Long-term Forecast for Commodity Prices and Mining Industry Funding

Commodities / Metals & Mining Oct 06, 2014 - 12:42 PM GMT

Rising global scarcity of resources – metals, minerals and energy – that an ever-increasing human population uses every day to sustain its unsustainable lifestyle, has been the most important topic since the burst of the dotcom bubble in 2000. The reason is simple: we live on a planet with a distinctly finite resource base and a rapidly growing population.

Rising global scarcity of resources – metals, minerals and energy – that an ever-increasing human population uses every day to sustain its unsustainable lifestyle, has been the most important topic since the burst of the dotcom bubble in 2000. The reason is simple: we live on a planet with a distinctly finite resource base and a rapidly growing population.

For over the last twelve years supply has struggled to keep pace with demand. Yet we experience a collective breakdown among junior miners of epic historical proportions. Confused investors have been questioning their portfolio strategies and have withdrawn their money from “value in the ground” to re-invest it into scarily overvalued internet companies with questionable earnings and even more precarious business models built on promises of more bites and bytes. Today’s situation displays eerie similarities to the business and economic developments leading up to year 2000 and the events we remember all too well. I am considering a new article with the title “50 shades of investor insanity”.

The vast majority of small and midsize miners have been facing a global cash crunch since 2008. As commodity prices corrected, the share prices of resource companies fell into an abyss without any fundamental justification, as it seems. Investors and banks became reluctant and very selective about where they put their money. Add to this a severe confidence crisis of investors into the business models of the TSX Venture Exchange and the companies listed on it, and the resulting toxic mix explains the total breakdown and annihilation of the traditional funding process in mining as we have known it for years. We have been witnessing the slow death of the traditional funding process of small and medium sized resource companies.

By all historical means and standards investors should be in the commodity sector with a healthy percentage of their portfolio, but aren’t.

With the complete drying out of funding for resource companies, exploration and the development of many crucial projects has come to a halt. Small and medium-sized miners are the key part of the mining-industry food chain. And they are unable to deliver due to lack of funding. The project pipeline for the mining industry is in fact as good as empty, and as new projects take years to develop, we should expect strongly rising commodity prices in the not so distant future just from that fact alone. I have been working since May trying to determine the various key parameters that determine the commodity prices and with it the available funding for mining companies. It is a work on a mathematical model in progress, which by no means makes claim to completeness or accuracy to decimal points. However, I do believe that the forecast for the direction of the markets at this stage is quite reliable. I may be able to present a better-refined model in a couple of weeks.

What are the input parameters? There are hard and soft economic factors. Some of these are pretty common sense, others are more difficult to grasp.

- Interest rates as they influence the production cycle of mines.

- Central bank action and stock market development, Investor Confidence.

- Demand for metals.

- Demand for energy.

- Increasing population and the development of the middle class as driving demand factor.

- Supply.

- Production costs.

One of the biggest challenges has been to bring these factors into a proper mathematical relation to each other. These factors were equally weighted, differentiated, standardized on past GDP figures of OECD countries and then compared to the CRB Index, to a cumulative demand and to a cumulative supply. Interested math wizzes may email me in order to get the underlying mathematical formula. It is in the nature of the data supplied to us that these are estimates, thus I would expect a 20% variation margin at this stage of the model, while we work on refining it.

Obviously critics could argue that the one or other factor should be weighted more over another. Admittedly that may be open for discussion, and we are working on it in an improved mathematical model. However I don’t think that it would change the fundamental outcome of this analysis.

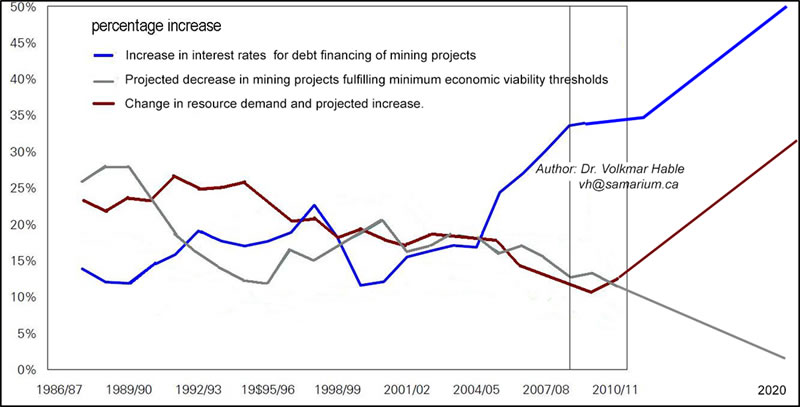

Interest rates as they influence the production cycle of mines.

