Watch Consumer Spending to Know When the Fed Will Cut Interest Rates

Interest-Rates / US Interest Rates Feb 04, 2024 - 04:15 PM GMTBy: Richard_Mills

The probability of interest rate cuts has many market participants pondering whether 2024 will bring a bull market for precious metals.

Gold has held up quite well despite the Fed’s tightening cycle, gaining 13% in 2023.

The Federal Reserve’s current interest-rate pause, due to successfully lowering inflation, and subsequent pivot to reducing interest rates, likely in mid-2024, is good news for commodities.

Lower rates will cause the dollar to fall and commodity prices to rise. When positive real interest rates, which favor bond investors, turn negative, it will especially affect gold prices to the upside.

I’ve been right in my prediction that the Fed would pause in June, 2023, and hike once or twice more before the end of the year.

I’ve also voiced my opinion that we will get a soft landing with no recession, with the important proviso that the Fed pauses its rate-hiking cycle, which it has already done.

Remarkably, the Federal Reserve has raised interest rates high enough to reverse the inflation rate, at one point at a 40-year high, without causing a severe downturn. And it’s done it in an extremely short amount of time.

The key questions now are: When does the Fed cut rates, and as importantly, why would it cut rates? If the Fed drops interest rates, what will it mean for precious metals?

Fortunately, we’ve already had a dry run that gave us an answer to the last question.

Many investors in December placed a bet on bullion when they figured the Fed was planning to lower interest rates in 2024. Spot gold hit a new record-high $2,135 an ounce on Dec. 3.

We’ve seen how sensitive the market is to monetary policy.

Just the suggestion of coming rate cuts pushed gold to lofty heights. The Fed’s messaging also caused bond yields and the dollar to fall. The benchmark 10-year Treasury slipped from 5% in November to 3.9% around Christmas-time. The US dollar index DXY dropped from 106.88 on Nov. 23 to 101.71, a reduction of 5%.

It turns out gold’s record-high was only temporary. Within a week, it fell under $2,000.

Meanwhile, the market’s reaction to statements that the Fed is not going to pivot as early as everyone thought (as early as March) strengthened the dollar and bond yields. In fact it is surprising to see gold trading mostly above $2,000 so far this year, since the precious metal usually moves in the opposite direction as these two variables.

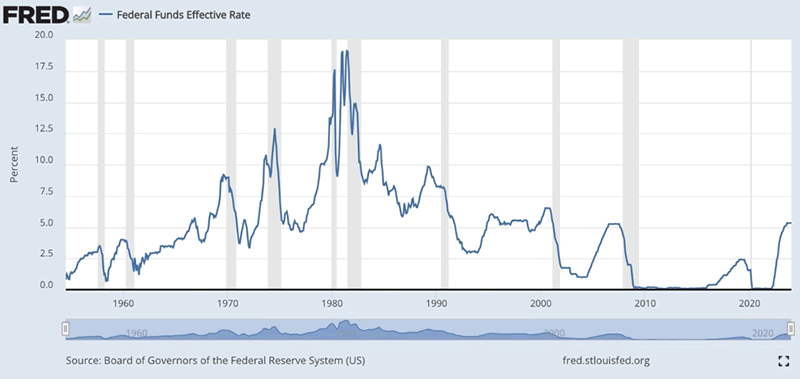

I personally believe the Fed will cut interest rates, but not until it sees some deterioration in the jobs market and particularly, a drop-off in consumer spending. I’m sticking to my prediction of three quarter-point rate cut in 2024, which would take the federal funds rate from 5.5% down to 4.75%.

Now to the first two questions: When will the Fed cut rates and why? (or why not?)

Let’s start with the observation that the US consumer makes up 70% of the economy (consumers also represent 70% of the global economy), so the Federal Reserve monitors consumer spending closely to see whether it is rising or falling.

Of course the Fed is also concerned about the health of the economy — measured mostly by the stock market — and its twin mandates of keeping inflation within its 2% target, and the economy near full employment.

