Few People Grasp What Geopolitical Power Shale Oil Gives To The US

Commodities / Shale Oil and Gas Jul 05, 2017 - 04:22 PM GMTBy: John_Mauldin

I know no one else with George Friedman’s breadth and depth of insight into today’s world.

I know no one else with George Friedman’s breadth and depth of insight into today’s world.

Right at the root of today’s major global issues, we find one little word: oil. So, I’ve asked George to bring us up to speed on the geopolitical implications of a remarkable phenomenon: the US shale oil industry.

There is good news here for the US, but big bad news for Saudi Arabia and Russia—and in fact any country with oil exports as its main source of income.

But without further ado, I’ll let George and his team enlighten you on this development themselves.

Shale Oil: Another Layer of US Power

June 15, 2017

Summary

There’s scarcely a reason to point out how geopolitically important energy is. Energy, particularly oil, is a source of geopolitical power. Every country needs it, but only some countries have the resources to procure it themselves. Some countries have enough of it that they can profit from its export, and others have so much that they rely on it almost exclusively to fuel their economies.

Saudi Arabia and Russia are two such countries. They spend a lot of money on social services, and they can afford to do so as long as oil revenue keeps flowing in. In times of prosperity, they can, through OPEC, bully other countries into doing their bidding and even dictate the direction of markets. But when oil prices are low, as they are now, they simply don’t have as much money to pacify their populations or exert influence abroad. Pressure on their governments builds.

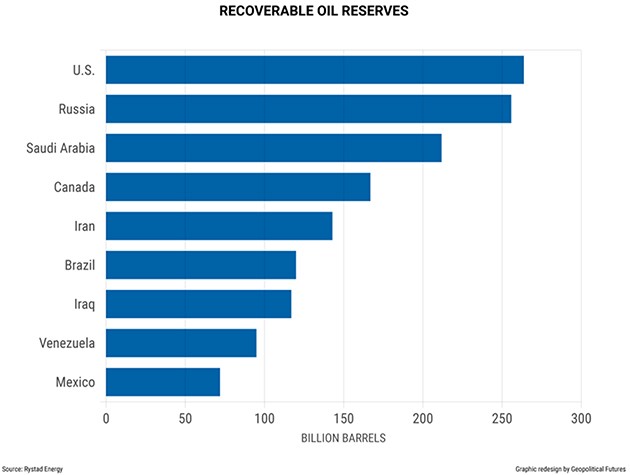

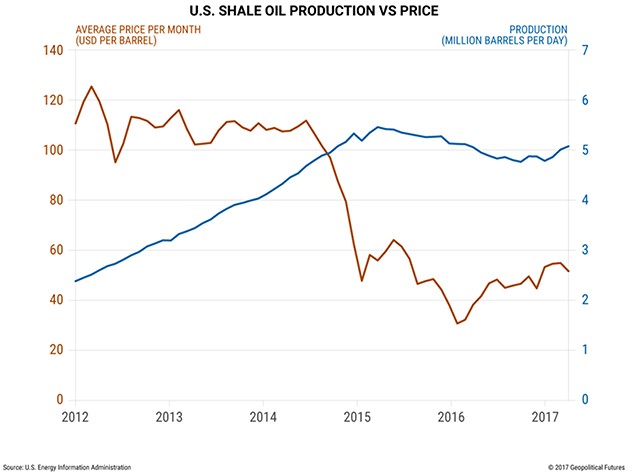

Simple supply and demand helps to explain why prices are low. When prices bottomed out a few years ago, most oil producers, including Saudi Arabia and Russia, were expected to cut production to normalize prices. Instead, they kept production high to increase their market share, thinking (incorrectly) that they would capitalize when prices rebounded. But perhaps a more important reason supply is so high, despite recent efforts by OPEC and Russia to cut production, is that the United States has exceeded expectations on how much oil it could bring to market. With the continued use of hydraulic fracturing and other related technologies, the United States is now believed to have more recoverable oil reserves than any other country in the world, and it is reaping the benefits of its newfound status.

Geopolitical Futures doesn’t forecast commodity prices, so we make no attempt to do so here. But the following report will outline a trend that has emerged over the past several years, one that will maintain downward pressure on prices and thus alter the global geopolitical landscape: affordable shale oil drilling in the United States.

