Turkey, 'Axis of Gold' and End of US Dollar Hegemony

Commodities / Gold and Silver 2017 Jan 19, 2017 - 02:51 PM GMTBy: GoldCore

Introduction

Introduction

Buy Gold and Lira, Sell Dollars To End “Economic Sabotage” – PM of Turkey

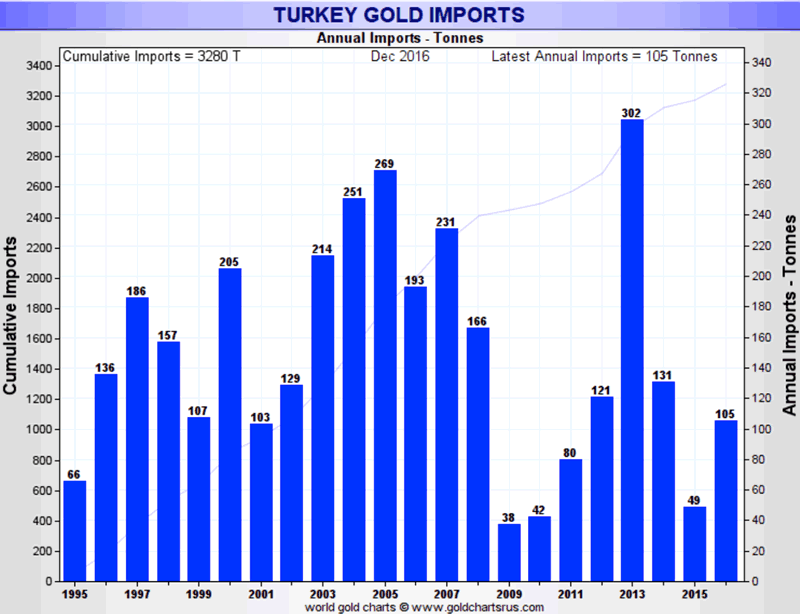

Gold Imports to Turkey Surge 688% In December

‘Tough Turkey’ today

Affinity for gold to save the day?

Central bank gold demand

Personal accumulation

Country’s gold reserves

Turkey Iran gold conduit

Axis of Evil to Axis of Gold

Conclusion: Gold as an insurance policy

Introduction

With a ‘Hard Brexit’ looking more likely and Trump’s inauguration this week, 2017 is well and truly under way.

What we expect the year to hold is probably not even half of what it really will. But from what we know, the upcoming French and German elections, referendums, geopolitical crises, steps towards reverse globalisation and a third of global government debt yielding negative interest rates, governments are already prompting central banks and investors to turn to the one asset that has survived millennia of financial and monetary crises.

One that is highly liquid and convertible into other currencies – gold.

Whilst mining output remains relatively flat and we are at peak gold, Western central banks have stopped gold sales, large emerging market economies continue to increase their gold reserves. China, Russia (both top gold purchasers in 2016) and now Turkey, are the notable players.

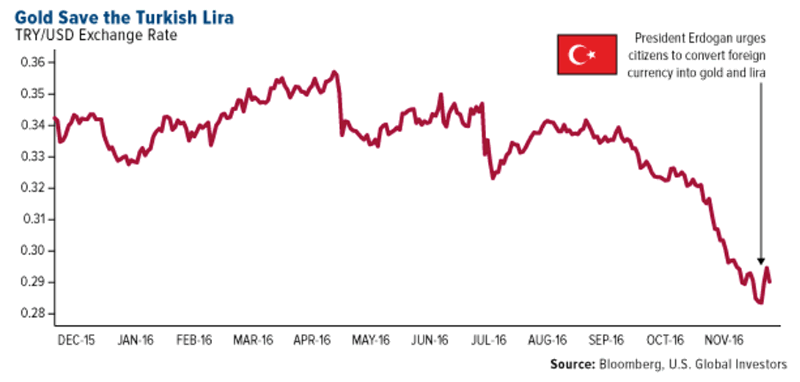

Turkey’s President Recep Tayyip Erdogan reminded us of this when he called on his citizens to buy gold:

“Those who keep dollar or Euro currency under their mattresses should come and turn them into Liras or gold.”

This has been met by such support that, not only did Turkish gold imports surge 688% in December, to reach their highest monthly level in two years but, according to Reuters, “fervent supporters have offered free haircuts, fish and even tombstones to those who can prove they have done so.”

