Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

Commodities / Protectionism Mar 02, 2018 - 03:10 PM GMTBy: GoldCore

– Global stocks slump as Trump risks trade wars

– Global stocks slump as Trump risks trade wars

– Gold prices little changed despite dollar weakness after tariff news

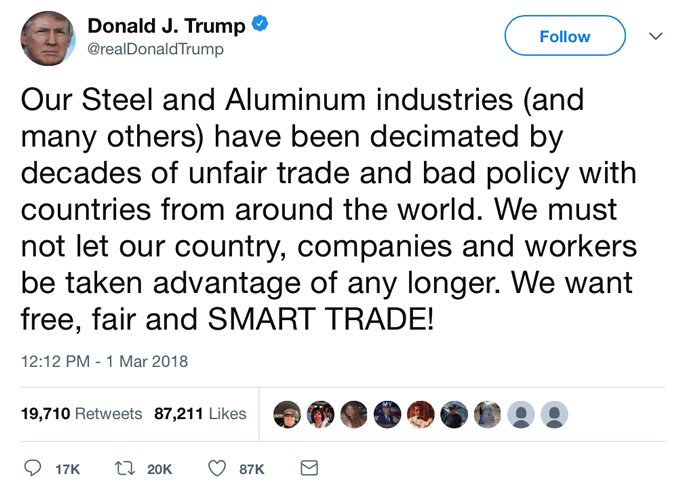

– Trump announced plans to impose heavy tariffs on imported metals

– China likely to retaliate with heavy tariffs on U.S. agricultural exports

– Geo-political tensions with EU and of course China and Russia to escalate

– Trade, currency wars and competitive currency devaluations tend to lead to actual war

– Russia unveils next generation of “invincible nuclear weapons”

– Safe haven gold bullion a hedge against protectionism and economic war

Editor Mark O’Byrne

Fears of a global trade and economic war swept across markets yesterday and this morning as President Trump announced very high tariffs on foreign steel and aluminium. In response U.S., Asian and European stocks has slumped, the dollar weakened and gold prices were flat prior to eking out small gains.

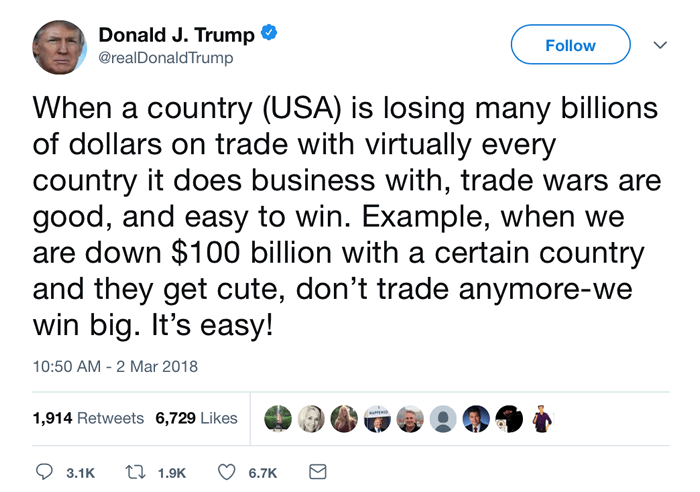

The response drew global condemnation but Trump, showing a wonderful grasp and understanding of economic history, pushed back against a wave of criticism against the hefty steel on imported base metals, with an ignorant tweet saying “trade wars are good and easy to win.”

Trump is facing anger from manufacturers and trade partners in Germany, most EU countries and of course China after announcing tariffs as high as 25% on imported steel and 10% on aluminum for “a long period of time.” The formal order is expected to be signed by Trump next week.

Anyone with even a rudimentary knowledge and understanding of history knows that protectionism and trade wars tend be badly impact economies and can lead to recessions, depressions and indeed war.

China is likely to be most affected by the move, sparking concerns that retaliations could come in the form of trade and currency wars. This is particularly a concern from the likes of Russia and China who have been quietly resisting, what they see as a U.S. drive for global domination, as an increasingly united force, for some time now.

