Graphite Seeing Some Upward Movement

Commodities / Graphene Oct 06, 2017 - 06:21 PM GMTBy: The_Gold_Report

With graphite prices starting to move upward, Ron Struthers of Struther's Resource Stock Report provides a primer on graphite and discusses his evaluation method for graphite companies.

With graphite prices starting to move upward, Ron Struthers of Struther's Resource Stock Report provides a primer on graphite and discusses his evaluation method for graphite companies.

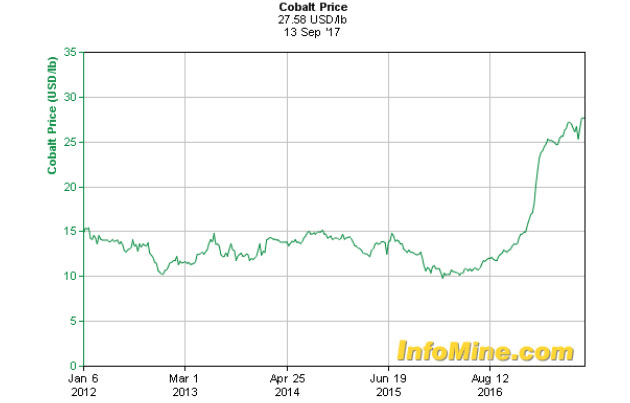

Lithium, graphite, vanadium, cobalt and other metals have been or are all starting to move higher. The graphite market has shown its first sign of life in a few years with some upward price pressure.

Lithium and Cobalt:

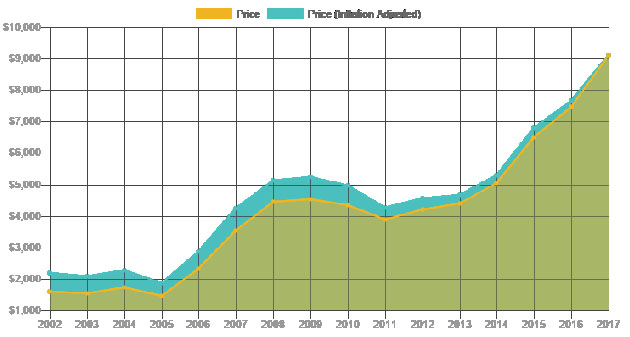

Lithium Price

The lithium price started taking off in 2014 and cobalt in 2017; graphite headed down in 2014 and has been trading flat since, but we are just now seeing some upward movement as noted by Northern Graphite, about a 30% rise in large flake graphite. Industrial Mineral Magazine noted that the supply of large and XL flake graphite is tight and some speculative investment is taking place.

However, much has changed and can be learned from the last up cycle in graphite.

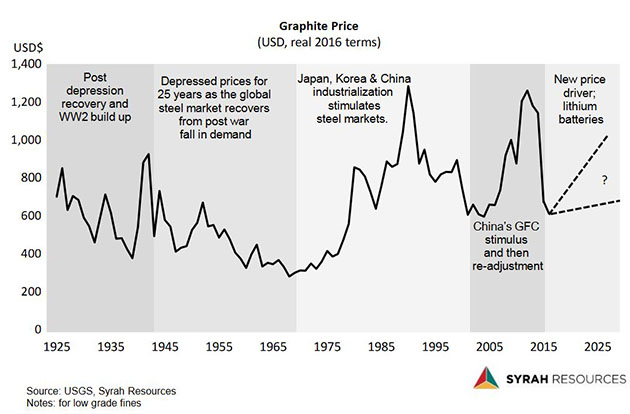

First, a look at a long-term price chart to give some current perspective. I got this from Syrah Resources Ltd.'s (SYR:ASX) website and like how it highlights the key drivers during the cycles. We know for certain now that the lithium battery cycle has already had a big effect on lithium and cobalt prices and the same will happen with graphite, only the extent or magnitude is not known and Syrah shows this with a predicted range and question mark.

Graphite 101

Since the last up cycle starting around 2010, despite all the time and money spent, there are no mine start ups in North America. I see two main reasons for this. First, they can't compete with the lower cost operations of current graphite mines, so much higher prices are needed for any chance of a North American startup.

Second, and probably the investor's most fatal error, is they think graphite juniors are like other mining juniors—drilling, 43-101 resource, PEA, mine permitting and financing, etc. This does not work for a few reasons.

First off, there is no market for graphite as there is for other metals and commodities. A graphite miner must make relations with end users or customers, such as offtake agreements. This is a major stumbling block because most North American juniors have not modeled their companies properly for this. They face a big hurdle because their PEA says they must produce say 40,000 tonnes per year or more of graphite for the economics to work, but few if any end users will agree to this much tonnage.

