both in great volume. The target for gold remains almost 1300, with a breakout inevitable.

The silver chart looks even more bullish. Instead of a clear reversal pattern, it shows a recovery pattern that struggles to find strong footing on the less stable 20-week moving average. Its move to reach old highs will be easier, once near-term resistance is overcome. The 50% retracement of the long run from last October to February would paint a line at the 12.3 level for Fibonacci support. He was a friend of Botticelli, Lambourghini, Zepharelli, and great grandfather to Roubini, surely good company to keep. Look for an upcoming crossover of the 20-wk MA (in blue) above the 50-wk MA (in red), a powerful technical bullish signal for moves to approach the July and March 2008 highs. It is also inevitable.

ROOT CAUSE OF BANK LOSS

The two root causes of the deep historically unprecedented US bank losses from bond assets and credit portfolios are housing price declines and home foreclosures. For to claim the banks have stabilized without the home prices or forced foreclosures is absurd on its face. What has changed would please US Federal Reserve Chairman Ben Bernanke, market psychology. He favors inflation expectorations for USTreasury Bonds over monetary growth, as the USDollar is debauched into oblivion. He favors consumer sentiment for the USEconomy over retail store shutdowns and shopping mall vacancies. The Wall Street maestros sold the investment community a bill of phony goods that will be evident by summer.

They engineered a bank sector rally based on falsified earnings reports, orders by the USFed to keep the Bank Stress Tests secret until May, a return of the uptick short stock rule, and a return to valuing bank assets by creative methods based upon valuation models. Those hidden proprietary models contain a scad of silly assumptions like a 7.0% jobless rate. The March data already gave us 8.5% on that meter, but the reality-based Shadow Govt Statistics claim the jobless rate (when people without jobs are counted) is 17.0% actually.

Housing prices continue down. The January Case-Shiller housing index for 20 cities showed a minus 19.0% change from a year ago, a statistic remarkably free of USGovt garbage adjustments. It is just the change from Jan 2008 to Jan 2009, no frills, no deception. The key point of the C-S housing index is that it has been in decline for consecutive months going back to the beginning of the officially recognized recession in December 2007. The other key point is that all 20 cities are in price decline, all of them. My forecast in the Hat Trick Letter, given in year 2005 and repeated in 2006, was for a seemingly endless housing decline in a powerful unprecedented bear market, in essence a double correction since Greenspan diverted the expected bear from its path in 2001, denying him his due. The price decline dictates impossible conditions to refinance under-water home loans, which applies to almost 30% of US homes with mortgages (loan balance exceeds current home price). Falling home prices encourage homeowners to stop making mortgage payments, viewed as throwing away money down a toilet.

Although repossessed bank-owned (real estate owned) REO liquidation sales make up 60% of total sales in the gogo states, REO listings make up only 33% of total listings. Banks are holding back inventory, amidst a flood. In doing so, they hide losses. Incredibly, exactly half of ordinary home sales outside bank liquidations are short sales, meaning sellers must produce cash above the sale price in the lawyer’s office. Individuals who own homes falling in value, whether sapped of equity or running negative equity, are unable to tap credit lines from Home Equity Lines of Credit (HELOC). Worse, as a household with negative home equity usually contains people who stop spending in normal fashion. The USEconomy is thus deeply affected by declining home prices. Banks in particular stand at the apex of losses, since their borrowers lose credit worthiness, and loan instruments are leveraged. More data and analysis is provided in the April Hat Trick Letter macro economic report just posted.

Sweetheart analyst Meredith Whitney expects home prices to fall another 30%. US banks and mortgage lenders would have much worse crippling losses ahead. She expects such losses would finally kill a long list of US banks, large and mid-sized. She makes a great point, saying “Home prices cannot bottom while liquidity is still contracting from the economy.” She predicts that peak-to-trough home price declines will average 50% nationally before the US housing crisis ends. We are halfway to the bottom, and likely have seen half of the bank losses to come. Whitney is known for her bearish calls, largely correct to date.

