The London Gold Market: What’s Behind the Smoke and Mirrors?

Commodities / Gold and Silver 2013 Jul 02, 2013 - 10:53 AM GMTBy: Jan_Skoyles

In our last two major research pieces we have been looking at the working parts of the gold market and where the heart of it lies. We’re trying to help investors understand where gold prices are really set.

In our last two major research pieces we have been looking at the working parts of the gold market and where the heart of it lies. We’re trying to help investors understand where gold prices are really set.

Today we take a look at the London gold market, an older and arguably larger market than COMEX.

A couple of weeks ago we explained how we had ‘found that the COMEX was still the beating heart of the gold market.’ Since this research piece, Bron Sucheki, whose work featured in our last piece, suggested this may not necessarily be the whole story. Mr Sucheki pointed out the size of the London ‘opaque’ OTC forward market and research that shows price discovery fluctuates between both COMEX and London.

In this next piece we look at the size of the London gold market and reflect on its size in relation to the rest of the gold market and its role in gold price discovery.

The London Gold Market

The London Gold Market, accounts for over 90% of all global over-the-counter (OTC) activity. In 2011 it accounted for 86% of total activity within the global gold market, 90% of which was spot transactions.

In comparison COMEX in New York accounted for just under 10% of total volume in 2011. Also unlike COMEX, the London gold market is entirely inaccessible to individuals and retail trade, the minimum amount of gold traded (per single transaction) is 1,000 oz.

Digging for London gold information

It will come as no surprise to readers when we say that the London market is exceptionally opaque.

As GFMS wrote in 1996:

“The other advantage of the OTC market is its confidentiality and lack of transparency: business can be conducted privately, sheltered from the attention of other market participants, competitors, regulators and, of course, analysts!”

This opaque nature of the London gold market makes it inherently difficult to not only compare to COMEX but to also ask if the unallocated nature of the OTC market is sustainable. It has been estimated that as much as 95% of all OTC activity within the London Gold Market is unallocated, although we have been unable to confirm this. The amount of gold backing unallocated accounts is not reported and gold expert Paul Mylchreest wrote in 2009 that ‘the subject is clouded in secrecy.’

Unlike COMEX, the LBMA is not an exchange and therefore the LBMA does not require members to report turnover, the only regular statistics to come out of London are the daily fixes and the monthly net clearing statistics. The clearing data is based on the returns from the London Precious Metals Clearing Company, made up of six clearing members.

The Clearing statistics

The LBMA release these ‘Clearing statistics’ on a monthly basis. These do not show the precise amount of gold traded, instead showing the average amount of gold transferred by the six LBMA clearing members each month.

The LBMA state the statistics show three things:

• Volume: the amount of metal transferred on average each day measured in millions of troy ounces. [‘Ounces transferred’ in the clearing statistics data is the average amount of gold that changes ownership each day.]

• Value: the value measured in USD, calculated by multiplying the volume figure by the monthly average London PM fixing price for gold.

• Number of transfers: the average number recorded each day.

N.B. only one side of the transaction (debit side) is recorded in order to avoid double counting.

According to a 2011 LBMA paper these figures contain:

- Loco London book transfers from one party in a clearing member’s books to another party in the same member’s books or in the books of another clearing member - Physical transfers and shipments by clearing members - Transfers over clearing members’ accounts at the Bank of England.

Excluded from these statistics are:

- Allocated and unallocated balance transfers where the sole purpose is for overnight credit - Physical movements arranged by clearing members in locations other than London.

Calculating gold volumes

Whilst the clearing statistics do give an idea of the volume of London traded gold, they arguably show just a fraction of the actual volume traded.

It is widely acknowledged that the clearing statistics do not show the true amount of gold traded on the London Gold Market. This is down to the ‘netting’ of trades, ‘if one participant buys and then sells 10,000 ounces of gold with the same counterpart for the same value date, although 20,000 ounces of gold have traded, there will be no movement of metal and no impact on the clearing statistics.” (Thunder Road Report 2009).

This is much higher than ratios previously reported.

As Paul Mylchreest writes the amount by which the clearing volumes should be multiplied is by anything from 5 to 9 in order to give a more accurate view of the daily turnover on the market. Whilst Peter L Smith writing in an Alchemist paper explains: ‘in my opinion the numbers are probably understated by as much as a factor of 3 times, or possibly even more during busy market periods or periods of high volatility.’