Introduction

Saudi Arabia and Russia are geopolitically important countries. What happens to Saudi Arabia affects the regional balance of the Middle East, and what happens to Russia affects Europe, East Asia and beyond. Their importance is due in no small part to their vast energy reserves, which are their primary source of government revenue. They create a high standard of living to which their populations are accustomed, pay state employees and give the government gravity on the global stage.

Since so much depends on energy, oil prices are more than just financially important. In Saudi Arabia, oil revenue has enabled the government to create patronage networks public and private alike. It has also enabled Riyadh to be the de facto leader of the Middle East. Without oil revenue, the government could not fund its Sunni Arab proxy groups in the battle for regional control, finance the war in Yemen, or even maintain social stability.

The story is much the same in Russia. Financial reserves have dwindled. Russia is considering cutting defense spending in the coming years (something it rarely does) and is struggling to finance state pensions. Now that its Reserve Fund is being depleted, Moscow will have to switch over to its National Wealth Fund, which has a little over $70 billion but which is, for various reasons, much more difficult to tap into.

OPEC, which Saudi Arabia essentially leads, has so much recoverable oil that it has been able to more or less control oil prices by adjusting production levels, sometimes in concert with Russia. But that is no longer the case. By some estimates, the United States has surpassed Saudi Arabia in recoverable oil reserves as advancements in hydraulic fracturing and horizontal drilling have enabled producers to access areas previously not thought possible.

A Deep History

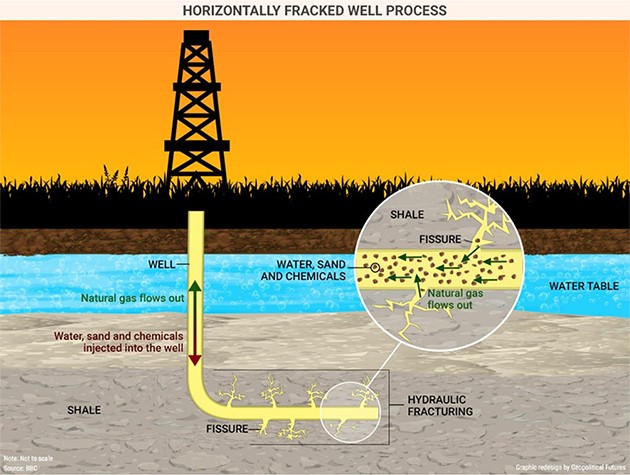

Hydraulic fracturing, more commonly referred to as fracking, is a process by which oil deposits found in shale rock formations are extracted. Shale oil, also called tight oil, is enmeshed in shale rock, which is located thousands of feet beneath the Earth’s surface and is generally less permeable than other rock types, making deposits more difficult to access—difficult, but not impossible. Once producers drill down far enough to reach the shale deposits, they inject a solution made mostly of water (hence hydraulic) at high speeds to break apart the rock (hence fracturing), creating fissures through which oil can flow. Included in the solution are certain chemicals that assist in the extraction process and a kind of sand that keeps the fissures open once the fracturing is complete. (The process can also be used for natural gas, and its effect on natural gas prices is similar, but for the purposes of this report we will focus on oil.)

Though fracking has become more of a household term in recent years, it’s hardly a new technology. It dates back to the mid-19th century, when a man named Col. Edward Roberts devised a way to lower an explosive device through a pipe in an oil well that had already been drilled. Some of the wells in which this technique was used were thereafter 1,000 percent more productive (that’s not a typo).

Roberts’ explosive device was eventually replaced by another explosive, nitroglycerine. Even though nitroglycerine was used as late as the 1990s, companies began to experiment with using more inert materials as early as the 1930s. In 1949, Halliburton became the first company to fracture a well with water.

It was also in the 1990s that producers began to combine fracking with a separate process known as horizontal drilling, which allows a well to be drilled vertically, then, when the drill hits the desired sedimentary layer, it is turned to drill parallel to the layer. In 1991, a well was successfully horizontally drilled and fractured for the first time, and in 1998, the first profitable horizontally fractured well was completed. The supply of US shale gas, and later shale oil, has increased ever since.

