Home Ownership Debt, Mortgages, Slavery and the Risk of Ruin

Housing-Market / Mortgages May 30, 2014 - 10:47 AM GMTBy: Nadeem_Walayat

Britain has a debt based economy where expanding total debt is the primary enabler for the economy to expand and that is the primary purpose of the Bank of England to enable governments to expand total debt be it public or private. However, following the credit crisis collapse of 2007-2009, individuals and banks become reluctant to borrow despite record low interest rates and hence why despite successive Governments (Labour and Coalition) having gone on a relentless spending binge to the tune of £750 billion of new debt the economy stagnated due to the failure to ignite a borrowing frenzy amongst Britain's working population.

Britain has a debt based economy where expanding total debt is the primary enabler for the economy to expand and that is the primary purpose of the Bank of England to enable governments to expand total debt be it public or private. However, following the credit crisis collapse of 2007-2009, individuals and banks become reluctant to borrow despite record low interest rates and hence why despite successive Governments (Labour and Coalition) having gone on a relentless spending binge to the tune of £750 billion of new debt the economy stagnated due to the failure to ignite a borrowing frenzy amongst Britain's working population.

However, as house price rises continue to accelerate, many people sat on the sidelines waiting for prices to fall or even crash will realise that it is just not going to happen, and in their despair at the relentless accelerating trend of rising prices, in increasing numbers will feel no choice but to jump onboard the property ladder as a they see the houses they have been viewing for many months being sold and asking prices trending ever higher.

However, as house price rises continue to accelerate, many people sat on the sidelines waiting for prices to fall or even crash will realise that it is just not going to happen, and in their despair at the relentless accelerating trend of rising prices, in increasing numbers will feel no choice but to jump onboard the property ladder as a they see the houses they have been viewing for many months being sold and asking prices trending ever higher.

In this respect the government has been bending over backwards to encourage people to take on debt the most notable of which during 2013 was the extension of the Help to Buy Scheme to all home buyers which was brought forward to the 1st of October 2013, and thus enabling the purchase of properties upto the value of £600,000 with just 5% deposits, i.e. an home buyer today only needs a £30k cash deposit to buy a £600k property, whereas before the scheme banks would have required a £125k deposit.

As you read this more and more home owners are being successfully conditioned to ignore the significance of the debt they are taking on as they become more and more fixated on house prices rising every month by £x thousands of pounds in value, far in excess of their monthly mortgage payments and in many cases approaching their monthly salaries, this acts as huge encouragement to not only to borrow to buy properties but also to save less and borrow for consumption which will meet the governments primary objective for inflating the economy by means of the housing market. Everyone will soon be playing the game of how much has the value of my home increased by, many if not most will be regular visitors to websites such as Zoopla to see how much their properties have increased by.

Mortgage Debt and the Risk of Ruin

The encouragement to load up on debt by various means such as Equity Release is once more being programmed into the psyche of home owners as they perceive this as a means of capitalising on the nominal increase in the value of their homes.

In life I meet many people who have no concept of their risk of ruin, but instead are fully aware of for instance the equity in their property. For example one person I met wanted my advice as they were contemplating releasing £100k of equity in their property on top of a £200k existing mortgage so that they could extend their property against a perceived existing property value of approx £350k.

What I attempted to point out to the person was their failure to comprehend that the more debt one accumulates then their risk of ruin becomes exponentially greater, because the debt becomes exponentially harder to service out of marginal income, i.e. a graph of debt to income would be logarithmic in terms of the risk of ruin. In this example the first £10k of mortgage debt would have a far smaller risk of ruin then adding an extra £10k to the total i.e. £200k +£10k. Where the extra £10k could be the tipping point that results in the loss of their property, never mind if they went ahead and borrowed an extra £100k! The whole debt crisis in terms of impact on home owners has it's basis in the failure of individuals to be conscious of their risk of ruin as they fell for the equity release sales pitches form the mortgage banks. This is precisely how the big banks blew-up, because they ignored their risk of ruin because they were too interested in hiding losses (mark to market) to bank bonuses on the basis of fictitious profits.

Again do not fall for the trap of perceiving the rise in house prices as means of realising capital or equity for consumption because you are just being deluded into SPENDING BORROWED money. Where the delusion is that the borrowers do not perceive it as an INCREASE in debt but instead a release of equity!

