Remembering Wharton: Detecting When the Fed Turns 'For or Against You'

Commodities / Gold and Silver 2021 Dec 22, 2021 - 12:22 PM GMTBy: The_Gold_Report

Precious metals expert Michael Ballanger remembers lessons learned years ago from a three-year course in "Stocks and Bonds 101," and how those principles still apply today.

In 1983, I was offered the opportunity to attend a three-year course in “Stocks and Bonds 101” courtesy of the Securities Industry Association. With little or no appreciation of what that course might actually do for me, I eagerly accepted because the main perk was a shingle for my office emblazoned with the title “The Wharton School” with my name just below it and signature-verified by a bunch of northeast blue bloods.

That three-year journey had a remarkable impact on my psyche. I met some of my earlier heroes like Martin Zweig, Jeremy Seigel, Julius Westheimer, and Gail Dudack, all of whom were really interesting personalities. But none were as impactive as a little-known trader called Robert Gordon. At first glance, I thought that he was the perfect image of a New Yorker – a cross between Robert DeNiro and John Travolta but, at maybe 5 feet 9 inches tall, at least a few inches taller. He was a disciple of the legendary Ivan Boesky (an arbitrageur who went to prison for insider trading in 1987), known for his understanding and skill in the art of taking advantage in inefficiencies in securities pricing.

“It is the moment in the cycle when the Fed turns 'for or against you' that one must detect, especially with today’s financial theater of excess debt and razor-thin leverage.”

—Michael Ballanger

During one of Gordon’s lectures, he explained to us what was then (1985) a rather obscure notion that an entity called “the U.S. Federal Reserve” was the primary driver for stock prices, but more importantly, he said the moment when policy shifted from “stocks friendly” to “stocks hostile” was when portfolio adjustments should be executed.

I remember a quote from the famed movie actor Omar Sharif, a very successful global bridge player and gambler who, when asked to what he attributed his phenomenal success “at the tables,” responded: “One must always be able to detect the moment in the evening when the cards turn for or against you.”

Applied to stocks, it is the moment in the cycle when the Fed turns “for or against you” that one must detect, especially with today’s financial theater of excess debt and razor-thin leverage.

I maintain that in the last three FOMC meetings that the risk-asset “cards” have turned against investors with the elimination of the word “transitory." Elevating the S&P 500 in order to boost the asymmetrical wealth effect has been supplanted with a return to one of the two principal mandates of the Fed (full maximum employment and price stability) and it is the new kid in town that falls under the category of “fighting inflation.” More importantly, when the noise you hear from the Marriner S. Eccles Building is no longer the popping of champagne corks every time the NASDAQ hits a new high but rather the clamor one hears after oil drops another few dollars per barrel, you know the punch bowl has been removed and that “the cards have turned.”

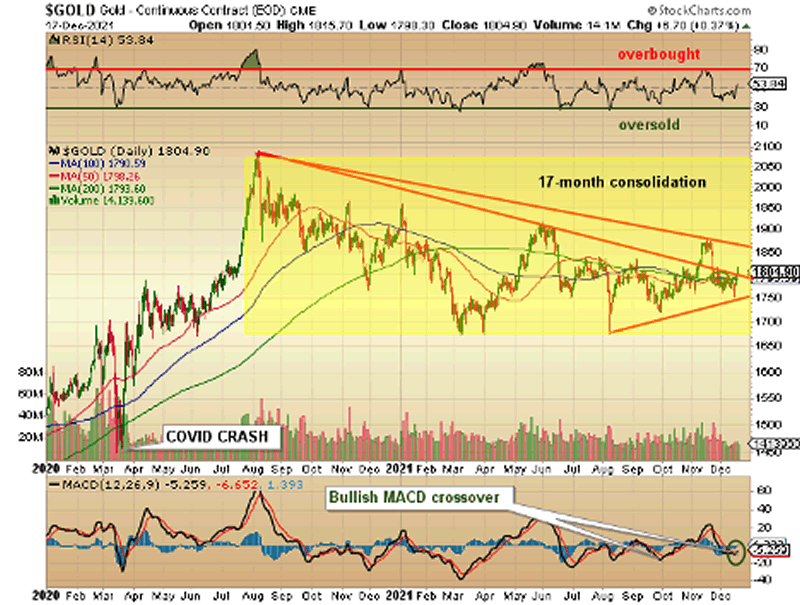

This is one of the primary factors explaining the inability of gold and silver to respond to the inflation numbers recently reported and decidedly “hot.” In this manner, gold and silver are responding as the barometers of impending weather change, and since sunny skies for the precious metals is the period of declining real interest rates (Fed Funds rate minus CPI), they are truly executing their historical predictive abilities and are acting as barometers of an approaching storm triggered by a pending reversal in the trend of the Fed Funds rate. It has been in decline for forty years during which gold has gone from $250/ounce to $2,100/ounce, so the current $1,800/ounce level is apparently discounting what we are all now reading and hearing – that the new bogeyman in the room is no longer the wealth effect but rather the spike in consumer prices. In other words, the Fed no longer has the backs of the Wall Street crowd but instead the backs of the Main Street crowd, and that's simply politics at its ugliest.

