Where Did All the Money Go?

Stock-Markets / Market Manipulation Sep 23, 2016 - 05:14 PM GMTBy: David_Galland

Dear Earthlings,

Dear Earthlings,

As we’re still readjusting to life in a small Argentine pueblo miles from anywhere, I’ve asked Stephen McBride, my associate and now neighbor (he just moved here), to take the reins for the bulk of this week’s assemblage of news, analysis, and wry commentary about the never-boring antics of the human ape.

You may recall Stephen’s wonderful exposé on George Soros, an article that continues to bounce around the Internet doing good service by alerting people to Soros’s nefarious deeds.

In this week’s article, Stephen takes a closer look at where all the many billions of dollars in government fines end up

This topic of government tangling up the economy is a key theme in the next edition of Compelling Investments Quantified. I know because I’m writing it and uncovering important facts about the explosion of regulation under the Obama administration, and the cost to the economy.

Like most people, you’ve probably been wondering why the US economy can’t seem to get out of first gear. Based on the research we’ve done, you need look for no other culprit than regulation strangulation.

With a bit of investment jiu-jitsu, we make the burdensome regulation our friend by uncovering a great company, which, due to an overreaction by investors to a potential government fine, is selling for well below its intrinsic value.

Only because we’ve all been a busy and haven’t gotten around to changing the offer, you can still sign up for Compelling Investments Quantified (CIQ) as a Charter Subscriber at a great price and with an unbeatable six-month money-back guarantee. Here’s the link.

As a related aside, one dear reader said I wasn’t being clear enough about the nature of CIQ. That may be true. I used to be pretty good at marketing, but don’t really spend much time on it anymore.

CIQ’s value to you is really quite simple. Jake Weber, Olivier Garret, and I—with help from other members of the team—scour the planet Earth for well-managed companies trading below their intrinsic value. As part of kicking the tires to ensure they are rock-solid financially, we deploy a quant model a company has to pass with flying colors in order to be recommended.

As a subscriber, you need only sit back, relax, enjoy a pleasant and informative read about the key economic and investment themes we are following, then peruse the details on our recommended company. If you like the recommendations, consider adding them to your portfolio at our recommended price.

Take six months to judge for yourself whether CIQ offers useful insights and great stock picks. If you decide it doesn’t, simply cancel your subscription for a full refund. If that sounds like a fair deal, then sign up ahead of the release of the next edition, Thursday, September 29, and we’ll also send you two very useful research reports, titled Crash Ahead? and Profiting in a Low Interest Rate World. Here are all the details.

And with that shameless but sincere plug, and turning up the volume on a small collection of the work of Massive Attack I put together, the parade begins with Stephen’s article, followed by some observations I made after witnessing a very unpleasant incident at the airport.

(Quick note: Note that we have added a commenting feature to the bottom of this week's edition. If you have something you'd like to say about today's editorial, we'd love to hear from you.)

David

Where Did All the Money Go?

By Stephen McBride

Now four weeks into my Argentine outback experience, I am beginning to realize that much of what we call “news” in the West is simply noise.

Take this headline for example, posted on most major news networks earlier in the week: “Donald Trump Jr. Compared Syrian Refugees to Poisoned Skittles.” This being the peak season of the most bizarre presidential race in my lifetime, I’ve become accustomed to reading such headlines.

Down here in Cafayate, things are different. Although the prior Argentine government had a well-deserved reputation as being criminally insane, nobody paid much attention to them. Monetary and foreign policy are not the topic of conversation over lunch, and nobody cares if a politician makes a politically incorrect comment.

Indeed, it is refreshing to be able to order a café negro alto in a restaurant without receiving funny looks and being asked to leave.

All of this got me thinking about another headline that has been plastered all over the media recently, “US DoJ hits Deutsche Bank with record $14bn fine.”

For their role in the mortgage-backed securities (MBS) fiasco, Deutsche Bank has been fined $14 billion by the Department of Justice. This is just the latest in fines dished out to banks by the various US acronym-authoritarians since 2010, with the total tally now more than $110 billion.

On the face of it, it seems fair that the banks get hit with fines related to the sale of junk mortgage-backed securities. Estimated losses on MBS alone to investors are between $750 billion and $1 trillion. The crisis also led to the housing collapse in which 7 million people lost their homes, the worst sort of personal and financial pain.

As the lawsuits filed by the DoJ, Fed, CFTC, and SEC were for defrauding customers, one would expect those directly impacted by the fraud to be recipients of the proceeds.

Well, it seems in the giant entanglement of bureaucracy that is the United States, that’s not the case.