The TRUTH is that rising house prices in reality do not MAKE people richer, but instead more susceptible to BORROWING MORE Money for CONSUMPTION as people delude themselves that they can somehow spend money against a rise in house prices, but the reality is that they will service the NEW debt through FUTURE WAGES and nothing that is linked to the actual rise in the value of their homes because to benefit from a rise in house prices they would need to realise it by either selling or generating an INCOME from the rise in house prices! i.e. by renting out their home or rooms so that it wholly covers the interest payable on the NEW debt and thus the income would need to be at a constant yield to rising house prices. That is how an home owner benefits from rising house prices and NOT by means of equity release for consumption.

If you want to have near zero risk of ruin then you really have to have no debt. However that is just not possible for 1/2 of home owners / buyers which means that you need exert strict discipline in regard to how much debt you are willing to take on that in my opinion should never exceed more than 75% LTV (loan to value).

Debt is Slavery

Debt IS from cradle to grave slavery. Not just for individuals but whole nations are turned into debt slaves by corrupt politicians whose ONLY objective is to bribe voters with borrowed money to get elected and then line their pockets. The consequences of bribing voters with borrowed money is INFLATION. After all there is no free lunch, the price paid for printing debt is loss of purchasing power for ALL fiat currencies.

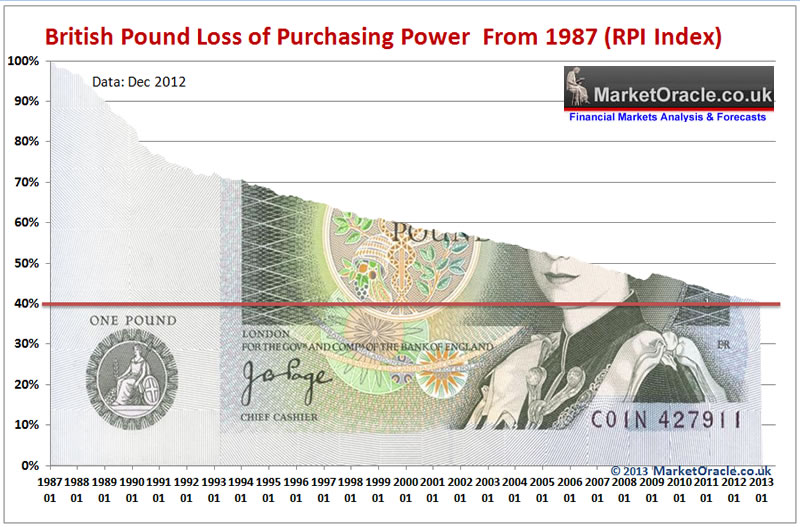

As an example today's pound in your pocket on the basis of RPI is worth less than 40% of its value of 25 years ago.

Which means that on average the same types of goods and services cost 2.5X more today then they did in 1988.

The people of all western nations, even those that personally do not have any debt are still debt slaves because they pay for the consequences of government money and debt printing fraud that buy votes through government deficit spending to finance public sector jobs, services and benefits that the country has no money to pay for and as a consequence of the election cycle these deficits are in perpetuity i.e. the politicians ALWAYS need to bribe the electorate which means that contrary to the PROPAGANDA that silver tongued politicians are so expert in stating, the DEBT IS NEVER REPAID, instead it will expand EXPONENTIALLY IN PERPETUITY

Today we hear a lot of discussion in the mainstream propaganda media of a currency war. Know this that there IS NO CURRENCY WAR, as I have voiced for well over 5 years now and as illustrated by the Inflation Mega-trend ebook of Jan 2010. If there is a war than it is one of INFLATION and its consequences of stealth theft of purchasing power because ALL CURRENCIES are in a state of perpetual free fall against one another.

To limit ones exposure to debt slavery one needs to immunise one self form the Debt based system which is by NOT BORROWING MONEY! This is easier said then done because we are literally bombarded with propaganda from an early age that seeks to brainwash us into becoming debt slaves.

- Do not use credit cards if you are unable to pay off the whole balance each month.

- Do no buy anything with debt money, especially junk chinese consumer goods which amount to nothing more than the transfer of Jobs from the West to the East.

- If you have any assets purchased with debt money then liquidate / sell them and pay down the debt because these assets will likely quickly lose their value over time i.e. such as car.

Yes, I fully understand it is difficult to counter cradle to grave brainwashing to become debt slaves, but do the sums and you will see that you will end up spending approx 1/3rd of your working life servicing your debts. You have effectively given away 1/3rd of your working life to the bankster elite. And this is not a casual relationship with your debt master but one of constantly finding yourself anxious if you are unable to meet the strict deadlines for servicing debt repayments that your debt master imposes on you, including making you homeless so to effectively have lost EVERYTHING you have worked hard for your whole life.