End users will require bulk samples to test and make sure it meets their needs. There are many uses and applications for graphite so depending what the user is producing their requirements will differ. They will also want large samples, in tons to verify their processes. Imagine how a junior is going to secure an offtake agreement when it cannot even predict when it will be producing, receive permits, get needed financing etc. Few if any end user are going to agree to buy your graphite at uncertain dates years down the road.

This is a very difficult scenario to overcome, matching your PEA production requirements with end users. Many juniors instead have focused on testing their graphite for battery use or this use or that to prove it will work. This is fine and dandy but may not necessarily help land offtake agreements.

The best solution is to start off mining smaller amounts, perhaps a few thousand tons per year to, say, maybe 10,000 tons and have an offtake agreement for that. Then ramp up production to higher amounts as you secure more end users. This also provides a method for end users to try bulk samples of your graphite and a miner may have to tailor production as users may want large flake or maybe fine graphite or any combination.

Syrah Resources has managed to do this with a lot of work on three or more end user agreements that will start at a low tonnage of 10,000 to 20,000 tons per year for each offtake and increase in future years.

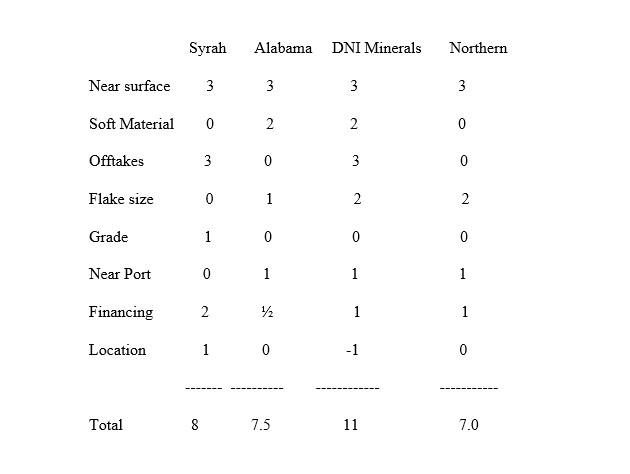

To have an efficient mine that can make money at low tonnage and ramp up production as new users come on board requires some unique properties. I have made up a point system about these qualities to perhaps help you in evaluating junior graphite companies.

Most important and #1 is the deposit must be on or near surface and I mean within 5 to 10 meters of surface at most and on surface ideal. If it is not, avoid the stock like the plague. There are two main reasons: on surface means low mining costs and it is much easier to increase production by expanding outwards rather than having to worry about a pit design going down. I give 3 points for being on surface

#2, if the graphite is in saprolite or a soft material, it makes for easier and cheaper mining and processing so I give another 2 points for this.

#3, is customer relationships and offtake agreements, without these a junior is just treading water. I give this 3 points, but only 1 point if the offtake only covers part of the PEA's annual production.

These are the three most important factors; there are a few others that can make a difference, but are a little less important on the point scale:

#4, Flake size distribution: many types of graphite can be sold profitably, but larger flake does command higher prices so it can help economics of a mine. If a miner is processing its graphite further to perhaps battery grade this might be a moot point, nevertheless, I think one point for 30% to 50% large and jumbo flake and 2 points if the deposit is over 50% large flake.

#5, Grade: more important is the ease of mining the material but all else equal, higher grade means less mining to produce a ton of graphite so it can help lower costs. I am going with one point if the grade is over 12%.

#6 is near port or end users: graphite is sold in I ton sacks in 20 ton containers, so a 10,000 ton per year user would be getting about one container per week. Being near a port or end user can reduce shipping costs. I am giving one point here. Currently all North America companies get one point because all graphite is shipped here from overseas, which makes them closer to end users.

#7 is financing: is always required so I am going with ½ point to one point if they have $0.5 to $5 million and two points over $5 million.

#8 location: I am going to subtract one or two points if the project has poor infrastructure in a non miner friendly location or some other disadvantage where it is located.

I eventually plan to do a table with many of the junior graphite miners on it but for now I will use three on our list, Syrah, Northern Graphite Corporation (NGC:TSX.V; NGPHF:OTCQX) and Alabama Graphite Corp. (CSPG:TSX.V; CSPGF:OTCQB).

Elcora Resources Corp. (ERA:TSX.V) does not really fit here because it is more of a processing company than a miner so is looked at differently.

Syrah Resources is the most advanced and nearing production. Its Balama Project in Mozambique is high grade at 16.2% and on surface but a long distance to the Port of Nacala, some 490km south east of the project. It is mostly fine graphite with only 20% large flake or better, but the mining costs are very low with bulk tonnage of 140,000 to 160,000 tons in the first year and practically no stripping. The company has offtake agreements and is fully financed to go to production.

Alabama Graphite has the Cossa project in Alabama, which is a great location, and the resource is on surface in soft weathered rock. The company has just over 30% large flake and it is low grade just under 3%. Alabama has demonstrated in a PEA that it can produce battery-grade graphite. The company has no offtake agreement.

