US Housing Market Crunching Banks, Earnings and Economy

Housing-Market / US Housing Aug 03, 2008 - 06:38 PM GMT

Housing, credit and labor … oh my! -“Recent data releases and reports suggest that the consumer will continue to be pressured on all fronts: income (or cash flow), wealth and credit. Consumers can spend using any of these buckets. However, with the labor market continuing to weaken, housing continuing to deteriorate and credit harder to come by, the outlook for spending remains bleak despite recent declines in gasoline prices.

Housing, credit and labor … oh my! -“Recent data releases and reports suggest that the consumer will continue to be pressured on all fronts: income (or cash flow), wealth and credit. Consumers can spend using any of these buckets. However, with the labor market continuing to weaken, housing continuing to deteriorate and credit harder to come by, the outlook for spending remains bleak despite recent declines in gasoline prices.

“High inventories suggest still-falling house prices putting further pressure on consumers' balance sheets. Although new home inventories declined in the latest month, the supply of both new and existing homes on the market remains elevated. As existing homes are occupied by consumers (as opposed to owned by builders) and with existing home sales making up more than 90% of all home sales in June, the high level of inventories in this category may be more meaningful to the consumer. Indeed, the low level of turnover in occupied homes suggests that more consumers may be feeling stuck in a losing trade.

“Access to credit is likely to become harder to come by and more expensive. The just released Beige Book appeared to capture some of the not-yet released Senior Loan Officer Survey for July (we estimate the release of this survey on 11 August). The Beige Book noted that ‘most districts reported a further tightening of credit standards…' Given how tight banks' lending standards have already become, it is hard to fathom how much tighter standards can get.

“Consumer cash flows seem unlikely to improve anytime soon. The labor market weakness evident in the claims figures suggest continued weakness in non-farm payrolls.

“The Treasury's refunding announcement will highlight the adverse effects on the budget of the rebate program and the risk to the budget posed by additional stimulus packages. We believe the deteriorating funding outlook may prompt the Treasury to re-introduce the 3-year note. This would be the second security re-introduced by the Treasury this calendar year as the Treasury responds to the worsening fiscal outlook.”

Drew Matus (Merrill Lynch): - Click here for the full report.

Source: Drew Matus, Merrill Lynch – The Market Economist , July 25, 2008.

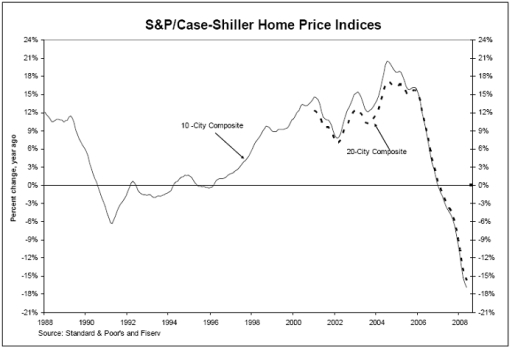

Standard & Poor's: S&P/Case-Shiller Composite Home Price Indices – record low annual declines

“Data through May 2008, released today by Standard & Poor's for its S&P/Case-Shiller1 Home Price Indices, the leading measure of US home prices, show annual declines in the prices of existing single family homes across the United States generally continued to worsen in May 2008. For the second straight month, all 20 MSAs posted annual declines, nine of which are posting record lows and 10 of which are in double-digits.

“The chart above depicts the annual returns of the 10-City Composite and the 20-City Composite Indices. Both composite indices continue to report annual declines in excess of 15.0%. The 10-City Composite posted a new record low of -16.9%, and the 20-City Composite recorded a record low of -15.8%.

“‘The overall real estate market continued to slide in May, with the 10-City and 20 City Composites declining by 1.0% and 0.9% for the month, respectively. Since August 2006, there has not been one month where we have seen overall price increases, as measured by the two Composites, says David M. Blitzer, Chairman of the Index Committee at Standard & Poor's.”

Source: Standard & Poor's , July 29, 2008.

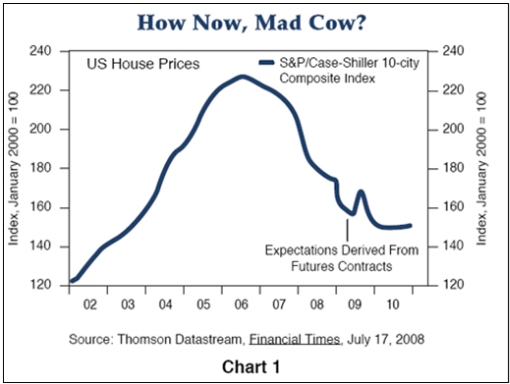

Bill Gross (Pimco): Mooooo!

Source: Bill Gross, Pimco , August 2008.