The United States has benefited from the shale revolution more than any other country. Not only does it have extensive shale formations, but most of its wells are located entirely within its territory, so producers don’t have to compete for jurisdiction or share their profits. (Brazil and Paraguay, for example, have overlapping oil interests that have sparked debate over ownership and sovereignty.) Still, the shale revolution is not exclusively American. Canada has some shale plays in operation, and from 2020 to 2040, Russia and Argentina are expected to tap into their shale oil reserves.

In the meantime, the United States is likely to become a net energy exporter in 2017, according to some estimates from the US Energy Information Administration. This is no small development; energy independence has been a strategic objective of Washington’s for some time. Shale oil has given it the means to achieve its goal.

Peculiar Economics

Energy independence, however, depends on the peculiar economics of the shale industry. Drilling for shale oil costs less per project than, say, deep-water drilling. There are two general types of costs: capital costs and operating costs. Capital costs are the investment required to drill and complete the well and build the facilities onsite to manage it. Operating costs are the ongoing costs after the well has been drilled. These are measured either in dollar per thousand cubic feet or in dollar per barrel.

The total well cost—the entire amount of investment required to set up a new well, including land, permits, drilling and completion—varies by location, but runs consistently in the low millions of dollars. A report by the EIA estimated that the average completion cost per well is around $5 million to $9 million, depending on the location of the deposits. Some companies, however, are able to drill and complete wells much more cheaply; Chesapeake Energy was able to complete wells in the Mississippi Lime in northern Oklahoma for $2.8 million per well in 2015.

According to the EIA, drilling accounts for 30–40 percent of all capital costs. Completion costs, which include the actual fracking process, account for 55–70 percent. Facilities costs, which include erecting onsite buildings as well as road construction to transport oil away from the site, account for 7–8 percent of well costs.

The same EIA report analyzed well completion costs across a number of companies and locations and determined that average costs, in terms of dollar per barrel of oil equivalent—an approximation of energy released by burning one barrel of oil—declined 7–22 percent from 2014 to 2015 and 25–30 percent from 2012 to 2015.

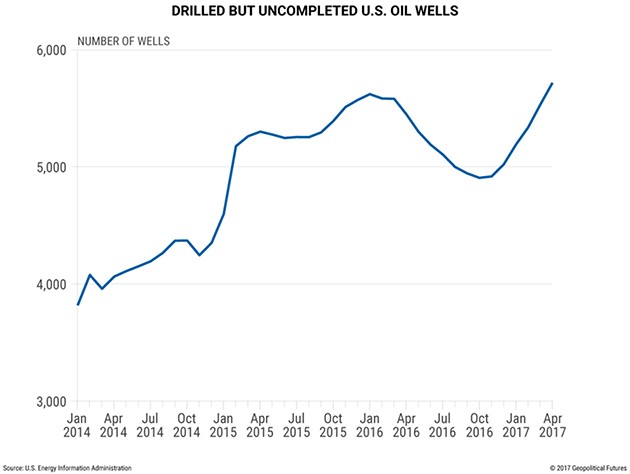

Importantly, some wells are drilled but not completed when funds dry up or when oil prices dictate that the well is no longer economically viable for the time being. In this scenario, the oil driller has effectively used the low permeability of the sedimentary layer to store oil until it’s ready to frack the deposits.

Once the oil starts to flow, operating costs tend to vary. Gathering, processing, and transporting can range from $2.25 to $5 per barrel for oil or higher, depending on how far it needs to be transported. Water disposal can range from $1 to $8 per barrel. Other general and administrative expenses range from $1 to $4 per barrel.

New drilling techniques can expedite the completion process and thus drive costs down further. Several years ago, a new well might have taken 3–4 weeks to drill. Now it can take as few as 7–10 days. Not only does this cut down on the overall costs of producing a barrel of oil, it also gives producers flexibility to respond to higher prices and to expand their operations. In fact, now that so many shale plays are known to produce, exploration is less risky, so companies are more willing to operate there.

