Gold and Stock Market Barometric Bedlam

Stock-Markets / Financial Markets 2020 Feb 05, 2020 - 01:47 PM GMTBy: The_Gold_Report

Sector expert Michael Ballanger charts last month's market moves. Back in the 1980s, I had a boss that was right out of Monty Python. A Canadian by birth, he was the son of a very wealthy English nobleman who spent a number of years in Brazil as CEO of Brazilian Traction, where he was raised by servants and nannies and attended private boarding school at Upper Canada College in Toronto.

"James" was a thoroughly English gentlemen on the outside but a scandalous hell-raiser in private quarters. I recall him at a squash club banquet standing on the dining table wrapped in the Union Jack, tumbler of gin in hand, reciting a totally X-rated, four-stanza limerick that began "The once were three nuns from Birmingham (pronounced BIR-MING-UM), and here is the story concerning 'em. . .". It was his saintly wife, "Jane," who solemnly declared in the wee hours of one debaucherous morning in his basement that we had better "cease and desist with this unnecessary drinking," never revealing what might be the definition of "necessary drinking," a conundrum left unsolved for nigh-on thirty-five years.

The reason I mention this is that as we await the reopening of Chinese markets after the New Year's week closures, I am sure that many investors are engaged in "necessary drinking" as they await either a) the crash in virus-infected markets or b) the arrival of the Chinese central planner trading desk and legion after legion of stock-buying roboticized carbon units pumping up stocks to prevent a total disintegration of all things Chinese next week.

I, for one, haven't decided which it will be but I went into this weekend happier than I have been in a month because there is only one thing worse than certainty of losing money and that is the UN-certainty of losing money. The stress of reacting to events is a good stress but worrying about the nature of events is bad stress and bad stress kills. We now know that global growth is tumbling and about to get worse and that the coronavirus is a global pandemic and that both events are good for what we own and bad for what we are short (or have already sold).

Precious metals investors have now departed the all-important month of January with a solid tailwind astern and clear skies ahead, but for stock investors, the barometric pressure has plunged like the mid-Atlantic in September. The legendary Richard Russell used to tell his subscribers that "event risk," be it monetary, fiscal or geopolitical, is just another excuse for Mr. Market deciding which way he wants to go, and for how long, and at what speed. So, when I discuss January 2020, I will avoid commentary on debt or viruses or impeachments, simply review the numbers and the charts, and try, as best I am able, to decipher the always-deceptive language of the market.

I decided in late December of last year that physical gold and silver were infinitely preferable as portfolio components to mining stocks. Recalling the debacle of October 1987, where gold rose and the miners crashed, I elected to defer purchases of the Gold and Silver Miner ETFs "until further notice."

Well, gold advanced and silver advanced last month but the HUI (unhedged gold and silver miners' index) was unable to post a gain because the precious metal tailwind was overpowered by the equity market headwind. As the old expression goes, when they raid the brothel, they take ALL the ladies, even the piano player. After all, paper is paper.

The two charts shown above are significant for the GGMA portfolio in that they confirm the long-term positive trend for the physical markets and underscore the reason that I have been advising everyone to focus on overweighting those positions while underweighting the Senior and Junior Gold Miners (GDX/GDXJ), which are best represented by the HUI index, which closed lower for the month.

Now, in a perfect world, I would have liked the HUI up for the month because it would have been a strong confirmation of the bull market in the entire complex, but because we have a possible non-confirmation of this, you have to focus on the individual stories (junior developers like Aftermath Silver Ltd. [AAG:TSX.V], Goldcliff Resource Corp. [GCN:TSX.V; GCFFF:OTCBB], Getchell Gold Corp. [GTCH:CSE], and Western Uranium & Vanadium Corp. [WUC:CSE; WSTRF:OTCQX]) rather than taking a blanket approach across the entire senior and junior universe.

It does not mean that the junior developers are going to be immune from overall equity market weakness, but being "story stocks," the inputs that drive them higher are often sufficient to offset the gloom—and gloom is what we saw for most of the U.S. stock exchanges, which closed out January on the downside.

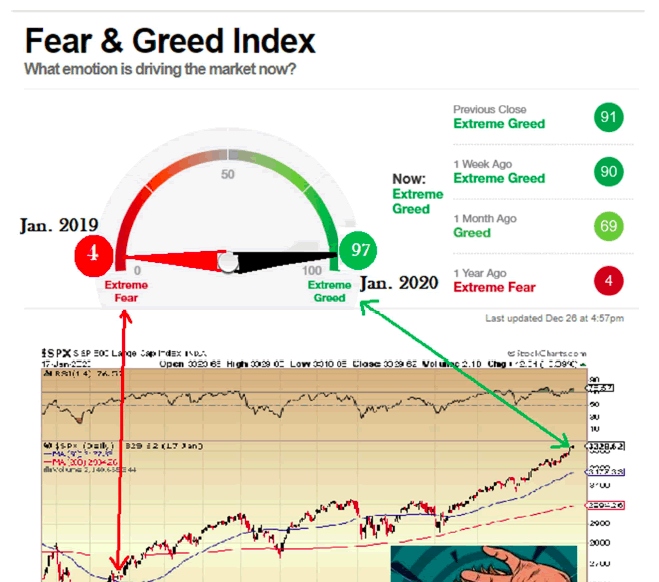

With the numbers now all in, the Dow Jones and the S&P 500 closed lower for the month, whereas the NASDAQ eked out a modest gain. Last week I spoke of the January Barometer and warned that while the mid-month tallies looked bullish, the end-of-month scorecard would prevail as the final determinant in the forecast. By closing January with a loss, the S&P reversed all euphoria evident in the Greed-Fear Index (shown below) tweeted out on Jan. 20 at S&P 3,324.