Debt financing is a key part of the mine development process. Higher interest rates require a higher post-tax IRR for mining projects. As interest rates rise fewer mining projects will fulfill the minimum threshold for economic viability.

The result:

- Limited supply

- Rising demand

- Rising commodity prices

- Higher profitability for surviving projects

- Higher share prices for mining companies

- Graph by Dr. Volkmar Hable, vh@samarium.ca

Remark: The numbers regarding the decrease in projects refer only to currently known projects per the International Mining Handbook. Projects not reported or not discovered obviously cannot be included.

Central bank action and stock market development, Investor Confidence.

In order to understand the correlation between the availability of funding for the mining industry we have to look also at the general state of the broader stock markets, as their well-being influences the TSX-V.

Numerous articles have been published in the last few years expressing their expectation that at least some of the liquidity would make its way into the mining sector. For most juniors and the TSX Venture Exchange these hopes did not transpire. The TSX Venture Exchange is the world’s largest market place for junior resource companies. Its wellbeing in the past has been directly related to the development of the broader stock market, which makes financial sense: investors typically need to make profits in the main markets before they would risk any of their hard earned dollars in the higher risk TSX-V market.

Above is a graph of the S&P 500 Index of the last 6 years: we are in a stock market that has been in a steep significant uptrend since the low in early 2009. In almost 6 years of un-interrupted stock market rally there hasn’t been one single significant correction. The S&P 500 Index bottomed in March 2009 at about 670 and at the writing of this article is above 2,000. The S&P 500 Index, thanks to the courtesy of QE, ZIRP, Central Bank purchases, and who knows what other contrivances, has been levitated to the euphoria level of 2,000.

The Federal Reserve’s third quantitative easing campaign (QE3) will end in October 2014. QE3 was significantly different from the first two easing campaigns QE1 and QE2, which were finite from their births on. QE3 was the Federal Reserve’s first open-ended debt-monetization campaign, with no limits and no rules. This unlimited scope of QE3 not only helped create a stock market rally of unprecedented historical dimensions (not on the TSX-V), but surely will also be known in history books as the largest experiment in human history. QE3 is not a market strategy, and even less some sort of medical prescription that a physician would give out to his patient after careful revision and clear diagnosis. It rather is a second-guessed trial therapy applied by the Federal Reserve’s decision makers to humans in the absence of any other useful ideas. No one knows the final outcome of QE3, no one has known from the start of QE3 its possible effects, no one even had a clear diagnosis of the economic problems in 2008, apart from general phrases like “irrational exuberance”. Well, we know one thing now, it boosted the stock markets big time. With QE3 Mr. Ponzi truly had found worthy successors to his notorious business scheme.

Since QE3 had not been given a defined end, stock market traders have accommodated themselves to the assumption that QE3 would be around to backstop stock markets indefinitely.

Hence every single stock market decline was quickly bought (except on the TSX-V), leading to the general stock markets soaring to new heights in a historically unprecedented stock market rally (again: NOT on the TSX-V whose investors were subjected to losses). The S&P 500 Index increased by 29.6% in 2013, the only full year of QE3. And the S&P 500 Index is up 39.5% since the start of QE3. And the stock markets had already enjoyed an 11 month uninterrupted straight rally before the Federal Reserve hit the markets with its QE3 Ponzi scheme in November 2012. As of the date of this article, the SPX had increased by 118.3% in just the last 42 months alone. There is no doubt that QE3, and not the underlying economic growth, was the solely responsible factor for the historical stock market rally. Now, as stock valuations have been for a long time at the top end of their valuation range, and that the QE3 party will soon be over, most analysts of sound mind and reason agree that a stock market correction is not only highly overdue but will also be very significant in terms of time and percentages. There is no such thing like a financial perpetuum mobile, creating something out of nothing. A 5+ year virtually un-interrupted stock market rally necessarily must have a correction at some point. When is anyone’s guess, but it would be prudent to assume that the end of QE3 might be the terminal trigger.