Northern Graphite's Bisset Creek is the only North American project with a bankable feasibility study. The project is near good infrastructure and has a lot of large and jumbo flake with a relative low grade at 1.65%. It has demonstrated it can produce battery-grade graphite and have no offtake agreements.

This point evaluation system is more about the graphite deposit as there are other factors that can affect an investment. Obviously, Syrah is totally different because it is near production. Some stocks will be priced too high, others too low. How advanced is the project, the size, management and do they have enough cash to go to next level? There are so many factors to consider.

However, having a very good project is the best place and way to start. That is why I highlighted:

DNI Metals Inc. (DNI:TSX.V; DG7:FSE) Recent Price $0.10

52 week trading range $0.02 to $0.15

Shares outstanding 63.3 million

The company has two projects adjacent to each other in Madagascar on a highway and just 50 km to the seaport. It already has a mining permit and the deposits are on surface in soft saprolite. Cougar Metals of Australia is advancing one project, the Vohitsara, and must complete a 43-101 resource and a PEA to earn 50%.

DNI is advancing the adjacent project, the Marofody, (same graphite) 100% and is indicated as 'NEW' on the map above. Both projects have seen a lot of trenching and some drilling and it looks like grades will be 5% to 10%, but with no 43-101, I could not give any points or certainty here.

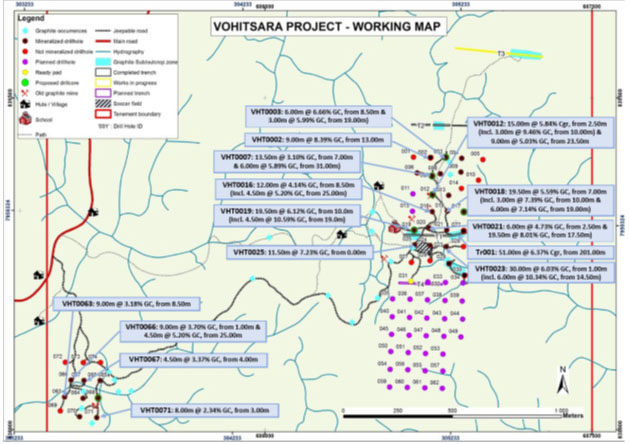

Vohitsara Project

Cougar Metals negotiated an extension with DNI Metals on its agreement so now it must complete an NI 43-101 resource report by October 31, 2017, and complete an NI 43-101 compliant PEA by December 31 to earn 50% interest in the project.

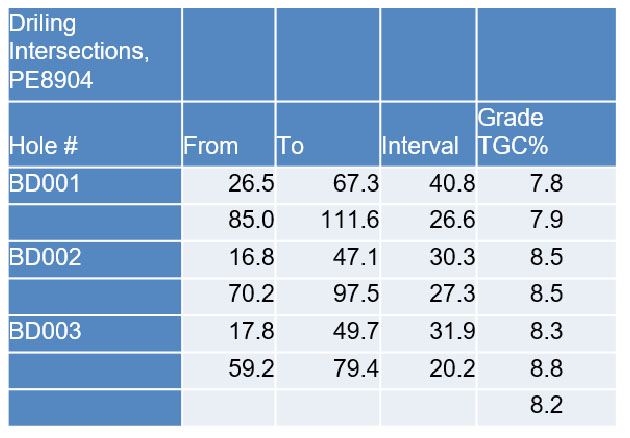

As of August 31, 45 air core drill holes and five diamond core holes have been reported with an average depth of the saprolite being approximately 28 meters on the property. The best intersect was 51 meters of 6.37% Cg. These recent results complement the initial results from the Main zone released on July 24, 2017, which included:

- VHT0025: 11.5 meters at 7.23% Cg (graphitic carbon) from surface;

- VHT0016: 12 meters at 4.14% Cg from 8.5 meters, and 4.5 meters at 5.2% Cg from 25 meters;

- VHT0019: 19.5 meters at 6.12% Cg from 10 meters, including 4.5 meters at 10.59% Cg from 19 meters.

On this drill map below if you find it hard to read, the black dots are highlighted holes that are complete and purple dots extending down are planned holes to complete the resource. Last update on drilling was the end of August and Cougar Metals just announced funds for drilling in mid September so looks like it will be hard pressed to complete the 43-101 resource by the end of October. However, the drill is on site and drilling will go very quickly because it is shallow and in soft saprolite.

DNI has done bulk samples for metallurgy test work with simple processing that resulted in over 98% total carbon with 28% super jumbo flakes and 65% large flake in the high-grade sample and 53% large flake in a lower-grade sample.

