Leading U.S. Economic Indicators Point to Improvement

Economics / Recession 2008 - 2010 Apr 14, 2009 - 12:48 PM GMTBy: Clif_Droke

Since the start of the new millennium and new century, many of the old truisms that applied to economic forecasting are no longer relevant. So many things have changed in the last nine years that a new set of economic “rules” is in order.

Since the start of the new millennium and new century, many of the old truisms that applied to economic forecasting are no longer relevant. So many things have changed in the last nine years that a new set of economic “rules” is in order.

For instance, it wasn’t that long ago that the saying, “What’s good for GM is good for America” was a valid economic maxim. Today this famous proverb has been reversed now that the government has taken partial ownership in the auto maker. In an ultimate twist of irony, the chief executive of the U.S. recently fired the president of General Motors. The lesson here is that what’s good for the U.S. isn’t necessarily good for GM.

Another of the Big Three automakers, Chrysler, is now seeking a partnership with Italy’s Fiat in hopes of surviving the auto industry downturn. Chrysler’s president, Jim Press, has warned that if Chrysler fails to survive “it could trigger a depression” due to the ripple effect of up to a million jobs lost as a consequence of its failure.

While there is no debating the fact that a Chrysler collapse would have a major impact on the economy, the scope and severity of the automaker’s fate has been exaggerated by many commentators. Those pundits who make their livelihoods on majoring on the negatives are running with Mr. Press’ comments and concocting countless scenarios of doom and gloom to accompany it. The pessimists also tend to focus on the economic numbers, which naturally have a negative bias since they reflect what happened 1-3 months ago.

Instead of focusing on backward-looking economic data, we’ll be looking at the forward-looking stock market indicators in this report. The leading market indicators can provide a glimpse ahead as the market typically discounts the business outlook 6-9 months in advance. You have to know which indicators to look at but when you examine them all in their proper context the intermediate-term picture that emerges is much more encouraging than the bleak picture being painted by the doom-and-gloom crowd.

Four of out our five key economic indicators are looking good right now. We touched on these indicators a couple of weeks ago and an update on them is in order. The indicator we had the most concern about, Fed-Ex (FDX), put in a solid performance last week. FDX was up over 6% on Thursday before the trading week ended and is now above its important 60-day moving average and about to test the dominant interim 90-day moving average. We’ll keep our eyes on Fed-Ex since any further improvement in this extremely important indicator bodes extremely well for the U.S. economic recovery.

Monster Worldwide (MWW) is another component in our New Economy Index and a reflection of the job market. Monster had a stellar week last week and was up nearly 12% alone on Thursday, April 9, and up by a further 12% on April 13. MWW is now above all three of its key moving averages in the 30/60/90-day MA series. This marks the first time since last spring that MWW has been above the 90-day MA. It’s still too early to make any concrete statements here but Monster may be pricing in an intermediate-term job market recovery.

E-bay (EBAY) was up nearly 8% on April 9 and is now putting some distance between its price line and the underlying 30/60/90-day MA series as the impressive turnaround in this indicator of the micro-business economy continues. EBAY hasn’t shown this much spunk in over a year and apparently the stock smells a turnaround in online transactions in the foreseeable future.

The fourth component of our economic index is Amazon.com (AMZN). AMZN has been on a rip-and-tear in recent months and we’ve been fortunate to have profited from its recent rally as AMZN is part of our official MSR stock portfolio. AMZN just reached our conservative short-term target of $80, at which point we’ve taken some profit on the stock already (see Trading Positions section below). AMZN is pointing to a definite recovery in online retail trade and we should see visible signs of this by mid-summer at the latest.

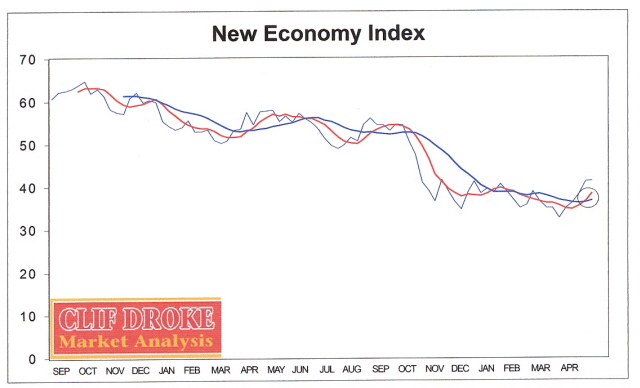

The final component of our leading economic index is Wal-Mart (WMT), the top retailer in the U.S. In contrast to the other four components of the index, WMT didn’t fare too well last week and was down nearly 4% on Thursday on high volume. WMT has always been an enigma, underperforming when common sense dictates it should be doing well and outperforming when by all accounts it should be doing poorly. I don’t place much faith in its movements one way or the other except that it still constitutes an important leg of the retail sector outlook. As such, its only reflection is how its weekly stock prices impacts the average price in the New Economy Index (NEI). Here’s what the latest NEI looks like as of April 9.

The two key moving averages for this kind of indicator are the 5-week and the 12-week simple moving averages. The 5-week is a reflection of the 10-week Kress cycle while the 12-week MA is the half-cycle component of the important 24-week cycle. The interaction between these two cycles is important for determining short- and intermediate-term directional bias. As you can see here, the 5-week MA has crossed above the 12-week MA. Moreover, and in contrast to the previous upside crossover (which proved to be a failure), the index price line itself has made a higher high above the previous highs. This makes it all the more likely that the “bullish” moving average crossover will stick this time and this in turn points to an intermediate-term economic recovery.

One of the key structural flaws in modern economic thought is the fallacy of “satiation economics.” This theory states that at some point along the curve, human wants become satisfied by production, and if production of those goods that satisfy continues then over-production results. This in turn leads to a glutting of supply and eventually to crashing prices. Keynesian economists are particularly fond of this fallacy and have offered it as one of the causes of the Great Depression of the 1930s.

Common sense observation teaches quite the opposite of this untenable position, namely that human desires are never fully satisfied and there can never be too much production. This is something that the great industrialist Henry Ford believed in and the success of his company is surviving the Depression attests to the veracity of it. Simply put, demand for goods and services is a constant and can never be satisfied, only suppressed. It is the lack of money which is the root of economic crises, not a surplus of goods or a general satisfaction of consumer desires.

Even during periods of economic contraction when people are afraid to spend money and become fiscally conservative the average worker has a mental list of all the things he plans to buy just as soon as money supply starts flowing again. Recessions don’t “cure” human greed – they only postpone its visible manifestation.

There is a popular idea being circulated in the financial press that consumer will only become more conservative when and if the money starts to flow. They will supposedly use the increase in financial liquidity to shore up their personal debts and save whatever they can rather than spend, or so we are told.

The reality is that they will spend whatever increase in money they obtain to satisfy those never-ending desires as is always the case following a period of severe monetary contraction. It is the proverbial spring being released and pushing things to the opposite extreme of the bust-boom cycle. When the concerted efforts of the feds at galvanizing the economy succeed, as is inevitable at this point, we will see consumers come out of their cocoons and start spending again.

By Clif Droke

www.clifdroke.com

Clif Droke is the editor of the daily Gold & Silver Stock Report. Published daily since 2002, the report provides forecasts and analysis of the leading gold, silver, uranium and energy stocks from a short-term technical standpoint. He is also the author of numerous books, including 'How to Read Chart Patterns for Greater Profits.' For more information visit www.clifdroke.com

Clif Droke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.