And this leads us to the world’s commodity markets and, in particular, the TSX-V. Investors rightfully wonder what will happen to the TSX-V in a broader stock market correction, which is close to the 2008 low already NOW BEFORE a broader stock market correction had even started. Will we see the TSX-V index below 400?

I believe resource investors have started a process of divorce and disengagement from the TSX-V in 2008 for reasons that I described in an earlier article that is available on mining.com and marketoracle.co.uk. While a rising tide (higher commodity prices) will lift all vessels, investors may indeed find out that some of these vessels have a broken hull and won’t come up again – clearly a significant concern with the TSX-V.

The TSX-V in the last 10 years has yielded nothing to investors:

If we were to take out from the TSX-V Index the few cash-flow generating companies and/or those with some real value (about 50 companies on the entire TSX-V), the TSX-V decline would show up as an almost total annihilation of market capitalization. What does this tell us about the TSX-V? Correct, it is a dysfunctional market.

Are we really to believe that in a broader stock market downturn investors will cry “I am Spartacus”, turn around, sell their blue chip holdings, and roll their hard earned dollars into the TSX-V ? The obvious answer is a no-no. The fact of the matter is that TSX-V investors have been thoroughly brainwashed and finally woke up to the onslaught of hype, hybris and the notoriety of misinformation, fraud and embezzlement. TSX-V investors have had it. In the absence of trust and occasional law enforcement they did what they had to do and pulled their money out of the TSX-V. The inexorable truth as far as the TSX-V is concerned remains that we are not dealing with a simple bear market but with the proper end of the TSX-V in its current constitution, as no one of the decision and law makers seems to be willing to do what has to be done.

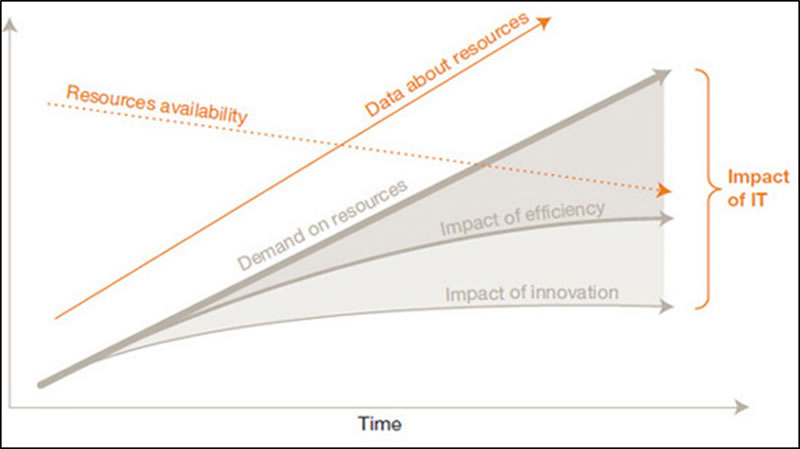

Demand for metals and non-energy resources from 2000 until 2020

A rising middle class and an ever-increasing world population will demand goods. Resources are needed to produce those goods, and energy is needed to transport those goods. We can expect a rising demand for resources, while at the same time the efficiency increase in resource production due to new technologies will lessen. This graph is the most inaccurate of all in this article as it is hard to measure, it is a guess on a best effort basis due to the lack of reliable measurable data. It relies on the fact that between the 60ies and the early 90ies new technologies allowed mines to be run more efficiently. However this efficiency increase effect is tapering off and shall be zero within the next 10 years or so.

Graph by Dr. Volkmar Hable, vh@samarium.ca

Below is a graph for the metal demand, which paints a bullish picture due to a increasing world GDP that in turn results from a higher population and a significantly growing middle class. The uptrend is unbroken.

Graph by Dr. Volkmar Hable, vh@samarium.ca

Demand for Energy Resources

The demand for energy resources shows a significant bullish picture for commodity prices as well. The underlying fundamental expansion needs no further explanation, as it is the subject of numerous news and articles.

Graph by Bloomberg with data from OECD, www.samariumgroup.com

Increasing population and the development of the middle class as driving demand factor.

The chart below illustrates how world population has changed in history.

At the dawn of agriculture, about 8000 B.C., the population of the world was approximately 5 million. Over the 8,000-year period up to 1 A.D. it grew to 200 million (some estimate 300 million or even 600, suggesting how imprecise population estimates of early historical periods can be), with a growth rate of under 0.05% per year.