Marafody Project

On July 26, 2017, the company entered into a non-binding agreement (“LOI”) to buy a property in Madagascar called the Marafody property. The purchase price for Marofody is U$1,650,000 cash, payable as follows:

- USD $100,000, upon signing the LOI

- USD $550,000 shall be paid in 60 days,

- USD $1,000,000 shall be paid in 90 days.

Over 600 meters of trenching has been completed by the previous owners. There was also some drilling done but not up to NI 43-101 standards, so it should be viewed as historical data. Nevertheless, it shows similar results to the adjacent Vohitsara project.

Wholesale Graphite Business

DNI also has a wholesale graphite business shipping material from high-quality producers in Brazil to North America, which has shown a steady increase in volume over the past year. This is very beneficial because of the relationships DNI has with end users.

On August 1, DNI announced an offtake agreement with Peninsula Mines to supply initially up to 20,000 tonnes per year to Korean end users.

Financial

Currently the company needs to raise some money to acquire and finish drilling on the Marafody project and complete the pilot plant. The pilot plant will be designed to process up to 6,000 tonnes per year.

To this end the company announced a $2.4 million financing and increased it to $2.8 million on September 25 for up to 35 million units at eight cents per unit and a full purchase warrant at 16 cents per share good for a period on 18 months. This financing has gone very well and I believe it is oversold.

Management

Daniel J. Weir, Executive Chairman, has worked for over 20 years at some of the top financial firms in Canada. He worked as an Institutional Equity Trader, and as a broker he managed over $500 million. Before joining DNI in November 2014, he was the Head of Institutional Sales at a boutique firm focused on financing mining companies. Having raised millions of dollars, both public and privately, Mr. Weir has expertise at evaluating and financing mining deals. Dan has managed large high tech electrical and energy management projects, having put himself through university as an electrician. Dan graduated from University of Toronto.

Paul L. Hart, MBA, CPA, CA Director,is a seasoned finance and operations executive with experience in the C-Suite, most recently as Chief Financial Officer and Corporate Secretary for a lithium ion battery manufacturer. In addition to his experience in clean-technology, he has held senior financial roles with public companies (TSX, NASDAQ) in the software, internet and financial services industries.

John Carter, Director, is currently the CEO of Northern Sphere Mining. Has over 35 years of experience in the metals and mining industries. Mr. Carter specializes in the engineering design and manufacturing of mineral processing equipment for mining operations and operators such as Timcal Inc., currently the largest natural graphite mining company in North America. He has built over 200 mineral processing plants around the world, including three graphite processing plants.

Keith Minty, P.Eng. MBA, Director, has more than 30 years of professional experience in mineral resource exploration and development in precious and base metals, industrial minerals. Mr. Minty obtained extensive graphite technical and operating experience at both North Coast Industries (now Northern Graphite Corporation) Bissett Creek Graphite and Cal Graphite Corporation (now Ontario Graphite Inc.) Kearney graphite mine and has experience of in the development of several past and new Sri Lanka graphite projects. Mr. Minty has had the opportunity of conducting Madagascar precious metals project valuations and is knowledgeable of the political and social requirements associated with Madagascar project development and operations.

Summary

Some may believe Madagascar carries some geopolitical risk but it is well known for its graphite and holds just over 50% of the worlds reserves. There has been over $9 billion invested in mining projects in Madagascar with the likes of Rio Tinto, Sherritt, Sumitomo and Kores. DNI's project lies in a well-defined graphitic belt, which has been producing for over 50 years.

DNI has two very good graphite properties that are on surface and hosted in soft saprolite material. This will make it very easy and cheap to mine. The company is carried on the Volhitsara project and has a 100% interest in its adjacent Marafody project.

Management has a lot of experience in graphite, currently running a graphite wholesale business and has previously built three graphite processing plants. The company has end user relationships with the wholesale business and an offtake agreement with Peninsula Mines to supply Korea.

On August, 17, 2017, DNI announced that it would be building a modular graphite pilot plant in Madagascar in order to test multiple zones in both of DNI’s projects and to produce up 6,000 tonnes of graphite per year.

There projects are very near infrastructure and appear to be a very good grade with a high percentage of large and jumbo flake. Mining permits are already in place.

For a graphite junior it simply cannot get much better than this. All it has to do is raise enough financing and execute.

Including the current financing there are approximately 98 million shares out and round up to an even 100 million and at 10 cents is only a $10 million market cap. This makes the valuation much cheaper than all the other graphite juniors I follow and I would surmise that within a few months when drilling and 43-101 resource numbers are completed, it may just have the best deposits.

The stock ran up in August on news and developments and the recent pull back in price provides a good entry point.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Ron Struthers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: DNI Metals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: DNI Metals is an advertiser at playstocks.net. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of DNI Metals, a company mentioned in this article.

Charts provided by the author.

(c) Copyright 2017, Struther's Resource Stock Report

i All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication. /i

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.