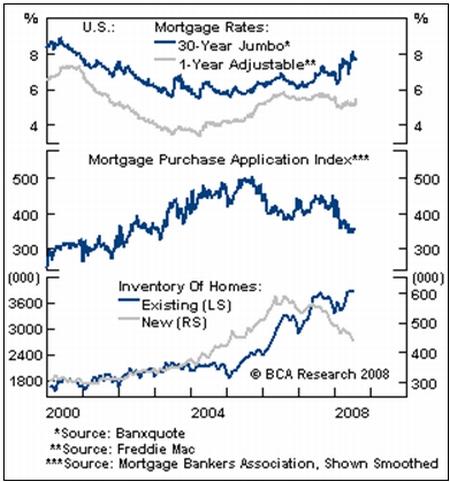

BCA Research: US housing – from bad to worse?

“Rising mortgage rates and mounting inventories warn that the US housing slump is far from over.

“Congress is trying to ease the burden on stretched homeowners, and moved decisively to prevent a meltdown in the GSEs. However, while positive, these efforts are not sufficient to turn things around. The ongoing economic slump and intense inflation fears are worsening the already grim housing outlook.

“Bond yields have risen in recent months, pushed up by increasing inflation concerns and comments from some members of the FOMC – Federal Open Mouth Committee. Financial institutions are also (belatedly) widening spreads and tightening lending standards.

“Moreover, the stock of unsold houses remains far too high to stabilize house prices, especially existing home inventories which hit a new high last month. Bottom line: Mortgage rates and inventories need to decline before housing stabilizes. Until then, the economy and banking system will remain at risk.”

Source: BCA Research , July 28, 2008.

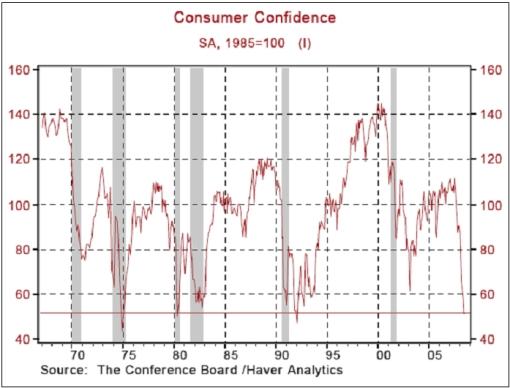

Asha Bangalore (Northern Trust): Consumer Confidence Index stabilizes, but consumers pessimistic about jobs

“The Conference Board's Consumer Confidence Index moved up slightly to 51.9 in July from 51.0 in June. The June reading of the index appears to be the cycle low, for now. The July report suggests that the outlook of consumers is stabilizing.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary , July 29, 2008.

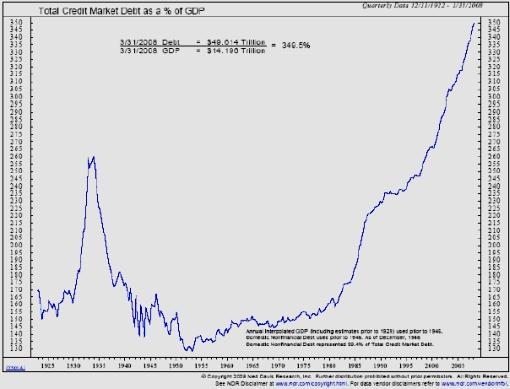

Bill King (The King Report): Has deleveraging even begun?

“… the scariest chart known to mankind”.

Source: Bill King, The King Report , July 30, 2008.

The New York Times: Worried banks sharply reduce business loans

“Banks struggling to recover from multibillion-dollar losses on real estate are curtailing loans to American businesses, depriving even healthy companies of money for expansion and hiring.

“Two vital forms of credit used by companies – commercial and industrial loans from banks, and short-term ‘commercial paper' not backed by collateral – collectively dropped almost 3% over the last year, to $3.27 trillion from $3.36 trillion, according to Federal Reserve data. That is the largest annual decline since the credit tightening that began with the last recession, in 2001.

“The scarcity of credit has intensified the strains on the economy by withholding capital from many companies, just as joblessness grows and consumers pull back from spending in the face of high gas prices, plummeting home values and mounting debt.”

“‘The second half of the year is shot,' said Michael T. Darda, chief economist at the trading firm MKM Partners in Greenwich, who was until recently optimistic that the economy would continue expanding. ‘Access to capital and credit is essential to growth. If that access is restrained or blocked, the economic system takes a hit.'

“Companies that rely on credit are now delaying and canceling expansion plans as they struggle to secure finance.”

Source: Peter D. Goodman, The New York Times , July 29, 2008.

James Quinn (Telegraph): Merrill Lynch bids to raise $8.5 billion as it faces further writedowns

“Merrill Lynch is to raise an extra $8.5 billion in fresh capital on top of $23.5 billion already raised in the past 12 months as the beleaguered investment bank took some drastic steps to right its capital position.

