Stock Market Rally Built On Sand? FASB Can Help!

Stock-Markets / Stocks Bear Market Mar 31, 2009 - 07:25 AM GMTBy: Chris_Ciovacco

It is apparent many have jumped on the "a low is in" bandwagon in recent weeks. Given the environment we are operating in (a bear market), it makes sense for us to adopt a skeptical view of the "good" news that lifted stocks in recent weeks. The rally began after Citigroup's talk of being "profitable" somehow found its way to the media on March 10, 2009. Below is a skeptical recap of some of the drivers of the impressive rally in stocks since the March 9, 2009 low.

It is apparent many have jumped on the "a low is in" bandwagon in recent weeks. Given the environment we are operating in (a bear market), it makes sense for us to adopt a skeptical view of the "good" news that lifted stocks in recent weeks. The rally began after Citigroup's talk of being "profitable" somehow found its way to the media on March 10, 2009. Below is a skeptical recap of some of the drivers of the impressive rally in stocks since the March 9, 2009 low.

FASB – A Night In Shining Armor: However, before we question the good in the recent "good" news which helped propel stocks higher, we must acknowledge another piece of "good" news that is coming to a press release near you this Thursday. When the stock market gets another government-induced-bailout rally after FASB (Financial Accounting Standards Board) approves changes to market to market accounting on April 2, 2009, it is wise to remember that all of the past government-induced-bailout rallies have been fully retraced (Bear Stearns, Fannie, ING, Fed liquidity-facilities-o-plenty, etc.). We describe the coming FASB move as government-induced because FASB is bowing to intense political pressure to significantly alter mark-to-market accounting. The politicians are applying pressure on FASB because financial firms (and large campaign contributors) are putting tremendous pressure on them. Notice the term investor is not included in the FASB story. For a somewhat lighthearted primer on mark-to-market, a quick scan of Pet Rocks and Mark-to-Market Accounting may be worth a laugh or two (and possibly some crying for investors who crave transparency). For details on this Thursday's FASB events, consult this Bloomberg story . Now on with the recap of all the recent positive developments for investors...

FASB – A Night In Shining Armor: However, before we question the good in the recent "good" news which helped propel stocks higher, we must acknowledge another piece of "good" news that is coming to a press release near you this Thursday. When the stock market gets another government-induced-bailout rally after FASB (Financial Accounting Standards Board) approves changes to market to market accounting on April 2, 2009, it is wise to remember that all of the past government-induced-bailout rallies have been fully retraced (Bear Stearns, Fannie, ING, Fed liquidity-facilities-o-plenty, etc.). We describe the coming FASB move as government-induced because FASB is bowing to intense political pressure to significantly alter mark-to-market accounting. The politicians are applying pressure on FASB because financial firms (and large campaign contributors) are putting tremendous pressure on them. Notice the term investor is not included in the FASB story. For a somewhat lighthearted primer on mark-to-market, a quick scan of Pet Rocks and Mark-to-Market Accounting may be worth a laugh or two (and possibly some crying for investors who crave transparency). For details on this Thursday's FASB events, consult this Bloomberg story . Now on with the recap of all the recent positive developments for investors...

Citigroup Is Profitable: The initial spark for the current rally was an "internal" Citigroup memo that conveniently was leaked to the media as stocks headed to lower lows. The memo said that Citigroup's core business was profitable year-to-date. The market's reaction highlighted investors' need to brush up on their accounting terms. Operating profit does not include what happens on Citi's balance sheet, which means losses on assets and securities can be staggering while Citi still earns an operating profit . With home prices continuing to fall, we will go out on a limb and say the odds are good Citi will have a few more balance sheet issues in the months ahead (maybe years).

Fed To The Rescue: Government intervention was another spark for the rally off the March lows (wow! – that's a new concept!). The state of the world must be less than stellar if the Fed feels it has to step in and buy Treasury bonds. Our government issues bonds…..and now the Fed is going to buy them…what?? This is money printing in its purest form. History has not been kind to money printers – excessive money printing always ends badly. It can work for a time, but the chickens will eventually come home to roost.