Appearing to back up these market assessments, in 2007,the LBMA’s Chief Executive wrote: ‘previous daily estimates of the daily volumes traded in the London market have suggested quantities are a positive multiple of the clearing volumes with a multiplier of between 5 and 9.’

Comparing London and COMEX gold markets

In a 2012 Lucey et al. paper (brought to our attention by Bron Sucheki), the size of the London Gold Market was calculated using one-off statistics collected confidentially by the LBMA, from members, in 2011.

These statistics showed members’ ‘turnover figures for spot, forwards and other transactions in the first quarter of 2011, with the data to be divided, if possible, between trades with other members and trades with non-members.’

The total LOCO London turnover data was then annualised by Lucey et al. to give an idea of trading volumes for 2011.

The authors found that whilst America’s futures and options exchanges are eight times smaller, they ‘are vastly more transparent with a constant flow of prices and daily volumes; information inherently lacking in the London OTC market.’

This, they give as their reason for the American market’s dominance for price discovery, alongside London.

Because of the uniqueness of the LBMA data release we are unable to recalculate for a more up-to-date perspective of the London Gold Market.

The writers are unable to say who ‘leads the dance’ when it comes to influencing the gold market and thus, the gold price. They almost go as far as to say that the size and dominance of the London spot market can be misleading when deciding which one is market dominant: ‘Mere volume alone does not in and of itself make a market dominant.’

Whilst we are unable to gather the extensive data available to academics such as Lucey et al, we are able to gauge an idea of the size of the London market, compared to COMEX using the clearing statistics.

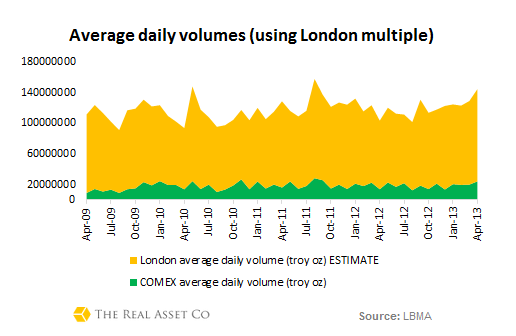

Based on the previous mention of understated volume statistics, and given the current period of volatility we will take a multiple of 5 to try to gauge a more accurate idea of the average daily volume passing through the London Gold market.

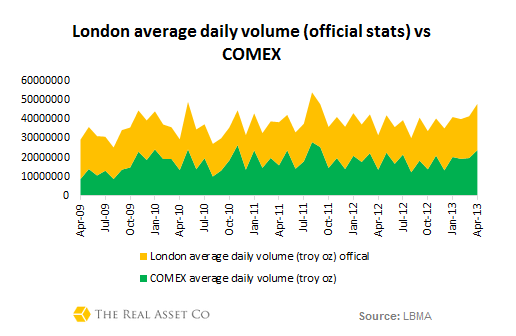

Without using multiples but instead the basic clearing statistics available to us it is still easy to see why one may assume the London market is the most influential.

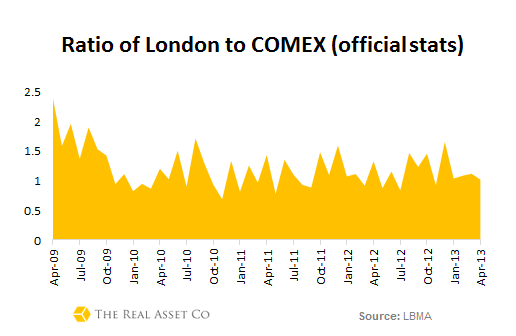

Using this data we can see the ratio of the London market to COMEX and note that London’s dominance has been far greater in previous years than it is currently.

This compliments Lucey et al’s findings that the London gold market remained the centre of price discovery throughout the Lehman brother’s crisis before switching back to New York.

However when applying a multiple to London clearing figures, in our case 5, the dominance of the London Gold Market is significant when compared to COMEX.

The increase is particularly impressive when you look at the activity in the run up to the April gold price fall. Incidentally, transfers for the month of April increased by 60%.

This is something we discuss further shortly.

Is there enough gold in London in order to meet physical demand?