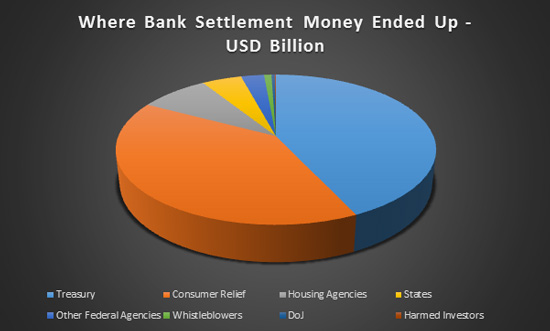

Show Me the Money

The below chart shows how the $110 billion in federal fines dished out since 2010 has been distributed.

You’ll have to squint to see the thin brown line representing restitution to harmed investors paid out from the $110 billion in fines.

Not so with the $49 billion that found its way into the Treasury. From there, the money was placed into the government’s general fund, where it can be spent on any budgeted item. The Treasury has said the settlement money isn’t specifically tracked and is “spent as Congress authorizes.”

Okay, not much help for the victims there. What about the $5.3 billion given to the states?

New York has used the money to build a new horse barn and stables at its state fair. Delaware is using the proceeds to subsidize local law enforcement email servers. In New Jersey, a mortgage firm collected a reward of $8.5 million for reporting bank misconduct. California gave its $700 million share of the settlement to its two largest pension funds. Illinois did the same.

What about the $45 billion earmarked for consumer relief?

On the face of it, many of the largest offenders seem to be on track with their consumer relief payments. Bank of America has dished out $6.3 billion, with JPMorgan tallying up $3.8 billion and Citibank $900 million.

But when I dug a little deeper into the settlement reports from these institutions, I found not all of the “consumer relief” funds are being directed to the victims of the mortgage crisis.

So far, Bank of America has dealt out around $4 billion in debt forgiveness and write-downs; JPMorgan has given $2 billion and Citibank $300 million. So who received the rest of the funds?

Liberal Assistance

A substantial portion of the funds has been allocated to federally approved, private organizations.

These federally approved organizations include La Raza—a Hispanic civil rights group that advocates for the advancement of Latino families. The National Urban League, whose goal is to enable African-Americans to achieve economic self-reliance, parity, power, and civil rights, is also a recipient. As is the National Community Reinvestment Coalition, Washington’s most aggressive lobbyist for the Community Reinvestment Act.

What do these organizations have in common? They’re all allies of the Obama administration, engaged in voter registration, community organizing, and lobbying in Washington for liberal policies.

The structure of the financial settlements gives the banks an added incentive to pour funds into these groups, instead of making restitution to individuals harmed by the bank frauds. Specifically, for every dollar donated to these groups, the banks receive double “consumer relief credit.” Bank of America, the only bank to fully disclose its donations, was able to rack up $194 million in “consumer relief credit” with just $84 million in donations to the above groups.

An August 2016 analysis of Bank of America’s donations by the Wall Street Journal found that of the 80 community groups that received money, each on average received over 10% of their 2015 budget from the bank.

So, of the estimated $750 billion to $1 trillion in losses, harmed investors have received a paltry $115 million. Borrowers who were sold mortgages they couldn’t afford or wrongly foreclosed on, have only received around $6 billion. These figures add up to a lot less than the $45 billion earmarked for consumer relief.

Penalty Profits

The highly publicized $110 billion figure is a huge sum of money to you or me, but how much did it impact the banks?

From 2004 to 2007, the year the housing market peaked, the four largest US banks made over $480 billion in net profits. A large portion of these profits originated from the selling of MBS.

Despite losses in 2008 and 2009, banks are back to posting record profits. In Q2 2016, the four largest US banks made $43.6 billion in profits, a 1.4% rise for the same quarter in 2015. Hey, what was that mortgage crisis thing anyway?

And the icing on the cake for the banks? The majority of the fines are tax-deductible.

Of the $5.06 billion fine paid by Goldman Sachs earlier this year, over half was tax-deductible. Of the $16.65 billion fine issued to Bank of America, $12 billion was tax-deductible.

Not too bad of a deal, after all.

Rancid Ratings

Although the banks packaged and sold the junk mortgage-backed securities, it was the rating agencies who inflated the ratings, allowing them to be sold as AAA. The only rating agency to be fined so far is Standard & Poor’s, which had to pay $1.5 billion in 2015.

But again, no proceeds will go to the actual victims hurt by the inflated ratings. The proceeds are to be split between the Department of Justice and the states.

During the lawsuit, S&P admitted it gave subprime mortgages AAA ratings to win business. This clip from The Big Short shows the shenanigans that were going on at the rating agencies pre-crisis.

In court, the DoJ cited an instant-message exchange between two S&P executives in 2006 which read, “It could be structured by cows and we would rate it,” as proof of the firm inflating ratings.

So, a blatant act of fraud, yet the ratings agencies and the executives in charge of the fraud have effectively been given a get-out-of-jail-free card.

Who Profits?