“Merrill, which just two weeks ago announced plans to raise almost $8 billion from asset sales including its 20% stake in financial news provider Bloomberg, revealed that it needs to raise the money after disclosing that it will take a financial ‘hit' of $10.6 billion in the third quarter.

“The news will come as a surprise to the financial community, which had hoped that the worse was over for Merrill, which has already been one of the largest victims to date of the continuing credit crisis.

“Prior to this latest series of writedowns and exceptional losses, Merrill has already written down $40 billion in assets and other instruments.

“But chairman and chief executive John Thain said that the news was positive, because of the fact it has been able to off-load the ‘substantial majority' of its positions in a certain type of complex debt vehicle.

“Mr Thain, who took over from Stan O'Neal last December, said the news marked a ‘significant milestone in our risk reduction efforts'.”

Source: James Quinn, Telegraph , July 29, 2008.

Financial Times: Banks pressed to follow Merrill's debt sale

“Leading global banks including Citigroup and UBS on Tuesday faced renewed pressure to write down or sell billions of dollars in toxic assets following Merrill Lynch's disposal of $30 billion in mortgage-related securities at a cut price.

“Merrill's move to sell collateralised debt obligations (CDOs) for $6.7 billion, or 22 cents on the dollar – announced on Monday night – raised hopes that other banks would be able to strike similar deals and purge their balance sheets of bad assets.

“However, the low price paid by Lone Star Funds, a distressed debt investor, to buy Merrill's CDOs sparked fears that the financial system could enter another spiral of huge writedowns followed by highly dilutive capital raisings.

“Merrill on Tuesday raised $8.5 billion – to offset $5.7 billion of writedowns caused by the CDO sales and other losses – by selling shares at $22.50, a 7.5% discount to Monday's close.

“Mike Mayo, Deutsche Bank analyst, said Merrill's action, a fortnight after John Thain, chief executive, said that it did not need more capital, ‘raises ongoing credibility issues for the industry'.”

Source: Francesco Guerrera, Ben White and Henny Sender, Financial Times , July 29, 2008.

Financial Times: Pimco's Joe McDevitt on bonds and inflation

“Joe McDevitt, head of Pimco Europe's London office, talks to Pauline Skypala about bonds, inflation and how Pimco, as bond house, aims to make money in a time of higher inflation, which historically has not been good news for bonds. He also explains how Pimco managed to avoid subprime exposure.”

Source: Financial Times , July 28, 2008.

David Pfaendler (Dresdner Kleinwort): Bond yields to fall

“Developed market bond yields should move markedly higher through the rest of this summer, but then fall sharply going into 2009, says Daniel Pfaendler, head of G10 economics & strategy at Dresdner Kleinwort.

“He believes the oil price shock and the unwinding of asset bubbles, over-leverage and economic imbalances in general should keep growth significantly below trend and real yields depressed for a protracted period of time.

“‘Price stability-oriented central banks – having learned their lessons from the 1970s – should become more hawkish in the near-term, thereby limiting the upward pressure on long-run inflation expectations,' Mr Pfaendler says. ‘As a result, we are convinced that the deflationary forces of the ‘Great Unwind' should gain the upper hand in 2009 and thereby bond markets in the developed world will not break out of the environment of structurally low yields which has been ruling over the current decade.'

“However, he believes inflation will peak around autumn and then fall significantly into 2009.

“He adds that the positive growth effects of US tax rebates should dissipate, raising the risk of a simultaneous recession in the US, the eurozone and the UK during winter.

“‘Therefore, real yields and inflation expectations should be able to fall in tandem, making long-duration as well as curve-steepening exposure across developed bond markets attractive again.'”

Source: Daniel Pfaendler, Dresdner Kleinwort (via Financial Times ), July 29, 2008.

Richard Russell (Dow Theory Letters): Message to foreign creditors

“We owe our foreign creditors billions of dollars. Furthermore, our foreign creditors already own hundreds of billions of dollars. And our foreign creditors' big worry, among other worries is – what happens if the dollar really tanks? Foreign holders of US dollars have already lost billions due to the slumping dollar. Yet, above all, the US needs our creditors holding on to their dollars and buying ever-more US bonds. What to do?

“Do you remember Treasury Secretary Paulson rushing all over the world — Beijing, Moscow, Berlin, Tokyo – you name it. What was he doing? I think he was beseeching our creditors, ‘Look, you've got to help us and at the same time help yourself. Hold on to your US bonds, hold on to your Fannie and Freddie paper, keep buying our paper and our bonds. If you don't, we're all facing a catastrophe.

