Stock and Financial Markets Stormy Weather

Stock-Markets / Financial Markets 2011 May 31, 2011 - 04:45 AM GMTBy: HRA_Advisory

US equity markets had continued to benefit from export driven bottom line growth, but are now sagging on hesitancy about the US domestic economy ahead of QEII buoyancy drying up in June. The Dollar decline that allowed export strength has also boosted US import costs. This could mean a modest US summer driving season unless recent declines in oil prices continue.

US equity markets had continued to benefit from export driven bottom line growth, but are now sagging on hesitancy about the US domestic economy ahead of QEII buoyancy drying up in June. The Dollar decline that allowed export strength has also boosted US import costs. This could mean a modest US summer driving season unless recent declines in oil prices continue.

China's inflation concern has taken up more of its policy. The tighter Yuan policy isn't showing up in the inflation rate but it will have some impact and mean that growth engine downshifts. On top of that the vagaries of nature and street crowds continue to add uncertainty.

We began the year with an "expect the unexpected" stance. May began with the death of bin Laden, which caused only the barest ripple of market applause. We stir entrails this time of year on whether to look for bargains early in the northern summer, or not -- a tough call this year.

The sector we focus on has been consolidating after doing very well. This downward move accelerated recently, which could hasten the start of a buying period. The recovery of the broader equity market after March events seems to be stalling after new highs again in the past couple of weeks. Its not looking comfortable though, and volumes are low. Are the market's about to repeat last summer's pause?

"Events" have been hard on the algorithmic. The muddle of just-in-time manufacturing waylaid by tsunami wasn't expected, but adjustments can be made for it. It's possible to program varied responses to currency and bond or inflation related policy shifts. However, aging powers having to choose between the old buddy system or newly emboldened Arabic Street is quite variable rich.

Despite these weakening events, inflationary pressure would be the most likely cause for a pause. Its not the G7 economies that are the big concern for us. The real pressure is in the growth economies that the high income economies still need for export support. This pressure comes from resource price gains, and most worryingly from high food prices and simple demand growth across many local markets. This again is event related.

Weather events have been getting a lot of ink lately, the most recent being the unusually heavy and deadly North American storm season. Our sympathy goes out to the victims of the southern US tornado onslaught, but it is slower motion events that concern markets. Weak crops and high food inflation are becoming a plague. Those still looking for a second market collapse and double dip recession will remind us the '30s dust bowl deepened the Depression. Markets run on perception so analogies like this can have an impact.

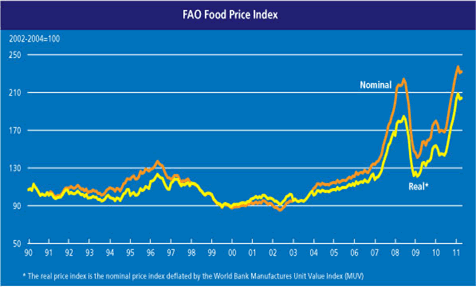

Perception aside, the problem is a real and serious one. The chart above, courtesy of the Food and Agriculture Organization of the UN, shows their food price index hitting new all-time highs, in both nominal and real terms. The price measure is already well above the levels reached in 2008. The one cause for optimism is that the commodity rout going on the past few sessions is driving speculative money out of grain and other "soft" markets too. This helps, but speculators aren't the main cause of price run ups. Its supply and demand, and there is no obvious easy fix.

Brazil has temporarily halted rice exports. Drought in China's wheat region may have the country importing grain for the first time this century. There is also news that China wants to import more sugar due to declining domestic supply and because imported sugar is cheaper. The need to import food may finally be pushing aside the weak Yuan policy. Not the best reason admittedly, but still better for overall balance in the exchange rate system.

A stronger Yuan won't stave off rural unrest in China by itself. It would however help with broader inflation and increase purchasing power for imported goods which could ease the transition for the poorer regions of China.