As a result, in December 2016 imports reached 36.7 tonnes, significantly more than the 4.65 tonnes seen in the same month in 2015. This accounted for more than one-third of the country’s annual imports of 106.2 tonnes, more than double 48.7 tonnes in 2015.

Before 1993, the Turkish gold market was not fully liberalised, since then the World Gold Council reports that they have seen ‘rapid growth of the sector’ and this is across all areas relevant to the physical gold market.

Encouragement to buy gold from the likes of Prime Minister Erdogan, who is very popular with huge swathes of the electorate, is not just a selfless act to protect citizens’ wealth during uncertain times in Turkey, the Middle East and across the globe. There are several factors at play here.

These factors should be considered with Turkey’s unique role in the global gold market, in mind. There is no country positioned in such a way (both geographically and politically) that plays all three major roles of producer, buyer and conduit, in the world of gold.

‘Tough Turkey’ today

Since 1950 the country has experienced at least one economic crisis per decade and today it is no secret that Turkey is struggling under both economic and political pressures. Along with heightened security concerns that have damaged the much relied-upon tourism sector, economic growth is sluggish, inflation is rising and a strong US dollar is not helping matters.

Despite this, Erdogan has recently tried to prevent the central bank from increasing interest rates.

All measures since taken by the central bank in order to boost liquidity in the system have lead to short-lived spikes in the Turkish lira. The Fitch-rating review on the 27th January is expected to downgrade the country’s credit rating to +BBB, something not even the failed coup made happen.

The push for support for gold is two-fold, first it is an attempt to boost trust in the central banking system which is in increasingly dire straights, the second is to support the underlying currency which is central to the ‘axis of gold’ (h/t Jim Rickards) that is Russia, China, Turkey and Iran. Both of these things push back against US dollar hegemony.

Gold to save the day?

Turkey’s citizens have long had an affinity to hold physical gold. It is rarely seen as an investment, few look at it as something that they will receive a return on. Instead it is a necessity and something that families hold for wealth preservation and as insurance.

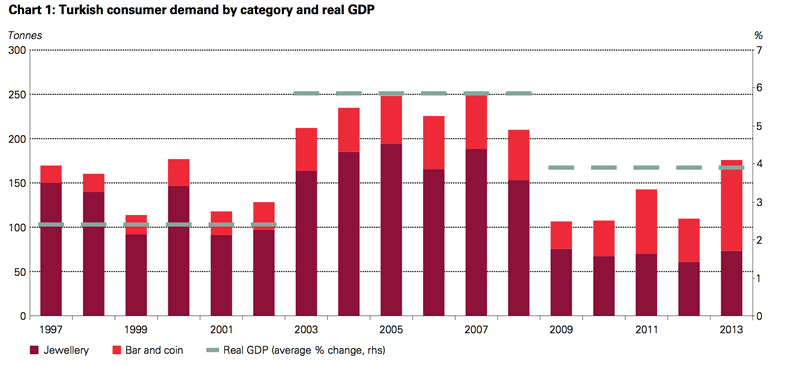

In 2015 the World Gold Council published a report entitled ‘Turkey: Gold In Action’. Much of the report focused on the imports of the country:

“At an average of 181 tonnes per annum over the past 10 years, Turkey is the world’s fourth largest consumer of gold accounting for around 6% of global consumer demand, and we estimate that Turkish households have accumulated at least 3,500t of ‘under-the-pillow’ gold.”

Therefore, it was not unusual for citizens to act on the PM’s exhortation to buy gold when Erdogan made his statement in December. Gold is bought for insurance, rather than investment, and Erdogan has recognised this.

The fall in the lira has meant a slump in demand in recent years, but this has changed recently. Whilst Trump’s victory saw the Turkish lira plummet further, it also drove up gold demand. A move which has been termed the ‘Fear Trade’ by Frank Holmes.

Then Erdogan’s calls for citizens to buy gold not only boosted imports but also helped to give some respite to the currency’s fall. As a result, the Turkish lira has found some support. This may seem a little contradictory given the idea that gold will save the Turkish lira when citizens buy gold. If the gold has to be imported this puts further pressure on the currency and widens the trade deficit.

However, it may be that the majority of recycled gold is bought domestically, which accounts for a large proportion of gold purchases.

Central bank gold demand

The title of this section is misleading. Usually when we talk about central bank gold demand we are referring to how much the central bank has purchased for its own reserves. However, when it comes to Turkish central bank demand they don’t so much need to purchase gold, they just amend policy in order to accumulate others’ holdings and therefore demand more of the yellow metal.