Just as I had never seen a reading of "4" a year ago, the "97" print seen two weeks ago was the biggest "sell" signal I have ever received. While it does not always give me precise timing, as we look back at the chart, it was pretty glaring.

Now, the NASDAQ was able to eke out a modest gain and many of the purists out there would have you think that the tech-heavy NASDAQ is the market. But if you take out Tesla and Amazon, which were squeezed higher Friday on bogus earnings euphoria, it could easily have had a red month.

Nevertheless, the January Barometer has issued a warning for us all, and the $64,000,000 question is whether or not these storm clouds are going to bring rain upon the gold and silver sectors.

If you recall my 2020 forecast Issue, I attempted to make the case for much higher gold and silver prices based on their utility as collateral for the mountain of global sovereign and corporate debt choking the life out everything. Well, with less travel, less spending and reduced consumer confidence, there will be certainly reduced taxable income and therefore reduced tax receipts. The downward spiral into fiscal hell has begun in earnest and the evidence is the rats all scrambling for the mooring ropes now that the old wooden ship is ablaze.

The 2019 portfolio remains 70% invested, with 30% cash awaiting a better entry point for physical gold and silver or the GDX/GDXJ dynamic duo, if they pull back to their 50-day moving averages (probably unlikely). The 2020 portfolio is being hunted down like a wounded animal and it is difficult because I am not seeing anything that is prompting me to capitulate. With stocks in freefall last week, one might have expected that gold would be in the $1,600s but we must be constantly mindful that every large hedge fund holding gold or gold futures has an algorithm that utilizes massive leverage to generate "alpha" (above-average returns). So when stocks get bombed, portfolios long stocks and gold or gold futures must reduce exposure—and that means they have to sell anything to reduce the leverage(debt) attached to the portfolio.

Fifty-eight handle maulings in the S&P are virtually guaranteed to exert pressure on all markets because of this unearthly addiction to leverage. Recall the 2007–2008 Global Financial Crisis, where the banks basically blew up the world while providing the once-in-a-lifetime catalyst for US$10,000 gold prices. We were literally hours away from a complete freeze-up in all facets of retail and institutional banking, and yet the hedge funds (Large Speculators), up to their eyeballs in highly-leveraged gold futures, were forced to liquidate massive Crimex gold positions to meet margin calls on other assets (like stocks). Instead of a moonshot to US$10,000, gold was taken down to US$695 in what commentators called the "deflationary collapse."

While I contend that conditions here in 2020 are diametrically opposite to those we faced in 2008, you have to keep a solid physical position on hand (and close to you) with a healthy cash position to take advantage of gold and silver miner bargains that present themselves during panics.

COT The COT this week was meaningless for gold but positive for silver, with Commercials covering shorts into silver's weakness but adding to shorts into gold's strength. The bigger picture to be considered is the wide gap between Large Specs (net long 330,092 contracts) and Commercials (net short 360,814 contracts).

As you can see from the COT chart shown below, if in the next eight weeks we get an acceleration in Large Spec buying and a forced reduction in aggregate shorts held by Commercials (bullion banks), then price has nowhere to go but up. The smaller red rectangle is my "best case" scenario, where most lines converge, as was the case in April–May 2019, when the banks covered the bulk of their shorts starting in mid-March and going right through the US$1,270 bottom in May.

Unlike other periods of declining gold prices, such as the September–November 2019 correction, there was virtually zero short covering by the Commercials, which is essentially why I have remained on high alert and cautious.

However, the game has changed, with equities in full retreat, so unless China rescues its markets, gold should be free from the competition of booming stock markets, which would be a welcome occurrence.

January 2020 will, in my humble opinion, go down in financial history as the month that the equities bubble popped and the onset of a bear market, but January will also mark the end of the consolidation/correction in precious metals. Importantly, the jury is still out for precious metals equities, as they still have much work to do to prove to me that they can trade countertrend to the other equities, as liquidity concerns escalate and emotions begin to run amok.

As investors, like mariners, all we need to do is stay focused on the horizon rather than on the waves crashing against our bow. The fiat currency regime of the past hundred years, stocks, are going to suffer. Portfolios anchored by large weightings of physically held precious metals and quality gold and silver producers, developers, and carefully selected explorers are going to massively outperform in the coming months.

Keep your eyes on the horizon; barometric bedlam need not affect everyone.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.