Brexit UK Vulnerable As Gold Bar Exports Distort UK Trade Figures

Commodities / Gold and Silver 2017 Oct 18, 2017 - 10:40 AM GMTBy: GoldCore

– Brexit UK vulnerable as gold bar exports distort UK trade figures

– Brexit UK vulnerable as gold bar exports distort UK trade figures

– Britain’s gold exports worth more than any other physical export

– Gold accounted for more than one in ten pounds of UK exports in July 2017

– UK’s stock of wealth has collapsed from a surplus of £469bn to a net deficit of £22bn – ONS error

– Brexiteers argue majority of trade is outside EU, this is due to large London gold exports

– Single gold bar (London Good Delivery) is, at today’s prices, worth just over £400,000

– “There are few things you’ll ever touch which pack so much weight into such a small size”

– UK’s economic vulnerability means safe haven gold essential protection

I’ve never played poker but I’m pretty sure the number one rule is not to reveal your cards to your opponents.

Yesterday the ONS possibly gave the EU one of the biggest reveals so far in Brexit negotiations. Revised figures from the statistics bureau showed the country’s stock of wealth has fallen from a surplus of £469 billion to a net deficit of £22 billion as reported by LBC.

This is down to FDI and fall in reserve foreign assets. In the first half of the year FDI fell from a £120 billion surplus in the first half of 2016 to a £25 billion deficit for the first half of this year.

With the UK totally losing its foreign assets, the EU (and the rest of the world) is aware that its safety net is no longer there. Not great timing, just as the government is trying to get through this crucial stage of Brexit negotiations.

The amount that has been knocked off the UK’s wealth is the equivalent of 40% of EU contributions. The bank balance isn’t the only thing the UK has at best misunderstood or at worst been mislead over. Their trade is not as internationally diverse as Brexiteers might have led markets to believe.

Following the referendum result there was an increase in Britain’s exports. Many pointed to the numbers as a sign of confidence in the future of the UK, following the Brexit vote.

It turns out that much maligned gold was to thank for this uptick. Without gold, the majority of the UK’s trade would be with the EU.

This is a reminder of how vulnerable we are to negotiations and reliant we are on the precious metal.

Gold’s saving role

As we can all recall, there was an air of uncertainty and panic surrounding the UK’s referendum last June. This prompted investors to diversify into gold bullion as a safe haven.

The increase in purchases of gold bars was so big that estimates of the country’s end-of-year GDP were pushed up. The majority of the gold sold in London eventually goes onto Switzerland, India and China. Therefore the export of gold is recorded as non-EU trade.

It is this that politicians, economists and the mainstream saw when they looked at export figures. An uptick in non-EU trade led them to conclude that Britain’s exports to the EU were growing which was a sign of confidence in the soon-to-be ex-EU Britain.

It was more of a sign of faith in the London Gold market over others in the UK. This past July Britain’s gold exports were greater than any other (physical) export. More than 10% of the value of UK exports in July were accounted for by gold.

Gold, the ultimate test for lack of confidence in the UK

Much of the gold didn’t even hang around in the UK. So little confidence did investors have. Reports show that some of that bullion bought in London was then moved out of the country to China, by investors, at the end of 2016.

These purchases and movement of gold was a double-edged sword, or contrasting sign of confidence and lack of confidence. It is an indication that foreign investors were still faithful to the hallmark that is the London Gold market, however have declining confidence in the United Kingdom.

Ed Conway on Sky News, explains the tricky picture this creates for those pushing confidence in the UK:

This raises doubts over one of the few Brexit claims which has yet to be challenged – that Britain now exports far more outside the EU than inside.

The official trade figures produced by HM Revenue & Customs show that over the past five years the EU’s share of Britain’s exports has dropped to 46%.

But strip gold out of the statistics and the EU’s share is still 50%. Falling, yes, but not quite as fast as the official numbers might have you believe.

There are a few provisos: for one thing, these numbers don’t include services trade – Britain’s real speciality, particularly with non-European partners.

Even so, when you exclude gold from the overall trade balance (goods and services) – a tricky operation since the numbers are fiddly and not altogether comparable – a similar thing happens: the share going to the EU rises from about 45% to 47%.

The lesson is clear: that while Britain remains a dynamic trading nation, it is actually considerably more reliant on trade with Europe than the official numbers suggest.

International investors put their faith in gold

No matter how long someone works in the world of gold investment, it never ceases to amaze how much faith and value is put into something so small. A London Good Delivery bar is currently worth just over £400,000. A huge amount given it weighs 12.5 kilos.

But little comes down to size, instead it is about history and solid economic evidence that proves its role as a safe haven and hedge against economic risks.