When we examined COMEX we asked if there was enough gold within the system to prevent any stress being placed on the exchange. After looking at COMEX warehouse inventories along with delivery and open interest data we concluded that at this moment there was little cause for concern.

Unfortunately once again given the opaque nature of the London Gold market data such as the amount of gold backing unallocated accounts, how much gold is held by clearing members etc. is unavailable to us. Therefore we are unable to comment on the stresses placed on the London Gold Market and its sustainability.

However for a quick exercise let’s speculate using the daily gold production figures and the number of London Good delivery bars.

In 2012 total world gold production was 2,700 tonnes, 7.4 tonnes per day or 237,915.5 troy ounces. Assuming actual gold transfers within the London Gold Market are 5 times those reported (as discussed above) then the amount of gold transferred within London is (on average) over 426 times daily gold production.

![]()

One would imagine that given the strictness with which refineries are awarded Good Delivery status that there would be an official figure of how many good delivery bars exist. This is not the case.

The only estimate we are able to find is from Adrian Douglas who estimates that there is approximately 15,000 metric tonnes of London Good Delivery bars, or 482 million troy ounces.

The value of an average five days trade on the London gold market matches the total potential stock of global Good Delivery bars.

Given that our previous research has found the COMEX cover ratio to range between 3 and 6 per cent in 2012, the activity in the London Gold market appears to be far less sustainable should buyers and central banks wish to take delivery of their unallocated gold.

The gold market drives price discovery

Given the size of the London market and the twice-daily fix, one might assume that it has a greater influence over gold price discovery than perhaps COMEX does. However, given the sudden fall in the gold price following developments on COMEX in April this is clearly not the case.

We previously fell victim to the general consensus that a futures market, in this case COMEX, would lead a spot market (London Gold Market) when it comes to price discovery. This is based on the more transparent nature of the information available.

Lucey et al (2012) find that the gold price making role switches between London and New York. They find that ‘the average London share of price discovery’ is between 45% and 55%.

They find ‘no direct linkages to particular economic or routine political events’ to cause the switches. Instead they conclude that ‘price discovery is unstable. We see at times when the price discovery is shared, other times when it is concentrated in one or the other market.’

Whilst further research is planned by Lucey et al to look further into what drives the switching of gold price discovery between London and New York, it is clear that it is something within the nature of those in the gold market driving the price.

We hypothesize that it is down to confidence.

At present COMEX is clearly taking control of the price. In our previous research we found that given current inventory draw downs and COMEX activity, the New York market is not immediately subject to any major stresses. I suspect the market is aware of this.

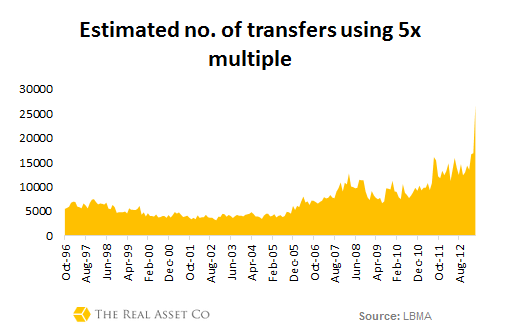

There is a clear issue in London however where the number of transactions cleared has climbed by 60% in April which suggests to us that we are seeing a switch in the location of gold price discovery.

Activity is clearly far greater within the London Gold market, which we believe might currently be reclaiming gold price discovery, but sadly the opaque nature of this market is a real barrier to more comparative analysis.

Whilst the opacity of the London gold market might suit some market participants, there is also a case to be made that it acts as a deterrent to participation, sound discussion and comparison, whilst also harming the reputation of the market itself.

We don’t see the nature of the gold game in London changing any time soon. For now it remains the great enigma for gold investors.

Jan Skoyles contributes to the The Real Asset Co research desk. Jan has recently graduated with a First in International Business and Economics. In her final year she developed a keen interest in Austrian economics, Libertarianism and particularly precious metals. The Real Asset Co. is a secure and efficient way to invest precious metals. Clients typically use our platform to build a long position and are using gold and silver bullion as a savings mechanism in the face on currency debasement and devaluations. The Real Asset Co. holds a distinctly Austrian world view and was launched to help savers and investors secure and protect their wealth and purchasing power.

© 2013 Copyright Jan Skoyles - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Jan Skoyles Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.