Home foreclosures continue up. The biggest single factor behind a home foreclosure is job loss with discontinued income. The second biggest factor is unexpected medical expenses, which extends to other family members like parents. RealtyTrac just reported today that home foreclosures for the first quarter of 2009 are up 24% from a year ago. In California, where the moratorium has lifted, foreclosures rose by 80% from February to March, hitting 50 thousand!!! The April increase could be well above 100% in makeup mode. JPMorgan, Wells Fargo, and Fannie & Freddie each lifted their moratorium. Incredibly, prime mortgages delinquent over 60 days more than doubled in 4Q2008 to 2.4%, when compared to the first quarter 2008. A uniform upward uptrend in the delinquency rates has occurred over the last several months. Nobody in Bank Land prefers to discuss the rising defaults of the prime mortgages, which include Pay Option ARMs, Intermediate term ARMs, and more. The prime default rates are much lower than the subprime and Alt-A garbage loans (often with no income, no documentation, no assets, and no verification), but the volume of prime home loans is huge, resulting in great potential for future bank loss. The adjustable rate mortgage default flood has begun, with full warning given to Hat Trick Letter subscribers several months ago. Mark Hanson has been indispensable source of great information.

Mr Mortgage, as he is known, has a great website (CLICK HERE) chock full of relevant timely data that is well ahead of the pack. His work is often quoted on national financial networks. He points out that Jumbo loans now comprise 31% of all fresh loan defaults. So the foreclosure problem has hit the high end, where losses per loan to banks will be much greater. All the delay in lifting the conforming Fannie Mae loan limit from $417k to $729k led to severe damage to high end property prices. Then you have the ‘Revolving Door’ of federal modified home loans. The 1Q2008 vintage modified loans defaulted 41% of the time after eight months. The 2Q2008 modified loans had a 46% default rate down the road. The third quarter trends are worsening, according to the Office of the Comptroller of the Currency (OCC) and the Office of Thrift Supervision. Data is not yet available. The Federal Housing Admin is the new subprime slime lender, under the USGovt leaky roof. At end of February, a huge 7.5% of FHA loans were deemed ‘seriously delinquent’, up from 6.2% a year earlier, typically with under 3% to 5% down payments. The FHA share of the US mortgage market soared to nearly 33% of loans originated in 4Q2008, from about 2% in 2006. More data and analysis is provided in the April Hat Trick Letter macro economic report just posted.

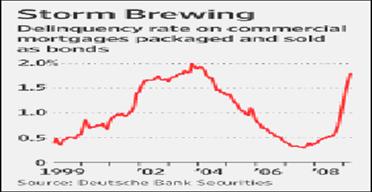

THE NEXT SHOE – COMMERCIAL MORTGAGES

The bank sector is debating this topic now, complete with considerable denial and departures from reality (what the facts state). Inside reports speak of grand internal sandbag projects by big banks to brace for the coming storm expected. The delinquency rate for commercial mortgages has more than doubled since September to 1.8% this month, on $700 billion in securitized loans, according to Deutsche Bank. This market is usually highly stable. The current delinquency rate is just below the peak in 2004. Some experts anticipate the current commercial slump will exceed that seen in the early 1990s. Foresight Analytics of Oakland California estimates the US banking sector could suffer as much as $250 billion in commercial real estate losses in the current crisis. They project that over 700 banks could fail as a result of their exposure to commercial real estate. That is five times the charges on commercial real estate debt between 1990 and 1995. Deutsche Bank estimates the default rates on the $700 billion of commercial mortgage backed securities could reach 30%, and aggregate loss rates could reach 10%.

Besides securities backed by commercial real estate loans, about $524.5 billion of whole commercial mortgages held on portfolios by US banks and thrifts will come due between 2009 and 2012. Nearly 50% would not qualify for refinancing in today’s credit environment, estimates Matthew Anderson at Foresight Analytics. Lenders generally reject loans over 65% of a commercial property value. General Growth was a victim today of inability to refinance and roll over their debt. They had strong fundamentals, but unfortunately bankers do not. More data and analysis is provided in the April Hat Trick Letter macro economic report just posted.

Besides securities backed by commercial real estate loans, about $524.5 billion of whole commercial mortgages held on portfolios by US banks and thrifts will come due between 2009 and 2012. Nearly 50% would not qualify for refinancing in today’s credit environment, estimates Matthew Anderson at Foresight Analytics. Lenders generally reject loans over 65% of a commercial property value. General Growth was a victim today of inability to refinance and roll over their debt. They had strong fundamentals, but unfortunately bankers do not. More data and analysis is provided in the April Hat Trick Letter macro economic report just posted.