Today, six years after the first fine was issued to US banks over the mortgage crisis, only a fraction of the headline $110 billion has made its way to the victims. With $49 billion being directed to the US Treasury, and the majority of fines being tax-deductible for banks, one has to ask, cui bono? Who profits?

The answer is obvious: the government and those with friends in high places.

If you were one of the individuals who suffered financial losses due to the MBS fraud, your odds of receiving restitution are slim, but not completely impossible. The link here will take you to the website of an organization established to try and get settlements for harmed individuals, distressed borrowers, or borrowers who were wrongly foreclosed on.

The Angry Wife

David again, popping back in to briefly share something I observed while in a security line at the airport.

As best as I could determine, a husband in the same line seemed to have forgotten some item related to their trip. The wife, heavy-set with only the faintest traces of youth still gracing her face, made her displeasure known by unleashing a tirade.

Clearly unconcerned that she was in close quarters with strangers, she began growling, flapping arms, cursing, and otherwise berating her unhappy spouse for his many faults. Based on her harsh narrative, the forgetting of something she deemed important was just the latest example of his shortcomings as a husband and a man.

“You ALWAYS screw things up!”

To ensure the nuances of her message were perfectly understood, she paused periodically and leaned in close, glaring intensely into the husband’s blinking eyes, her countenance the very portrait of hate. She then punctuated the true depths of her feelings with a somewhat threatening wave of her hand in his face.

The object of her scorn, the prototypical tubbish, early-forties desk jockey, unfashionable black glasses hanging off his nose and his otherwise bald pate topped off with a monk’s ring, weathered the abuse meekly, his every feeble attempt to defend himself snappishly put down by hell-wife.

It is not my intention to take sides in the one-sided battle, because as far as I know the tubby hubby was entirely at fault. Perhaps, in addition to being forgetful, he was consistently inattentive, slovenly, humorless, and lacking in sex drive. To wit, lacking in the traits required for his wife to want to take care of her sorely neglected looks, or to playfully tug at his ear for being absent-minded instead of humiliating him publicly.

Alternatively, the fault could have rested largely with her. She might have been just as she appeared—a self-hating, husband-hating, life-hating harpy with social graces somewhere between junkyard mean and scouring the earth with hell’s own fury.

No, rather than taking sides, the point of this idle musing is to wonder aloud how it is that either, or both, of the partners in this unhappy coupling could put off their inevitable divorce for even a day.

Had it been me, at the first flap of her flabby mitt in my face, she would have been flying alone.

But the reality is, I would never have let it get to that point. That’s because my modus operandi has always been to never let bothersome issues in my life go unaddressed—and a spouse who hated me, for good reason or not, would definitely fall into that category.

It’s not healthy to live a life full of conflict and stress, and I certainly hope none of you dear readers would ever fall into such a rut or allow yourself to remain in such a rut for even a minute.

There’s a reason we moved to a small town in the Argentine outback: it’s about as laid back a place as can be found on planet Earth. Not unlike having to witness the angry wife, when we’re back in the US, these days it seems everywhere you turn there is unpleasant social friction, political tension, and the constant potential for armed conflict.

The latest inanity, of white businesses being targeted in Charlotte, NC because a black police officer shot an armed black man in mid-charge, serves to underscore the point.

Just thinking about life back in the “first world” raises my blood pressure, just as having to listen to the harpy’s tirade up close and personal did.

And, so, with that, I’m off to the Athletic Club, followed by lunch on the plaza and, after a brief siesta, maybe a nice horseback ride. Why not? We only live once, so we might as well enjoy it to the fullest.

Here Come the Clowns

Revealed by Reddit

By now, everyone is well aware of the Clinton email scandal. And that she sent classified information on an unsecured private email server, then had the server wiped and when asked by the FBI to hand over all the emails sent, failed to do so.

Well, it turns out that the individual who “mistakenly” wiped Mrs. Clinton’s email server clean used the popular information sharing site, Reddit, to seek tech advice on how to “strip out a VIP’s (VERY VIP) email address from a bunch of archived emails.” We’d call it a smoking gun; the media will, of course, largely ignore it.

Oh, the Hypocrisy!

The Washington Post, one of four organizations that received and published leaked NSA documents from Edward Snowden, is now calling for his prosecution. This makes the Post the first paper to call for prosecution of its own source. Is it any wonder the mainstream media is dying?

And with that, we’ll sign off for the week by thanking you once again for reading and for sharing The Passing Parade with your friends.

Until next week, thanks for reading!

David Galland

Managing Editor, The Passing Parade

Garret/Galland Research provides private investors and financial service professionals with original research on compelling investments uncovered by our team. Sign up for one or both of our free weekly e-letters. The Passing Parade offers fast-paced, entertaining, and always interesting observations on the global economy, markets, and more. Sign up now… it’s free!

© 2016 David Galland - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.