Talk about a stronger Yuan comes on top of a concerted tightening policy that is finally impacting oil and metal prices. The most recent statistics out of China include weaker Purchasing Manager Indices and inflation numbers that appear to be peaking. The move out of commodities based on these is now fully underway.

Weakening metals and energy prices are a necessary consolidation that we have been looking for, which offers some relief for weak economies. It doesn't help other, poorer economies deal with their food issues though. These keep piling up. Whatever the direct political causes might be, the rash of street protests in the world have an underlying concern about soaring food costs.

Certainly there are some dire predictions for this year's weather, but we won't wade in on them. Rather, we will point out that changing crop conditions have had as much impact on history as kings or bishops. Early signals over the next few months of crop potential in the north may have a larger than usual impact on equity markets. We add that watch to the waiting game on QEII's end.

Rising food costs could (and should) hasten a reduction in the global farm subsidy system. This may be wishful thinking politically, but higher market prices and demand suggest the time is ripe to try. The subsidy system in wealthy economies has hurt capital input elsewhere and closed some markets to developing world farmers. Now that shortage is on the table and prices are high across the board this will be a talking point. It should be kept track of.

The currency mix will also be important to this. Liquidity created to hold the Yen down for 20 years was combined with protected high-cost food producers. Japan could take advantage of Yen strength that liquidity and low external debt now bring to rethink that food subsidy system. Tokyo certainly has better places to spend the money after the tsunami.

The EU has always had a transfers system around agriculture. It's a smaller fraction of the budget than it used to be and is being reformed, but is still there. The will to push reform further as part of a global realignment may be in place. It would need to recognize the debt realities of EU members, but the ECB focus on inflation positions the Eurozone to refocus trade.

The US situation is similar but arguably tougher to deal with right now. Reducing direct subsidies would be small change against the Federal deficit. Like most industrialized democracies the rural vote has a large impact. The Fed's loose money policy is making US export of all commodities more viable, and sensible. It should be taking this export gain, but it shouldn't need to subsidize to do that.

The subsidy system has been such that other big, wealthy exporters like Canada and Australia compete, but not too heavily. In the low income world subsidy tends to be for inputs like power and soil additives, which have also moved up in price. The problem with that has been a skewing of capital allocation to farming. Sound familiar?

Some blame global warming for shortage, while others say the Malthusian equation is simply setting in. We think it's another case of a century of technological based cost reductions working through to their end. Food has rejoined metals and energy in reverting to a larger slice of a global economy that has been prosperous enough to add hugely to the population base.

Investment from the Mid-East and East Asia in Africa is changing that. How well that feeds locals is now the issue. There will be more unrest in more places if some solutions don't get found. Food is not an issue that can be put off.

Another issue shared by the US and China is income disparity. In the US this is taking a back seat to debt. China has been trying to work through that by creating non-rural payrolls, with great success so far. But now urban workers are demanding higher wages to better inflation and that is eating up the country's competitive advantage.

China is one country where higher food prices (if they are allowed) could be an added boon for a very large rural population hoping for better living standards. The export of low wage manufacturing from China means the next Wal-Mart will do its shopping in places like Viet Nam, Indonesia, Pakistan and Nigeria. How does the US compete with that?

Strictly speaking, it can't. There is no point trying to outdo developing countries on low wage manufacturing. Quality, innovation and productivity are the only realistic competitive advantage for a country like the US. This worked for Germany after all, and no one would classify it as a low wage country.

That means the US accepts that it needs to resume the hard goods export model it had before it became a global investor. That has been happening, with last month's exports reaching an all-time high. It's one more reason why strong dollar talk in Washington is just that. Export sectors have been the real wealth and job creators lately and no one in Washington will mess with that.

That notwithstanding, last month we laid out what may eventually turn the US$ back up as a cautionary tale on when precious metal prices could top. At the same time we have been reordering the list a bit to reduce exposure in silver relative to gold.