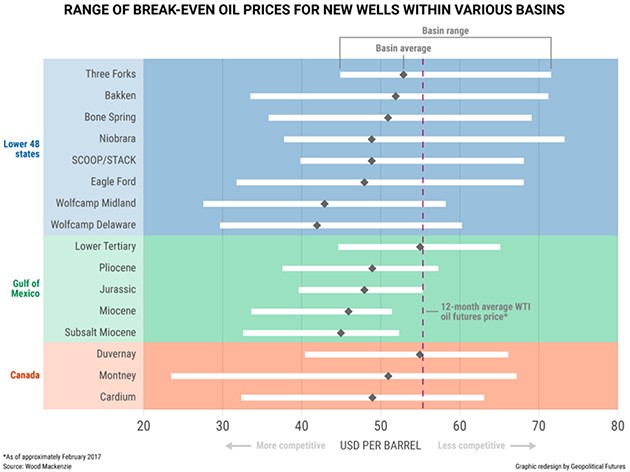

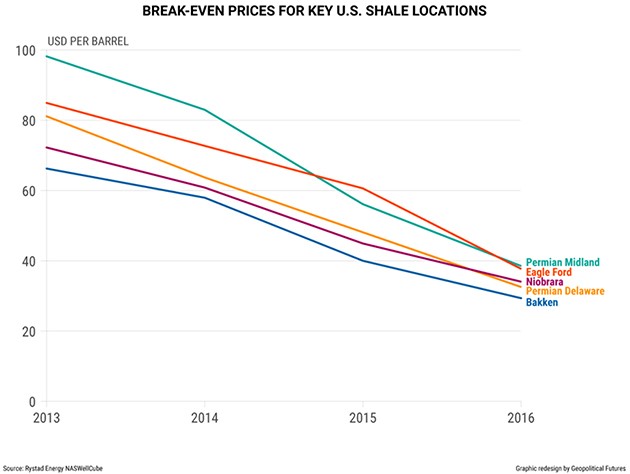

Since capital and operating costs are so varied, there is no single break-even price for shale oil. But if we average wells by location, we can get a sense of which prices generate profit and which do not.

Wood Mackenzie, an energy research and consulting firm, estimates that 60 percent of all crude reserves that are economically viable at $60 per barrel or less are located in US shale reserves. This figure is different for every well, of course—some are unprofitable even at $46.88—but it is notably lower than the break-even price just a few years ago, around $80–$100 per barrel.

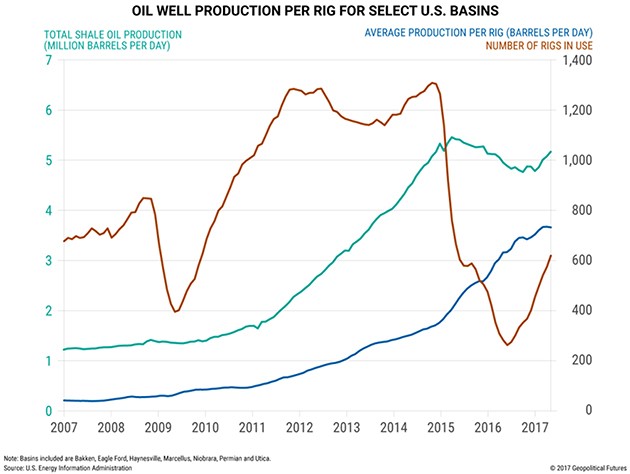

In fact, break-even prices are down at most shale locations. This is partly because of lower costs and partly because of higher yield enabled by newer technologies. And while total rig count has declined significantly, production has remained stable.

What complicates things is that technological innovation raised some absolute costs of drilling even as it yielded more oil from wells. Consider fracking sand. Producers eventually figured out that if they injected the wells with a hydraulic solution that contained more sand than the previous solutions did, their wells yielded more oil. The solution was then adopted throughout the industry. This increased the demand and therefore the price for sand.

The price of labor has risen too. When oil prices declined from mid-2014 to early 2016, many shale sites were left uncompleted and their crews laid off. When prices rebounded to the $40–$50 range, as many as 400,000 workers returned to complete the wells. But since the demand for labor was widespread, companies were forced to offer more competitive wages to attract skilled personnel back to their sites.

And then there are the vendors who provide goods to drilling companies. When prices bottomed out in 2015, vendors sold their wares at low margins—the only way companies could afford them. If the price of oil rises in the next 1–3 years, vendors will raise their prices in kind, knowing that their customers can foot the bill. These short-term gains, however, will be modest at best. Some analysts believe the inflation rate of input costs could reach 10–20 percent.