“‘The dollar on a purchasing power parity is ridiculously cheap now. And as soon as possible, we'll raise rates and that will strengthen the dollar. In the mean time, we'll talk the strong dollar. And we promise that we will not let the dollar hit the skids. A stronger dollar will help us and help you. Just hold our bonds, hold our paper, and keep buying our bonds. Furthermore, we'll allow your Sovereign Wealth Funds to buy our assets. Buy all of the US you want. But rest assured, WE WILL DEFEND THE DOLLAR.'

“In my opinion, that was the deal. That was the reason why Paulson was running all over the world with his secret message.”

Source: Richard Russell, Dow Theory Letters , July 30, 2008.

Reuters: US Treasury to boost 10-year note sales

“Faced with a swelling federal budget deficit as a slowing economy saps tax revenues, the US Treasury is expected to boost the frequency of 10-year note sales and offer more 30-year bonds next month.

“Analysts estimate the Treasury will announce plans to sell $15 billion to $16 billion in 10-year notes and $9 billion to $10 billion in long bonds at its refunding announcement on Wednesday.

“‘There's a realization that these higher deficits are going to be with us for a while because the outlook for growth in the second half and into next year has deteriorated,' said Lou Crandall, chief economist at Wrightson ICAP in Jersey City, New Jersey. ‘It's an appropriate time for the Treasury to be locking in some longer-term borrowing.'”

Source: David Lawder, Reuters , July 25, 2008.

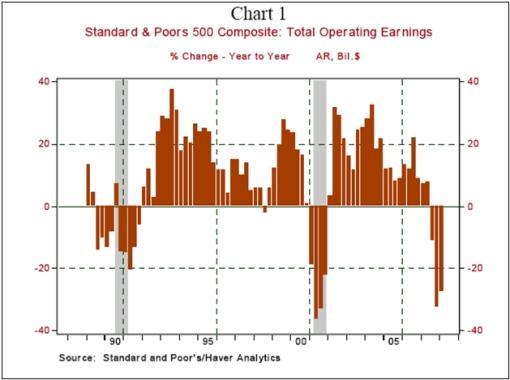

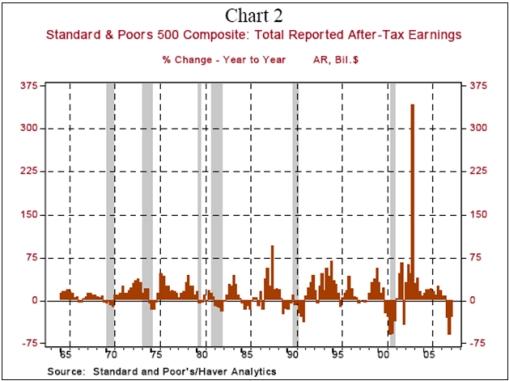

Paul Kasriel (Northern Trust): S&P 500 corporate profits leave little recession doubt

“Are we in a recession or are we not? The debate goes on. Take a look at the year-over-year change in operating profits of the S&P 500 corporations (see Chart 1). Profits have declined for three consecutive quarters through the first quarter of this year. Given reports of second-quarter profits to date and estimates of those corporate profits to be reported, it is a good bet that year-over-year profits will be down for four consecutive quarters. The data series in Chart 1 only goes back to the first quarter of 1989. But these limited data points suggest that the current behavior of corporate profits is signaling a recession. The data for year-over-year changes in reported S&P 500 profits (see Chart 2) start in the first quarter of 1965. The message is the same – current corporate profit behavior is consistent with past behavior in periods of recession.”

Source: Paul Kasriel, Northern Trust – Daily Global Commentary , July 28, 2008.

Richard Russel (Dow Theory Letters): Is bull still alive?

“… could we be watching a vicious but erratic correction in an ongoing bull market? As far as I'm concerned, this is the multi-trillion dollar question of the day and the month and the year. Because if this is a correction rather than a primary bear market, then this market could tend to hold, and this market could be building a base. And if so, then 18 billion shorts will begin to get squeezed. And if this market is in the process of building a base, then the big money will begin, slowly and subtly, to re-enter the market.”

Source: Richard Russell, Dow Theory Letters , August 1, 2008.

David Fuller (Fullermoney): Outlook for Western banks?

“Fullermoney has been very cautious regarding Western banks for a number of months, not least because of the weak performance and obvious fundamental problems. Consequently we emphasised that a lengthy convalescence would be required. However bank shares were driven down to eyebrow-raising levels, with the help of record short selling, prior to a rebound earlier this month.

“What can we conclude about the Western banks today?

“I would now describe my view as cautiously bullish, which requires some explanation. Cautious because some further write downs and dilution of shareholders' equity remains possible, and even if this was discounted by the recent lows, I do not see a business model for rapid recovery. In other words, while it would be a relief to see less cowboy capitalism from the banks, profits growth under more conservative management policies is likely to seem pedestrian for a while, not least while the deflationary, recessionary winds continue to blow.