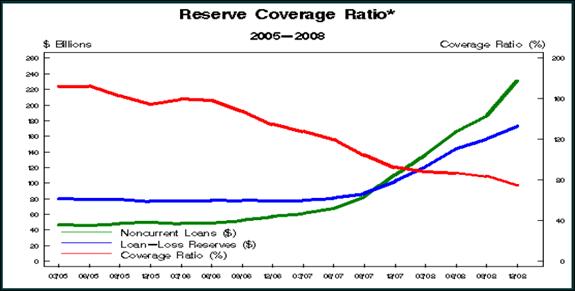

BANKS ARE NOT READY FOR MORE LOSSES

The official FDIC Banking Profile report from the fourth quarter of 2009 reveals that failing loans have risen faster than reserves. The big banks cannot bring in new capital (from TARProgram, USGovt-sponsored carry trades, or equity investors in Saudi Arabia) to match growth in their losses. This has caused the ‘coverage ratio’ to plunge below 100%, cut in half since 2005. It is below 80% actually (shown in red). The big banks must dig into earnings to build loan loss reserves. Case in point JPMorgan today, adding $4.2 billion into loss reserves. Case in point Capital One yesterday, reporting credit card charge-offs of $526.5 million. Banks remain behind the curve. Banks face multiple fronts for profound losses, as mortgages are but one factor. Recall the Bernanke claims in 2007 that subprimes would be contained, no broad contagion to bonds would occur, the USEconomy would be insulated, and the total bank losses would be under $200 billion. What a hack! But then again, he is just a dumb professor, now a full-time lithographer. It seems the gold journals contain numerous better bank analysts and economic forecasters than the good chairman.

Michael Mayo of Calyon Securities gave warning of broadening bank losses, which actually roiled the stock market when released. He said, “Mortgage related losses are about halfway to their peak, while credit card and consumer loan losses are only a third of the way to their expected highest levels. The nation’s largest banks may be transitioning from a financial crisis marked by write-downs of capital, to an economic crisis featuring large loan losses.” And then the headline catching report from Calyon Securities suggesting that total bank loan losses could reach 5.5% by the end of year 2010.

CREDIT CRISIS AUTOPSY

Here is fine piece of analytic work from a friend named Trace Mayer. He comes to the gold community with a different slant and background. He has a law scholar with emphasis on the Constitution, especially how it applies to the gold and currency topics. In his e-book entitled “The Great Credit Contraction” one can read about the historical significance of a crisis that will surely reshape the world. The global economy is built on an illusion currency that is evaporating before our very eyes. This book is an autopsy of the current worldwide systems and begins with financial history, discusses the current great deflationary credit contraction, projects the future environment, and concludes with suggestions on how to generate and preserve wealth in this challenging time. An appendix analyzes important topics. (CLICK HERE TO ORDER)

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

At least 30 recently on correct forecasts regarding the bailout parade, numerous nationalization deals such as for Fannie Mae and the grand Mortgage Rescue.

“You seem to have it nailed. I used to think you were paranoid. Now I think you are psychic!” (ShawnU in Ontario)

“Your analysis is of outstanding quality, the best I have read. In particular, as a person on the spot, I can confirm the accuracy of your bleak assessment of our prospects in the UK.” (JanB in England)

“Your unmatched ability to find and unmask a string of significant nuggets, and to wrap them into a meaningful mosaic of the treachery-*****-stupidity which comprise our current financial system, make yours the most informative and valuable of investment letters. You have refined the ‘bits-and-pieces' approach into an awesome intellectual tool.” (RobertN in Texas)

“Your reports scare the hell out of me every month, probably more so over time, since so many of your predictions have turned out to be very accurate. I am afraid you might be right that by the end of 2008, we are in a pretty severe situation, with civil unrest and severe financial stress on Main Street.” (GeorgeC in Minnesota)

by Jim Willie CB

Editor of the “HAT TRICK LETTER”

Home: Golden Jackass website

Subscribe: Hat Trick Letter

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by compromised central bankers and inept economic advisors, whose interference has irreversibly altered and damaged the world financial system, urgently pushed after the removed anchor of money to gold. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.