On Friday, Jan. 26, the release of the personal consumption expenditures (PCE) price index strengthened the argument that the Fed will reduce rates later this year. Core PCE (i.e., stripping out food and energy) is the Fed’s preferred inflation gauge.

On a six-month annualized basis, core PCE was below the Fed’s 2% target in December for a second straight month, at 1.9%. On an annualized basis core PCE was 2.9%. Even if we take the latter figure, inflation appears to be coming down to the Fed’s 2% target.

So, with inflation pretty much beaten, does that mean it’s time to cut interest rates? A week ago, the analysts seemed to think so.

“Evidence continues to pile up that the Fed has met its inflation goal, which will make it harder for officials to hold off on cutting rates until midyear,” Bloomberg quoted an economist with LH Meyer/Monetary Policy Analytics.

“The stage is set for the Fed to take steps toward cutting rates and tapering the pace of Quantitative Tightening (QT) in coming months. We expect the Fed to begin lowering the federal funds rate target range in March as it attempts to stick a soft landing,” Bloomberg Economics agreed.

When the Federal Open Market Committee had its regular meeting this past Tuesday-Wednesday, it voted for the fourth consecutive meeting to leave interest rates alone, at 5.25-5.5%. CNN reported the Fed made a statement indicating it was done raising interest rates, by removing language that suggested a willingness to keep raising rates until inflation was under control, i.e., nearing 2%.

But hold on. The Fed also made clear it is not ready to start cutting, and particularly will not lower rates in March, as previously expected.

Fresh economic data out Friday, Feb. 2, provided more information for Fed watchers like me to digest.

According to the Bureau of Labor Statistics report, the economy added 353,000 jobs in January, and 333,000 in December. Most industries gained positions last month, with the exception of mining and natural gas extraction. The numbers doubled consensus forecasts of 176,500 new jobs.

More good news: unemployment remained at 3.7%, and wages grew 0.6% for the month and 4.5% year over year. CNN said it’s the 24th consecutive month that the US jobless rate has been under 4%.

“The fact that the unemployment rate has been below 4% for 24 months straight for the first time since 1967 is truly remarkable,” Joe Brusuelas, chief economist and principal at RSM US, told CNN Business.

This despite the fact that the Federal Reserve has hiked interest rates 11 times since March, 2022. We’re talking about the biggest and fastest increase in interest rates in a generation.

Indeed the economy appears to be firing on all cylinders — defying expectations that the Fed’s tight monetary policy would crash the economy and lead to a recession.

CNN notes that January’s job gains dashed market expectations for a Fed rate cut to come sooner than later, perhaps as early as March, and for the central bank to cut as many as six times in 2024. Investors’ probability for a March rate cut dropped from 38% to under 20% on Friday, according to the CME FedWatch Tool.

Far from collapsing, the US economy grew 2.5% in 2023, up from 1.9% in 2022. Fourth-quarter GDP was even better, at 3.3%.

The Associated Press notes that consumers drove growth in the final quarter of 2023, with spending expanding at an annual 2.8%, on goods like clothing, furniture and recreational vehicles, and services like hotels and restaurant meals.

Fun fact: Taylor Swift’s Eras Tour is expected to generate close to $5 billion in the United States alone.

“If Taylor Swift were an economy, she’d be bigger than 50 countries,” said Dan Fleetwood, president of QuestionPro Research and Insights, in a Time Magazine story.

Many saw Swift watching the Kansas City Chiefs last weekend in the NFL Conference Championship game. According to the New York Post,

Taylor Swift has helped direct big bucks toward the NFL — with 16% of US shoppers admitting the pop star influenced them to spend cash on football in the walkup to Super Bowl LVIII, according to a recent survey.

The numbers mean that of 333.3 million Americans, according to the latest census data, some 53 million have spent money on the sport since Swift and Kansas City Chiefs tight end Travis Kelce first went public with their romance.

Most shelled out cash for jerseys and memorabilia or on a streaming service subscription to watch NFL games, according to a study on credit card spending by online financial firm LendingTree on Monday.