Reverberations and reactions came from across the globe, from as far as Australia where The Australian Industry Group warned that the move may trigger retaliation and a spread of protectionist policies around the globe.

“It’s a really bad idea…it can get pretty dark pretty quickly”

The general consensus by market and trade experts is that this is a wrong-move by the Trump administration, who are once again sticking to emotive campaign promises to American workers and corporations rather than the welfare of the wider U.S. economy and the now closely integrated global economy.

“It’s a really bad idea — how bad depends on what the the rest of the world does in response,” said Mark Zandi, chief economist at Moody’s Analytics Inc, to Bloomberg.

Zandi went on to tell Bloomberg that whilst the US tariffs alone may have only minimal impact on growth and inflation in the US:

“I can’t imagine the rest of the world is going to stand still for very long. The scenarios you can construct can get pretty dark pretty quickly.”

How can a tariff lead to ‘dark’ times? Quite simply through retaliation and unforeseen consequences on the part of the Trump administration.

The EU has already expressed disgust at the move whilst the United States’ own William Dudley warned yesterday of increased pressure on prices and jobs.

Retaliation from EU, China and anywhere else you can think of

Yesterday the EC’s Head Jean-Claude Juncker promised that the Commission would ‘react firmly’ with ‘countermeasures’ to these moves announced by President Trump.

“We will not sit idly while our industry is hit with unfair measures that put thousands of European jobs at risk.”

Reports state that Trump was advised to exclude allies from the tariff but this was ignored. Juncker picked up on this and referred to the EU’s history as a security ally of the United States, expressing his fury at the impact this new move would have on the wider global economy.

Meanwhile in China, officials were warming up to respond with their own tariffs that will impact the country. These measures by the US said Wen Xianjun, vice chairman of the China Nonferrous Metals Industry Association “overturn the international trade order…Other countries, including China, will [also] take relevant retaliatory measures.”

Many expect China to retaliate with its own tariffs on agricultural goods, namely sorghum of which China is the biggest importer of US produce. This could hurt the US but Trump even more:

The US now sends China about US$1billon a year worth of sorghum, the grain used to make gut-busting baiju alcohol. And in the US, much of the sorghum comes from places like Texas, Kansas and Oklahoma – all states handily won by Trump in the 2016 election. It’s almost as if the Chinese leadership keeps a 2016 electoral college map pinned to the wall in Zhongnanhai. Source SCMP

Inflation and interest rate increases

Good news for gold owners is that tariffs such as these will likely lead to an uptick in inflation. But, surely this will increase interest rates? You might argue. Perhaps. But given gold’s response so far to increased rates from the Federal Reserve, it seems like it is unlikely to respond negatively to tightening in monetary policy.

“Raising trade barriers would risk setting off a trade war, which could damage economic growth prospects around the world,” New York Fed President William Dudley said in Brazil on Thursday. “If tariffs go up, it will, at the margin, tend to put more upward pressure on prices, and those upward pressure on prices will have to be considered by the monetary authority.”

Tariff-lead inflation may add to the stagflation pressures that we are already seeing in many western economies – especially the UK. Inflation has been in stealth mode in the US or the rest of the world. Slowly but surely and imperceptibly, people are seeing a reduction in their spending power and increase in living costs. This may become more obvious in the coming months.

This latest move by Trump may not instantly feed through to every-day Americans but it is likely to cost jobs and increase prices after some time-lag.

The impact on jobs and the subsequent reaction is one we should be wary of. Back in the 1970s a rolling belt of shocks and crises (as we see today) signalled the end of a major boom period. In response more government intervention was triggered across the West. New regulations for both the labour and capital markets were introduced, stifling innovation and global trade.

Trade war today, shooting or cyber war tomorrow?