Geithner - The Man In The White Hat: More government intervention? You bet. Secretary Geithner's toxic asset program will use leverage to artificially boost asset prices. We've been down this road before – it did not work in the last bull market (unless you forget the crash) – and Geithner's plan more than likely will not work either. You cannot permanently suspend the laws of supply and demand with printed money or government subsidies. Secretary Geithner's plan may work for a time, but as soon as the leverage or subsidies are removed, or when supply gets artificially inflated (as we saw in residential housing), prices will come down. Money manager Dr. John Hussman on the Geithner Plan:

From early reports regarding the toxic assets plan, it appears that the Treasury envisions allowing private investors to bid for toxic mortgage securities, but only to put up about 7% of the purchase price, with the TARP matching that amount - the remainder being "non-recourse" financing from the Fed and FDIC. This essentially implies that the government would grant bidders a put option against 86% of whatever price is bid. This is not only an invitation for rampant moral hazard, as it would allow the financing of largely speculative and inefficiently priced bids with the public bearing the cost of losses, but of much greater concern, it is a likely recipe for the insolvency of the Federal Deposit Insurance Corporation, and represents a major end-run around Congress by unelected bureaucrats. (entire article).

Great News! Housing Inventories Are High And Prices Keep Dropping! Before we cover last week's positive news on the housing front, keep in mind, when houses decline in value, the collateral backing loans and mortgage-backed securities drops right along with prices. Declining collateral values mean more trouble for the toxic assets that are currently "clogging" the financial system. The plus side of last week's housing report was sales increased 4.7% in February. That portion of the report was good news since the excessive inventory has to be cleared out in order to get supply and demand back in balance. However, sales are only part of the equation here. Do you think it would be good for the banks' balance sheets and the value of mortgage-backed securities if sales went up 50%, but prices were down 50%? No, that would be awful for banks and holders of securities tied to housing. Yes, sales were up in last week's report, but prices were down.

The median sales price fell to $200,900, down a record 18.1% compared with February 2008. This is the lowest median price since December 2003. We would agree that if sales were up with lower prices that would be good news IF the sales significantly reduced the glut of supply of homes for sale. No such luck – yes, inventory was reduced by 2.9%, but we still have a 12.2 month supply of unsold new homes using the current pace of sales. The housing market needs to get supply and demand back in balance so prices can stabilize and maybe even go up. Until prices stabilize, there is really no good news. How close are we to a better balance of supply and demand? Regrettably, not close at all. A healthy market where prices can remain stable has about 6 months of supply – we currently have over 12 months. You do not need to have a doctorate in economics to conclude prices still have further downside. Lower prices mean more problems for banks and holders of toxic securities backed by residential real estate.

Valuations Are Attractive!: According the Yale's Robert Shiller as of Monday's close, stocks are trading at 14 times earnings based on average earnings over the last 10 years. A PE of 14 is mildly attractive, but not once in a generation financial crisis attractive. We also have to consider the earnings from the last ten years came during a period of high leverage and high margins. We will not see high leverage and high margins again for some time, which means the PE of 14 probably makes stocks look more desirable than they really are based on earnings prospects for the next ten years.

Our Bias Should Be Negative In A Bear Market: Wall Street analysts and the financial media follow the path of least resistance:

- They publish bullish stories when stocks have been moving up for a few weeks, and

- They write bearish stories when stocks have dropped for a few weeks.

When stocks are going up, it is human nature to avoid the appearance of going against the grain by writing negatively slanted reports when readers are instinctively much more receptive to a positive report. In recent weeks it has not been difficult for many to climb on board the "The-Bottom-Is-In-Express". It's just that sometimes it is better to patiently wait in the station for the right train to come in. If you are not sure of the train's destination, don't hop on board. Patience can be a financial virtue.

Bias in news coverage can be frustrating since a good reporter should keep an open mind and present both sides of any story. However, good investors should carry some degree of bias when evaluating fundamental and technical data. The key is that bias has to be flexible depending on the primary mood (trend) of the market. During a bull market, it pays to be skeptical of the significance of a correction in stocks or bad news. It also pays to take what the bears say with a grain of salt because the primary trend in a bull market is up. Our goal is to stay with the primary trend as long as possible within the framework of good money management (e.g. cutting losses), which, to some degree, requires the ability to tune out day to day distractions.

During a bear market, it pays to view any positive countertrend rally or good news with some healthy skepticism. It also pays to take whatever the bulls say with a grain of salt because the powerful collective thoughts of market participants, on average, are driving asset prices lower.