According to WGC data, Turkey has the 14th largest amount of central bank gold reserves with 396.5 tonnes. However, this means little given a proportion of this includes gold holdings by commercial banks. At the bottom of the World Gold Council’s official central bank holding’s list they place a foot note on Turkey, that reads “Gold has been added to Turkey’s balance sheet as a result of a policy accepting gold in its reserve requirements from commercial banks.”

This is because in 2012 the Turkish central bank increased the amount of gold commercial banks could hold as reserves to meet their reserve liability requirements, to 20%. Any form of gold was accepted as collateral. The government were looking to mobilise ‘under the pillow gold’. Banks were also told that gold reserves could not count towards foreign currency liabilities.

The World Gold Council wrote in 2015, “By the end of 2013, commercial banks held around 250t, equivalent to US$10.4bn, some of which had been put to work supporting Turkey’s economy. Most of this was from investors switching Turkish lira and foreign currency into gold accounts. But it also includes 40t – about US$1.7bn – of Turkey’s “under- the-pillow” stock, which has been mobilised since mid-2012.”

The 20% was soon increased to 30% and as of September 2016, an additional 5% was permitted, in order to “…bring out residents’ gold into the economy and to increase foreign exchange reserves.”

It took until just 2014 for the central bank’s reserves to climb by 350% from 2011’s figures and saw gold become the top investment option amongst Turkish citizens’, ahead of real estate.

A central bank paper written in 2014 stated, “the new policy framework… has been successful in achieving a soft landing in the economy and lessening the financial stability risks”.

Personal accumulation

Since the liberalisation of the Turkish gold market, local banks have offered gold accounts for its citizens, however as of 2012 much of the privately held gold was outside of the banking system. Estimates vary as to how much is privately held, ranging from 3,500t to 5,000t.

The government has, since 2011 tried a number of routes and incentives to encourage citizens to get their gold into the banking system, this is part of the drive to reduce the risk of a liquidity crisis.

As Tim Ash, told the FT, “It’s essentially to further encourage banks to mop up the considerable gold savings of the population (under the mattress – might be uncomfortable), deposit these as part of reserve requirements, and then frees up FX, and potentially I guess lira liquidity when the need arises.”

The move to mobilise deposits did bring some positives (as mentioned above) the currency rose, interest rates fell along with the significant current account deficit, and government bonds were once again made ‘investment grade status.’

The move was seen as such a success that Central Bank governor Erdem Basci was awarded the Banker’s 2012 ‘Central Banker of the Year award’.

However, overall the ‘scheme’ has had varying results, so reports Metals Focus, “Although at its peak in June 2013 some 260 tonnes was held in gold deposit accounts, the bulk of this was made through cash payments, rather than from gold collected from the public…Furthermore,” “gold held in these deposits has since fallen sharply, to now stand at around 70 tonnes.”

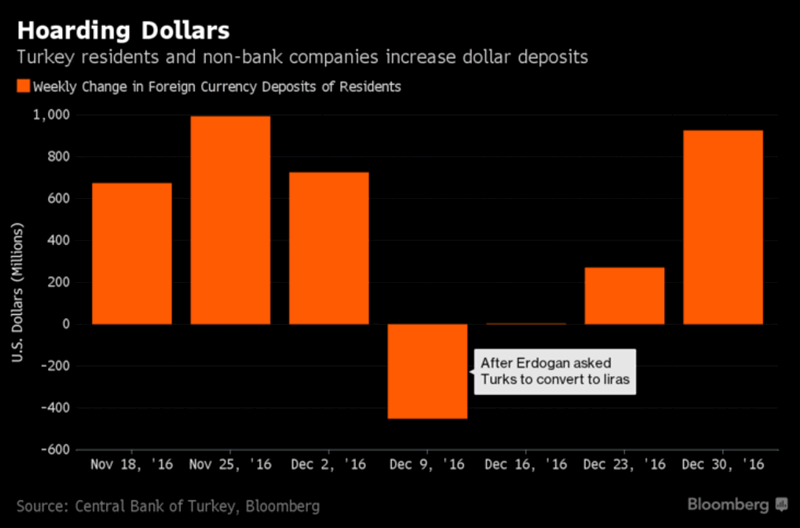

Interestingly, we should note that despite Erdogan’s calls to support the lira and gold (and subsequent increases in gold imports) US dollar deposits by Turkish residents and non-bank companies rose for a third week, last week.

Gold is harder for citizens to move out of the financial system, the view is likely to be that when the time comes citizens will struggle to get deposits out of the system and instead they can be used to support the currency and the banking system.