These increased gold purchases show international investors still hold the London Good Delivery system to a high standard but do not have faith in the economy.

It is quite a contrast to the UK government which puts little faith into gold, with very low gold reserves despite the UK having no natural gold assets for mining.

The faith of foreign investors in gold over the British economy is one which is unlikely to change. Not only is the Brexit picture getting bleaker but so are figures that indicate in what poor health the system is in.

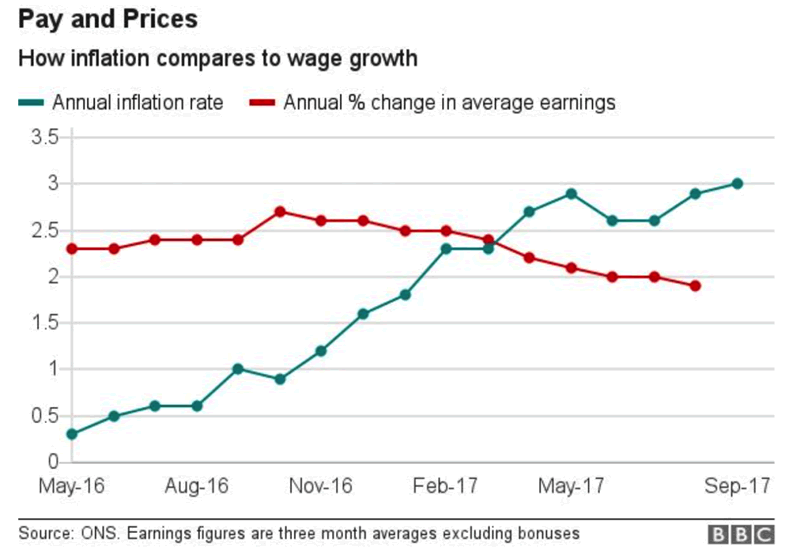

Today the news that inflation has hit 3%, a five-year high, is bad news for all holders of the pound and particular bad news for those who continue to see their wages squeezed.

Gold is an excellent hedge against the serious damage inflation leaves in its wake. It is also an excellent hedge against government mismanagement and weak economic decisions.

International investors and gold buyers including central banks are better informed about this than the UK’s own government. The same group who are supposed to be managing the country’s finances.

Conclusion

Yesterday UK and EU leaders agreed that Brexit negotiations needed to ‘accelerate’. Despite some forced smiles and statements from officials on both sides it’s clear that the most infamous (and expensive) divorce discussion is not going well.

The longer politicians and bureaucrats continue to snipe at one another the less time there is for the United Kingdom to build and grow trade relationships in the wider world.

This is bad news for sterling, for jobs and for our overall wealth. We are in an extremely vulnerable position.

The UK government continues to ask the public for their faith and support in the Brexit negotiations. However this is too little too late. Very little support has been shown for British voters and outside investors when it comes to how the economy has (and will be managed). The public is unlikely to respond positively.

Inflation is climbing, property is stumbling and wages and pensions continue to be at risk from cuts and mismanagement.

Those vulnerable to Brexit negotiations must follow in the footsteps of those international investors by placing their faith in gold rather than await the outcome of negotiations being carried out by self-serving politicians and bureaucrats.

Gold Prices (LBMA AM)

17 Oct: USD 1,289.70, GBP 973.47 & EUR 1,097.02 per ounce

16 Oct: USD 1,305.15, GBP 981.08 & EUR 1,107.03 per ounce

13 Oct: USD 1,293.90, GBP 972.88 & EUR 1,093.73 per ounce

12 Oct: USD 1,294.45, GBP 977.96 & EUR 1,092.26 per ounce

11 Oct: USD 1,290.20, GBP 978.62 & EUR 1,091.90 per ounce

10 Oct: USD 1,289.60, GBP 977.77 & EUR 1,094.61 per ounce

09 Oct: USD 1,282.15, GBP 976.23 & EUR 1,092.01 per ounce

Silver Prices (LBMA)

17 Oct: USD 17.11, GBP 12.96 & EUR 14.55 per ounce

16 Oct: USD 17.41, GBP 13.09 & EUR 14.75 per ounce

13 Oct: USD 17.20, GBP 12.94 & EUR 14.55 per ounce

12 Oct: USD 17.20, GBP 13.06 & EUR 14.50 per ounce

11 Oct: USD 17.15, GBP 13.00 & EUR 14.51 per ounce

10 Oct: USD 17.12, GBP 12.98 & EUR 14.53 per ounce

09 Oct: USD 16.92, GBP 12.86 & EUR 14.41 per ounce

Mark O'Byrne

This update can be found on the GoldCore blog here.

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information containd in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.