Retail investors are seemingly off the sidelines, with US stock markets reaching new heights on an almost daily basis. The S&P 500 registered an all-time closing high of 4,958.61 points Friday, as tech stocks soared and investors digested the positive employment report. Reuters said all three major US stock indexes notched their fourth consecutive weekly gains.

Manufacturing is up too: the Institute for Supply Management (ISM) said Thursday that its January manufacturing PMI increased to 49.1, compared to 47.1 in December.

What does the strong economy mean for monetary policy? Well, the January BLS report indicates the job market is strong, wages are rising, and this was reflected in a record-high stock market close. I previously said there was a 50-50 chance of the Fed cutting rates by a quarter-point in March, but these latest numbers, imo, put that chance at zero.

Why cut rates when the economy is booming? If we think of each interest rate percentage as a bullet, the Fed has 5.5 bullets in the chamber. Why fire one off needlessly? In hiking rates 11 times in the past nearly two years, the organization has given itself ample room to maneuver. If it only cuts rates by a quarter-point each time, that’s 22 opportunities to lower rates to 0% — which is where we ended up when the Fed aggressively cut interest rates following the onset of the covid-19 pandemic in early 2020.

It seems we have come full circle — we are now back above 5%, where the federal funds rate was in mid-2007, just before the 2008 financial crisis which started the now-familiar quantitative easing policy of slashing interest rates and injecting liquidity into the financial system through the Fed’s purchase of government bonds and mortgage-backed securities.

(Some think we could have elevated rates for awhile. Former Treasury Secretary Lawrence Summers on Friday warned of +3% yields on US Treasury bills through to 2030.)

In 2008, the US consumer had stopped spending, and the Fed needed to change that. It did it through QE/ money-printing, and dramatically lowering interest rates.

The same thing happened when the pandemic hit. The sudden drop in consumer spending panicked the Fed, which went on another QE bender, only this time, the government got involved by sending direct stimulus checks to Americans. Corporations received covid relief too.

Not only that, but the Fed dropped interest rates to 0-0.25%, goosing the economy by making borrowed money practically free.

These things go in cycles and it’s only a matter of time before the wheel turns again, back to lower rates.

Right now, the Fed needs to see inflation stabilizing. They want to see a sustained period of cooling inflation below their 2% target before lowering borrowing costs.

To me, this means a minimum of five months of continued lower inflation.

I’ll stay with my original projection of three quarter-point rate reductions this year. These are “token” cuts that could be political in nature. Remember, this is an election year and the Fed, despite its claimed independence, has been known to take sides. The New York Times recently wrote,

The Fed may have already, and unintentionally, helped Mr. Biden’s re-election prospects by holding rates steady for the back half of 2023 as inflation cooled. Continued rate increases could have slammed the breaks on economic activity and increased the chances that the economy slipped into recession — which is one reason progressive groups, and some Democratic senators, urged Fed officials to pause rate increases last year.

Of course there are other, more practical reasons for lowering interest rates, the “US public debt-to-GDP ratio is at 94% and rising by more than 5% per year, enough to double the ratio within 13 years”, and the national debt now sitting at a jaw-dropping $34 trillion. Interest costs have nearly doubled over the past three years, from $345 billion in 2020 to $659 billion in 2023.

Conclusion

It’s hard to say when a rate cut is coming (9 out of 10 economists predict April 30th/May 1st meeting); there is certainly no hurry. As far as the Fed is concerned, everything is coming up roses. Why rock the boat?

But when a rate cut does come, and AOTH agrees the April/May meeting is likely for the first quarter point cut, the decision will, imo, be driven by the spending habits of US consumers, which remember, make up 70% of the economy. Signals could include reduced consumer spending, credit card debt, loan and mortgage delinquencies, a higher savings rate, and wage deflation. The Fed will also of course, be watching unemployment numbers closely.

In the meantime, I’m positioning myself for the coming interest rate cuts, and the subsequent weakening of the US dollar, by purchasing the shares of junior gold and silver companies, which offer great leverage to rising metal prices.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector. His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2024 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.