“Taking a longer-term view, I would not be surprised to see a signification consolidation within the Western banking industry over the next few years. This will inevitably favour the strong players. Meanwhile, conservative investors may prefer bank bonds to equity.

“Looking at the charts' action for bank indices such as S&P 500 Regional Banks, DJ Euro Banks and FTSE 350 Banks, we certainly had climactic action in mid-July, as pointed out at the time. We have also seen some of the biggest rallies since bear markets for the deeply troubled Western bank sectors commenced, not least because of short covering. That probably marks at least the beginning of the bottoming out process.

“While these bank indices have eased in the last three days, after encountering overhead resistance evident from the January-March range lows, they have retained more of the recent rally than broader indices in the USA, Continental Europe and the UK. This may have something to do with the recent investigations regarding shorting, but it could also indicate that the banks themselves are less bearish of their sector. From a bullish perspective, it would be encouraging if bank indices maintained their recent relative strength and also held at least half of this month's gains.”

Source: David Fuller, Fullermoney , July 28, 2008.

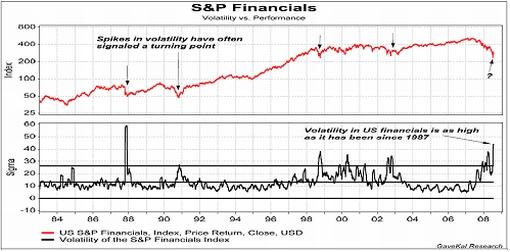

GaveKal: S&P Financials – Spikes in volatility usually signal turning points

Source: GaveKal – Checking the Boxes , July 29, 2008.

Paul Danis (Lehman Brothers): Japanese rally has legs

“The outperformance of Japanese stocks over the past few months looks set to continue, believes Paul Danis, equity strategist at Lehman Brothers.

“‘After strongly underperforming from early 2006 to March this year, Japan has outperformed the global equity market by 14% in dollar terms and 24% in local currency terms since mid-March,' he says. ‘We think that the rally has legs.'

“Mr Danis notes that the total cash yield in Japan has bucked the global trend and kept rising as net stock buybacks have increased, in contrast to the US and UK. ‘We view this development as supportive for two reasons. First, it reduces equity supply. Second, it is a vote of confidence from the Japanese corporate sector.'

“Mr Danis also says that while the economic backdrop in Japan is far from great, he expects growth to be strong relative to the rest of the world. ‘Some key Japanese economic indicators are showing resilience, and there are continued signs that Japan's economy is exiting a deflationary period.'

“He adds that analysts have aggressively marked down Japanese company earnings expectations, while for the World ex-Japan composite, earnings are still at peak levels. ‘There is scope for this gap to close, which should benefit Japanese stocks relative to global markets in aggregate.

“‘We recommend investors with a global mandate overweight Japan in equity-dedicated portfolios.'”

Source: Paul Danis, Lehman Brothers (via Financial Times ), July 28, 2008.

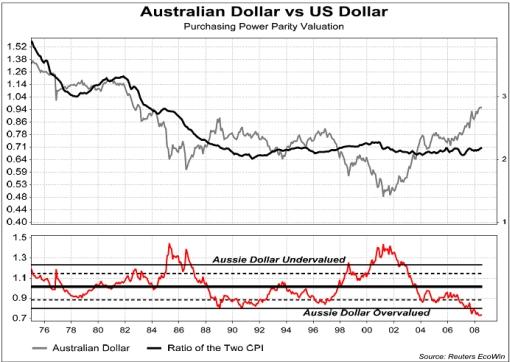

GaveKal: Australian dollar grossly overvalued against US dollar

Source: GaveKal – Checking the Boxes , July 28, 2008.

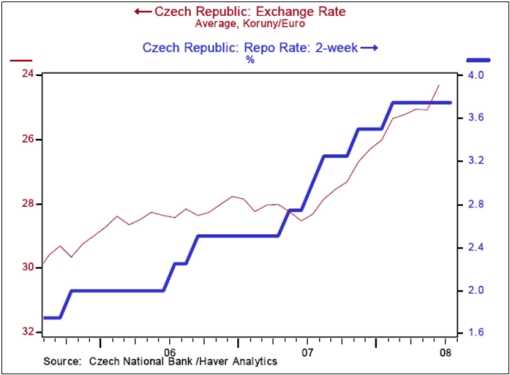

Victoria Marklew (Northern Trust): Central European currencies running out of steam?