History repeats itself and it looks like we’re going into full repeat mode on the ‘How Politicians Screw Up’ channel. In previous trade wars they have often descended from currency wars as countries fight to compete by devaluing their currencies in order to maintain share of exports and hence jobs.

We appear to be seeing the same happen today. For many years China has kept it’s currency cheap in order to make exports attractive, Trump is calling them out on this. Yet the U.S. and many countries have themselves engaged in competitive currency devaluations in recent years and we look set to see them again.

Unsurprisingly countries soon find an excuse to take issue with its competitor country’s politics and soon give reason to go to war. As Jim Rickards explains:

After a few years, the futility of currency wars becomes apparent, and countries resort to trade wars. This consists of punitive tariffs, export subsidies and nontariff barriers to trade.

The dynamic is the same as in a currency war. The first country to impose tariffs gets a short-term advantage, but retaliation is not long in coming and the initial advantage is eliminated as trading partners impose tariffs in response.

Trade wars produce the same result as currency wars. Despite the illusion of short-term advantage, in the long-run everyone is worse off. The original condition of too much debt and too little growth never goes away.

Finally, tensions rise, rival blocs are formed and a shooting war begins. The shooting wars often have a not-so-hidden economic grievance or rationale behind them.

Already we appear to be in a low level cyber war as Russia, China and western nations show their muscle when it comes to hacking and taking control of various online services and infrastructures. These tensions and this already fraught situation could deteriorate quickly.

This is no longer just about cyber wars, yesterday Putin proudly unveiled the country’s new armament. Stating that the West needed to learn that the new state of affairs was ‘not a bluff’ he revealed the “low-flying, difficult-to-spot cruise missile… with a practically unlimited range and an unpredictable flight path, which can bypass lines of interception and is invincible in the face of all existing and future systems of both missile defence and air defence.”

The Cold War is back and is hotting up with the very real risk of Hot War and all that entails.

Make sure your wealth doesn’t get ‘called up’ to fight in the war

There are many side-effects of wartime, one of the most long-lasting is the financial impact on individuals’ savings. As explained, trade wars frequently turn to currency wars which can decimate the capital of companies and the wealth of people and nations. It can also result in stocks and shares losing value sharply and crashing and and cause governments to devalue people’s savings and in the next crisis, bail-ins will likely see savers’ accounts plundered … all for the public good of course.

This is where gold bullion comes into its own. Throughout history it has acted as a safe haven during times of protectionism and economic war. This was seen most recently in the 1970s.

The world was already a very uncertain financial and economic place with a lot of clouds on the horizon. Trump’s reckless actions have made this outlook even more uncertain. This bodes well for the gold price in the coming months and years.

Safe haven gold bullion will come into its own as these real risks become manifest.

Gold Prices (LBMA AM)

02 Mar: USD 1,316.75, GBP 955.70 & EUR 1,071.04 per ounce

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

28 Feb: USD 1,320.30, GBP 951.14 & EUR 1,080.53 per ounce

27 Feb: USD 1,332.75, GBP 954.78 & EUR 1,081.26 per ounce

26 Feb: USD 1,339.05, GBP 953.00 & EUR 1,085.30 per ounce

23 Feb: USD 1,328.90, GBP 951.09 & EUR 1,079.20 per ounce

22 Feb: USD 1,323.50, GBP 952.66 & EUR 1,076.40 per ounce

Silver Prices (LBMA)

02 Mar: USD 16.45, GBP 11.92 & EUR 13.36 per ounce

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

28 Feb: USD 16.44, GBP 11.88 & EUR 13.45 per ounce

27 Feb: USD 16.61, GBP 11.91 & EUR 13.48 per ounce

26 Feb: USD 16.67, GBP 11.88 & EUR 13.52 per ounce

23 Feb: USD 16.61, GBP 11.88 & EUR 13.50 per ounce

22 Feb: USD 16.47, GBP 11.86 & EUR 13.40 per ounce

Mark O'Byrne

This update can be found on the GoldCore blog here.

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information containd in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.