U.S. Unfunded Liabilities The Coming Big Squeeze on Your Wallet

Politics / Government Spending Nov 05, 2013 - 03:01 PM GMTBy: Don_Miller

As the politicos in Washington continue to move the deck chairs around on the Titanic, ignoring the monster iceberg in plain sight, I'm keeping my eyes wide open. Here are a few tidbits from a recently published Social Security Administration factsheet:

As the politicos in Washington continue to move the deck chairs around on the Titanic, ignoring the monster iceberg in plain sight, I'm keeping my eyes wide open. Here are a few tidbits from a recently published Social Security Administration factsheet:

- An estimated 161 million workers—94% of all workers—are covered under Social Security.

- In 1940, the life expectancy of a 65-year-old was almost 14 years; today it is more than 20 years.

- By 2033, the number of older Americans will increase from 45.1 million today to 77.4 million.

- There are currently 2.8 workers for each Social Security beneficiary. By 2033, there will be 2.1 workers for each beneficiary.

We can forget about the trust fund when the cupboard is bare. Right now, today, the government collects Social Security taxes from the work force. From those receipts, it pays out Social Security benefits. In 2010 the Congressional Budget Office announced, "[T]he system will pay out more in benefits than it receives in payroll taxes, an important threshold it was not expected to cross until at least 2016." Baby boomers will retire at a rate of 10,000 per day for the next 19 years, and the gap between Social Security tax revenue and expenditures will grow with each passing day.

Social Security is just the tip of the iceberg. In 2011 USA Today pegged the US government's unfunded liabilities at $61.6 trillion. That's $528,000 per household. I doubt most Americans, regardless of their age, have a spare half million to bail out the government. All the wealth of the Warren Buffetts and Oprah Winfreys of our country wouldn't even make a dent.

The rest of the world knows what's going on. Historically, other countries have lent us the money to help pay our bills. Keeping our economy in spending mode helped them sell exports to the US and create jobs. That lending is slowing down radically as the world grows concerned about the US government's ability to pay its bills.

In January, CNS news gave us a pretty shabby report card:

"[T]he Federal Reserve revealed that its holdings of U.S. government debt had increased to an all-time record of $1,696,691,000,000 as of the close of business on Wednesday. The Fed's holdings of U.S. government debt have increased by 257 percent since … Jan. 20, 2009, and the Fed is currently the single largest holder of U.S. government debt."

If other countries won't lend us money and our tax revenue is not enough to cover expenses, the Federal Reserve will just keep creating money without much more than a simple accounting entry.

What comes next? You have all heard pundits predict a crash or talk about unsustainable debt. What does that really mean? First, folks depending on the government for income or benefits will take a huge hit. Many Generation Xers (wisely) assume Social Security won't even be around when they reach retirement age. Any help they get from the government will be icing on the cake. They know the system is unsustainable.

And while the Federal Reserve continues to create money out of thin air, Social Security gets clobbered, and expenses will continue to rise—rapidly. I asked Terry Coxon, a senior economist at Casey Research, what will happen when people catch on. He explained:

"When price inflation starts to become obvious, more and more people will behave as though they are playing a game of Old Maid. They'll try to get rid of depreciating dollars. And that effort—to get rid of dollars before they lose even more value—will make inflation even worse. The players who diversified out of dollars early will win the game."

Seniors and savers are particularly vulnerable during periods of high inflation. They worked hard, saved their money, and need it to last. But if their nest eggs are denominated in a rapidly inflating currency, their buying power could vanish virtually overnight. And as their nest eggs shrink, Social Security, food stamps, and government benefits will buy fewer goods and services to boot.

This is no accident, folks. Governments hopelessly in debt create inflation so they can pay their obligations with depreciated currency units.

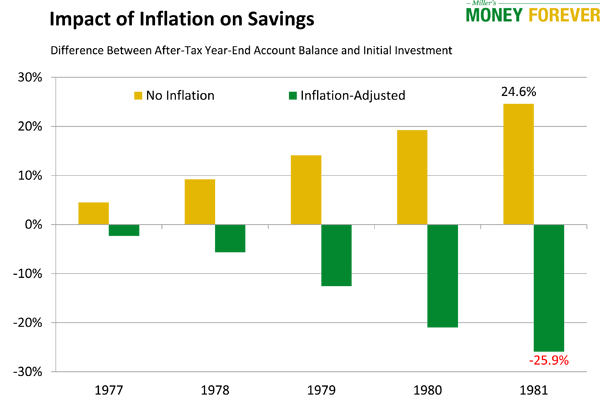

The big squeeze is coming. It will trap us between rising costs and withering incomes. Carter-era inflation is the closest most Americans have come to what lies ahead. Let me refresh your memory.

- 1977—6.5% inflation

- 1978—7.6% inflation

- 1979—11.3% inflation

- 1980—13.5% inflation

- 1981—10.3% inflation

It wasn't pretty. Imagine you bought a $100,000, five-year certificate of deposit on January 1, 1977. The interest rate for the CD was 6%, paid annually, and you were in the 25% income tax bracket. At the end of five years, assuming you reinvested your after-tax interest income, you would have received $24,600 plus your initial $100,000 investment. Would you have been any better off? No.

Your net return adjusted for inflation would have been $74,100. That's a 25.9% decline in purchasing power. Inflation would have reduced your net worth by the cost of a well-equipped, mid-size automobile.

Inflation can devastate our standard of living. We know prices are going up. Money doesn't seem to go as far, but it's tough to calculate the decline. Still, we know we need to do something.

How can we protect ourselves? Holding assets that historically retain their value is a good start. Gold and precious metals are a prime example. Those who specialize in precious metals like to point out that gold is not getting more expensive; our currency is just losing its value.

Farmland and foreign currencies in countries that are not papering over their debt are also viable sources of protection.

Money Forever subscribers know that we subject our portfolio investments to a Five-Point Balancing Test. Number 4 is: "Does it protect against inflation?" In part, that means investing in companies with a large international base. There are many foreign companies that trade in the US market, and we keep our eyes peeled for the best among them.

When a currency experiences high inflation, no one wants it. In our lifetimes the currencies of Argentina, Brazil, Mexico, and Zimbabwe have become totally worthless. Those who followed Terry's advice and got out of those currencies early kept a much larger portion of their wealth.

When ultra-high inflation arrives, desperate governments will do anything to protect themselves. Instituting currency controls that make it difficult, if not impossible, for their citizens to dump a quickly depreciating currency is one of their favorite moves. By then it may be too late to protect ourselves.

The time to discard your Old Maid card and pick up inflation protection opportunities is now. When it comes to protecting your life savings, it is far better to take precautionary steps a year early than one day too late. If you'd like access to inflation-protecting investments specifically curated for seniors and savers, click here to become a Money Forever subscriber today.

© 2013 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.