“The three major currencies of central Europe have appreciated strongly against the euro so far this year, boosted to varying degrees by rising interest rates, strong economic growth, and positive investor sentiment – the latter buoyed by the final confirmation that Slovakia will adopt the euro next January. However, there are some preliminary signs that the region's strong growth rates are about to slow. Interest rates may be at their peak in Poland and Hungary, and a rate cut may be in the cards in the Czech Republic. All of which suggests that the Polish zloty, Czech koruna, and Hungarian forint may also have peaked for now.

“With Eurozone membership coming up next January, Slovakia's central bank is focused on keeping its policy rate level with the ECB's refi rate. As a result, the bank yesterday left its two-week repo rate unchanged at 4.25% and will follow any subsequent ECB moves in the run-up to January 1. In the Big Three, however, the picture is more complicated. All three have been hit by a surge in inflation thanks to rocketing food and fuel prices. June's (EU-harmonized) annual rate came in at 6.7% in Hungary and in the Czech Republic, and at 4.6% in Poland. Currency appreciation has helped to restrain import price pressures somewhat in all three countries, but the Hungarian and Polish central banks remain biased toward tightening. However, the Czech central bank has shifted to a more dovish stance, and may even lower its policy rate next week.”

Source: Victoria Marklew, Northern Trust – Daily Global Commentary , July 30, 2008.

Financial Times: Zimbabwe to lop zeroes off currency

“Zimbabwe's economy is unravelling at such a pace that the central bank is set to slash yet more zeroes from the country's increasingly worthless currency.

“State media on Sunday quoted Gideon Gono, the Reserve Bank of Zimbabwe governor and one of the members of the ruling elite targeted by fresh western sanctions last week, as saying he would extend a currency policy that has so far failed to stem hyperinflation.

“‘This time, we will make sure that those zeroes that would come knocking on the governor's window will not return,' Mr Gono was quoted as saying on Saturday in a speech to farmers.

“Independent estimates put Zimbabwe's inflation rate well above the official 2.2 million per cent, prompting the introduction last week of a 100 billion Zimbabwean dollar note. Even state media reported Mr Gono's comments ‘drew laughter' from his audience.

“The governor is expected to chop three or six zeroes from the currency, following a three-zero cut in 2006.

“Beside the inflationary zeroes haunting Mr Gono, analysts and some opposition politicians say the crumbling economy in what was once a regional bread basket is perhaps the single greatest factor that might force Robert Mugabe, president, into relaxing his grip on power.”

“The government blames the economic strife on ‘illegal' sanctions, condemning opponents who point to violence land seizures that have contributed to a drastic fall in agricultural output.”

Source: Tom Burgis and Tony Hawkins, Financial Times , July 27, 2008.

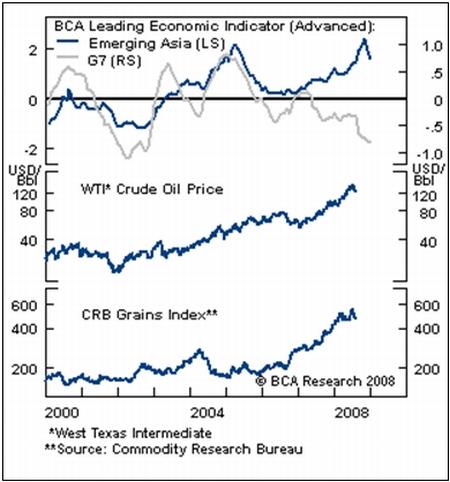

BCA Research: Food and energy prices – prolonged correction underway?

“Global growth is downshifting and the cyclical economic backdrop is no longer supportive of further commodity price gains.

“Inflation angst should begin to recede now that food and energy prices are gradually coming off the boil. As prices continue to correct, it should become clear that prior price increases have not filtered into a generalized inflation upturn, and consumer prices remain under control (at least in developed countries). Our Leading Economic Indicator (LEI) for the G7 shows no signs that weakness is approaching an end and the emerging Asia LEI is warning of a cooling in the rapidly growing developing world, led by a softening in the Chinese economy.

“The weaker growth outlook along with reductions in energy subsidies, and a tightening in policy by several emerging market central banks (because of inflation concerns related to the commodity boom) will only reinforce the tendency for commodity demand growth to slow.

“Bottom line: Prices are set to correct further and the inflation scare should retreat along with expectations for rate hikes.”

Source: BCA Research , July 30, 2008.

David Fuller (Fullermoney): Oil price key to global GDP growth and stock markets

“1. The oil price is currently by far the most important factor in terms of global GDP growth. Consequently it is also a huge influence on the direction of various stock market indices, and big moves up or down have a psychological leash effect on other commodities, including gold.

“2. Supply and demand for crude oil is difficult to forecast, at the best of times, which these are not. In recent years, supply has probably been adversely affected by costs and shortages of manpower or equipment, at least as much as depletion. Demand is inevitably price sensitive, not least during spikes.

“So where do we stand in terms of the Peak Oil debate?