A tremendous change occurred with the industrial revolution: whereas it had taken all of human history until around 1800 for world population to reach one billion, the second billion was achieved in only 130 years (1930), the third billion in less than 30 years (1959), the fourth billion in 15 years (1974), and the fifth billion in only 13 years (1987). During the 20th century alone, the population in the world has grown from 1.65 billion to 6 billion. In 1970, there were roughly half as many people in the world as there are now. Because of declining growth rates, it will now take over 200 years to double again.

The simple conclusion: more people will need more resources and more energy.

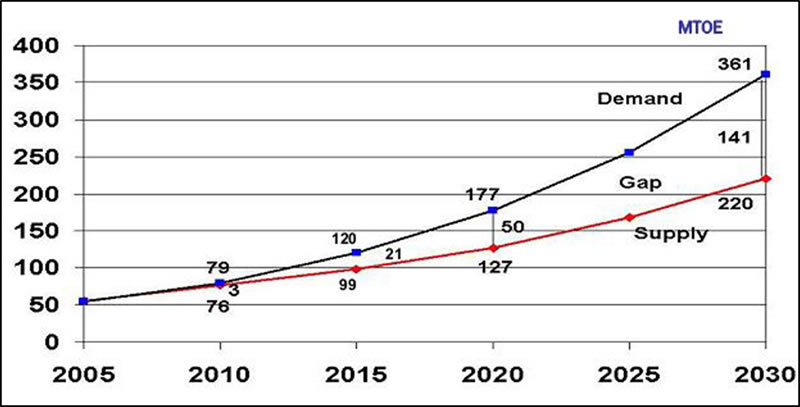

Supply

The gap between energy demand and supply until 2030

Graph by Dr. Volkmar Hable, vh@samarium.ca

Energy resources show a significant gap between demand and available supply developing from here to 2030.

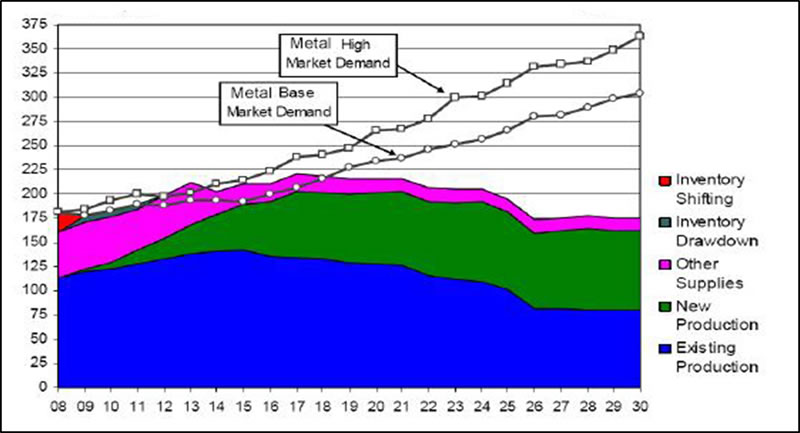

Supply of metallic resources from 2008 to 2030

Graph by Dr. Volkmar Hable, vh@samarium.ca

Metallic resources as well show animportant supply shortfall until 2030.

Industries as end users should be starting now to address this issue considering the long development cycles of resource projects.

The Rise of Production costs as Total Cash Costs in relation to other price factors

Graph by Dr. Volkmar Hable, vh@samarium.ca

The total cash costs, formerly known simply as production costs, have been on the rise as well. However they are not expected to be a significant contributor to price forming in a demand driven environment. On the other side costs are not expected to fall. Thus an ever-increasing cost base will call for higher-grade deposits, a trend that may very well be offset by significantly higher resource prices. An increase in resource prices will lead to previously unproductive deposits to be suddenly above breakeven.