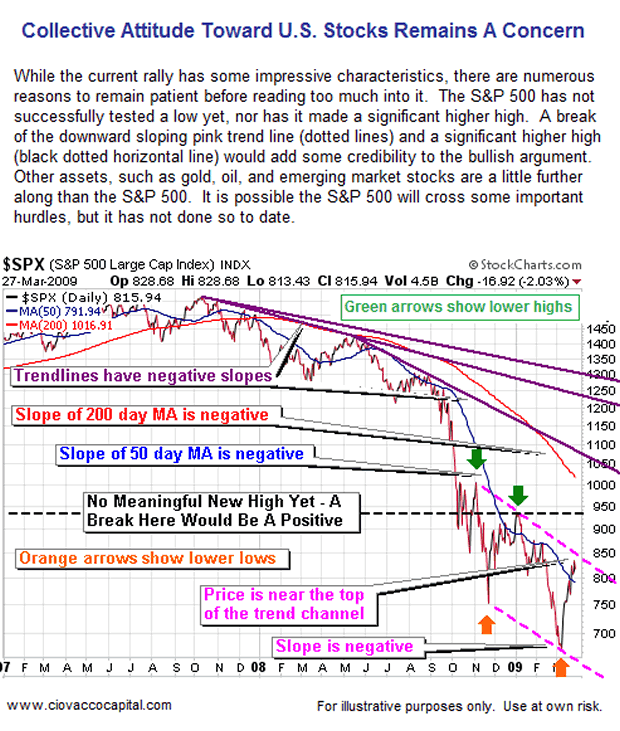

We remain firmly entrenched in a bear market despite the recent rally and despite countless calls for a bottom. We may have already put in a bottom, but, at this point, there is no need to guess . If we do indeed have a bottom in place, we can adjust as the observable evidence unfolds. In a new bull market, there will be plenty of time to make money. Even if the recent lows were "the bottom", the odds are good those lows will be re-tested in the coming weeks or months, which would throw a little cold water on the Wall Street perma-bull mantra of, "you can’t miss the start of a new bull market". The chart below, created after Friday's (3/27/09) close, continues to stress the need for patience and skepticism.

In our brief review of some of the market's fundamentals above, we have not even touched on rising unemployment, which is driving up default rates on all kinds of debt, including consumer credit cards. As we covered in Rallies: The Million Dollar Question , numerous markets including oil (USO, USL), emerging market stocks (EEM), and commodities (DBC, DBB, DBA), are facing technical challenges in addition to significant economic weakness, and excess capacity (see Fundamentals May Halt Stock Rally: Should I Stay or Should I Go? ). Our negative bias always needs to be balanced with an open mind. Bear markets always end - this one will be no different. Besides, don't get too discouraged, we have a mark-to-market rally in the wings - always some government changes to look forward to!

The charts and commentary above are for illustrative and educational purposes only and are not recommendations to buy or sell any security.

By Chris Ciovacco

Ciovacco Capital Management

Copyright (C) 2009 Ciovacco Capital Management, LLC All Rights Reserved.

Chris Ciovacco is the Chief Investment Officer for Ciovacco Capital Management, LLC. More on the web at www.ciovaccocapital.com

Ciovacco Capital Management, LLC is an independent money management firm based in Atlanta, Georgia. As a registered investment advisor, CCM helps individual investors, large & small; achieve improved investment results via independent research and globally diversified investment portfolios. Since we are a fee-based firm, our only objective is to help you protect and grow your assets. Our long-term, theme-oriented, buy-and-hold approach allows for portfolio rebalancing from time to time to adjust to new opportunities or changing market conditions. When looking at money managers in Atlanta, take a hard look at CCM.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors and tax advisors before making any investment decisions. Opinions expressed in these reports may change without prior notice. This memorandum is based on information available to the public. No representation is made that it is accurate or complete. This memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned. The investments discussed or recommended in this report may be unsuitable for investors depending on their specific investment objectives and financial position. Past performance is not necessarily a guide to future performance. The price or value of the investments to which this report relates, either directly or indirectly, may fall or rise against the interest of investors. All prices and yields contained in this report are subject to change without notice. This information is based on hypothetical assumptions and is intended for illustrative purposes only. THERE ARE NO WARRANTIES, EXPRESSED OR IMPLIED, AS TO ACCURACY, COMPLETENESS, OR RESULTS OBTAINED FROM ANY INFORMATION CONTAINED IN THIS ARTICLE. PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

Chris Ciovacco Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.