“I am a long-term believer in Peak Oil but a short-term sceptic. Even some of the best and most farsighted analysts often predict dramatic, seminal events many years before they actually occur, not least I suspect because life is short and our time is precious.

“Meanwhile, the daily chart of crude oil has shown increasingly conclusive evidence of a significant peak commencing with that big downward dynamic on 15th July.”

Source: David Fuller, Fullermoney , July 29, 2008.

Reuters: Gold options point to $1,200

“Heavy bets in deep out-of-the-money calls and other bullish plays in the gold options market indicate bullion has a shot at rallying to an all-time peak of $1,200 an ounce by the end of the year.

“Gold has soared furiously – a few years ago the metal was trading at $250 an ounce – as investors poured into the market due to inflation fears, a weakened dollar and market turmoil.

“‘There are a lot of people who think that by the end of the year we'll be trading $1,200 to $1,500. They are not very expensive options, so people are buying them,” said John Bilello, COMEX gold options floor trader.

“Bilello said that many option investors were currently adjusting positions after gold's sharp fall but he saw recent strong volume of December $1,000 calls, bull call spreads between $1,200 and $1,300, and the selling of put options – all of which are betting that gold will rise further.”

Source: Frank Tang, Reuters , July 25, 2008.

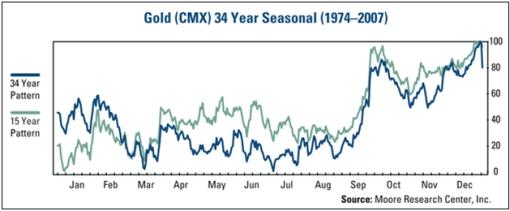

Frank Holmes (US Global Investors): Consider gold now

“The fundamentals for gold have not changed, and with negative real interest rates in the US, this is a good time to maintain exposure to gold investments. As you can clearly see from the chart below, July and August generally mark a low time for gold before prices climb with the arrival of the fall buying season, which is another reason to consider gold now.”

Source: Frank Holmes, US Global Investors – Weekly Investor Alert , August 1, 2008.

Bloomberg: European inflation quickened to 16-year high in July

“Inflation in Europe accelerated to the fastest pace in more than 16 years in July, restricting the European Central Bank's room to bolster the economy even as unemployment starts to increase.

“The inflation rate for the 15-nation euro region rose to 4.1% from 4% in June, the European Union statistics office in Luxembourg said today. The rate, the highest since April 1992, matched the median estimate of 36 economists in a Bloomberg News survey. A separate report showed unemployment was 7.3% in June, exceeding the 7.2% median forecast.

“The ECB, which aims to keep inflation just below 2%, raised its key interest rate by a quarter point to 4.25% on July 3, a seven-year high. The risk is that higher borrowing costs will exacerbate the economic slowdown. Europe's manufacturing and service industries are contracting and confidence in the economic outlook this month plunged the most since the September 11 terrorist attacks in 2001.”

“‘The growth outlook has deteriorated,' said Martin van Vliet, an economist at ING Group in Amsterdam, who doesn't expect the ECB to raise rates again. ‘But the ECB will keep open the possibility of one further rate hike because a wage-price spiral could be even more damaging than the economic downturn we're seeing now.'”

Source: Fergal O'Brien, Bloomberg , July 31, 2008.

Christopher Wood (CLSA): Data from Britain remains grim

“Finally, the data from Britain remains grim. The number of mortgage approvals for house purchase in the UK fell by 68% YoY to 36,000 in June, the lowest level since the data series began in 1993, according to the Bank of England. Net lending to individuals also slowed from £5.1 billion in May to £4 billion in June, the lowest level since February 1999. The Nationwide Building Society also reported today that house prices fell by 8.1% YoY in July, the largest annual decline since the monthly data series began in 1991.

“It is surely only a matter of time before the Bank of England stops worrying about ‘inflation'. Macro traders should stay short sterling and continue to bet on falling interest rates. With the oil-led commodity complex showing signs of breaking down, the same trades should be put on in Australia in terms of shorting the currency and betting on falling rates. The money markets are now discounting only a 25bp interest rate cut by March 2009 in both Britain and Australia.”

Source: Christopher Wood, Greed & Fear - CLSA , July 31, 2008.

Bloomberg: Australia facing “once-in-100-year” housing slump

“Australia may be headed for a housing recession similar to those roiling the US and UK.

“The cause is a combination of rising default rates, the biggest drop in home prices in five years, the highest borrowing costs in a decade and slowing economic growth.

“Prices in the property market – described by the International Monetary Fund in April as one of the world's most ‘overvalued' – will fall 30% by 2010, according to Gerard Minack, senior economist at Morgan Stanley in Sydney. Prices dropped in all of Australia's major cities last month for the first time since just before the Great Depression.