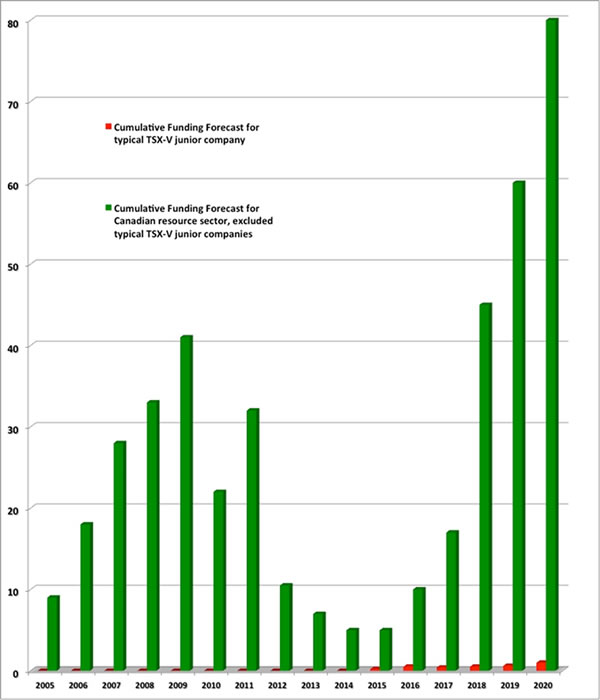

Funding Forecast for the Canadian Resource Industry in Billions USD

The chart below is not caused alone by an empty project pipeline but is the result of the mathematical combination of several macroeconomic and financial market factors. I expect the general funding crisis to bottom sometimes during next year, and possibly 2016, followed by a strong bull market in commodities.

On the other side I do not expect a recovery of the traditional business model of the typical TSX-V junior company, as long as structural issues are not addressed. We can safely expect a large number of TSX-V listed companies to not survive the near future, and is hard to see that anything else other than a new form of investor insanity will drive up the TSX-V.

Source: Dr. Volkmar Hable, vh@samarium.ca

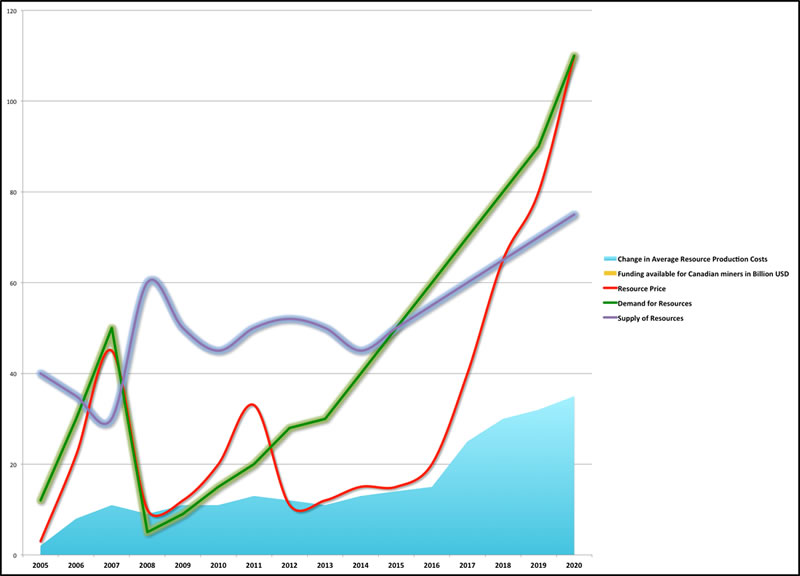

The weighted principal hard factors determining the funding available to Canadian miners until 2020, adjusted for inflation.

Graph by Dr. Volkmar Hable, vh@samarium.ca

As can be seen in the chart above, it is not so much the supply but rather varying demand that influences the resource prices. A typical hallmark of a market that is increasingly influenced by scarcity. We can safely assume significantly higher resource prices in the years to come, which is good news for Canadian miners. As a side note: while I have been focusing on Canadian miners in my analysis, we can extrapolate this forecast to the rest of the mining world without the fear for deviations. Canada’s miners are a mirror image of the world.

Dr. Volkmar Hable

vh@samarium.ca

Dr. Volkmar Hable is a geologist and physicist by training, he holds a Ph.D. in geosciences and a B.Sc. in Agriculture and Agronomics among other, and is fluent in English, French, Spanish, and German. He was CEO CEN-European operations of Fortune 500 company Adecco, manager of a Swiss hedge fund for 7 years and has spent a year in the Diplomatic Corps. He currently is a member of the in British-Columbia accredited Consular Corps, a director and fund advisor of Samarium Investment Corporation and CEO of Samarium Borealis Corporation.

© 2014 Copyright Dr. Volkmar Hable - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.