I have made no secret my detest for the entire banking fraternity around the world. Prior to the Four Pillars being torn down in the 1980s, real estate sales, insurance, banking, and brokerage were not allowed to be combined; they had to stick to their knitting, so to speak. And as a former member of the brokerage industry, I recall the whining and bitching that happened when the banks began buying all of the old venerable brokerage houses such as McLeod Young Weir (Scotia), Wood Gundy (CIBC), and Dominion Securities (RBC). The common wisdom was that letting creativity-starved, boring bankers into the room with the far more aggressive and entrepreneurial risk takers in the brokerage industry would result in a smothering of growth and innovation. It would be like opening the door of the beer fridge in your garage in July to try to cool off the garage – never going to happen. However, one thing that the naysayers failed to comprehend was the one catalyst that could ever transform the conservative thinking of the bankers into the aggressive behavior of the brokers was the only lubricant required for kinetics to evolve – greed. For years and years, the privately owned brokerage firms had employee payouts literally five times that of their banker brethren but once the banks were allowed into the securities racket, they leveraged their “favored status” with the politicians and the regulators and took greed to another level. In the days when the BNA Act forbade bankers from speculating with depositor savings, money was protected and nurtured by boring bankers while wild-eyed speculation was the habitat of the flamboyant brokers, be it buying bonds on margin or bets on the future price of pork bellies via the futures markets.

Alas, what happened in effect was that those beer fridges were more akin to nuclear greed reactors so when they opened them up, the garages went volcanic in record time and with infinite contagion. The sad reality of the dotcom bubble and the subprime bubble and now the “Everything” bubble is that the wild-eyed gunslinger/speculators of the pre-1980s era could never have blown up the financial system because they were constrained by a lack of capital but once the shackles of regulatory restraint were thrown off in the name of globalism, the bankers used infinite leverage along with unlimited capital (debt) fully-condoned by the politicians to advance their profits while transforming the financial system into a global “Fail-Safe” mechanism.

For bankers, the one constant that guarantees them a raise every year is the persistent increase in the amount of money circulating in the economy (M2) because it all has to get filtered through the banking industry and whether it is the mortgage that allows them to control your home or the fee they charge you to store your paycheck every month, they get their pound of flesh no matter what the occasion.

So, when I am constantly haranguing about the Fed, it is because the mainstream media, led by CNBC, portrays the Fed as the caretaker of public’s financial welfare while nothing could be further from the truth. All of this “stimulus” results in more and more currency sloshing around the system. The brokers love to talk about their “AUM” (Assets Under Management”) because most now operate on a fee-based compensation system so if you are charging a flat 2% fee, then your total “comp” is based solely on AUM. Similarly, since banks as an industry also operate on a fee-based system, when the Fed and the Treasury (or Bank of Canada and Parliament) open up the spigots and inflate the money supply, they by default increase the AUM for an entire industry. What I rage on about is that not one other citizen or business benefits from a debasing of one’s domestic currency but since central banks were created by and for their members (the banking industry), then pandemics and financial crises and market crashes all provide the needed cover for the banks to a) secure the collateral behind their loans and b) provide a larger pool of capital (AUM) upon which they can charge fees. The ultimate form of “inflation-indexed compensation” is the paycheck earned by a banker. The more inflation they create, the more fees they charge – and it drives me bonkers.

As I head into the last two weeks of 2021, I look at the GGMA portfolio and see five winners versus three losers with the best gain in Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) (up 73.53% YTD) with the worst being Norseman Silver Ltd. (NOC:TSX.V)(down 38.75% YTD). The portfolio is having a good year relative to other precious metals portfolios, sporting an average gain of over 20% but since the portfolio was overweighted in Getchell (56.14% allocation), the net gain in the portfolio for the year is 59%. It should be noted that it was up a great deal more in November prior to the big uranium meltdown (Western Uranium & Vanadium Corp. (WUC:CSE; WSTRF:OTCQX) was up over 354% in November only to succumb to profit-taking and now sports a return YTD of “only” 60.55%).

If the truth were to be known, this year has been a disappointment for many (if not most) gold and silver investors because if you did not have Great Bear or Pretium or Amarillo, you were the proverbial jilted bride standing abandoned at the altar. We got financial turmoil (Evergrande defaults); we got global stimulus (everywhere); and we wound up with spiraling consumer prices (6.8% CPI). What we did not get was anything close to a tradable rally in the precious metals sector. The biggest slap in the face was silver, where every market maven and podcast promoter got it totally wrong. The “Electrification Trade” looked great in May and it looks awful here in December while my “sell signal” on oil back in November above USD $80/bbl. was a retrospective exercise in contrarian investing. Everywhere I looked back then, I saw “Oil to $150!” plastered from stem to gudgeon.

The investment forecast is now “in flux” and all of the assumptions, including mine, are open for extreme scrutiny. John Maynard Keynes is cited quite often as the originator of the quote “When the facts change, I change my mind,” or as I like to say, “When conditions change, I change.” We have had everything but the kitchen sink thrown at the global economy in the form of gold-bullish and silver-bullish stimulus and yet gold remains down 5.72% YTD and silver down 15.38% YTD while the S&P500 is ahead 25.98% YTD. Furthermore, we are heading into the final two weeks of the trading year with Fed’s message stating quite clearly that inflation is their top priority now which implies that they have gone “hostile” and that nice warm feeling stock investors have had in their lower backs since March of 2009 has now become a poisoned dagger aimed at their spines. The dichotomy I now face lies in the need for the PMs to become “the only game in town” but with a hostile Fed, one has to wonder how sentiment for the precious metals can change for the better.

I think it lies in gold’s uncanny ability as a barometer to signal a change in policy. It sensed a shift in May of 2019 during Jerome Powell’s lame attempt at “balance sheet normalization” by beginning the ascent from USD $1,269 to over $1,500 by the time the REPO moves bailing out the hedge funds long “junk” (high-yield) bonds were revealed.

Once the world accepts this sad and painful truth and legislates the practice into oblivion, free market capitalism returns and the playing field levels out.

This will be my final missive for the year with the 2022 Forecast Issue scheduled for a New Years Day release, so to all of my subscribers, followers, friends, and foes, enjoy the season and may 2022 be a good one.

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at miningjunkie216@outlook.com for subscription information.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.