The move to bring gold into the banking system is likely a move to prevent a situation whereby banks are unable to meet creditors’ demand for repayment – a liquidity crisis. This is something the country has been working to avoid since the 2000/2001 liquidity crisis in Turkey. However, it became something that looked like happening again in 2011.

The increase in gold reserves is also likely to be designed to counteract any leaps in domestic gold demand by providing a liquidity pool, so as to try and reduce the need to import gold and weaken the lira. However, this would leave banks wide open to a run, should depositors demand their gold back, en masse. Not impossible to imagine that their gold might not be so easy to get at in such a situation and a reason that Turkish people should keep some of their gold in secure storage in vaults internationally.

Country’s gold reserves

Arguably the country doesn’t need to go on a huge gold grab from its citizens. Turkey is Europe’s largest gold producer. Every year since 2001 gold production has climbed, from 2t in 2001 to 33.5t in 2013.

According to the World Gold Council, the Turkey’s Ministry of Energy & Natural Resources estimate gold reserves to be 840t, and resources to be as high as 6,500t. The government continues to encourage growth in the gold mining sector with well-considered incentive schemes to get mining companies up and running.

Gold recycling is also well-established in the country and there is strong supply-chain. With this and it’s growing mining sector it isn’t surprising that is one of a handful of countries that has more than one LBMA accredited refinery, an excellent position to be in as the gateway between Europe, Asia and the Middle East.

Whilst mined amounts may seem small compared to the likes of China, it is not be sniffed at given the potential resource and established recycling trade. Considering it’s geographical position and refineries, Turkey’s homegrown gold may well be very valuable to the country and its allies.

Conduit to Iran

It is not only Turkey’s rumoured plans for the gold it is bringing into the banking system and refining, that has grabbed the attention of the gold world but also its relationships and role as a conduit to other countries building up their gold reserves.

In May 2012 the Turkish Statistical Institute reported that gold sales to Iran, from Turkey, had increased by over 30 times in the first quarter of the year, gold exports between the two countries had increased by nine metric tonnes; in 2011 the amount exported was just 286kg.

Prior to 2012 the country had been a gold importer for 28 of the previous 31 years. It became an exporter when Iran began selling the country gas and accepted gold bullion as payment. This was, of course, done in order to circumvent international sanctions.

In 2012, I wrote, “In January it was reported that Turkey were preparing to bypass UN sanctions by trading with Iran for oil in exchange for gold…The Turkish government has assured the US that they will reduce oil imports from the Islamic Republic this year, however total trade increased by 47% in the first quarter of 2012 between the two countries. It is not surprising Iran has become one of Turkey’s biggest trading partners; the country benefited heavily from the Iran-Iraq war in 1980-1988, becoming a trading partner to both parties…

‘…It is this recent surge in trade with Iran which analysts believe accounts for the tripling in demand by Iran for Turkey’s precious metals, mainly gold. The longer the Islamic Republic remains isolated, the greater the trade in Turkish gold, and the longer high prices in the local market are maintained. Reuters report that the fall in the rial’s value against the dollar has caused an increase gold investment for savings purposes.”

This trade apparently continues today, explains Jim Rickards:

“Reliable data is not available for Iran, however, exports from Turkey and Dubai to Iran are significant, and there is good reason to conclude that Iran is also a rising gold power relative to the size of its economy.”

Axis of Gold

And where does all this lead to? The ‘Axis of Gold’, as entitled by Rickards. Once again, it is very important to consider Turkey’s geographical position and allies when it comes to gold demand.

“A major blind spot in U.S. strategic economic doctrine is the increasing use of physical gold by China, Russia, Iran, Turkey and others both to avoid the impact of U.S. sanctions and create an offensive counterweight to U.S. dominance of dollar payment systems…Russia, China, Turkey, and Iran constitute a new “Axis of Gold” prepared to undermine confidence in the U.S. dollar.”

This has been confirmed by Erdogan himself, as reported by Hurriyet, in early December last year. As the Turkish President Erodgan opened a new mall he took the opportunity to say a few words about the country’s foreign exchange ideas ‘“I proposed Putin the following: Let’s do our trade in local currencies. Whatever I buy [from you] I shall pay you in Russian ruble, and whatever you buy from me make the payment in Turkish Liras,” said Erdogan on December 3…

The move to accumulate gold in Russia is no secret, and as Putin advisor, Sergey Glazyev told Russian Insider, in April 2016, ‘The ruble is the most gold-backed currency in the world’.