You only have a limited amount of time, i.e. say 45 years max of productive working life, do you want to give up 15 years of your most productive years in exchange for a garage full of chinese junk?

The bottom line is that if you cannot afford to buy it from earnings or savings then don't buy it!

The Circle of Slavery - Past, Present and Future

The reason why debt slavery is so seductive is because if offers instant gratification, flat screen tv, car, house in a near instance, because we all have at the back of our minds that our Time on Earth is LIMITED, we only have a short lease on life and so our natural state is highly conducive towards becoming debt slaves.

Debt slavery is another manifestation of the theft of our future, it is nothing new just the latest device to steal ones life because for eons humans have been successfully conditioned to give up control over their lives on the basis of ancient myths being utilised to make promises of how you will only really beginning to live AFTER they die in exchange for your PRESENT LIFE.

Debt slavery - Sell your future for an instant gratification in the present.

Religious slavery - Sell your future because you will only really begin to live after you die.

Instead, as I have written in countless articles (see archive) the answer is to focus on the PRESENT. For it is ones actions in the present that determine the future.

Debt Free Freedom?

The solution is not to BORROW MONEY!

I fully understand that is is very, very difficult for people who have been brainwashed to be able to consider this, but I assure you, not handing over approx 1/3rd of your earnings towards the elite's debt servicing will result in a far more prosperous and stress free life and all you need to do to overcome your programming is exert some self confidence in respect of the tendency towards instant gratification because usually working towards a goal is far more rewarding than actually achieving the goal and the worst thing people can do is to achieve goals without work, which is a recipe for personal disaster which is what debt slavery entails.

Labour, Liberal, Conservative, or SNP it does not matter they are ALL party to the debt slavery system that they operate from local councils right through to national governments. So the likes of the SNP propagandising the Scottish Referendum as a freedom movement is a red herring, as there is no freedom for the Scottish people but a means for the Scottish Bankster's and Elite to be able to implement more locally targeted mechanism to enslave the Scottish people by means of debt.

What the people of Britain need is an alternative system to the debt and tax slavery system that funnels wealth to the bankster elite, the starting point for such a system would have ZERO taxation and NO debt industry, which means that the unproductive bloated public sectors would not exist and the governments would not have the means to bribe voters with nor would the banking elite have the means of conjuring money out of thin air which they lend to debt slaves to work to service their whole lives, otherwise your children and grand children will continue to born into a debt and tax based slavery system.

In our society the worst place for ordinary people to be is in debt, for you risk ruining the rest of your lives as being in debt either by design or chance (parking fines etc) can soon spiral out of control. Therefore people need mechanisms to first avoid getting into debt and then the consequences of official charges, penalties and fees from spiraling out of control.

The bottom line is that one needs to work hard to achieve and maintain ones freedom in today's western debt based societies where the young adults are exposed to intense propaganda aimed at turning them into life-long debt slaves such as via the Universities which for approx 75% of students are in my opinion a SCAM because they will still end up flipping burgers or stacking shelves, only after the scamming universities have fleeced them out of approaching £50,000.

House Price Inflation is the Ultimate Mechanism for Slavery

In my opinion virtually all of us have been successfully brainwashed / conditioned to become slaves of the elite by means debt slavery, the primary mechanism for control preys on our natural instinct for a secure shelter / home that we can only achieve by means of saddling ourselves up with a mountain of debt.

Our current system of housing market debt slavery is by design for if successive governments had favoured independence and freedom then they would not have sold off 60% of the social housing stock.

As mentioned earlier governments inflate house prices to give the illusion of an increase in wealth which encourages more debt funded consumption against the rise in house prices and perceived increase in wealth.

All of this despite the simple fact that house price inflation ONLY benefits the wealthy.

For instance ordinary people buy a house for say £150k, it inflates in price by say 25%, thus ordinary people feel £37.5k richer which encourages debt fuelled consumption against this rise in house prices. But are people really £37.5k richer ?

Do the maths, now what is the value of your next target home ? What was it £250k, But that will also have gone by about 25% (probably more) so it will now be priced at £312.5k or have increased by £62.5k against your property which will have increased by £37.5k this leaving you £25k WORSE OFF than if house prices had NOT risen and there in lies the beauty of the house price inflation scam, for the masses have been successfully conditioned by the media / system to see house price inflation as being great ! But in reality it only really benefits the elite who's £1 million+ mansions are LEVERAGED to average house prices, for instance a £2million home would have increased by say 50% in price to now stand at £4 million, so whilst you have gained £25k the elite has gained £2 million ! Proportionately the elite has made 80X what you have made and thus putting you exponentially further away from where the elite was before i.e. your £150k property was 7.5% of the elites mansion but now your £187.5k mansion is only 4.7% of what the elites property is worth therefore in effect house price inflation acts as one of the primary mechanisms for the transfer of wealth from the workers to the elite.

