Insurance Companies Profit from Obamacare

Politics / US Politics Oct 30, 2013 - 11:19 AM GMTBy: BATR

No one can reasonably deny that the major Insurance Companies were the driving force behind the writing of the Affordable Care Act legislation. "The health care industry spent nearly $500 million lobbying for health care issues in 2012, and $243 million so far in 2013." Obamacare or Corporate-care: The Writing of the Affordable Care Act, sums up the process.

No one can reasonably deny that the major Insurance Companies were the driving force behind the writing of the Affordable Care Act legislation. "The health care industry spent nearly $500 million lobbying for health care issues in 2012, and $243 million so far in 2013." Obamacare or Corporate-care: The Writing of the Affordable Care Act, sums up the process.

"Essentially, the ACA was designed to write the for-profit health care system into law, increase corporate profits, and to discourage people from demanding a health care system that would actually provide real health care coverage for all. The ACA wasn’t written to fix a broken system – it was written to ensure that the broken system would be kept in place. After all, from the standpoint of the health care industry, the system is working just fine for their profits."

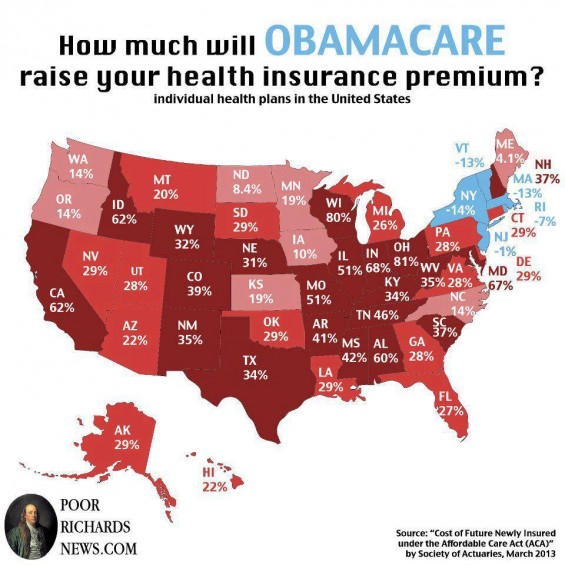

Since the public insurance providers are enjoying a jump in their stock values and a protected rise in premiums, the normal conclusion is that Obamacare is the big winner in the socialization of medicine. Before going any further, The Health Care Blog raises a curious issues regarding Obamacare in the article, Does Obamacare Limit Profits for Health Insurance Companies in Your State?

"The ACA imposes a minimum medical loss ratio (MLR) on all insurers. The MLR is the amount of money spent on covered person medical care divided by the total revenue received through premiums.

The ACA requires health insurers in the individual and small group market to spend 80 percent of their premiums (after subtracting taxes and regulatory fees) on medical costs. The corresponding figure for large groups is 85 percent.

Even though the MLR is a national law, it may not apply in your state. Why? Because many States are petitioning for a waiver.

Why did these States receive waivers? For a variety of reasons, but one of the reasons is due to the fact that some states have a less competitive medical market. Maine, for instance, requested a MLR of 65%. The reason was that State only has two large commercial insurers, Anthem Blue Cross Blue Shield (with 49% of the market) and MEGA Life and Health Insurance Company (with 33% of the market)."

Now put this argument into a proper perspective. WHY should insurance companies profit at all, and WHY is it necessary for private companies to issue insurance for medical coverage to begin with?

Readers of Negotium know this series advocates free enterprise economics. However, the mandate requirements in Obamacare are nothing more than a guarantee for insurance companies to terminate current catastrophic coverage and offer highly expensive policies that include unnecessary treatment.

With this reality in mind, as the horror reports come in daily, sticker shock is forcing Middle America into untenable decisions. Add the practice of reducing employment to part time status and that train wreck is becoming more like the black plague.

The medical care alternative is not universal Medicaid for an impoverished population. However, the article Rush on Medicaid could spell trouble for ObamaCare’s health, cites "The Democrat and Chronicle newspaper reports that in New York, nearly 24,000 of the 37,000 newly enrolled residents are going into Medicaid, which millions of New Yorkers are already on. Just 13,313 chose private plans."Such blowback dooms the failed experiment. When your heart stops pumping, a bypass will not work. It is time to look for a transplant.

One such option outlined in the essay, Could nonprofit health insurance plans be the real reformers?, is a viable alternative would be the fostering of nonprofit health insurance CO-OPs (Consumer Oriented and Operated Plans) throughout the country.The Affordable Care Act might even facilitate a medical graft.

"They could even hasten the day when the big investor-owned corporations cede the marketplace to nonprofits and move on to other ways of earning a profit.

The reform law provides a total of $3.4 billion in loans for local groups that meet high eligibility criteria, so several more prospective CO-OPs will be selected in the months ahead. We’re not talking about grants here. The start-up money must be repaid to the government — with interest. All of the CO-OPs will have to offer coverage through the Internet-based marketplaces (exchanges) the reform law requires states to establish by January 1, 2014.

If all goes as planned, every state will have at least one CO-OP. And there are reports that at least one plan already has negotiated a good rate with local hospitals by explaining how CO-OPs can help them reduce the amount of uncompensated care they incur every year by treating uninsured patients."

In the real world, the lobbyists for the mega corporatists own the politicians. In spite of this influence, the uproar of the citizenry is building, by the fallout from the Obamacare weapon of mass destruction. The normal fallout shelters for the careerists "pols" will not protect them from the wrath of a sickly public, who cannot afford medical coverage.

Add to this diagnosis, Obamacare Causes Doctor to Retire."The Deloitte Center for Health Solutions survey of more than 600 physicians, which found "Six in 10 physicians (62 percent) said it is likely many of their colleagues will retire earlier than planned in the next one to three years."

The prescription for a long-term solution is to promote alternative medicine that reduces a damaging dependency on pharmaceutical drugs. The side effect disclaimers need to extend to the practice of medicine itself. Excluding homoeopathy alternatives coverage from patient’s choice only perpetuates the for profit hospital model. Charity medicine, now viewed with the same disdain as bloodletting, by the medical establishment, is a prime causality of the Obamacare. The lobotomy culture never will cure the mental illness of the eugenics cult.

Insurance companies will play divine with their clout of who qualifies for payment of treatment. In an interview, The God Factor Interview, Obama states: "If there’s a senior citizen in downstate Illinois that’s struggling to pay for their medicine and having to chose between medicine and the rent, that makes my life poorer even if it’s not my grandparent." Well, your health insurance donors will not suffer, only the rest of us.

James Hall – October 30, 2013

Source : http://www.batr.org/negotium/103013.html

Discuss or comment about this essay on the BATR Forum

"Many seek to become a Syndicated Columnist, while the few strive to be a Vindicated Publisher"

© 2013 Copyright BATR - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors

BATR Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.