The Hurriyet report continues:

He added that he had made the same offer to China and Iran and his offer was found reasonable. “We have given the necessary instructions to our central banks and we will try to conduct such [trade] relationships between us through this way,” Erdogan said.

Erdogan again reiterated his call to Turkish citizens to convert their foreign exchange into gold or the Turkish Lira. “Those who keep foreign currency under their mattress should come and turn them into lira or gold,” he said.’

Conclusion: Gold as an insurance policy

Turkey may well have major issues in many areas of its economy, but it is positioning itself for the changing of the monetary guard that we are slowly witnessing around the world, and it is using gold as its insurance and safe haven in the ongoing and soon to escalate currency wars.

Russia and China are poised for a weakening of the dollar and of the influence of the last superpower and indeed the potential political and financial contagion in the EU.

Turkey feels aggreived and sees itself as a victim of “economic sabotage” and of dollar “hegemony” and largely ignored by the EU when it comes to the refugee crisis and growing threat of terrorism.

All three countries have shown a strong affinity through gold across all levels – government, banking system and citizens.

Whether you think of the Turkey in Europe or not, there is no country on the continent that is able to play all three roles of producer, conduit and accumulator of gold in the same way that Turkey can.

The US dollar system currently rules the international payments sphere, but moves to step away from it are already in play by those in the ‘Axis of gold’. As Jim Rickards has pointed out

“…adversaries do not issue currencies that are potential alternatives to the dollar because of inadequate rule-of-law, immature bond markets, primitive capital markets infrastructure, or all three. The only feasible alternatives to dollar dominance are special drawing rights (SDRs) issued by the IMF, and gold.”

In an increasingly multi polar world where the heavily indebted, near bankrupt U.S. economy and by extension the U.S. dollar look very vulnerable, gold is the ideal currency for those seeking to protect themselves from the coming decline of the dollar.

This applies for all – for apolitical investors, for U.S. allies and especially as we have seen for the U.S.’ competitors and adversaries who are looking to operate beyond the realms of the US-dollar denominated SWIFT payments and dollar based monetary system.

Gold is highly liquid, cannot fall victim to cyber warfare and is very difficult to steal or confiscate if owned in the safest ways – allocated and segregated gold coins and bars in the safest jurisdictions in the world. It has throughout history and in recent months shown its safe haven attributes and value as a hedge against dollar and other fiat currencies weakness and devaluation.

Credit Card Limits Increased To 50,000 (£ $ €)

Due to ongoing requests for higher credit and debit card transactions, we have increased our maximum card transaction sizes from 5,000 to 50,000 GBP, EUR or USD.

KNOWLEDGE IS POWER

10 Important Points To Consider Before You Buy Gold

Please share our research with family, friends and colleagues who you think would benefit from being informed by it.

Gold Prices (LBMA AM)

18 Jan: USD 1,212.50, GBP 984.91 & EUR 1,134.78 per ounce

17 Jan: USD 1,217.50, GBP 1,003.59 & EUR 1,141.65 per ounce

16 Jan: USD 1,202.75, GBP 997.56 & EUR 1,135.40 per ounce

13 Jan: USD 1,196.35, GBP 978.85 & EUR 1,123.25 per ounce

12 Jan: USD 1,206.65, GBP 984.39 & EUR 1,135.82 per ounce

11 Jan: USD 1,187.55, GBP 979.25 & EUR 1,128.41 per ounce

10 Jan: USD 1,183.20, GBP 974.60 & EUR 1,118.12 per ounce

09 Jan: USD 1,176.10, GBP 968.75 & EUR 1,118.59 per ounce

Silver Prices (LBMA)

18 Jan: USD 17.12, GBP 13.93 & EUR 16.01 per ounce

17 Jan: USD 17.00, GBP 13.91 & EUR 15.87 per ounce

16 Jan: USD 16.82, GBP 13.94 & EUR 15.87 per ounce

13 Jan: USD 16.76, GBP 13.76 & EUR 15.74 per ounce

12 Jan: USD 16.91, GBP 13.77 & EUR 15.87 per ounce

11 Jan: USD 16.79, GBP 13.84 & EUR 15.96 per ounce

10 Jan: USD 16.66, GBP 13.73 & EUR 15.76 per ounce

09 Jan: USD 16.52, GBP 13.57 & EUR 15.69 per ounce

Mark O'Byrne

This update can be found on the GoldCore blog here.

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.