What Could Reverse The Global Stock and Commodity Markets Decline?

Stock-Markets / Stock Markets 2015 Sep 30, 2015 - 12:19 PM GMTBy: Clif_Droke

Falling stock and commodity prices around the world are underscoring a change of fortunes for the global economy. As the shockwaves from Europe, China and the developing markets spreads, there is a growing sense among investors that the U.S. might be the next casualty of the global slowdown.

Falling stock and commodity prices around the world are underscoring a change of fortunes for the global economy. As the shockwaves from Europe, China and the developing markets spreads, there is a growing sense among investors that the U.S. might be the next casualty of the global slowdown.

Economists have already begun questioning what, if anything, the Federal Reserve might be able to do to stem the financial market selling pressure. Weakness has been broad-based and is visible in stocks, commodities as well as high-yield corporate bonds. Since the first bear market of the new millennium, the Fed has played an outsized role as a stimulator of equity markets and the economy.

Congress has long since surrendered its sovereignty to the Fed in the way of introducing stimulus measures (e.g. lower taxes and lifting regulatory burdens), and has simply looked to the central bank in times of trouble. That dynamic will likely change in the years ahead as it becomes increasingly apparent that the Fed's stimulus game since 2002 has likely played itself out.

With interest rates near zero and quantitative easing (QE) on the shelf, economists wonder what the Fed could possibly due to reverse a major bear market if it develops. The latest crisis which threatens the U.S. financial system originated from abroad with problems China and the emerging markets. Economists are debating what impact a global economic slowdown might have on the mighty U.S. economy and whether or not the U.S. could shrug off global weakness.

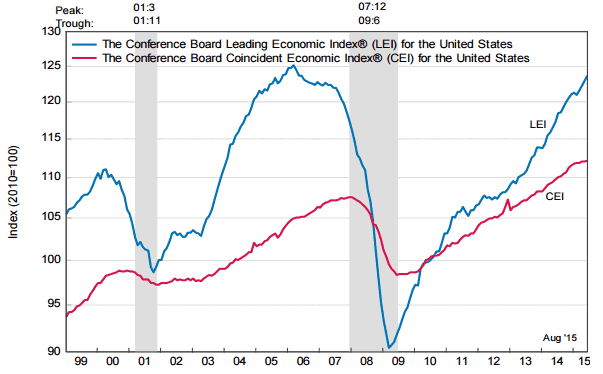

The most reliable leading indicators of domestic economic strength, including the Conference Board's Leading Economic Index (LEI), show no sign of weakness in the U.S. economy yet. In view of how much momentum as the economy currently has, it will likely take several months before current financial market and global economic problems show up in U.S. economic statistics. It wouldn't be surprising to see consumer spending levels remain elevated in the coming months even if the global economy continues deteriorating.

It seems to be a mantra among classical economists that "recessions cause bear markets." Anyone who has spent a number of years in the world of finance knows the falsity of this statement. There have been numerous instances of bear markets preceding recessions, including the 2000-2002 bear market. So if the current equity market weakness develops into a longer-term bear market it wouldn't be the first time equities turned sharply lower while the economy was still strong.

The question economists should be asking is, "What happens to the economy if a bear market in stocks and commodities persists for several months?" Is the U.S. economy strong enough to withstand a major bear market? I don't think there's any question that a major bear market would eventually have a residual impact on economic performance. As heavily reliant as today's economy is on the financial market, any prolonged downturn of stock prices is bound to have a negative spillover effect at some point. The additional negative impact of a weakening global economy would make it even more difficult for the U.S. economy to remain the lone bastion of strength in a troubled world.

All of this leads to the ultimate question as to what it will take to reverse the broad market decline and revive the bull? Since it started with the global market decline, I submit that the answer will have to come from aboard. As previously mentioned, the U.S. central bank appears to have played its hand. Fed members, moreover, seem resolutely clueless as to how to approach the developing crisis. One week the leading Fed members suggest an interest rate increase is inevitable by year's end, while the next week they reverse their position. This indecisiveness and lack of leadership is causing investors to lose confidence, and that's not helping the stock market.

As an aside, I would point out that every incoming Fed president of the last 40 years has had to deal with a crisis of varying magnitude within the first couple of years of their tenure. Volcker had the inflation crisis, Greenspan had the 1987 stock market crash, Bernanke had the credit crisis, and Yellen will most likely have the global market/economic crisis to deal with. How the crisis was addressed determined the efficacy of the Fed president's subsequent tenure. While it's too early to tell, it's beginning to look like Yellen may not be up to the task of handling the crisis with the firm resolution it requires.

A reversal of the global market decline would likely require a decisive and coordinated response among the world's major central banks to truly do "whatever it takes" to revive global growth. Unlike the famous platitude of ECB president Draghi, the leading central banks will have to aggressively loosen monetary policy without ceasing. They must avoid Japan's recent mistake of stimulating monetary policy, which proved effective, then undermining that policy by raising taxes.

The mistakes of Europe in recent years in the way of pursuing austerity policies will also have to be steadfastly avoided. Brazil has seemingly gone down this road after its socialist government proposed a package of drastic austerity measures. Brazil is in deep recession due to the global collapse in commodities prices and is desperately trying to revive its economy. Unfortunately, the country's leadership is repeating a critical blunder made by many European nations in recent years. It's unlikely the outcome will be any different.

The alternative to a coordinately global monetary and fiscal policy response would be a laissez faire approach. Simply letting events take their course and allowing prices to seek their natural levels, while resisting the temptation to raise taxes or impose austerity, would probably be best for the long-term health of the economy. It would probably take several years before the economy's imbalances were completely rectified, however, and it's unlikely that policymakers have the foresight or patience to follow this approach. It would also be an admission that the policies of the past decade were ineffective, and failure isn't something bureaucrats and politicians like to admit.

In the final analysis, the most likely policy response will involve a heavy commitment of liquidity and lower interest rates among the world's major central bankers. The sooner a coordinated loose money policy is initiated, the less damage the global economy will suffer in the near term. And while it's true that a global QE would be tantamount to kicking the proverbial debt can down the road, can kicking as an economic policy has served the U.S. well for many decades. It's not the most preferred policy, but it has proven effective as long as there's enough road to kick it down.

Mastering Moving Averages

The moving average is one of the most versatile of all trading tools and should be a part of every investor's arsenal. Far more than a simple trend line, it's also a dynamic momentum indicator as well as a means of identifying support and resistance across variable time frames. It can also be used in place of an overbought/oversold oscillator when used in relationship to the price of the stock or ETF you're trading in.

In my latest book, Mastering Moving Averages, I remove the mystique behind stock and ETF trading and reveal a simple and reliable system that allows retail traders to profit from both up and down moves in the market. The trading techniques discussed in the book have been carefully calibrated to match today's fast-moving and sometimes volatile market environment. If you're interested in moving average trading techniques, you'll want to read this book.

Order today and receive an autographed copy along with a copy of the book, The Best Strategies for Momentum Traders. Your order also includes a FREE 1-month trial subscription to the Momentum Strategies Report newsletter: http://www.clifdroke.com/books/masteringma.html

By Clif Droke

www.clifdroke.com

Clif Droke is the editor of the daily Gold & Silver Stock Report. Published daily since 2002, the report provides forecasts and analysis of the leading gold, silver, uranium and energy stocks from a short-term technical standpoint. He is also the author of numerous books, including 'How to Read Chart Patterns for Greater Profits.' For more information visit www.clifdroke.com

Clif Droke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.