Drilling companies also have to pay for the land on which they operate. Some of the richer shale territories such as the Permian Basin charge a high price because they are in such high demand. The Trump administration has pledged to make it easier for companies to drill for oil, and if that is the case, it’s reasonable to assume there may be more land available for shale exploration in the future.

Costly though these factors may be, they are ultimately short-term risks for energy companies. The industry would continue to innovate even if, all things equal, oil prices increased. In fact, wells have been pretty productive independently of price trends. Higher prices will keep the drillers drilling until oversupply drives prices down again.

No Reason Not To

And therein lie the geopolitical consequences of the shale revolution. In Russia and Saudi Arabia, it’s still much cheaper to drill for conventional oil than for shale oil. Each can produce a barrel for about $10–$15. With oil priced at $50, the government in Riyadh will make more money off a single barrel than a shale oil driller will for the foreseeable future. This explains why, even when prices fell so dramatically from 2014 to 2016, OPEC could afford to maintain high levels of production. Its members (and Russia) thought that if they kept prices low and captured market share, they could outlast US shale producers who could, in theory, no longer afford to operate.

It was a sensible strategy at the time. The problem is it didn’t work. OPEC didn’t expect shale oil drillers to lower their costs as much as they did, nor did it anticipate how quickly they could complete unfinished projects. A shale oil driller in the United States, moreover, doesn’t need to be more profitable than Saudi Arabia to drill new wells; the driller just needs to fetch a sufficient return on invested capital. When prices are low, drillers simply forgo exploration and concentrate on the completed wells that produce enough oil to justify their existence.

The number of drilled but incomplete wells has grown over the past few months. When oil prices reach the upper end of the $40–$60 per barrel range, these wells will begin to produce, bringing even more oil onto the market. This is a foreboding prospect for countries like Saudi Arabia and Russia that depend so heavily on hydrocarbons. Sure, they can produce oil more cheaply than their US counterparts, but rampant government expenditures make their fiscal break-even point—the price at which their budget is not running a deficit—much higher. The International Monetary Fund estimates that oil will need to cost $78–$80 per barrel in the next two years for the government in Riyadh to break even on its fiscal budget. Russia’s break-even point is lower at $68 per barrel, but it’s still higher than current prices. Short of that, the two countries will have to run budget deficits—which depletes their fiscal reserves—to continue the social spending programs that earn them the support of their people.

For Russia, that means cutting state pension plans on which more than 90 percent of its citizens depend for their retirement. For Saudi Arabia, that means cutting benefits for state employees who have grown accustomed to a comfortable lifestyle. It is in both cases a recipe for social discontent—something both governments are keenly aware of.

US shale producers, meanwhile, are now profitable at levels below the fiscal break-even points of Russia and Saudi Arabia. They have no reason not to drill more. So even if prices climb high enough for Riyadh and Moscow to break even, it is unlikely that they will stay there for long, since high prices encourage shale producers to drill more.

In light of this dynamic, the United States is uniquely positioned to be energy independent—or at least less dependent on oil imports—something it has wanted to be for decades. Contemporary US power is built on two layers: its military might and its relative independence on exports at a time of stagnant global demand. Energy independence would give it a third layer, making it only more powerful. The agility of its oil sector to respond to market forces is simply more than Russia and Saudi Arabia can bring to bear.

Conclusion

OPEC’s strategy—gaining market share to put shale drillers out of business—has failed. Shale oil producers have proved capable of reducing their per barrel costs and competing on the global market at price points that would have been unimaginable just a few years ago. If OPEC (or Russia) raised prices by cutting production, they would make shale producers only more profitable. If they kept prices low by raising production, they would only spur more innovation by shale oil producers.

Geopolitics is rarely a zero-sum game. But in the case of shale oil, what’s good for the US is bad for its rivals.

Get Varying Expert Opinions in One Publication with John Mauldin’s Outside the Box

Every week, celebrated economic commentator John Mauldin highlights a well-researched, controversial essay from a fellow economic expert. Whether you find them inspiring, upsetting, or outrageous… they’ll all make you think Outside the Box. Get the newsletter free in your inbox every Wednesday.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.