“‘Australia is headed for a once-in-100-year real-estate slump,' John Edwards, chief executive officer of Residex Ltd., said. ‘I have never seen the convergence of so many negatives.'”

Source: Jacob Greber, Bloomberg , July 31, 2008.

Bloomberg: IMF sees “soft landing” in Japan

“The International Monetary Fund urged the Bank of Japan to refrain from raising interest rates for now as the world's second-largest economy heads for a ‘soft landing'.

“Bank of Japan ‘policy should remain accommodative' as IMF directors see ‘little risk in delaying monetary tightening', the Washington-based lender said today in its annual review of the Japanese economy. ‘Directors look forward to a gradual normalization of interest rates once downside risks to growth recede.'

“The fund's 1.5% growth forecast for this year matches the median estimate among economists surveyed by Bloomberg News. The assessment indicates Japan will avoid a contraction even as exports weaken, hurt by slowing demand in the US and Europe.

“‘The Japanese economy has shown resilience to the US slowdown and global financial turmoil,' the IMF said in the review. ‘The near-term economic outlook is for a soft-landing, although there remain risks from the global economy.'

“Inflation excluding food and fuel prices is ‘expected to stay contained' and an ‘undervalued' yen may rise against other currencies, it said.”

Source: Christopher Swann, Bloomberg , July 29, 2008.

Financial Times: Japanese inflation at highest level in a decade

“Inflation in Japan accelerated in June to 1.9%, the fastest pace in more than a decade because of surging energy and food prices.

“Japan was until recently in deflation and so price pressures remain mild compared with most of the world. Excluding energy and food, CPI rose just 0.1% last month.

“Japan's inflation is not caused by domestic demand, so the Bank of Japan is seen to have little scope to raise rates from the current level of 0.5%. The bank's concern is increasingly turning towards growth.

“This month, the central bank cut its economic growth forecast from 1.5% to 1.2% for the year ending March 2009.

“The squeeze on consumers is likely to hit consumption in the second quarter. Coupled with last month's first export decline in more than 4½ years, some economists are forecasting that second-quarter GDP growth will be negative.”

Source: Lindsay Whipp, Financial Times , July 26, 2008.

Ambrose Evans-Pritchard (Telegraph): Kremlin's heavy hand triggers foreign exodus

“Foreign investors have become extremely wary of the Russian stock market after the Kremlin moved yet again to tighten its noose around the country's energy and mining sector, launching anti-trust probes against London-listed Evraz Holding and Raspadsky Coal.

“The move follows last week's assault on steel and coal giant Mechel for alleged overpricing of raw materials and using offshore trading to cut its tax bill.

“Moscow's RTS stock market index has fallen by 25% since May on fears that premier Vladimir Putin is once again using probes or other heavy-handed methods to reorder the strategic landscape.

“The bare-knuckle fight for control over BP's Russian TNK-BP has deeply shocked investors in the City and New York. The joint venture had been launched in 2003 with the personal blessing of Mr Putin, making it quite different from the foreign resource grab during the Yeltsin era that so enrages Russian nationalists.

“‘The market is panicking and foreign investors are pulling out of equities,' said Michael Ganske, a Russia expert at Commerzbank.

“‘People fear that the rule of law is breaking down. I think this is an overreaction, but the Russian government has to be careful in the way it uses rhetoric in this investment climate,' he said.”

Source: Ambrose Evans-Pritchard, Telegraph , July 31, 2008.

Financial Times: India “aggressive” on inflation

“India's latest 50 basis point increase in interest rates signals an ‘aggressive' shift from growth to tackling inflation, says Deepak Lalwani, director of Indian investments at Astaire & Partners. He tells James Lamont, FT world news editor, that the talk of 10% economic growth in India is now a ‘dim prospect'.”

Source: James Lamont, Financial Times , July 29, 2008.

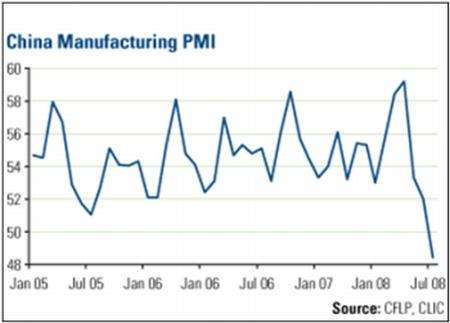

US Global Investors: Weak Chinese PMI reduces risk of overtightening

“China's official Purchasing Managers' Index dropped below 50 for the first time since 2005, suggesting a contraction in manufacturing that is hurt by both slower exports and higher input costs. While a negative data point, this may reinforce China's new policy focus on GDP growth and reduce the risk of overtightening.”

Source: Frank Holmes, US Global Investors – Weekly Investor Alert , August 1, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.