Silver continued its strong price run until the end of April and came just shy of making a new notional high. It was a very short lived spike and the metal has been falling since. Silver has now given back all the move that began in March. Margin requirements for futures traders were raised several times during the move up which silver bugs are pointing to as the cause of the fall. Futures markets attract speculators that use maximum leverage and may have sold rather than put up more margin. Similar steep down moves were seen in the oil market when margin requirements were upped there in recent sessions.

However, the margin changes mainly reflected increased contract size as prices rose. Traders with sufficient conviction could have put up more margin. The fact they chose to sell rather than do that indicated there was plenty of short term money in these markets. Momentum traders that had taken over the tape in some trades cut and ran when the trend changed.

Similar moves have been seen across the commodity space during the past couple of weeks. We want to be clear here. We are not saying that internal market issues like margin requirements are the reason for the price pull backs. They might have hastened the moves in a couple of the most overdone markets, but only because traders had already decided it was time to take profits.

We don't think the US$ bear has left the woods yet, nor do we think the longer term commodity bull cycle has suddenly evaporated. We do think that growth economy central bankers are starting to succeed in slowing their economies. That success, plus ongoing concerns like QEII, European debt squabbles and US debt ceiling smack downs has traders blowing the froth off metal and other commodity markets. It's what they do.

Copper has finally made the move back below the $4 mark we have been expecting for months. Copper's move can be more directly attributed to signs of slowing in China, though it too had a speculative component that needed to be dented. Now that the spell has been broken there may be a bit more downside left before the red metal is again ready to base and provide another sustained up leg in price again.

We are still focused on market warehouse stocks to time the red metal, and so far they are not suggesting it's time to go long. The Shanghai total is down some, so we may be approaching the "right" price soon.

Similar moves have been seen across the base metal space. For the most part, the scale of the current pull backs has been in direct relationship to earlier upward price moves. In short, the larger the late 2010-early 2011 price increase in a particular metal the bigger the resulting correction. This is what would be expected in a market where prices were being reset to match lowered expectations or greater concerns.

Gold has been an exception so far. In percentage terms the pullback has been small. This reflects gold's status as a quasi-currency and its insurance value. We expect that to continue and gold to be one of the stronger metals as the markets settle.

During silver's 1980 run many wondered where the buying came from and lined up with grandma's silverware to cash in. No such line ups are seen this time even though the recent run up looked pretty bubbly by the time it peaked. Again, this points to the current price moves in commodities being corrective, not a "sky is falling" scenario.

Now that traders are lightening commodity positions and markets are easing, the question is when and where to we find a bottom. At a macro level, the big risks are growth economies slowing too much, QEII ending with a bang not a whimper and politicians in Europe and the US letting gridlock keep them from negotiating debt deals.

China has proven adept at managing growth so far. Likewise, for all the handwringing about QEII the bond markets are acting a lot less worried than people who talk about bond markets. Both of these situations may end well, but it will be at least a couple of months before that is known. That points to a bottoming during mid-summer and charts that may yet look a lot like last year's. We plan to position accordingly.

Ω

Sign up to receive HRA commentary, interviews and our latest free special report on Iron Ore & Potash, including a new HRA recommended company! www.hraadvisory.com

By David Coffin and Eric Coffin

http://www.hraadvisory.com

David Coffin and Eric Coffin are the editors of the HRA Journal, HRA Dispatch and HRA Special Delivery; a family of publications that are focused on metals exploration, development and production companies. Combined mining industry and market experience of over 50 years has made them among the most trusted independent analysts in the sector since they began publication of The Hard Rock Analyst in 1995. They were among the first to draw attention to the current commodities super cycle and the disastrous effects of massive forward gold hedging backed up by low grade mining in the 1990's. They have generated one of the best track records in the business thanks to decades of experience and contacts throughout the industry that help them get the story to their readers first. Please visit their website at www.hraadvisory.com for more information.

© 2010 Copyright HRA Advisory - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

HRA Advisory Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.