Off course it is extremely hard for conditioned slaves to break their masters bonds especially given such an ingenious system of house price inflation wealth transfer mechanism. So I am not expect 99% of the people reading this to be able to break these systemic bonds as you will all still desire to partake in the house price inflation debt slavery system no matter what facts are presented to illustrate that at the end of the day only the wealthy win and the more wealthy the person then the greater will be the increase in wealth as the curve is exponential. So I am just letting you know the primary reason for why we have perpetual house prices inflation is so as to enable the elite to own virtually everything in the long run until either there is a revolution or a the government steals from the rich to bribe the poor to vote for them, but even then the elite are a bunch of crafty buggers as they always know a way out so the theft is usually from the middle classes rather than those with real wealth.

Today the only people who are free are those who do not work in service of their debt masters because most of us remain convinced that we must borrow money to the maximum extent to be able to buy a house, for that is how we are controlled for the duration of our adult lives, from student debts, to consumption debts to housing debts, to retirement residency debts, for that is how the elite increases its wealth, where not even an economic depression halts the accumulation of wealth amongst the elite, instead the percentage of wages siphoned off by a myriad of methods such as inflation increases, hence the cost of living crisis.

The Real Secret to Financial Success

In my experience the real secret of financial success is...... continues in the New UK Housing Market Ebook available for FREE DOWNLOAD (only requirement is a valid email address).

New Housing Market Ebook - FREE DOWNLOAD

New Housing Market Ebook - FREE DOWNLOAD

The housing market ebook of over 300 pages comprises four main parts :

1. U.S. Housing Market Analysis and Trend Forecast 2013-2016 - 27 pages

The US housing market analysis and concluding trend forecast at the start of 2013 acted as a good lead exercise for the subsequent more in-depth analysis of the UK housing market.

2. U.K. Housing Market Analysis and House Prices Forecast 2014-2018 - 107 pages

The second part comprises the bulk of analysis that concludes in several detailed trend forecasts including that for UK house prices from 2014 to 2018 and their implications for the outcome of the next General Election (May 2015) as well as the Scottish Referendum.

3. Housing Market Guides - 138 Pages

Over 1/3rd of the ebook comprises of extensive guides that cover virtually every aspect of the process of buying, selling and owning properties, including many value increasing home improvements continuing on in how to save on running and repair costs with timely maintenance tasks and even guides on which value losing home improvements should be avoided.

- What Can You Afford to Buy?

- Home Buyers Guide

- Home Sellers Guide

- Top 15 Value Increasing Home Improvements

- Home Improvements to Avoid

- Home Winter Weather Proofing 22 Point Survey

These guides will further be supplemented from Mid 2014 onwards by a series of online videos and regularly updated calculators such as the Home Buying Profit and Loss Calculator, which will seek to give calculations on whether to buy or rent based on personal individual circumstances, that will be updated to include the latest expected trend trajectories for future house price inflation i.e. you will have your own personal house price forecast.

4. Historic Analysis 2007 to 2012 - 40 pages

A selection of 10 historic articles of analysis to illustrate the process of analysis during key stages of the housing markets trend from the euphoric bubble high, to a state of denial as house prices entered a literal free fall, to the depths of depression and then emergence of the embryonic bull market during 2012 that gave birth to the bull market proper of 2013.

FREE DOWNLOAD (Only requirement is a valid email address)

Source and comments: http://www.marketoracle.co.uk/Article45833.html

By Nadeem Walayat

Copyright © 2005-2014 Marketoracle.co.uk (Market Oracle Ltd). All rights reserved.

Nadeem Walayat has over 25 years experience of trading derivatives, portfolio management and analysing the financial markets, including one of few who both anticipated and Beat the 1987 Crash. Nadeem's forward looking analysis focuses on UK inflation, economy, interest rates and housing market. He is the author of five ebook's in the The Inflation Mega-Trend and Stocks Stealth Bull Market series that can be downloaded for Free.

Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication that presents in-depth analysis from over 1000 experienced analysts on a range of views of the probable direction of the financial markets, thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication that presents in-depth analysis from over 1000 experienced analysts on a range of views of the probable direction of the financial markets, thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Nadeem Walayat Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.